SMR Data Center Strategy, Switch’s 13 MW Ormat PPA, Google’s 150 MW Deal, and 25 SMR Applications (2021 to 2026)

Grid Constraints Drive Data Center On-Site Power Projects

Data center operators are fundamentally shifting their energy procurement strategy from intermittent renewable power purchase agreements (PPAs) to the direct acquisition of firm, 24/7 clean power sources like geothermal and nuclear. This strategic pivot is a direct response to the dual pressures of explosive AI-driven electricity demand and increasingly congested public grids, which can have interconnection queues stretching up to eight years. By developing power generation on-site or through direct agreements, operators are bypassing these critical infrastructure bottlenecks to secure the reliable, baseload energy required for mission-critical digital infrastructure.

- Between 2021 and 2024, the primary challenge was the identification of scalable, reliable power to meet surging demand, with data center electricity consumption projected to nearly double to 530 TWh by 2028. While interest in advanced clean energy grew, procurement was still dominated by solar and wind PPAs, whose intermittency proved a liability for 24/7 operations.

- The period from 2025 to today marks the execution phase, where strategy has translated into commercial agreements. In January 2026, Switch signed a 20-year, 13 MW geothermal PPA with Ormat Technologies, followed by Google‘s larger 150 MW geothermal deal with Ormat in February 2026, confirming a definitive trend toward securing firm, carbon-free power.

- This strategic shift is not limited to geothermal. Microsoft secured a nuclear PPA with Constellation Energy in August 2025, while ENTRA 1 and the Tennessee Valley Authority (TVA) partnered to deploy Nu Scale Power‘s SMR technology, demonstrating a diversified industry-wide movement to co-locate firm power generation with data center loads.

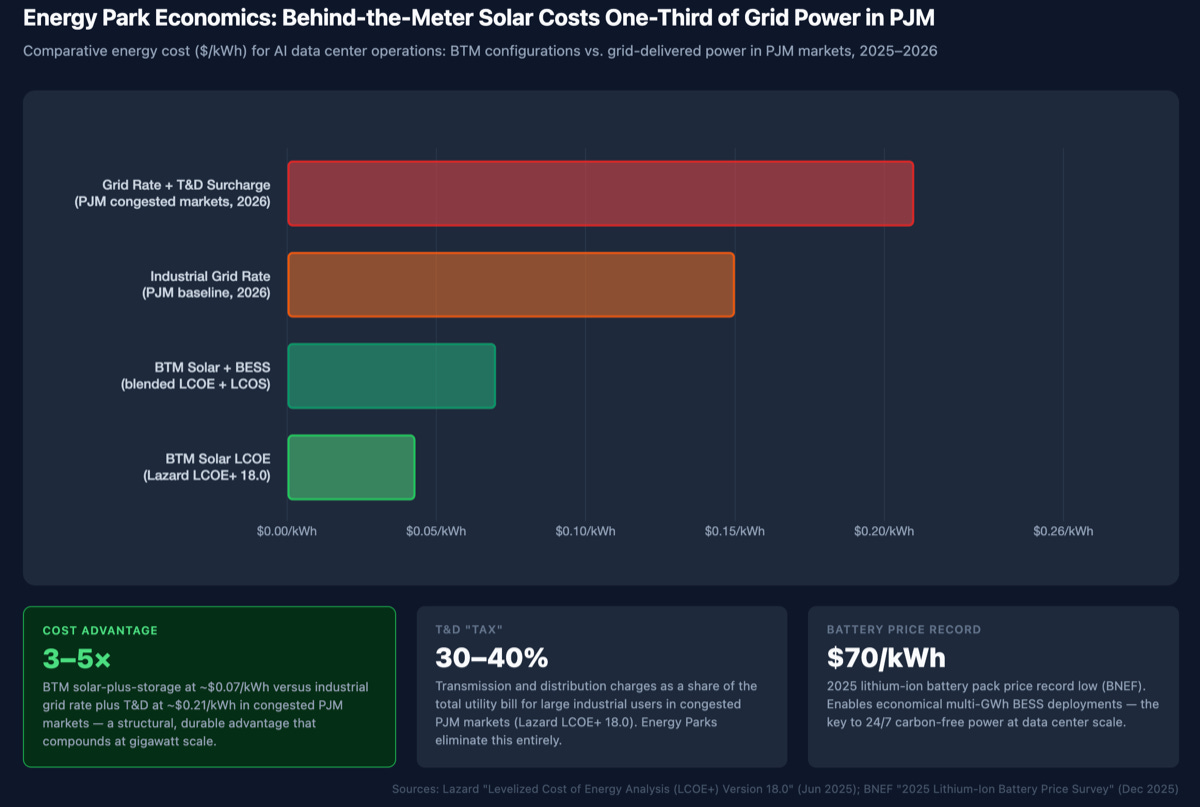

On-Site Power Offers Major Data Center Cost Savings

This chart directly illustrates the economic driver for moving to on-site power, showing it can be significantly cheaper than sourcing electricity from a congested grid.

