BHP DAC Pivot, 30% Steel Decarbonization Goal, 1 Asian Consortium, and Carbon Mineralization Focus (2025)

Indirect Carbon Removal, BHP Prioritizes Value Chain Over High-Cost DAC

In 2025, BHP is deliberately avoiding direct investment in high-cost, technologically nascent Direct Air Capture projects, instead focusing its decarbonization efforts on its value chain and synergistic carbon removal methods that align with its core mining operations. This strategic pivot marks a significant shift from the broad climate pledges common across the industry between 2021 and 2024 to a more pragmatic and capital-efficient approach tailored to its business model. The company’s choice is a direct response to the challenging economics of the current Direct Air Capture market.

- By leading a new consortium in August 2025 to explore carbon capture initiatives across Asia, BHP is addressing emissions within a key geographical market for its products rather than building expensive, stand-alone facilities.

- The company established a medium-term goal to support partners in developing steel production technology with a 30% lower greenhouse gas intensity by 2030, tackling its significant Scope 3 emissions at the source.

- Instead of investing in mechanical DAC, which costs between $300 and $500 per tonne, BHP is exploring the use of its own mine tailings for carbon mineralization, a method that turns mining waste into a carbon sink.

- This strategy leverages existing assets and partnerships to de-risk its decarbonization pathway, a crucial consideration under new, more complex financial regulations like the “One Big Beautiful Bill Act” (OBBBA) enacted in July 2025.

