UAE Hydrogen Strategy 2026: Why Downstream Mobility Pilots are Outpacing Upstream Production

Hydrogen Adoption in the UAE: A Dual-Track Strategy Emerges

The UAE’s hydrogen market is adopting a dual-track strategy, separating ambitious, capital-intensive upstream production plans from pragmatic, operational downstream mobility pilots. While state-owned entities like ADNOC focus on developing large-scale blue and green hydrogen facilities for future export, national oil company ENOC is concentrating on building the immediate, domestic use-case for hydrogen in the transport sector. This bifurcation allows the nation to pursue long-term global leadership in hydrogen supply while simultaneously de-risking domestic demand and infrastructure through smaller, targeted projects.

- Between 2021 and 2024, the strategic focus was on establishing foundational upstream capabilities. This period was defined by high-level alliances like the Abu Dhabi Hydrogen Alliance and agreements by ADNOC to explore million-tonne-per-annum blue ammonia production facilities with partners like GS Energy and Mitsui. The primary commercial activity was centered on future production capacity.

- From 2025 onward, the most visible commercial progress has shifted to the downstream sector. This change is marked by ENOC‘s trial agreement with Dubai’s Roads and Transport Authority (RTA) on March 20, 2025, to supply green hydrogen for city buses. This initiative leverages hydrogen from DEWA‘s operational pilot plant, creating a complete, albeit small-scale, value chain from production to end-use.

- The emergence of tangible mobility projects, such as fueling airport buses and public transport, demonstrates a strategic pivot from planning to execution. ENOC‘s role as a distributor and infrastructure operator, rather than a producer, validates a phased approach to market creation, proving the technology in a controlled environment before committing to wider-scale infrastructure.

