Top 10 Enhanced Geothermal Companies: Fervo’s 320 MW SCE Deal, $0.82 B Revenue (2024-2025)

The geothermal energy sector is undergoing a critical transformation, pivoting from a niche renewable to a cornerstone of 24/7 clean baseload power. This shift is driven by the immense electricity appetite of data centers and artificial intelligence, creating a clear division in the market. The industry’s leadership in 2024 and 2025 is defined by two distinct groups: established, vertically-integrated operators who command global capacity, and next-generation pioneers who are commercializing Enhanced Geothermal Systems (EGS) through landmark deals. Key signals include Fervo Energy’s record-breaking 320 MW Power Purchase Agreement (PPA) with Southern California Edison and the CTR and Baker Hughes partnership for a 500 MW project aimed directly at data centers. The dominant theme for 2025 is the de-risking and bankability of advanced geothermal, as major technology companies and utilities sign large-scale contracts that validate EGS as a scalable, firm power solution.

1. Ormat Technologies Partners with SLB for EGS

Company: Ormat Technologies

Installation Capacity: 1, 268 MW (geothermal and solar)

Applications: Grid-scale power generation, EGS development

Source: SLB and Ormat Partner to Accelerate Integrated Geothermal Asset …

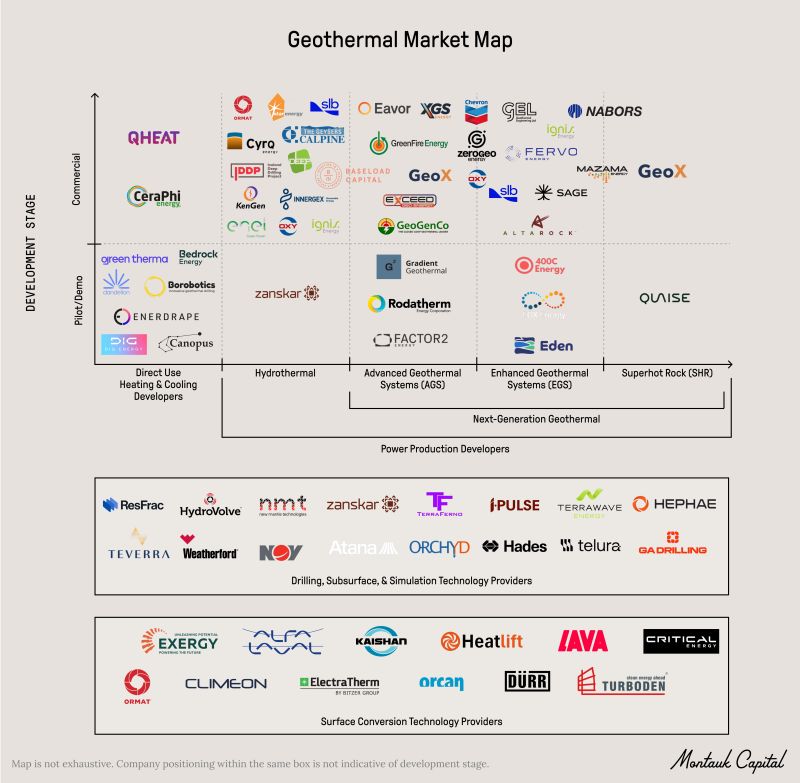

Geothermal Market Mapped by Technology and Stage

The section discusses a partnership between Ormat and SLB to advance Enhanced Geothermal Systems (EGS). This chart provides essential context by mapping out various geothermal technologies, including EGS, and classifying their current commercial or developmental stage, illustrating the landscape in which this partnership operates.

(Source: LinkedIn)

2. Calpine Corporation Operates World’s Largest Complex

Company: Calpine Corporation

Installation Capacity: 1, 520 MW

Applications: Baseload power from The Geysers complex

Source: Is Geothermal the Next Focus for Renewable Energy Venture?

US Leads Global Geothermal Capacity in 2024

The section highlights Calpine Corporation’s operation of the world’s largest geothermal complex, The Geysers, which is located in the US. This chart directly reflects the impact of such large-scale operations, showing the US as the global leader in geothermal capacity.