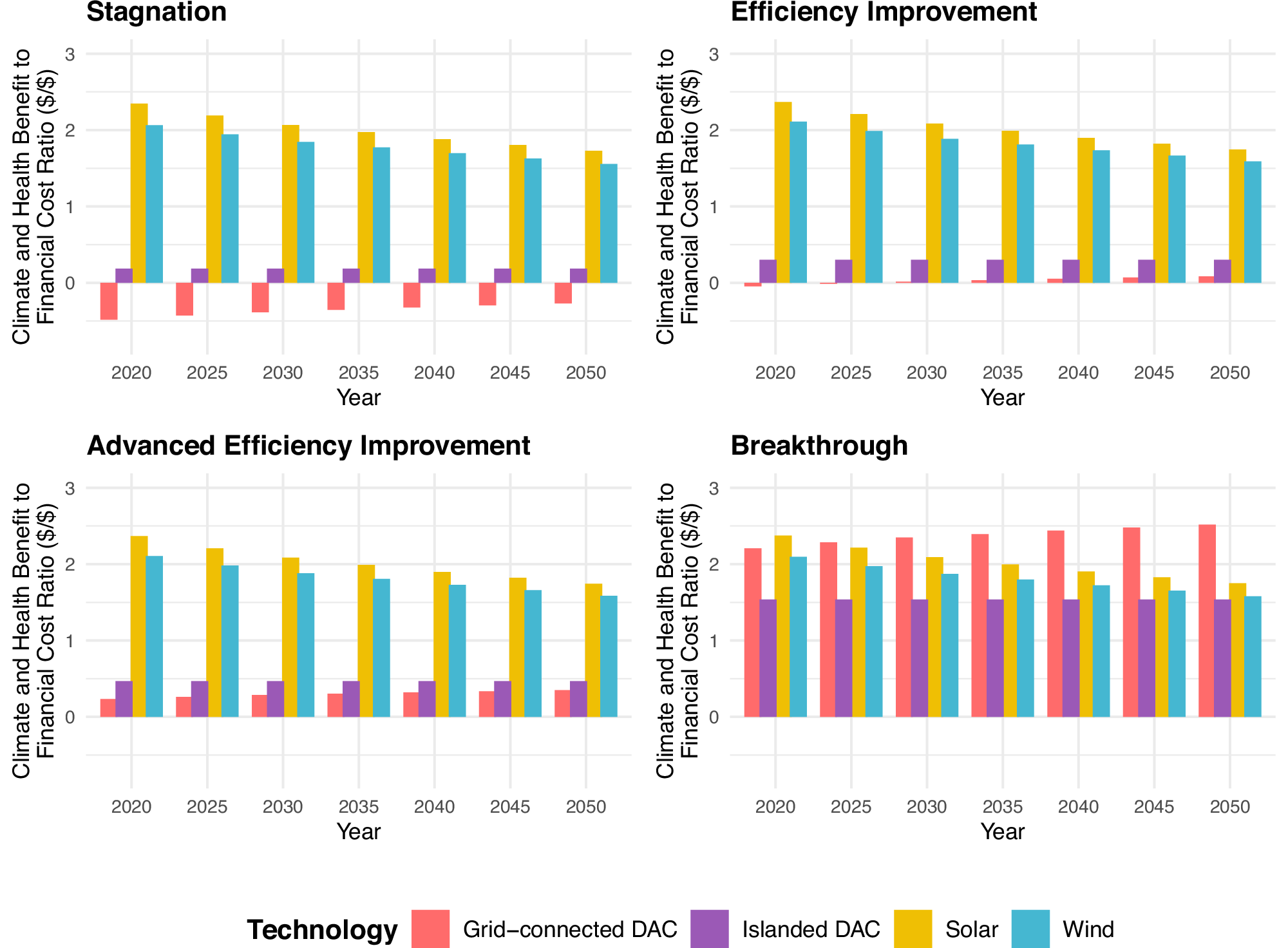

DAC’s Cost-Benefit Lags Solar and Wind

The chart provides the economic rationale (high cost of DAC) for BHP’s strategic choice to prioritize its value chain over high-cost Direct Air Capture, as stated in the section heading.

(Source: Nature)

$4.5 B in Capital, BHP Focuses on Core Mining and Critical Minerals

BHP’s 2025 capital expenditures show a clear prioritization of core business growth and the supply of energy transition materials over speculative ventures into the developing DAC market. This allocation of capital underscores a strategy to strengthen its fundamental operations while pursuing lower-cost, synergistic decarbonization pathways.

- Capital expenditure on the Jansen Stage 2 potash project reached $4.5 billion as of June 2025, demonstrating a major investment in its primary mining portfolio.

- BHP identified a cumulative industry need of approximately $250 billion in growth capital for copper to meet a 1.5-degree climate scenario, positioning itself as a key supplier rather than a consumer of high-cost carbon removal technologies.

- This financial discipline stands in contrast to the high capital costs of DAC and the unstable policy environment, where financing for large-scale carbon removal projects has become more challenging.

- The company’s internal carbon pricing mechanism, highlighted in March 2025 as a successful corporate decarbonization tool, likely reinforces investment decisions that favor established operations and partnerships with clear returns over high-risk technology plays.

Renewable Energy M&A Activity Reached $117B in 2024

The chart offers broad market context on capital allocation in the energy sector, providing a macro-level backdrop for the section’s discussion of BHP’s specific $4.5 billion capital focus.

(Source: Energy Central)

Table: BHP 2025 Strategic Capital Allocation

| Project / Investment Focus | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Copper Industry Growth | Aug 2025 | BHP estimates the copper industry requires ~$250 billion in growth capital to meet transition-related demand, a market it plans to supply. This signals a focus on providing critical materials for decarbonization. | BHP |

| Jansen Stage 2 Potash Project | Jun 2025 | Capital expenditure on the project totaled $4.5 billion to date, highlighting continued, significant investment in core mining assets with defined market demand. | BHP |

BHP 1 Asian Consortium and Steel Industry Partnerships (2025)

BHP’s 2025 decarbonization strategy is executed primarily through collaborative partnerships that target emissions in hard-to-abate sectors and key geographical markets, rather than through in-house technology development. This model allows the company to influence large-scale emissions reduction and de-risk technology adoption without bearing the full capital burden.

- In August 2025, BHP assumed a leadership role in a consortium to investigate carbon capture solutions across Asia, directly engaging with the industrial ecosystem in its primary customer base.