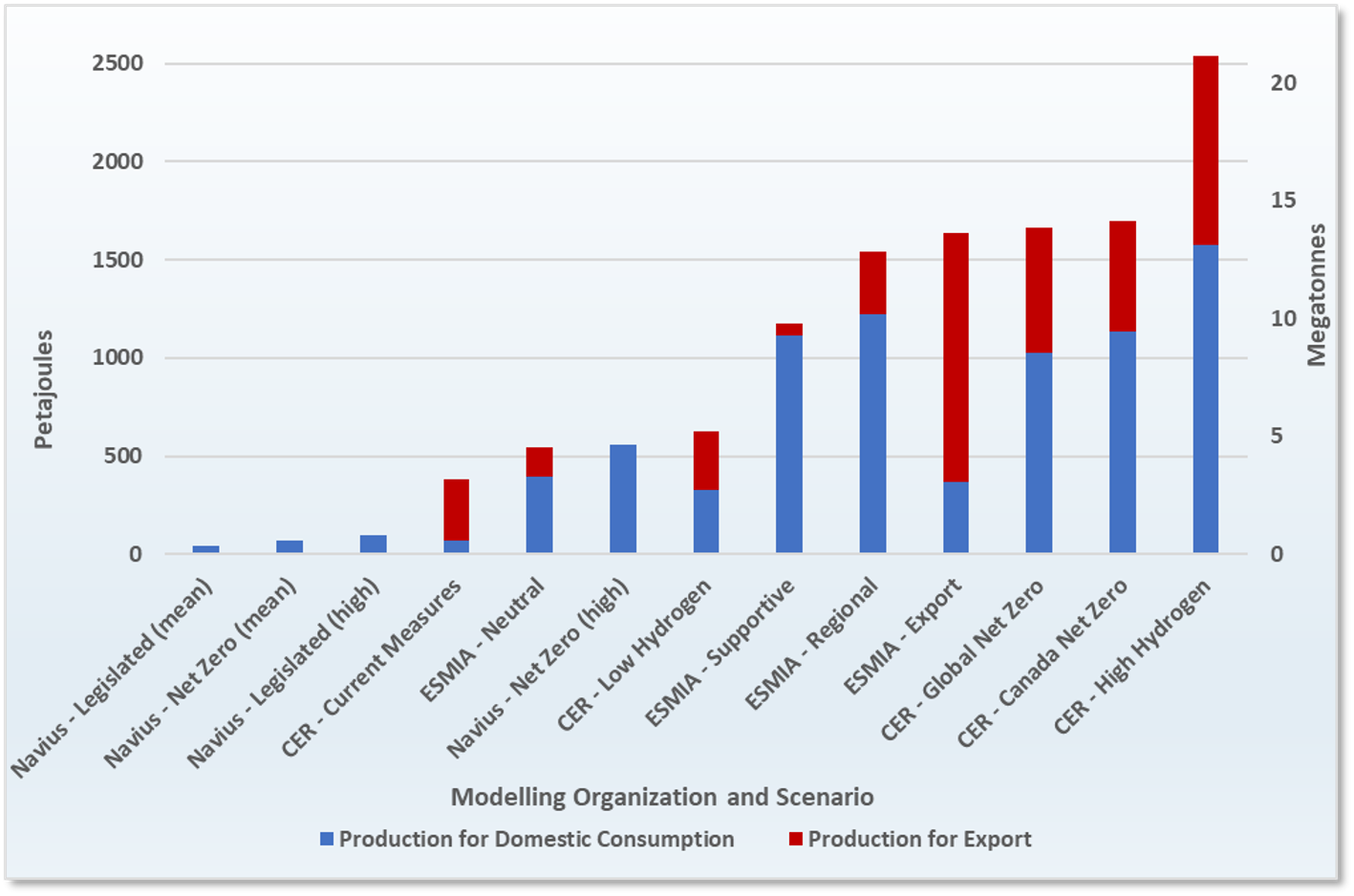

Hydrogen Strategy Splits Domestic and Export Focus

This chart illustrates the UAE’s dual-track strategy by visualizing the division between hydrogen produced for domestic consumption and volumes intended for the export market.

(Source: Natural Resources Canada – Canada.ca)

Partnerships Reveal Divergent Strategies for Production and Market Creation

Strategic partnerships are the primary mechanism driving the UAE’s hydrogen ambitions, but the nature of these collaborations reveals two distinct goals. Upstream alliances are structured to secure technology and capital for large-scale production, targeting the global export market. In contrast, downstream partnerships are focused on creating a localized, integrated ecosystem to validate demand and test the operational viability of hydrogen as a domestic transport fuel.

Offtake Agreements Rise for Industrial and Transport

This chart reflects the divergent partnership strategies by showing the growth in offtake agreements for both industrial uses (upstream) and transport (downstream).

(Source: Net Zero Technology Centre)

- Upstream partnerships are characterized by large-scale investment targets and technology transfer. For example, Masdar‘s October 2, 2025, partnership with Iberdrola to invest up to €15 billion in offshore wind and green hydrogen projects is focused on building massive production capacity. Similarly, ADNOC’s earlier partnerships were geared towards developing export-oriented blue ammonia facilities.

- Downstream partnerships are focused on offtake and infrastructure. ENOC’s core hydrogen strategy revolves around its collaborations with DEWA, which supplies the green hydrogen, and the RTA, which provides the end-user fleet of buses. This creates a closed-loop system that proves the business case at a manageable scale.

- Bridging these two tracks, ENOC‘s August 2024 feasibility study with Japan’s IHI Corporation to explore a green ammonia supply chain and its November 2025 Mo U with Emirates for Sustainable Aviation Fuel (SAF) signal future integration. These initiatives lay the groundwork for connecting large-scale hydrogen production to high-value end markets like aviation, which will require both production scale and sophisticated distribution infrastructure.

Table: Comparative Partnership Strategies in the UAE Hydrogen Sector

| Company & Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ENOC & Emirates | Dec 2025 | Mo U to explore the supply of Sustainable Aviation Fuel (SAF) in Dubai, linking hydrogen to the future aviation fuel market. | Biomass Magazine |

| Masdar & Iberdrola | Oct 2025 | Upstream partnership to invest up to €15 billion in offshore wind and green hydrogen production projects, targeting large-scale supply. | WAM.ae |

| ENOC & RTA | Mar 2025 | Downstream trial agreement for ENOC to supply green hydrogen to RTA‘s bus fleet, creating a real-world test for mobility. | ENOC Group |

| ENOC & IHI Corporation | Aug 2024 | Feasibility study to establish a supply chain for green ammonia and hydrogen, exploring future production and international trade. | [PDF] Japan Energy Summit |

| ADNOC & Japanese Partners | Jan 2023 | Upstream joint study agreement to develop a 1 million tonnes per annum blue ammonia production facility in Ruwais for export. | ADNOC |

Geography of Hydrogen: Dubai as Mobility Testbed, Abu Dhabi as Production Hub

Within the UAE, a clear geographic division of labor has emerged in the hydrogen sector, with Dubai establishing itself as the center for practical mobility applications while Abu Dhabi remains the focal point for large-scale production and export strategies. This regional specialization allows for parallel development, enabling Dubai to build a domestic market and operational expertise while Abu Dhabi focuses on the capital-intensive challenge of becoming a global hydrogen supplier.

