AI Infrastructure Energy Demand, $7 T Data Center Investment, $690 B Hyperscaler Spend, and 165% Power Demand Growth (2024 to 2030)

The U.S. convertible bond market is experiencing a record-breaking surge, driven by the unprecedented capital demand of the artificial intelligence sector. This financial trend is a direct consequence of the AI revolution’s immense physical requirements, which include a multi-trillion-dollar buildout of energy and data center infrastructure. Companies are using convertible debt to fund this expansion, fundamentally reshaping capital flows into the energy and technology sectors.

AI Energy Demand Risks, Surging Data Center Power Needs and Grid Constraints

The AI infrastructure buildout is creating an unprecedented, non-cyclical demand for energy, shifting the primary risk for data center growth from capital availability to physical power and grid capacity.

- Before 2025, data center energy use was a known but manageable factor in utility planning. The rapid commercialization of AI has created a step-change in demand, with forecasts from September 2024 projecting that data center electricity consumption will surge by 4 to 10 times by 2030.

- This has inverted the primary constraint on growth. While funding was a key hurdle in the 2021-2024 period, the convertible bond market’s boom, with issuance doubling year-over-year to $34 billion in early 2026, shows capital is now abundant. The new bottleneck is power availability and grid interconnection queues, which are causing significant development delays.

- The scale of this energy demand is forcing technology companies to become de facto energy investors. Hyperscalers could spend over $1 trillion on the power infrastructure required to support their AI ambitions, moving beyond simple power purchase agreements to directly financing new generation and grid upgrades.

- This dynamic is creating a new investment super-cycle in the energy sector itself. The immense power needs are accelerating investment in reliable, 24/7 generation, with natural gas M&A activity climbing 25% in 2024 to approximately $20 billion, driven by AI-related demand.

