Hydrogen Bus Fleets 2026: 127 Bologna Buses, 500 Ballard Modules, and 14 Commercial Agreements

Hydrogen Bus Commercial Scale Deployments and Key Risks

Hydrogen Bus Commercial Scale Deployments and Key Risks

In 2026, the global hydrogen bus market is defined by a strategic division: large-scale, subsidy-driven fleet deployments are accelerating in Europe, while North America advances through significant pilot programs and foundational infrastructure investments. This contrasts with the 2021-2024 period, which was characterized by smaller-scale trials and technology validation. Now, the focus has shifted to operationalizing large fleets and confronting the economic realities of fuel costs and infrastructure maintenance, as highlighted by both successful deployments and notable failures.

- Between 2021 and 2024, hydrogen bus projects were largely exploratory pilots. In 2026, the market has moved to significant commercial orders, exemplified by Bologna, Italy’s plan to roll out 127 hydrogen-powered buses starting in May 2026, one of Europe’s largest single deployments.

- The failure of Aberdeen’s pioneering hydrogen bus fleet in 2026 provides critical, negative operating data. The project was abandoned due to unsustainable hydrogen fuel costs reaching £25 per kilogram and refueling station maintenance costs equating to 30% of the initial capital expenditure annually.

- In North America, the transition is moving from concept to reality. The Victor Valley Transit Authority (VVTA) in California unveiled 13 new hydrogen fuel cell buses in January 2026, supported by a new fueling station, indicating a move towards establishing operational ecosystems.

- The scale of ambition is clear in Asia, where Foshan, China, operates the world’s largest municipal fleet with over 1, 000 hydrogen buses, supported by a network of 36 dedicated fueling stations. This level of maturity, established prior to 2025, serves as a benchmark for Western markets.

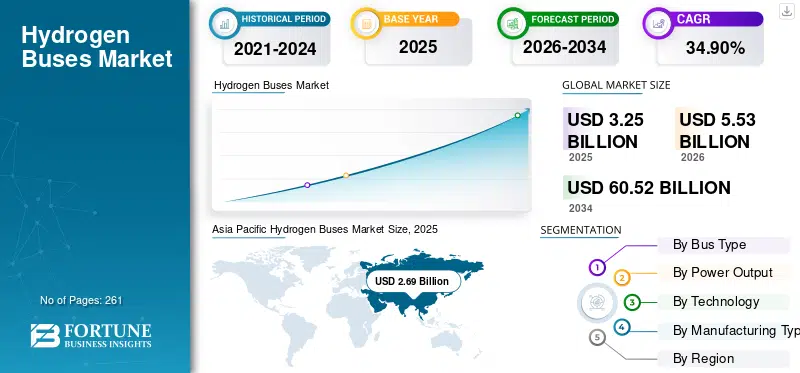

Global Market to Exceed $60B

This forecast illustrates the “commercial scale” discussed in the section by projecting explosive market growth from $5.5 billion in 2026. This quantifies the market opportunity driving large-scale deployments.

(Source: Fortune Business Insights)

$26 M in Grants, German and US Hydrogen Bus Investments

Government subsidies remain the primary financial driver for hydrogen bus adoption in 2026, directly funding both vehicle procurement and essential infrastructure projects. Unlike the broader research grants common from 2021-2024, current funding is targeted at specific, large-scale fleet deployments, with nine-figure directives and multi-million-dollar grants per project becoming standard practice to bridge the significant capital and operational cost gap between hydrogen and conventional technologies.

Table: Key Hydrogen Bus Fleet Investments and Grants (2026)

| Recipient / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ruhrbahn (Germany) | Feb 2026 | Received an €11.6 million (approx. $12.5 M) grant from the German government to acquire 52 new hydrogen buses. This subsidy of over €223, 000 per bus will expand its fleet to 78 vehicles. | Hydrogen Insight |

| Riverside Transit Agency (RTA, USA) | Jan 2026 | Awarded an $8.7 million federal grant to construct hydrogen fueling stations at its facilities in Riverside and Hemet, California, to support its future fuel cell electric bus fleet. | Riverside Transit Agency |

| German Federal Government | Spring 2026 | Scheduled to launch a new €500 million (approx. $540 M) funding directive to accelerate the scaling of hydrogen bus fleets and related infrastructure across Germany. | Ballard Power Systems |

Ballard and New Flyer 500 Fuel Cell Module Partnership

The competitive landscape in 2026 is solidifying around strategic partnerships that integrate fuel cell technology with vehicle manufacturing, creating scalable platforms for transit agencies. The most significant development is the multi-year supply agreement between Ballard Power Systems and New Flyer, which standardizes a key part of the North American supply chain. This move from bespoke, small-scale integrations seen from 2021-2024 to large, repeatable orders signals market maturation and supplier confidence.