Middle East Becomes a Key Hydrogen Supplier

This chart supports Abu Dhabi’s role as a production hub by showing the Middle East is a significant source of future low-carbon hydrogen supply for the world.

(Source: Carbon Credits)

- Between 2021 and 2024, Abu Dhabi solidified its role as the center of the UAE’s upstream hydrogen ambitions. The formation of the Abu Dhabi Hydrogen Alliance and ADNOC‘s plans for large-scale production facilities in Ruwais signaled a clear focus on becoming a major hydrogen and ammonia exporter.

- Starting in 2025, Dubai has become the epicenter of tangible hydrogen application. The crucial activities are concentrated around ENOC‘s green hydrogen refueling station at Expo City Dubai, which serves as the hub for the RTA bus trials and demonstrations for the Dubai Airshow.

- This functional split minimizes direct competition for resources and allows each Emirate to leverage its strengths. Dubai utilizes its position as a logistics and urban innovation hub to test last-mile delivery and consumer-facing infrastructure, while Abu Dhabi leverages its energy production and industrial base to plan for global-scale supply chains.

Technology Maturity: Refueling Infrastructure Moves from Pilot to Operational Reality

While the underlying technology for green hydrogen production is advancing, the most significant maturation in the UAE’s hydrogen ecosystem has been in the downstream refueling infrastructure, which has progressed from a concept to an operational, revenue-generating asset. This shift from pilot project launch to real-world application provides critical data on performance, logistics, and safety, which is essential for future network expansion.

- The period between 2021 and late 2023 was focused on construction and launch. The key event was the inauguration of ENOC‘s integrated green hydrogen refueling station in December 2023, a collaborative effort with DEWA. At this stage, the technology was proven by its existence, but its operational viability was still theoretical.

- In 2025, the technology’s maturity is being validated through active commercial use. By August 2025, DEWA’s production facility, the source of the hydrogen, had produced over 100 tonnes, demonstrating consistent supply. Simultaneously, ENOC‘s station is no longer just a showcase; it is actively fueling public transport vehicles for the RTA, proving its technical reliability in a live environment.

- This contrasts with the status of large-scale production technologies, which largely remain in the feasibility study or early development phases. The success of the refueling station provides a tangible proof point that can attract vehicle OEMs and fleet operators, helping to solve the chicken-and-egg problem between fuel availability and vehicle adoption.

SWOT Analysis: ENOC’s Downstream Focus in the UAE Hydrogen Market

ENOC’s strategy of focusing on downstream distribution leverages its core competencies but also creates dependencies on a nascent market and third-party producers. The evolution from 2021 to 2025 shows a successful transition from planning to execution, validating the company’s role as a key enabler of hydrogen mobility in Dubai.

- Strengths: ENOC’s primary strength is its extensive network of retail fuel stations and its expertise in fuel logistics and distribution, providing a clear and unrivaled path to scale for hydrogen mobility infrastructure.

- Weaknesses: The strategy’s main weakness is the complete dependence on external partners like DEWA for hydrogen supply, which could create pricing and volume risks as demand grows.

- Opportunities: The key opportunity lies in becoming the dominant hydrogen retailer for Dubai’s mobility sector and leveraging this position to enter the future market for e-fuels like SAF, as indicated by the Emirates Mo U.

- Threats: The primary threats are slow adoption of hydrogen vehicles by consumers and fleet operators, competition from alternative clean fuels like electricity, and the potential for larger players like ADNOC to expand their “H 2 GO” retail brand into Dubai.

Table: SWOT Analysis for ENOC’s Hydrogen Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Theoretical advantage of existing retail network and logistics capabilities. | Demonstrated ability to integrate a hydrogen dispenser into an existing station and manage refueling for a commercial partner (RTA). | The theoretical advantage was validated with the successful launch and operation of the Expo City station, proving technical and operational capability. |

| Weaknesses | No hydrogen production capacity and no operational experience with hydrogen as a fuel. | Still reliant on a single supplier (DEWA) from a pilot-scale plant. The IHI study is only an exploration of future supply. | The dependence on a single, small-scale producer has been confirmed as a potential bottleneck for future growth if demand accelerates. |

| Opportunities | Mo Us with Neste to explore SAF and plans to support Dubai’s Green Mobility Strategy. | Formal trial agreement with RTA for buses and a new Mo U with Emirates for SAF supply, directly linking hydrogen to public transport and aviation. | The opportunity has moved from strategic alignment to a concrete commercial trial with a major public transport authority, providing a clear path to market. |

| Threats | General market uncertainty and competition from EVs. ADNOC announces its “H 2 GO” refueling brand. | ADNOC‘s plans for its own stations continue. Alternative technologies, like BEEAH’s hydrogen-from-waste plant, create new production pathways outside ENOC‘s ecosystem. | The competitive environment has become more defined, with clear alternative pathways for both hydrogen production and distribution emerging. |