- The company formalized its commitment to work with steel industry partners on a technology pathway to lower GHG emissions intensity by 30% by 2030, addressing its most significant source of value chain emissions.

- This partnership-led approach is consistent with the findings of an AIST roadmap from July 2025, which emphasized collaborative pilot projects as a method for de-risking new iron and steel manufacturing technologies.

Corporate Buyers Drive Carbon Removal Market in 2025

The chart explains the market dynamic that enables BHP’s partnership strategy, showing that corporate buyers (like BHP and its steel partners) are the primary drivers of the carbon removal market.

(Source: AlliedOffsets)

Table: BHP’s 2025 Carbon Reduction Partnerships

| Partner / Initiative | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Asian Carbon Capture Consortium | Aug 2025 | BHP is leading a consortium to explore carbon capture projects in Asia, targeting emissions reduction in a key operational and customer region. | Yahoo Finance |

| Steel Industry Partners | Aug 2025 | Announced a goal to support partners in developing steelmaking technology with a 30% reduction in GHG intensity, directly targeting its Scope 3 emissions. | BHP |

| Internal Carbon Pricing (ICP) | Mar 2025 | BHP was recognized as one of three major firms successfully using an ICP mechanism to steer corporate strategy and investment toward decarbonization. | National University of Singapore |

Carbon Market Dominated by Avoidance Credits

This chart highlights the strategic value of BHP’s partnerships, which focus on direct decarbonization, by contrasting them with the broader carbon market’s reliance on lower-quality avoidance credits.

(Source: AlliedOffsets)

Asia and Australia Focus, BHP Aligns Carbon Strategy with Operations

BHP’s 2025 carbon strategy is geographically concentrated in Asia and Australia, directly aligning with its major operational hubs and key customer markets. This regional focus ensures that its decarbonization efforts are synergistic with its core business, targeting the areas of greatest material impact.

- The decision to lead a carbon capture consortium in Asia directly addresses the emissions footprint of the region’s industrial sector, which is the primary market for BHP’s iron ore and metallurgical coal.

- Australia, particularly Western Australia, has emerged as a key area for exploring carbon mineralization. The presence of companies like Arca, which in 2025 began deploying technology to turn mine tailings into carbon sinks at Australian sites, provides a strong regional precedent for BHP to leverage its own mining waste.

- This targeted geographic strategy contrasts with the broader, subsidy-driven development of DAC hubs seen in other parts of the world, allowing BHP to focus on solutions with a clearer line of sight to commercial and operational viability.

Synergistic CDR vs. Immature DAC, BHP’s 2025 Technology Choice

BHP’s 2025 strategy demonstrates a clear preference for deploying more mature, synergistic carbon dioxide removal technologies like carbon mineralization over the technologically immature and costly mechanical DAC systems. This choice reflects a pragmatic assessment of the current technology landscape and a desire to link decarbonization directly to its industrial strengths.

- In 2025, DAC technology remains expensive, with operational costs ranging from $300 to $500 per tonne and capital costs as high as $3, 000 per tonne of annual capacity, making it an economically challenging proposition for large-scale private investment without heavy subsidies.

- Carbon mineralization, which uses alkaline materials like mine tailings to capture atmospheric CO₂, offers a more synergistic pathway for a mining company. It transforms a waste liability into a potential asset for generating carbon credits, as noted in industry analyses from June 2025.

- The pursuit of lower-emissions steelmaking through partnerships relies on advancing point-source capture and process efficiencies, which are more established and economically viable technology pathways compared to DAC.

- BHP’s approach validates the market reality that while DAC holds long-term promise, it is not yet mature enough for at-scale adoption by major industrial players focused on near-term, capital-efficient emissions reduction.

Direct Air Capture Market Poised for Explosive Growth

This chart provides important market context for BHP’s technology choice, showing that while BHP deems DAC ‘immature’ for its current needs, it is a rapidly growing market, making BHP’s decision a strategic one.