Fuel Cell Bus Market Reaches $1.36B

The chart highlights the market context for the Ballard and New Flyer partnership, identifying them as key players in the growing fuel cell bus segment. It quantifies the market these strategic alliances are competing for.

(Source: Mordor Intelligence)

Table: Hydrogen Bus Strategic Partnerships and Alliances (2026)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ballard Power Systems & New Flyer | Mar 2026 | Ballard secured its largest-ever single order from New Flyer for 500 FCmove®-HD+ fuel cell modules (50 MW total capacity). Deliveries begin in 2026 to meet anticipated demand from U.S. and Canadian transit agencies. | Renewable Energy Industry |

| Caetano Bus & Metro of Porto | Mar 2026 | Caetano Bus is leading a consortium to operate 12 H 2.City Gold 18-meter articulated buses on a fully decarbonized Bus Rapid Transit (BRT) corridor in Porto, Portugal. This project demonstrates hydrogen’s suitability for high-capacity transit. | Caetano Bus |

| IMI plc & Stadtwerke Bielefeld | Jan 2026 | IMI supplied a 1 MW VIVO electrolyzer to a municipal utility in Bielefeld, Germany, to produce local green hydrogen for a fleet of 29 buses. This demonstrates a model of integrated, locally-sourced renewable fuel production. | Hydrogen Tech World |

Europe vs. China: Geographic Leadership in Hydrogen Bus Deployments

Geographic activity in the hydrogen bus sector is concentrated in Europe and China, but for different reasons. Europe’s growth is driven by aggressive, top-down decarbonization policies and substantial public funding, leading to major fleet orders in Italy and Germany. In contrast, China’s leadership is based on years of sustained industrial policy that has created massive scale and a dense infrastructure network, a level of maturity that Western markets are only now beginning to pursue.

Asia-Pacific Leads Hydrogen Bus Market

This chart validates the section’s discussion of geographic leadership, showing the Asia-Pacific region’s dominance (66.5%) in the 2026 market. This data supports the contrast between established Asian markets and growing Western ones.

(Source: Persistence Market Research)

- Europe is the center of policy-driven adoption. In 2026, Bologna, Italy’s 127-bus deployment and Cologne, Germany’s fleet of over 100 buses represent the region’s most significant commitments. These projects are directly enabled by national and EU-level subsidies aimed at meeting zero-emission targets.

- China remains the undisputed global leader in sheer scale. The city of Foshan alone operates a fleet exceeding 1, 000 hydrogen buses, a scale achieved through long-term state support that has fostered a complete domestic supply chain and an extensive network of 36 fueling stations.

- North America is in a nascent but growing phase, primarily centered in California. Projects like AC Transit’s plan to build a fueling station for 30 buses and VVTA’s operational 13-bus fleet in 2026 highlight a region focused on building foundational infrastructure before committing to larger-scale deployments.

- Other regions are launching strategic pilots. In 2026, Brasília launched Brazil’s first commercial green hydrogen bus, and Austria’s Villach region is deploying 36 buses fueled by a dedicated new production plant, showing that smaller nations are adopting a model of co-located production and consumption.

Hydrogen Bus Technology: Operational Viability vs. Economic Reality

Hydrogen fuel cell bus technology is operationally mature, offering range and refueling times comparable to diesel, which is a key advantage over battery-electric alternatives on demanding routes. However, the economic viability remains a significant challenge in 2026. The high cost of hydrogen fuel and the intensive maintenance requirements for refueling infrastructure create a major disconnect between the technology’s performance and its financial sustainability without heavy subsidies.

PEM Fuel Cells Dominate Bus Technology

This chart directly supports the section’s focus on technology by breaking down the market and identifying PEM fuel cells as the dominant technology (98.8%). This provides specific data on the “operationally mature” technology mentioned.

(Source: Persistence Market Research)

- From a performance standpoint, modern hydrogen buses demonstrate an operational range of 300–500 km and have proven reliable in cold weather conditions, making them a viable solution for transit agencies with long or hilly routes where battery-electric buses struggle.

- The primary barrier is fuel cost. The 2026 failure of Aberdeen’s fleet was driven by a hydrogen price of £25 per kilogram, a rate that makes operating costs far exceed those of diesel or battery-electric buses and renders the technology uncompetitive on a total cost of ownership basis.

- Infrastructure costs are another major hurdle. A fueling station for a mid-sized fleet of 20-40 buses costs between $15 million and $30 million. Furthermore, the Aberdeen case revealed that annual operations and maintenance can equal 30% of the station’s initial capital cost, a recurring expense that challenges long-term financial models.

