Exxon Mobil CCUS Ambition, $20 B Investment, CF Industries Deal, and 4 M Tonne Capacity Target (2021 to 2026)

CCUS Adoption Risks, Exxon Mobil’s $100 B Question and Policy Reliance

The large-scale adoption of Carbon Capture, Utilization, and Storage (CCUS), as pursued by Exxon Mobil, is less a test of technical feasibility and more a function of navigating significant policy and political risks that can alter project economics overnight. The company’s ambition to build the world’s largest carbon management business is fundamentally dependent on the long-term stability of government incentives, a factor that has proven increasingly volatile.

- Between 2021 and 2024, foundational policy frameworks were established, most notably the enhancement of the U.S. Section 45 Q tax credit. This incentive, providing $85 per metric ton for CO 2 stored in dedicated geologic formations, created the core economic rationale for large-scale CCUS investments by making previously unprofitable projects viable.

- From 2025 to today, the fragility of this policy reliance became apparent. In June 2025, the U.S. Department of Energy (DOE) abruptly canceled $3.7 billion in awards for decarbonization projects, an action that impacted companies like Calpine and Ørsted. While not directly hitting Exxon Mobil, this move signaled a volatile political environment for capital-intensive, long-term energy projects and underscored the primary risk to its strategy.

- Despite the political headwinds, commercial activity has accelerated since 2025. Exxon Mobil continues to advance its Gulf Coast hub strategy, securing partnerships and developing infrastructure, indicating a corporate commitment to the business model as long as the core 45 Q incentive remains intact.

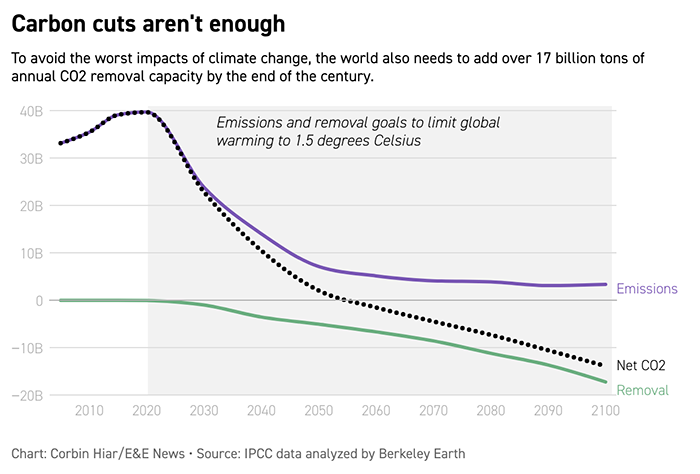

Vast CO2 Removal Needed to Meet Climate Goals

This chart quantifies the immense scale of carbon removal required to meet climate goals, directly contextualizing the massive market opportunity and investment thesis behind CCUS, which is central to the section’s “$100 B Question”.

(Source: E&E News)

$20 B Plan, Exxon Mobil’s Investment Moderation and Volatility

Exxon Mobil’s investment in its Low Carbon Solutions business is substantial but demonstrates calculated volatility, with the deployment of capital explicitly contingent on the stability of government incentives and prevailing market conditions. The company’s spending plans reflect a pragmatic, returns-focused approach rather than an unconditional commitment to decarbonization.

- The company plans to invest approximately $20 billion in its lower-emission portfolio between 2025 and 2030. This figure represents a significant moderation from a potential $30 billion discussed prior to 2025, signaling that future spending levels are highly sensitive to favorable government policies and project economics.

- In December 2025, reports surfaced that Exxon Mobil would cut its low-carbon spending by $10 billion to redirect capital toward upstream oil and gas. This highlights a dynamic capital allocation strategy that prioritizes shareholder returns and reacts swiftly to shifting market and policy signals.

- A crucial component of the strategy is its customer focus, with roughly 60% of the $20 billion investment aimed at projects that reduce emissions for third-party industrial customers. This underscores the company’s objective to build a new, service-based business centered on decarbonization, with a target of generating over $2 billion in additional earnings.

ExxonMobil Oil Production Projected to Rebound by 2025

This chart illustrates the projected performance of Exxon Mobil’s core oil production business, which is the primary source of capital for its $20B low-carbon plan and is subject to the market volatility mentioned in the section heading.

(Source: Forbes)

Table: Exxon Mobil Low-Carbon Investment and Strategic Plan Evolution

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Capital Expenditure Plan | 2025–2030 | Moderated investment of ~$20 billion in low-carbon solutions, with 60% aimed at reducing third-party emissions. Spending is conditional on policy support. | S&P Global |

| Spending Reduction | Dec 2025 | Announcement of a $10 billion cut in the low-carbon budget to shift investment back towards traditional upstream oil and gas, reflecting a pivot based on market conditions. | The Chemical Engineer |

| Initial Investment Commitment | Apr 2025 | Earlier, more aggressive plan to invest up to $30 billion by 2030 in low-carbon technologies, including CCUS, hydrogen, and lithium. | Climate Insider |

Exxon Mobil 900-Mile Pipeline, CF Industries Pact (2025 to 2026)

Exxon Mobil’s strategy is materializing through large-scale infrastructure projects and critical anchor partnerships designed to de-risk massive capital outlays and validate the commercial demand for “decarbonization as a service.” These agreements are the most tangible signals of the company’s progress in building an integrated carbon management network.

