Electric Truck Exports, 40% Domestic Target, 6 Chinese OEMs Eye Europe, and 3, 000 Charging Stations (2024 to 2026)

54% Market Share Peak, China’s OEMs Heavy-Duty Electrification

China’s heavy-duty truck market has crossed a critical threshold, moving from policy-driven experimentation to commercially-led mass adoption as total cost of ownership (TCO) becomes favorable for fleet operators.

- Between 2021 and 2024, the market share for electric heavy-duty trucks (HDTs) was nascent, growing from negligible levels to just over 3% of new sales in 2024.

- The market saw an inflection point in 2025, with market share for new sales jumping to 9% for the full year and hitting a monthly peak of 22% in the first half of the year.

- This acceleration culminated in December 2025, when new-energy HDTs outsold diesel models for the first time, capturing a record 53.89% of monthly sales with over 45, 000 units registered.

- The momentum has proven durable, with market share sustaining well above previous levels, reaching 27% in Q 1 2026 and 28.9% by April 2026, confirming a structural shift in the freight market.

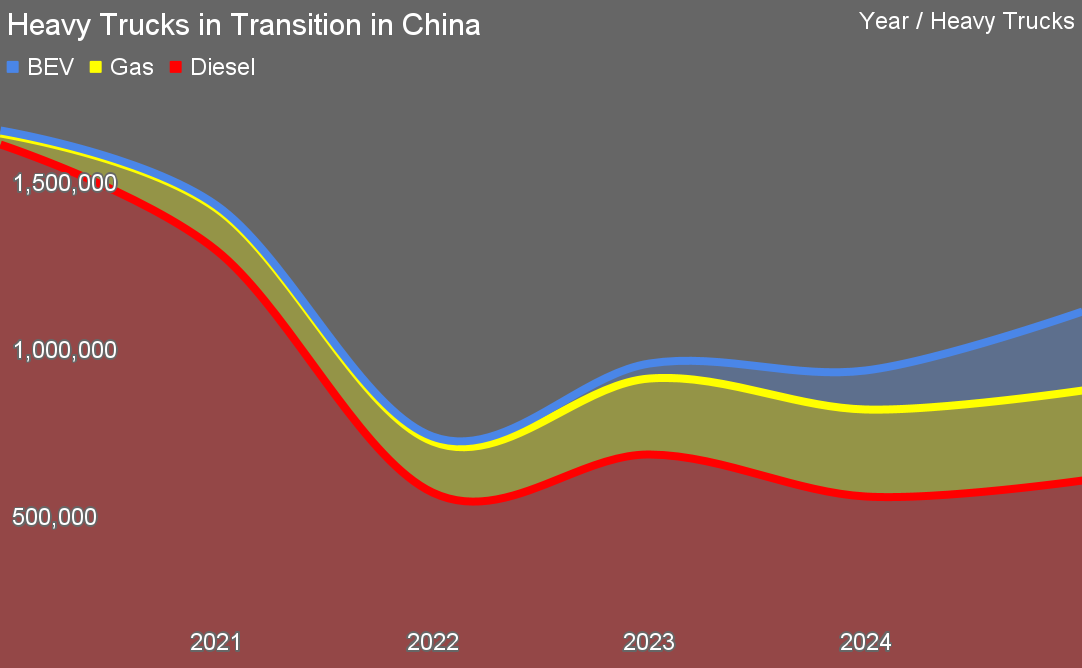

China’s Heavy Truck Market Composition Shifts 2021-2024

This chart directly visualizes the core theme of the section, showing the shift towards electrification in China’s heavy-duty truck market. The ‘54% market share peak’ mentioned in the heading would be a key data point on this chart, illustrating the success of China’s OEMs.

(Source: CleanTechnica)

China’s National Plan $81, 600 Truck Subsidies and Tax Waivers (2024 to 2026)

China’s central government has de-risked the transition to electric heavy trucks by implementing a sweeping national plan that combines direct financial incentives with clear, long-term mandates for infrastructure development.

- The core of the strategy, announced in June 2026, sets a national target for new-energy vehicles to comprise 40% of heavy truck sales by 2030, creating a predictable demand signal for the entire supply chain.