Scenario Modelling: 2026 Will Be a Decisive Year for Hydrogen Mobility

If the ENOC-RTA bus trials demonstrate commercial viability and operational reliability through 2025, watch for ENOC to announce a multi-site expansion of its hydrogen refueling network in 2026. This expansion would be a critical signal that the downstream mobility model is succeeding, likely triggering further investment in both refueling infrastructure and vehicle procurement. The stability of the broader region, however, remains a key variable, as any disruption could impact the long-term investment climate for the entire energy transition.

- Success Signal: The most important indicator to watch is the outcome of the RTA bus trial. A positive result, defined by reliable performance and manageable operating costs, would provide the business case for expanding the refueling network beyond the single Expo City site.

- Market Expansion Signal: Progress on the Emirates SAF Mo U is another critical milestone. An announcement of a pilot production project or a firm offtake agreement would confirm that ENOC is successfully bridging its current hydrogen activities to the much larger and more lucrative aviation decarbonization market.

- Pivot Signal: Conversely, if the bus trials face significant technical or economic challenges, or if vehicle adoption remains stagnant, watch for ENOC to increase its investments in parallel clean energy tracks. Accelerated deployment of fast EV chargers with ION or new biodiesel initiatives would suggest a strategic pivot to more mature technologies.

- External Risk: The entire transition is predicated on regional stability, as long-term, capital-intensive energy projects require a predictable investment environment. Geopolitical shocks can dramatically alter project economics and timelines, impacting both hydrogen development and the reliability of existing LNG supply chains that currently underpin the global energy system.

Frequently Asked Questions

Why does the article say the UAE has a ‘dual-track’ hydrogen strategy?

The UAE’s strategy is described as ‘dual-track’ because it separates ambitious, long-term upstream production goals from more immediate, practical downstream mobility pilots. While state-owned entities in Abu Dhabi like ADNOC focus on developing massive hydrogen facilities for future export, Dubai-based ENOC is concentrating on building a domestic use-case for hydrogen in the transport sector, allowing for parallel progress on both global supply and local demand.

What is the main difference between Abu Dhabi’s and Dubai’s roles in the hydrogen sector?

The article outlines a clear geographic division of labor. Abu Dhabi is positioned as the UAE’s primary production hub, focusing on capital-intensive, large-scale blue and green hydrogen and ammonia facilities intended for the global export market. In contrast, Dubai has become the testbed for practical mobility applications, using its urban environment to pilot hydrogen-fueled public transport and build out refueling infrastructure.

According to the analysis, why are downstream mobility projects outpacing upstream production?

Downstream mobility pilots are outpacing large-scale production because they are smaller, more pragmatic, and can be executed faster. Projects like the ENOC-RTA bus trial leverage existing pilot-scale production from DEWA to create a complete, operational value chain. This allows for tangible progress and real-world data collection, while massive upstream projects remain in the longer, more complex phases of planning, securing capital, and large-scale engineering.

Who are the key partners in Dubai’s hydrogen mobility pilot, and what are their roles?

The core partnership creating Dubai’s hydrogen mobility ecosystem consists of three entities: DEWA (Dubai Electricity and Water Authority), which produces the green hydrogen at its operational pilot plant; ENOC Group, which acts as the distributor and infrastructure operator by running the hydrogen refueling station; and the RTA (Roads and Transport Authority), which provides the end-user fleet of buses for the trial.

Based on the SWOT analysis, what is the biggest risk or weakness in ENOC’s current hydrogen strategy?

The primary weakness identified for ENOC is its complete dependence on a single external partner, DEWA, for its hydrogen supply. This reliance on a pilot-scale production plant could create future bottlenecks related to both pricing and volume if demand for hydrogen fuel grows faster than the available supply, potentially hindering ENOC’s ability to scale its refueling network.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.