(Source: ScienceDirect.com)

3. Enel Green Power Maintains Global Portfolio

Company: Enel Green Power

Installation Capacity: 800 MW

Applications: Global renewable energy production

Source: Ten of the world’s largest renewable energy projects

Global Energy Demand to Grow 10-20% by 2050

The section focuses on Enel Green Power’s global portfolio. This chart, showing projected growth in global energy demand, provides the high-level strategic context for why a company like Enel maintains a diverse, worldwide portfolio of energy assets, including geothermal.

4. Pertamina Leads in Indonesia’s 2.6 GW Market

Company: Pertamina Geothermal Energy (PGE)

Installation Capacity: Operator in a market with 2.6 GW installed

Applications: National baseload power generation

Source: Think Geo Energy’s Top 10 Geothermal Countries 2024 – Power

5. Ken Gen Powers Kenya with Geothermal

Company: Ken Gen (Kenya Electricity Generating Company)

Installation Capacity: Total portfolio of 1, 904 MW (geothermal is a major share)

Applications: National electricity supply

Source: Ken Gen Illuminates Energy Landscape with Geothermal and …

US Leads Top 10 Geothermal Nations

The section is about KenGen’s role in powering Kenya with geothermal energy. As Kenya is one of the top 10 geothermal producers globally, this chart contextualizes Kenya’s position within the leading group of geothermal nations.

(Source: Energy Central)

6. Energy Development Corp. in the Philippines

Company: Energy Development Corporation (EDC)

Installation Capacity: Operator in a market with over 1.9 GW installed

Applications: Baseload power in a mature geothermal market

Source: Geothermal Energy: What it is, its History and Benefits | Enel Group

US Leads Top 10 Geothermal Nations

The section discusses the Energy Development Corporation in the Philippines. This chart is relevant because the Philippines is a top global producer of geothermal energy, and the visual helps to place the nation’s contribution in a worldwide context.

(Source: ThinkGeoEnergy)

7. Fervo Energy Signs World’s Largest Geothermal PPA

Company: Fervo Energy

Installation Capacity: 320 MW (PPA with SCE)

Applications: Clean firm power for utilities, EGS validation

Source: Fervo Energy Announces 320 MW Power Purchase Agreements …

Geothermal VC Funding Lags Behind Nuclear

This section announces Fervo Energy’s landmark PPA, a major commercial milestone. The chart on venture capital funding provides context to the financial landscape, highlighting that while commercial deals are happening, the underlying investment environment for new geothermal technology has challenges compared to other sectors, making Fervo’s success more notable.

(Source: Montauk Capital – Substack)

8. CTR and Baker Hughes Launch 500 MW Project for AI

Company: CTR and Baker Hughes

Installation Capacity: 500 MW

Applications: Powering data centers and AI growth

Source: CTR and Baker Hughes Join Forces on 500 MW Geothermal Project …

9. XGS Energy and Meta Announce 150 MW Project

Company: XGS Energy and Meta

Installation Capacity: 150 MW

Applications: Clean, firm power for corporate carbon-free goals

Source: XGS Energy and Meta to Partner on 150 MW Advanced Geothermal …

Tech Giants Partner on Geothermal Projects

The section describes a specific partnership between XGS Energy and Meta. This chart perfectly illustrates the broader trend of which this partnership is a part, showing that multiple tech giants are now engaging with geothermal energy providers.

(Source: Information Technology and Innovation Foundation (ITIF))

10. Toshiba Supplies World’s Largest Geothermal Turbine

Company: Toshiba

Installation Capacity: 184 MW (single turbine for Tauhara II plant)

Applications: Manufacturing of geothermal turbines and equipment

Source: New Zealand’s Tauhara Geothermal Power Station – Comes Online

Geothermal Technologies Compared by Type and Cost

The section focuses on Toshiba supplying the world’s largest geothermal turbine. This chart explains the different types of geothermal power plants (like Flash Steam or Binary Cycle) where such turbines are a critical component, providing technological context for the announcement.