(Source: Market.us)

SWOT Analysis, BHP Indirect Carbon Removal Strategy

The 2025 analysis shows BHP’s strategic strengths lie in leveraging core assets for carbon management, while weaknesses include a dependency on partner progress and nascent technologies. Opportunities exist in carbon credit generation from mineralization, with threats from policy shifts and the high cost of eventual DAC entry.

- Strengths: The company effectively leverages its massive operational footprint and waste streams (mine tailings) for potential carbon removal, avoiding the high capital risk of direct DAC investment.

- Weaknesses: Progress in decarbonization, particularly in its Scope 3 emissions, is heavily dependent on the technological success and adoption rates of its external steelmaking partners.

- Opportunities: Carbon mineralization presents an opportunity to create a new revenue stream from carbon credits, turning a cost center into a value generator while simultaneously addressing emissions.

- Threats: The strategy is exposed to regulatory volatility, such as changes to the 45 Q tax credit under the OBBBA, and the risk of being outpaced if a competitor or new technology rapidly reduces the cost of DAC.

Table: SWOT Analysis for BHP’s Indirect Carbon Removal Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strength | Strong balance sheet and scale to fund large-scale climate initiatives. | Leverages core mining operations for synergistic CDR (mineralization), avoiding high-risk DAC CAPEX while focusing capital on core growth (e.g., Jansen project). | The strategy shifted from being a potential capital provider for climate tech to an active user of synergistic technologies that enhance the core business. |

| Weakness | Broad Scope 3 reduction goals for steelmaking without clearly defined, commercially viable technology pathways. | Decarbonization progress is now explicitly tied to the success of external steel industry partners and the scalability of emerging tech like mineralization. | The risk profile shifted from internal capital risk to external execution risk dependent on partners’ R&D and adoption cycles. |

| Opportunity | Positioned as a potential large-scale purchaser of carbon credits to meet climate targets. | Actively exploring pathways to generate carbon credits from mine tailings, creating a new potential revenue stream while supplying critical transition metals like copper. | The company’s role evolved from being a potential credit buyer to a potential credit generator and key enabler of the energy transition. |

| Threat | General reputational and market risk associated with being a major emitter and fossil fuel producer. | Specific regulatory uncertainty (e.g., OBBBA’s impact on 45 Q project finance) and the competitive risk of falling behind if DAC costs drop unexpectedly. | Threats became more tangible, moving from broad ESG concerns to specific policy and technology race dynamics that could impact future competitiveness. |

BHP 2026 Outlook, 1 Mineralization Pilot and Asian CCS Milestones

If BHP formalizes a carbon mineralization pilot in Australia in the next year, watch for a strategic move to quantify and monetize carbon credits from its waste streams, signaling a new, scalable business model for large-scale miners.

- If the Asian carbon capture consortium announces its first specific project, watch for the technology choice (point-source vs. DAC) and the associated financing structure, which will reveal the commercial viability of large-scale CCS in the region post-OBBBA.

- If steelmaking partners report tangible progress toward the 30% GHG reduction goal, this could be happening: BHP’s value-chain-first strategy is being validated, proving more effective than direct technology investment.

- If BHP announces a formal partnership with a mineralization technology firm like Arca, this signals that the company is moving to build a defensible, low-cost carbon removal capability that mining competitors cannot easily replicate.

Potassium Hydroxide Market Forecasts Steady Growth

This chart provides specific, technical context for the ‘mineralization pilot’ mentioned in the section, as potassium hydroxide is a key chemical input for certain mineralization technologies.

(Source: Persistence Market Research)

The questions your competitors are already asking

This report covers one angle of BHP’s decarbonization strategy. The questions that matter most depend on your work.

- How does carbon mineralization using mine tailings compare to mechanical DAC for cost and scalability in the mining sector?

- BHP’s activities in steel decarbonization. Is the partnership to cut GHG intensity by 30% progressing from pilot to deployment?

- Which mining operators are pivoting from direct air capture to value chain decarbonization strategies?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.