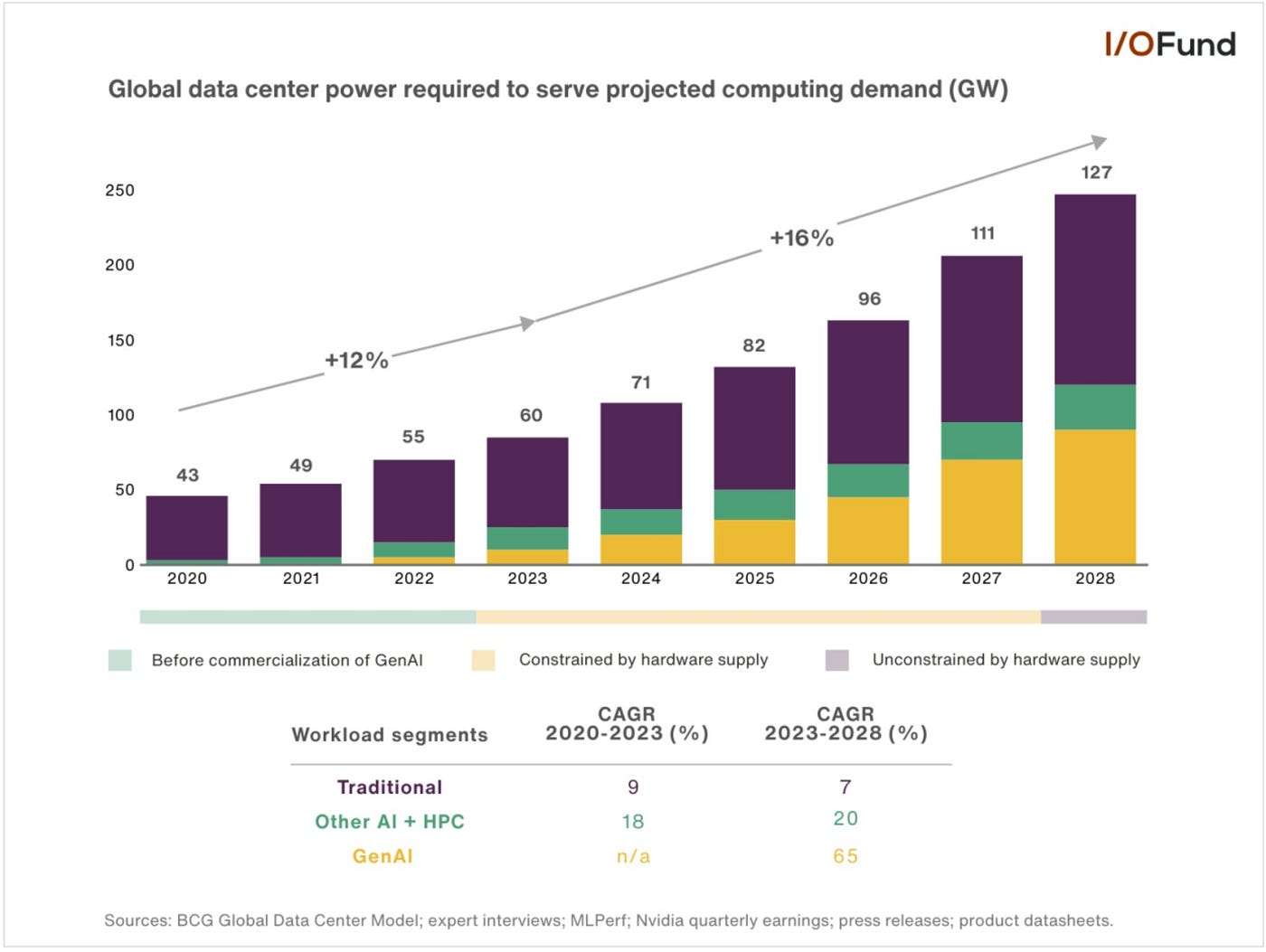

GenAI to Drive Surge in Data Center Power

This chart directly visualizes the core theme of the section, illustrating the projected surge in power consumption by data centers driven by GenAI, which aligns perfectly with the section’s focus on ‘AI Energy Demand Risks’ and ‘Surging Data Center Power Needs’.

(Source: Beth Kindig – Medium)

$7 T Investment Forecast, AI Data Center CAPEX and Convertible Bond Financing

The AI sector is driving a multi-trillion-dollar capital expenditure cycle, leveraging the convertible bond market as a preferred tool to fund this rapid expansion due to its cost-effectiveness in a higher interest rate environment.

- Projections for AI-related infrastructure spending are at a historic scale, with firms like Mc Kinsey forecasting $5.2 trillion for AI-specific data centers alone and KKR projecting up to $7 trillion for the total data center build-out by 2030.

- The convertible bond market has become a primary vehicle for this fundraising. Issuance volume in the third quarter of 2025 was up 174% compared to the same period in 2024, with AI-related deals constituting 50% of U.S. convertible issuance since August 2025.

- Major technology companies are raising billions through these instruments. Recent examples include Akamai‘s $3.0 billion offering and Nebius Group‘s $2.75 billion deal, both of which featured 0% coupons, highlighting strong investor appetite and the efficiency of this financing method for high-growth firms.

Hyperscaler Capex Map for 2026 AI Buildout

The chart’s focus on ‘Hyperscaler Capex’ and ‘AI Buildout’ provides a specific, forward-looking data point that perfectly complements the section’s discussion of a ‘$7 T Investment Forecast’ and ‘AI Data Center CAPEX’.

(Source: The Business Engineer)

Table: Recent AI & Energy-Related Convertible Bond Offerings

| Company / Announcement Date | Market Segment | Details and Strategic Purpose | Source |

|---|---|---|---|

| Akamai (May 19, 2026) | Data Center/Cloud | Raised $3.0 billion with a 0% coupon and a conversion premium between 35.0% and 42.5%, using the proceeds to fund its expanding cloud and data center footprint. | Stock Titan |

| Advanced Energy (May 16, 2026) | Power Systems/Semiconductors | Announced a $1.0 billion offering of 0% convertible notes to reshape its debt profile and provide capital for growth driven by semiconductor and data center demand. | Yahoo Finance |

| Liberty Energy (Feb 4, 2026) | Energy Services | Priced an upsized $700 million private debt offering with a 0% coupon, providing capital for expansion to meet rising energy demand. | Fidelity |

| Nebius Group (Sep 10, 2025) | Cloud/AI Infrastructure | Priced an upsized private offering of $2.75 billion in convertible senior notes to fund its expansion in AI and cloud infrastructure. | Nebius Group |

US Market Focus, AI Infrastructure’s Concentration of Capital and Energy Demand

The AI infrastructure boom and its associated capital market activity are heavily concentrated in the United States, which is creating intense, localized pressure on regional energy grids and supply chains.

- The U.S. convertible bond market is the epicenter of this financing trend. It saw issuance reach $117 billion in 2025 and is on a record pace for 2026, significantly outpacing other regions and demonstrating its central role in funding the AI buildout.

- This financial concentration reflects the physical concentration of AI development. Aggregate annual AI infrastructure commitments from the top five U.S. tech giants are projected to hit $690 billion in 2026, with the majority of this capital deployed domestically.

- This domestic focus attracts global supply chain investments, such as SK Hynix‘s plan for a $3.87 billion advanced packaging plant in Indiana, reinforcing the U.S. as the central hub for the entire AI hardware and data center ecosystem.

- The U.S. regulatory environment further distinguishes it. The SEC’s proposed rescission of its climate disclosure rule in May 2026 reduces a federal reporting burden for energy-intensive projects, potentially making development more straightforward compared to regions with stricter mandates, although state-level rules persist.

Chart Shows Explosive Growth in Installation and Electricity

This chart quantifies the ‘Explosive Growth’ in electricity usage, which directly supports the section’s focus on the ‘Concentration of Capital and Energy Demand’ resulting from the AI infrastructure boom, a trend heavily centered in the US market.

(Source: Beth Kindig – Medium)

Financing Technology Maturity, Convertible Bonds as a Commercial-Scale Tool for AI Expansion

Convertible bonds have matured from a niche financing instrument into a mainstream, commercial-scale tool used by large-cap technology firms to fund the AI infrastructure buildout, signaling a strategic validation of this hybrid security.