- The supply chain for key components is maturing. Ballard Power Systems‘ landmark deal with New Flyer for 500 of its 100 k W FCmove®-HD+ modules, designed specifically for heavy-duty vehicles, indicates standardization and scaled production are underway to support the North American market.

SWOT Analysis: Hydrogen Bus Fleet Deployments (2026)

The strategic position of hydrogen buses has become clearer in 2026, with government mandates creating significant market opportunities while high operational costs pose a serious threat to long-term viability. The period from 2021 to 2024 validated the technology’s performance, but 2025-2026 has exposed its current economic unsustainability without continued public financial support.

Market Growth Rate Accelerates

This chart quantifies the “Opportunities” element of the SWOT analysis by projecting an acceleration in market growth to 29.3% CAGR. This highlights the significant market potential that government mandates are creating.

(Source: Persistence Market Research)

Table: SWOT Analysis for Hydrogen Bus Fleets (2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated long range and fast refueling in pilot projects. Performed well in extreme weather conditions where battery-electric buses faced challenges. | Operational range of up to 600 km specified in new orders (Wałbrzych, Poland). Deployed in high-capacity BRT systems (Porto, Portugal), proving suitability for demanding routes. | The operational advantages for specific use cases (long-range, high-utilization) have been validated and are now driving procurement decisions for specialized routes. |

| Weaknesses | High vehicle capital costs compared to diesel and BEVs. Limited and unreliable refueling infrastructure. Lack of operational data at scale. | Extremely high fuel costs (£25/kg in Aberdeen) and high infrastructure O&M (30% of CAPEX annually) led to fleet failure. Continued reliance on heavy subsidies (€223, 000 per bus for Ruhrbahn). | The true, unsustainable operational costs have been exposed at scale, confirming that the technology is not yet economically self-sufficient. |

| Opportunities | Growing government interest in decarbonizing public transit. Potential for green hydrogen production to lower fuel costs and emissions. | Massive government funding programs (Germany’s €500 M directive). Large-scale component orders (Ballard’s 500-unit deal) creating a more robust supply chain. Integrated production/fueling projects emerge (Kelag, Austria). | Policy has solidified into concrete, large-scale funding mechanisms, creating a protected, non-discretionary market for vehicle and infrastructure suppliers in the near term. |

| Threats | Competition from rapidly improving battery-electric bus technology. Volatility in hydrogen fuel pricing. Public perception risk from pilot failures. | High-profile fleet abandonment (Aberdeen) creates a negative precedent. Lack of a secondary market for used vehicles means scrapped assets. Long-term viability is entirely dependent on future fuel price reductions. | The risk of widespread fleet abandonments after subsidy periods end has been validated. The technology’s long-term fate depends entirely on solving the hydrogen cost equation. |

Scenario Modeling: Subsidy-Driven Growth vs. Economic Headwinds

The critical factor for the hydrogen bus market in the year ahead is the tension between government-funded expansion and severe operational cost realities. If the price of green hydrogen does not fall significantly and infrastructure reliability does not improve, the market faces a potential wave of project cancellations and fleet abandonments once initial subsidy periods expire. Watch for transit agencies in Germany and Italy to release early operating cost data from their new, large fleets, as this will serve as a crucial bellwether for the entire sector.

Market Forecasted for Explosive Growth

This aggressive forecast, projecting a 47.9% CAGR to $180B, perfectly illustrates the high-stakes “subsidy-driven growth” scenario described in the section. It quantifies the potential outcome if economic headwinds are overcome.

(Source: Straits Research)

- If this happens: New projects continue to bundle vehicle orders with long-term, fixed-price hydrogen fuel contracts and integrated, on-site production (like the IMI electrolyzer project in Germany).

- Watch this: The operational cost per mile reported by Bologna’s 127-bus fleet and Ruhrbahn’s expanding 78-bus operation. If these figures are substantially lower than Aberdeen’s, it will signal that cost issues can be managed at scale.

- These could be happening: Fuel cell suppliers like Ballard and vehicle OEMs like New Flyer will see continued order growth as public funding programs (e.g., Germany’s €500 M directive) are disbursed. However, transit agencies may begin lobbying for extended operational subsidies to cover fuel costs, shifting the financial burden from capital to recurring expenses. The heavy transportation sector will closely monitor these developments.

The questions your competitors are already asking

This report covers one angle of commercial-scale hydrogen bus fleet deployments. The questions that matter most depend on your work.

- What is actually happening with Bologna’s 127-bus hydrogen fleet deployment since the announcement?

- What does the Aberdeen data reveal about the actual cost of hydrogen fuel and refueling station maintenance for bus fleets?

- Which North American transit agencies are progressing from pilot programs to commercial-scale hydrogen bus deployments?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.