- The centerpiece of the strategy is the creation of a massive CCUS hub along the U.S. Gulf Coast. Exxon Mobil is investing billions to construct a 900-mile network of pipelines designed to transport CO 2 from various industrial emitters to centralized, permanent underground storage sites.

- A key commercial validation of this model is the partnership with CF Industries, a major ammonia producer. CF Industries is investing $4 billion to connect its facilities to Exxon Mobil’s network, demonstrating tangible market demand from heavy industry for a reliable decarbonization service. Other major emitters have also engaged, such as industrial gas company Linde.

- Exxon Mobil plans to bring new carbon capture facilities online in 2026 and 2027. These projects are expected to collectively capture approximately 4 million metric tons of CO 2 per year, representing a significant step in scaling its operational capacity and generating fee-based revenue.

Carbon Capture Pipeline Capacity Surges After 2020

This chart provides crucial industry context, showing that Exxon Mobil’s 900-mile pipeline project is part of a broader, post-2020 surge in building CCUS pipeline infrastructure, validating the project’s strategic direction.

(Source: Trellis)

Table: Exxon Mobil Key Carbon Capture Projects and Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Gulf Coast CCS Infrastructure | May 2026 | Construction of a vast 900-mile pipeline network to connect industrial customers to CO 2 storage sites, forming the backbone of the “CCS-as-a-service” model. | The Daily Upside |

| CF Industries Partnership | May 2026 | Major industrial partner CF Industries is investing $4 billion to utilize Exxon’s CCS network, serving as a critical anchor customer that validates the commercial model. | Streamline Feed |

| New Capture Facilities | May 2026 | Plans to start additional facilities in 2026 and 2027 with a combined capacity to capture approximately 4 million tons of CO 2 annually, scaling up operational capabilities. | The Globe and Mail |

Chart Outlines Key CCUS Market Segments

This chart serves as a conceptual guide for the accompanying table, outlining the different market segments for CCUS. It allows the reader to categorize and better understand the strategic placement of Exxon Mobil’s specific projects and agreements listed in the table.

(Source: IDTechEx)

US Gulf Coast, Exxon Mobil’s Geographic Focus for CCUS Hubs

Exxon Mobil’s global CCUS strategy is geographically concentrated on the U.S. Gulf Coast, a region strategically selected for its unique and powerful combination of dense industrial emissions and world-class subsurface geology suitable for permanent CO 2 sequestration. This focus allows the company to build an efficient, hub-and-spoke model and achieve economies of scale that would be impossible with disparate, smaller projects.

- From 2021 to 2024, CCUS projects globally were often smaller in scale and focused on proving technology or satisfying local regulatory requirements. The strategic shift for Exxon Mobil since 2025 has been toward developing a concentrated, world-scale market for carbon management services in a single region.

- The U.S. Gulf Coast is the ideal location for this strategy due to its high density of industrial emitters, including refineries, petrochemical plants, and manufacturing facilities. This creates a large, addressable market of customers in close proximity who require solutions to decarbonize.

- The region’s geology offers vast, porous rock formations deep underground, which are essential for the permanent and safe storage of CO 2. Exxon Mobil leverages its extensive subsurface expertise from decades of oil and gas exploration to identify and manage these sequestration sites.

- The planned 900-mile pipeline is the physical manifestation of this geographic strategy, creating the essential “midstream” infrastructure to connect the numerous sources of CO 2 (the customers) with the secure storage sites (the service).

ExxonMobil Targets Gulf Coast for CCS Hub

The chart is a direct visual representation of the section’s topic, mapping out Exxon Mobil’s targeted geographic focus for its carbon capture and storage hubs along the US Gulf Coast.

(Source: Hart Energy)

CCUS Commercial Scale, Exxon Mobil’s Execution Challenge

While the underlying technologies for both carbon capture and geologic storage are mature and have been deployed for decades, Exxon Mobil’s primary challenge lies in executing the integration of these components at an unprecedented commercial scale. The goal is to create not just a series of projects but a new, reliable, service-based infrastructure network for the energy industry.

- In the period from 2021 to 2024, the focus for many in the industry was on piloting capture technologies or using CO 2 for enhanced oil recovery, which Exxon Mobil has done for decades. The technology components were proven in isolation.

- The strategic shift from 2025 onward is from component-level maturity to system-level integration at massive scale. The core challenge is no longer the capture chemistry but building and operating a multi-user transportation and storage network with the reliability of a utility. This involves complex logistics, permitting, and long-term reservoir management.