- During the 2021-2024 period, convertible bonds were regaining favor but were not yet the dominant instrument for large-scale tech funding. The market was characterized by a recovery from earlier dips rather than the explosive growth seen today.

- From 2025 onward, the instrument has been adopted at an unprecedented scale. Global issuance hit a 24-year high in 2025 at approximately $166.5 billion, driven by its appeal to both issuers and investors in a higher interest rate environment.

- The structure of the instrument has been refined for efficiency. Issuers now consistently achieve low or zero-coupon rates and high conversion premiums, such as the 35.0% to 42.5% premium in Akamai’s recent deal, making it more efficient than straight debt or equity offerings.

- Investor appetite has matured alongside issuer demand. The strong performance of U.S. convertible bonds, which outperformed the S&P 500 through October 2025, demonstrates a robust and well-understood market for these hybrid securities.

SWOT Analysis, The AI-Energy Nexus and Convertible Bond Financing

The AI-driven boom in convertible bonds presents a powerful financing mechanism for a historic infrastructure buildout, but it also introduces significant concentration risk tied to the performance of the tech sector and the physical constraints of the energy grid.

- The primary strength is the instrument’s ability to provide lower-cost capital for the massive AI buildout.

- A key weakness is the high concentration in the AI sector, creating systemic refinancing risk if the equity boom falters.

- The major opportunity is the convergence of tech and energy finance, driving a new super-cycle of investment in power generation.

- The most significant threat shifts from financial market volatility to the physical limitations of the energy grid.

Investment Activity in AI Energy Provider Stock

The chart illustrates investment trends in ‘AI Energy Provider Stock,’ providing a tangible data point for the ‘AI-Energy Nexus’ that is the subject of the section’s SWOT analysis. It highlights the investor interest and opportunities in this space.

(Source: Beth Kindig – Medium)

Table: SWOT Analysis for the AI-Driven Convertible Bond Market

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Flexible financing tool for post-pandemic growth; lower coupons than traditional debt. | Primary, multi-billion dollar funding mechanism for AI. Issuers achieve 0% coupons and high conversion premiums (30%+). Strong investor demand. | Validated as a mainstream, large-scale financing instrument for large-cap technology companies. |

| Weaknesses | Perceived complexity; smaller investor base compared to straight debt markets. | High concentration in the AI sector. Significant refinancing risk if stock prices fail to exceed conversion thresholds, creating a “wall of debt.” | Risk profile shifted from instrument-specific complexity to sector-specific concentration and refinancing exposure. |

| Opportunities | General corporate financing and refinancing in a recovering economy. | Funding a multi-trillion-dollar AI infrastructure super-cycle. Driving a parallel investment boom in energy generation to meet demand. | The scale of opportunity magnified from corporate growth to funding a generational infrastructure transformation across tech and energy. |

| Threats | Rising interest rates making straight debt more competitive; general market volatility. | Physical constraints (power availability, grid bottlenecks) are the primary threat. A downturn in the AI equity boom could trigger a financing crisis. | Threats evolved from purely financial (market rates) to physical and systemic (grid capacity, AI bubble risk). |

Scenario Modelling, AI Energy Demand and Project Finance Innovation

The critical path forward involves de-risking the massive energy infrastructure buildout required for AI, which will likely necessitate a convergence of financing models that blend the speed of corporate finance with the long-term stability of project finance.

- If the AI equity rally and associated capital raising continue, watch for hyperscalers to become direct equity partners in new power generation projects, moving beyond PPAs to secure their long-term energy supply and control costs.

- If grid interconnection queues remain a primary bottleneck, watch for a surge in demand for on-site power solutions and microgrids for data centers, potentially funded by new asset-backed securities or “green” convertible bonds tied to specific sustainable energy projects.

- If a downturn in the technology sector occurs, watch for a potential “stranded asset” crisis, affecting not only data centers but also the energy projects that were greenlit based on now-unrealized demand, forcing a rapid reassessment of infrastructure debt risk.

- These could be happening: Energy companies and utilities may begin issuing their own convertible or equity-linked securities to fund the rapid deployment of new power assets, adopting financing tools from their new, fast-moving customer base to accelerate development timelines.

AI Boom Drives Unprecedented Semiconductor Growth

Semiconductor growth is a leading indicator for the scale of AI infrastructure buildout. This chart provides a foundational data trend that would be a critical input for the ‘Scenario Modelling’ of future ‘AI Energy Demand’ discussed in this section.

(Source: ISI Markets)

The questions your competitors are already asking

This report covers one angle of the US convertible bond market’s role in financing the AI-driven energy and data center buildout. The questions that matter most depend on your work.

- What is the outlook for data center power infrastructure deployment to meet the projected 165% demand growth by 2030?

- What are the opportunities for energy companies and utilities in the $1 trillion hyperscaler power infrastructure market?

- Which sectors are best positioned to capture value as the primary bottleneck for data center growth shifts from capital to power availability?

- Hyperscaler activities in direct energy infrastructure investment. Are they moving beyond power purchase agreements to directly financing new generation?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.