- To overcome the high upfront capital cost of electric trucks, the government offers purchase subsidies that can reach as high as USD 81, 600 per vehicle, covering a significant portion of the price premium over diesel models.

- Fiscal policy further incentivizes adoption through a waiver of the 10% vehicle purchase tax for qualifying new-energy vehicles, although this exemption is scheduled to be reduced starting in 2026.

- The plan mandates the construction of approximately 3, 000 dedicated heavy-duty charging and battery-swapping stations by 2030, directly addressing infrastructure bottlenecks and ensuring operational viability for fleets.

China’s HDT Fleet Projected to Shift from Diesel

The section describes a national plan with subsidies to encourage EV truck adoption. This chart illustrates the projected outcome of such a plan, showing the expected shift away from diesel in the heavy-duty truck (HDT) fleet, directly linking policy to future market changes.

(Source: Nature)

Table: China’s Heavy-Duty EV Incentives and Mandates

| Policy | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| National Adoption Target | 2026-2030 | Mandates that 40% of new heavy-duty truck sales must be new-energy vehicles by 2030, aiming for a fleet of over 1.6 million units. Creates long-term demand certainty for manufacturers and investors. | Cn EVPost |

| Purchase Subsidies | Ongoing (Phasing Out) | Provides direct financial support up to USD 81, 600 per heavy-duty truck. Directly lowers the initial capital expenditure for fleet operators, making the TCO calculation favorable sooner. | IEA |

| Tax Exemptions | Full Exemption until 2025; Halved in 2026-2027 | Waives a 10% vehicle purchase tax on electric trucks. This further reduces the upfront acquisition cost compared to diesel equivalents, accelerating adoption. | The ICCT |

| Infrastructure Mandate | By 2030 | Requires the construction of approximately 3, 000 heavy-duty charging and battery-swapping stations. Solves the chicken-and-egg problem by ensuring a reliable energy network is built in parallel with the vehicle fleet. | Reuters |

China vs. The World, SANY Group Prepares for European Export Push

Having established unparalleled domestic market scale, leading Chinese manufacturers are now pivoting to an aggressive global export strategy, with Europe as the primary target for disruption.

- Prior to 2025, China’s focus was almost exclusively on cultivating its domestic market, where it now accounts for over 90% of global electric truck sales.

- The rapid maturation of its domestic market has created significant manufacturing overcapacity and a cost structure that is highly competitive on a global scale.

- Starting in 2026, a wave of Chinese OEMs are set to enter the European market; at least six manufacturers, including industry leaders SANY Group, BYD, and Geely’s Farizon unit, have announced plans for European expansion.

- This export push poses a direct challenge to established European players like Volvo and Daimler, as Chinese brands are projected to have a cost advantage of up to 30% due to their economies of scale and control over the battery supply chain. While Chinese firms expand, Western companies like Einride are focused on specialized autonomous and electric freight solutions in markets like the U.S.

TCO Parity Achieved, China’s Electric Trucks Reach Commercial Scale

Battery-electric heavy trucks in China have achieved commercial maturity for specific applications, driven by a rapid convergence of lower operating costs, improving battery technology, and innovative business models like battery swapping.

- Between 2021-2024, the primary barrier to adoption was the high upfront cost, with electric models costing two to three times more than diesel, making the total cost of ownership (TCO) viable only with heavy subsidies.

- By 2025, the economic calculus shifted; TCO parity or advantage was achieved in high-utilization, short-to-medium haul applications like port drayage and regional logistics, where lower energy and maintenance costs outweigh the initial investment. In China, electricity for heavy trucks is reported to cost 65% less per kilometer than diesel.

- Battery technology has matured, with capacities now concentrating in the 300-500 k Wh range, sufficient for many regional routes. The domestic supply chain, dominated by CATL, provides these batteries at a scale and cost unattainable in other regions.

- To address range anxiety and long charging times, Chinese OEMs like Sany Heavy Industry have pioneered battery-swapping models, allowing a truck to exchange a depleted battery for a full one in minutes, a model that has proven highly effective in 24/7 commercial operations.

SWOT Analysis, China’s OEMs Strengths and Global Market Threats

China’s strategic industrial policy has built a formidable domestic electric truck industry with immense strengths in manufacturing scale and cost, but its global expansion faces threats from international trade policies and competition.