- The company’s target to capture 4 million tons of CO 2 annually from new facilities starting in the 2026-2027 timeframe serves as a critical near-term test. Meeting this goal would validate its ability to manage the immense logistical and execution risks associated with scaling this new business line. While other companies like Hyundai and Aircapture are working on novel capture technologies, Exxon Mobil’s focus is on deploying proven solutions at scale.

Carbon Capture Technologies Compared by Maturity

The chart directly illustrates the ‘Execution Challenge’ by comparing the technological maturity of various carbon capture methods, highlighting that many are not yet at a commercial scale, which is the core challenge for Exxon Mobil.

(Source: C&EN – American Chemical Society)

SWOT Analysis, Exxon Mobil’s CCUS Strengths and Policy Risks

Exxon Mobil’s formidable engineering capabilities and financial scale position it as a credible leader in the emerging CCUS market, but this strength is counterbalanced by an acute dependency on external policy support. This makes regulatory and political stability the single most critical variable determining the success of its multi-billion-dollar strategy.

- Strengths in project management and subsurface geology are being leveraged to build a first-mover advantage.

- Weaknesses include high capital intensity and long project lead times, making the business vulnerable to market cyclicality.

- Opportunities are centered on creating a new, stable, fee-based revenue stream from industrial decarbonization, a market projected to be worth over $30 billion by 2035.

- Threats are dominated by policy risk, as demonstrated by recent political volatility and funding cancellations.

Table: SWOT Analysis for Exxon Mobil’s CCUS Business

| SWOT Category | 2021 – 2024 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Leveraged extensive engineering, project management, and subsurface geology expertise from core oil and gas business. | Applied expertise to secure tangible projects like the Gulf Coast hub and sign anchor partners like CF Industries. | The company’s core competencies were validated as directly transferable and effective in establishing a market-leading position. |

| Weaknesses | Business model was theoretical and exposed to high capital costs and long payback periods. Public and investor skepticism was high. | Moderated investment from a potential $30 B to ~$20 B, showing sensitivity to returns and an unwillingness to over-commit capital without policy certainty. | The weakness of capital intensity was confirmed, forcing a more cautious, staged investment approach contingent on de-risking factors. |

| Opportunities | The CCUS market was projected to grow, driven by net-zero targets and the potential for new, fee-based revenue streams. | Market growth forecasts solidified, with projections showing a path to a $30 B+ market by 2035. Competitors like Occidental and Shell also advanced plans, validating the market’s potential. | The market opportunity was validated by competitor actions and increasingly bullish market research, confirming the strategic rationale. |

| Threats | The primary threat was theoretical: potential changes to the 45 Q tax credit or a negative shift in the political climate for decarbonization. | The threat became real with the DOE’s cancellation of $3.7 B in grants, creating a tangible example of political and policy risk that could derail projects. | The theoretical policy risk was validated as a clear and present danger to the business model, shifting it from a hypothetical concern to a core strategic consideration. |

Exxon Mobil 45 Q Dependency, What to Watch in 2026 and Beyond

The trajectory of Exxon Mobil’s entire carbon capture business in the coming years will be dictated almost exclusively by the legislative and regulatory stability of the Section 45 Q tax credit. Any material changes to this incentive represent the most significant near-term risk and would force an immediate strategic reassessment.

- If the 45 Q tax credit of $85/ton remains stable or its terms are extended, watch for Exxon Mobil to accelerate Final Investment Decisions (FIDs) on its Gulf Coast hub components and announce additional long-term offtake agreements with industrial partners. This would signal confidence in the long-term economics of the business.

- If political momentum builds to reduce, phase out, or repeal the 45 Q credit, watch for a swift and public moderation or pause in Exxon Mobil’s low-carbon capital expenditure. Capital would likely be reallocated to shorter-cycle, higher-return traditional upstream oil and gas projects.

- A key operational signal to monitor is the physical progress on the 900-mile Gulf Coast pipeline network. Steady progress on permitting and construction would validate the company’s ability to execute complex infrastructure projects. Significant delays could indicate unforeseen execution headwinds or permitting challenges, adding risk to the timeline.

- Finally, watch for new commercial agreements beyond the initial anchor tenants. The ability to sign up a diverse portfolio of industrial customers across different sectors will be a key indicator of market traction and the broad acceptance of the CCUS-as-a-service model. The actions of financial institutions like TD Bank and corporate buyers like Microsoft in the broader carbon removal market will also serve as a bellwether for corporate demand.

The questions your competitors are already asking

This report covers one angle of Exxon Mobil’s $100 billion bet on carbon capture. The questions that matter most depend on your work.

- What is the outlook for the US 45Q tax credit, and how does its stability impact Exxon Mobil’s CCUS project economics?

- Exxon Mobil investments and funding. Is the company’s $20 billion plan on track to meet its 4 million tonne capacity target by 2026?

- What is actually happening with Exxon Mobil’s Gulf Coast CCUS hub since the CF Industries deal was announced?

- Which industrial operators on the Gulf Coast are signing up for Exxon Mobil’s carbon capture and storage services?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.