Table: Geothermal Company Projects and Capacity (2024-2025)

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Ormat Technologies | 1, 268 MW | Grid-scale power generation, EGS development | SLB and Ormat Partner to Accelerate Integrated Geothermal Asset … |

| Calpine Corporation | 1, 520 MW | Baseload power from The Geysers complex | Is Geothermal the Next Focus for Renewable Energy Venture? |

| Enel Green Power | 800 MW | Global renewable energy production | Ten of the world’s largest renewable energy projects |

| Pertamina Geothermal Energy (PGE) | Operator in 2.6 GW market | National baseload power generation | Think Geo Energy’s Top 10 Geothermal Countries 2024 – Power |

| Ken Gen | 1, 904 MW portfolio | National electricity supply | Ken Gen Illuminates Energy Landscape with Geothermal and … |

| Energy Development Corporation (EDC) | Operator in 1.9 GW market | Baseload power in a mature geothermal market | Geothermal Energy: What it is, its History and Benefits | Enel Group |

| Fervo Energy | 320 MW (PPA) | Clean firm power for utilities, EGS validation | Fervo Energy Announces 320 MW Power Purchase Agreements … |

| CTR and Baker Hughes | 500 MW | Powering data centers and AI growth | CTR and Baker Hughes Join Forces on 500 MW Geothermal Project … |

| XGS Energy and Meta | 150 MW | Clean, firm power for corporate carbon-free goals | XGS Energy and Meta to Partner on 150 MW Advanced Geothermal … |

| Toshiba | 184 MW (turbine) | Manufacturing of geothermal turbines and equipment | New Zealand’s Tauhara Geothermal Power Station – Comes Online |

500 MW, CTR and Baker Hughes Target AI Data Centers

The primary application driving geothermal’s resurgence is the need for clean, 24/7 baseload power for digital infrastructure. The partnership between CTR and Baker Hughes to develop a 500 MW project explicitly for data centers and AI, announced in September 2025, is the clearest signal of this trend. It follows a pattern set by Fervo Energy’s initial 3.5 MW EGS project with Google and is amplified by the XGS Energy and Meta partnership for a 150 MW project. This shift from general grid support to dedicated power for high-value, high-demand industrial clients indicates that geothermal’s high capacity factor (over 98%) is its most valuable asset in a market grappling with the intermittency of other renewables.

USA vs. Indonesia, Pertamina’s 2.6 GW National Capacity

The geographic distribution of geothermal leadership reveals two parallel paths to scale. On one hand, nations with abundant conventional hydrothermal resources continue to lead in installed capacity. Indonesia, with 2.6 GW of capacity, is the world’s second-largest market, where operators like Pertamina Geothermal Energy are dominant. Similarly, the Philippines (1.9 GW, with Energy Development Corporation) and Kenya (where Ken Gen is a major producer) rely on these established resources. On the other hand, the United States is leading the technology-driven expansion of Enhanced Geothermal Systems. Projects from Fervo Energy in Nevada, CTR in California, and XGS Energy in New Mexico show that EGS is unlocking geothermal potential in new regions, driven by innovation and demand from domestic tech companies.

EGS Commercialization, Fervo Energy’s 320 MW PPA

The recent commercial activity provides a clear view of technological maturity. Established operators like Calpine Corporation (1, 520 MW) and Ormat Technologies (1, 268 MW) represent the mature, highly reliable conventional geothermal model. Their scale is built on decades of developing high-quality hydrothermal sites. In contrast, companies like Fervo Energy are proving the commercial viability of EGS. Its 320 MW PPA with Southern California Edison, announced in June 2024, is a landmark event, moving EGS from demonstration to utility-scale deployment. The reaction from incumbents, such as Ormat’s partnership with oilfield services giant SLB in October 2025 to pursue EGS, confirms that the next generation of geothermal technology has arrived and is now a competitive necessity.

Fervo Energy $255 M Funding for EGS Deployment (2025)

The critical strategic action for the geothermal sector in the year ahead is the standardization of EGS drilling and development to rapidly drive down costs and accelerate deployment. The goal is to create a “manufacturing” model akin to the shale revolution, enabling predictable and scalable project execution. Success will be determined by which companies can most effectively transfer oil and gas expertise to create geothermal reservoirs on demand.

- The $255 million capital raise by Fervo Energy in January 2025 is a direct injection of funds intended to scale its proven horizontal drilling technology and replicate its pilot success at a commercial level.

- The CTR and Baker Hughes partnership announced in September 2025 is a strong signal of this convergence, pairing a project developer with a global leader in drilling and completions technology.

- Ormat’s decision to partner with SLB in October 2025 validates this trend from the incumbent side, showing that even the largest traditional players recognize the need for oilfield services expertise to compete in the EGS market.

- Corporate demand, exemplified by the XGS Energy and Meta project announced in June 2025, provides the crucial bankability for these first-of-a-kind, large-scale EGS projects, ensuring a ready market for the power they produce.