(Source: Energy Industry Insights from Avanza Energy – Substack)

$10 B in Commitments, Data Center Nuclear Investment Accelerates

Major technology companies are directing billions in capital toward advanced nuclear and geothermal technologies, signaling a long-term strategic investment in securing baseload power independent of the grid. These financial commitments, bolstered by significant government incentives, are de-risking first-of-a-kind projects and creating a bankable path for technologies essential for powering the AI economy. This trend reflects a calculated decision to internalize energy supply chains to ensure reliability and cost predictability.

Hyperscalers Commit Billions to Secure Clean Power

The chart details multi-billion dollar investments by major tech companies in nuclear and other firm power sources, directly supporting the section’s focus on accelerating capital commitments.

(Source: Energy Industry Insights from Avanza Energy – Substack)

- Hyperscalers are leading the investment charge, with Amazon and Google collectively committing over $10 billion to advanced nuclear partnerships. This level of private capital injection validates the technology’s strategic importance for meeting future energy needs.

- Government support is a critical enabler. The Inflation Reduction Act’s technology-neutral tax credits and the Department of Energy’s programs provide crucial financial backstops, including a 30% Investment Tax Credit (ITC) for geothermal and nuclear projects.

- The global Small Modular Reactor (SMR) market is forecast to grow to $7.14 billion by 2030. This growth is underpinned by data center demand and the pursuit of energy security, creating a clear market signal for SMR developers and their supply chains.

Table: Data Center Clean Energy Investments and Commitments

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google / Kairos Power | Oct 2024 | Agreement to purchase power from a fleet of mini nuclear reactors, marking a first-mover commitment to advanced nuclear to power AI datacenters. | The Guardian |

| Microsoft / SMR Exploration | Oct 2024 | Investigating the use of next-generation reactors to power its data centers, supported by a $900 M DOE fund to spur SMR deployment. | POWER Magazine |

| Meta / Sage Geosystems | Sep 2024 | Agreement to procure 150 MW of geothermal power for data centers, with operations planned to start in 2027. | Virginia Mercury |

Switch Data Centers 2 Firm Power Partnerships, Ormat and SMRs (2021 to 2026)

Strategic partnerships between data center operators and developers of firm clean power technologies are now the primary mechanism for acquiring 24/7 carbon-free energy. These collaborations are moving beyond simple PPA offtakes to encompass joint development, technology validation, and long-term energy planning. This model allows data center operators to secure power capacity years in advance while providing developers with the bankable, long-term contracts needed to finance capital-intensive projects.

- The January 2026 PPA between Switch and Ormat Technologies for 13 MW of geothermal power is a landmark deal, representing Ormat‘s first direct agreement with a data center operator and securing baseload power for Switch‘s Nevada campuses starting in 2030.

- This trend was reinforced when Google signed a significantly larger portfolio PPA with Ormat in February 2026 for up to 150 MW of new geothermal capacity, also in Nevada, demonstrating a scalable and repeatable partnership model.

- The market is diversifying its firm power sources, as shown by Microsoft‘s August 2025 agreement with Constellation Energy to purchase power from a restarted portion of the Three Mile Island nuclear plant, tapping into existing nuclear assets for immediate baseload capacity.

- Forward-looking partnerships are also solidifying for next-generation nuclear, with ENTRA 1 and TVA‘s January 2026 agreement to deploy up to 6 GW of nuclear capacity using Nu Scale Power‘s SMR technology, directly targeting future data center demand.

Table: Key Data Center Firm Power Partnerships (2025 – 2026)

| Data Center Operator | Power Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|---|

| Ormat Technologies | Feb 2026 | Portfolio PPA for up to 150 MW of new geothermal power to supply data centers in Nevada, enabling 24/7 carbon-free energy goals. | Ormat Technologies | |

| Switch | Ormat Technologies | Jan 2026 | 20-year PPA for approximately 13 MW of baseload geothermal capacity from the Salt Wells plant to power Nevada data centers. | Ormat Technologies |

| ENTRA 1 (for data centers) | TVA / Nu Scale Power | Jan 2026 | Agreement with TVA to deploy up to 6 GW of nuclear capacity using Nu Scale Power‘s SMR technology to meet future data center demand. | Yahoo Finance |

| Microsoft | Constellation Energy | Aug 2025 | 20-year PPA to purchase energy from a restarted portion of the Three Mile Island nuclear plant, securing baseload carbon-free power. | AFIRE |

US West Focus, Data Center Firm Power in Nevada

The development of firm, clean power for data centers is geographically concentrated in regions with favorable geology for geothermal energy and a clear regulatory path for development. The U.S. West, particularly Nevada, has emerged as the primary hub for these projects, driven by its abundant geothermal resources and established data center presence. This geographic clustering allows for the creation of localized energy ecosystems that can support multiple hyperscale facilities.

- Between 2021 and 2024, data center site selection was primarily driven by proximity to fiber networks and existing grid substations. While renewable PPAs were signed across the country, the power was often wheeled across long distances, disconnected from the physical location of the data center.