- Strengths: Unmatched manufacturing scale, a dominant position in the battery supply chain, and strong government policy support create a significant cost advantage.

- Weaknesses: The industry’s growth is still partially dependent on subsidies that are being phased out, and the immense power demand from megawatt-scale charging poses a significant challenge to local grid infrastructure.

- Opportunities: A massive and growing export market, particularly in Europe, where established OEMs are moving more slowly on electrification and at a higher price point.

- Threats: Potential for protectionist trade policies (tariffs) in Europe and North America in response to low-cost imports, and intensifying domestic competition that could erode margins.

China Pictured as an “Electrostate” vs. Western “Petrostates”

A SWOT analysis examines strategic positioning. This conceptual chart visually represents a core strength and opportunity for China (its ‘Electrostate’ focus) against a comparative weakness or threat for Western competitors (reliance on oil), fitting the strategic nature of the section.

(Source: CleanTechnica)

Table: SWOT Analysis for China’s Heavy-Duty EV Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Growing manufacturing base and strong government commitment to EVs. Dominated passenger EV battery supply chains. | Achieved massive scale in heavy-duty truck production (half of world’s output). CATL holds 71.5% of the HDT battery market. TCO advantage is proven. | The strategy to leverage domestic scale for cost leadership was validated. China now dominates the entire HDT EV value chain, not just components. |

| Weaknesses | High vehicle purchase price (2-3 x diesel). TCO depended heavily on subsidies. Limited charging infrastructure for heavy trucks. | Grid strain becomes a major bottleneck, with a single heavy-duty charger potentially drawing 3.75 MW. Subsidy dependence is lessening but still a factor. | The primary weakness shifted from vehicle cost to infrastructure constraints. The grid’s ability to support megawatt charging is now the main operational risk. |

| Opportunities | Focus on domestic market growth in specific segments like ports and mining. Early export exploration. | A clear pivot to exports, with at least 6 major OEMs planning to enter Europe in 2026. Potential to undercut European rivals by 30%. | The opportunity transformed from domestic market creation to global market disruption. The scale achieved at home is now being weaponized for export. |

| Threats | Domestic competition among many startups and established players. Risk of policy changes and subsidy cuts. | International trade friction and the high likelihood of tariffs or anti-dumping actions in Europe and North America. Competition from Western incumbents accelerating their EV plans. | The primary threat is now external and geopolitical. Success will depend as much on navigating trade policy as it does on technology and cost. |

China’s OEMs 6 Competitors Entering Europe by 2026

The most critical strategic development to watch in the next 18 months is the execution of Chinese OEM export strategies into Europe, which will test the competitiveness of both the Chinese products and the resolve of European incumbents.

- If Chinese OEMs successfully establish a beachhead in the European market by offering trucks at a significant discount, watch for a rapid response from European manufacturers like Volvo and Daimler, who may be forced to accelerate their own cost-reduction and electrification timelines.

- The European Union’s policy response will be a key signal. Watch for the initiation of anti-dumping investigations or the imposition of tariffs on Chinese electric trucks, which could slow their market penetration.

- The adoption rate among European fleet operators will be the ultimate validation. Watch the initial sales figures and TCO case studies from early adopters of brands like SANY Group and BYD in Europe to gauge their real-world performance and market acceptance. This global competition includes specialized freight operators and technology providers like ADS-TEC Energy, which focuses on battery-buffered ultra-fast charging solutions that could enable EV trucking.

Chinese-Made BEVs Increase Global Market Share

This chart illustrates the broader trend of Chinese BEVs gaining ground in the global market. This increasing market share is the enabling factor that allows multiple Chinese OEMs to successfully compete and enter new markets like Europe by 2026.

(Source: Reddit)

The questions your competitors are already asking

This report covers one angle of China’s heavy-truck electrification push. The questions that matter most depend on your work.

- Which Chinese OEMs are gaining or losing ground in the electric heavy-truck market?

- What is the outlook for electric heavy-truck adoption, and is China on track to meet its 40% sales target by 2030?

- What are the export opportunities for Chinese electric truck OEMs in the European market?

- How does the total cost of ownership (TCO) for electric heavy-trucks now compare to diesel for Chinese fleet operators?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.