- From 2025 onward, the focus has sharpened on co-locating generation with load. Nevada is the epicenter of this trend, hosting the recent geothermal PPAs for both Switch and Google with Ormat. The state’s rich geothermal potential makes it a natural fit for this strategy.

- While other data center hubs like Virginia are exploring their geothermal potential, Nevada‘s recent commercial agreements provide a tangible blueprint for other states to follow. The success of these projects will likely spur similar developments in other geologically favorable regions.

- The geographic footprint for SMRs is less defined but is beginning to take shape. The partnership between TVA and ENTRA 1 to deploy Nu Scale reactors points to the Southeast as a key future region for nuclear-powered data centers, leveraging the utility’s nuclear expertise and existing sites.

SMR Commercialization, 25 NRC Applications Expected by 2029

While conventional geothermal power is a mature and bankable technology, the data center industry’s long-term energy strategy relies on the parallel advancement of next-generation Enhanced Geothermal Systems (EGS) and the successful commercialization of SMRs. The industry is actively underwriting the maturation of these technologies, recognizing that both are required to meet the exponential growth in power demand projected through the next decade.

- Conventional geothermal, as used in the Ormat deals, offers a proven, high-capacity factor (>90%) solution today. The next frontier is EGS, which is projected to achieve a highly competitive Levelized Cost of Energy (LCOE) of $45/MWh by 2035 and could unlock geothermal resources nationwide.

- Between 2021 and 2024, SMRs were largely in the design and certification phase, with Nu Scale achieving a major milestone but commercial projects facing economic headwinds.

- The period from 2025 has shown tangible progress toward commercialization, highlighted by the U.S. Nuclear Regulatory Commission (NRC) expecting to receive 25 licensing applications for SMRs and advanced reactors by 2029. This signals a robust pipeline of projects moving toward deployment.

- The primary remaining hurdle for SMRs is reducing the high capital cost of first-of-a-kind (FOAK) units, estimated between $63/MWh and $180/MWh. Data center PPAs provide the revenue certainty needed for developers to progress down the cost curve through standardized manufacturing and serial production.

SWOT Analysis, SMR and Geothermal Data Center Power Strategy

The strategy to power data centers with dedicated geothermal and SMRs provides a credible path to achieving energy independence and 24/7 carbon-free operations. However, it is exposed to significant execution risks related to high upfront capital costs, long and complex regulatory processes, and the unproven economics of first-of-a-kind SMR projects. Success will depend on sustained policy support and a disciplined approach to project delivery.

Table: SWOT Analysis for Firm Clean Power in Data Centers

| Category | Strengths | Weaknesses | Opportunities | Threats |

|---|---|---|---|---|

| Technology | High capacity factor (>90%) for 24/7 baseload power. Small land footprint for SMRs (~50 acres) allows co-location. | Long project development and construction timelines (5-10 years). Unproven economics for first-of-a-kind SMRs. | Cost reduction through serial production of SMRs (up to 40%). Maturation of Enhanced Geothermal Systems (EGS) to expand geographic reach. | Delays in SMR technology commercialization or failure to meet cost targets. Public opposition to nuclear projects. |

| Economics | Insulation from volatile electricity market prices. Long-term cost certainty through 20-year PPAs. | High upfront capital expenditures (SMR CAPEX: $7, 000-$8, 000/k W). High LCOE for early SMR projects ($63-$180/MWh). | Inflation Reduction Act incentives, including a 30% ITC. Soaring power demand from AI creates a large, guaranteed customer base. | Changes in tax policy or incentive structures. Unexpected cost overruns in construction. Competition from future low-cost energy storage. |

| Infrastructure | Bypasses congested public grid interconnection queues. Reduces reliance on long-distance transmission infrastructure. | Requires specialized supply chains and a skilled workforce for nuclear construction and operation. | Creation of dedicated, resilient “power islands” for critical digital infrastructure. Opportunity to revitalize nuclear supply chains. | Grid instability in surrounding regions affecting project construction and operations. Supply chain bottlenecks for critical components. |

SMR Deployment Signals, Watch for Switch’s First Nuclear PPA

The most critical indicator to monitor in the next 12-24 months is the announcement of the first direct PPA between a major colocation operator like Switch and an SMR developer. Such an agreement would serve as a powerful market signal, validating the financial and regulatory viability of co-locating new nuclear power with data centers and potentially triggering a wave of similar deals across the industry.

- While hyperscalers have led with early-stage nuclear agreements, a deal from a colocation provider would demonstrate that this strategy is viable beyond the largest tech companies and is scalable across the broader digital infrastructure market.

- Progress on the 25 SMR license applications expected by the NRC before 2029 will be a key barometer of the industry’s health. The successful approval of a design intended for a data center project would mark a major milestone.

- Monitor the projected and actual LCOE for SMR projects. Any significant downward revision from the current wide range of $63-$180/MWh, particularly for “Nth-of-a-kind” projects, would dramatically improve the business case and accelerate adoption.

- Policy remains a crucial variable. The continuation and effective implementation of federal incentives like the IRA’s tax credits are essential for the economic feasibility of these capital-intensive, long-term projects.