Plug Power PEM Electrolysis, 30 MW Barrow FID with Carlton Power, and 55 MW in UK Projects (2025 to 2026)

Green Hydrogen Projects: A Shift from Hype to Bankability

The green hydrogen sector is undergoing a critical transition from speculative project announcements to a focus on execution, where only projects with a clear path to bankability are advancing. The period between 2021 and 2024 was characterized by a wave of ambitious gigawatt-scale project announcements, but the subsequent era from 2025 to today has been defined by a market correction, with numerous cancellations and a new emphasis on the “trinity” of success: proven technology, government revenue support, and secured long-term offtake agreements.

- Between 2021 and 2024, the market was driven by national strategies and large-scale ambitions, with companies announcing massive projects often lacking firm offtake commitments or clear subsidy pathways.

- Starting in 2025, a wave of high-profile cancellations from major players like BP, Air Products, and Statkraft signaled a market reset. Factors like high costs, policy delays, and uncertain demand forced a pragmatic shift away from speculative ventures.

- The Final Investment Decision (FID) for Plug Power‘s 30 MW Barrow Green Hydrogen project in May 2026 exemplifies the new, successful model. It is anchored by a long-term offtake agreement with Kimberly-Clark and supported by UK government subsidy mechanisms, demonstrating a viable, de-risked path to commercial operation.

- This shift validates that mid-scale projects (10-50 MW) with co-located industrial offtakers are proving more successful than larger, more complex export-oriented hubs in the current market environment. The focus is now on industrial decarbonization in specific clusters, minimizing transportation costs and demand risk.

Plug Power’s UK Hydrogen Project Reaches FID

The chart’s reference to a project reaching a Final Investment Decision (FID) directly exemplifies the section’s theme of projects transitioning from ‘hype’ to ‘bankability’.

(Source: YouTube)

Project Cancellations: Market Reality Forces Strategic Realignments

Beginning in 2025, the green hydrogen industry experienced a significant contraction as major energy and utility companies cancelled or indefinitely postponed large-scale projects, citing unfavorable economics and a lack of clear government support. This consolidation phase filtered out speculative ventures and underscored the immense challenge of bridging the cost gap between green hydrogen and fossil fuels without robust, long-term policy and offtake certainty.

- The cancellations highlight a recurring theme: government ambition and policy announcements alone are insufficient to drive investment. Projects require tangible, bankable revenue support mechanisms, as the lack of such support was cited by Air Products for scrapping its £2 billion UK import terminal.

- Energy majors like BP made strategic pivots, cancelling green hydrogen projects in the UK and Oman. This reflects a broader trend of capital discipline where hydrogen projects must compete for funding with other, more mature energy transition technologies.

- Even utilities with strong renewable credentials, such as Statkraft, have paused new green hydrogen development, indicating that the market fundamentals and risk-reward profile remain challenging even for experienced players.

Plug Power Financials Show Deep 2026 Losses

This chart, showing significant financial losses for a major player, illustrates the ‘market reality’ forcing ‘strategic realignments’ and potentially leading to the ‘project cancellations’ discussed in the section.

(Source: Yahoo Finance)

Table: Notable Green Hydrogen Project Setbacks (2025-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| BP / H 2 Teesside | Jan 13, 2026 | Cancelled a 1.2 GW blue hydrogen project, citing land use conflicts and weak demand prospects, further clouding the UK’s hydrogen outlook. | Argus Media |

| BP / Duqm Green Hydrogen | Dec 22, 2025 | Cancelled its planned 1.5 GW green hydrogen project in Oman, marking a significant strategic withdrawal from a major international project. | [PDF] Fractal Energy Storage News |

| Scottish Power | Sep 02, 2025 | Paused the development of its renewable hydrogen projects in the UK despite having already secured subsidy agreements, signaling deep market uncertainty. | Argus Media |

| Air Products / Immingham Terminal | Jun 17, 2025 | Cancelled its £2 billion hydrogen and ammonia import terminal in the UK, explicitly blaming the lack of a supportive government policy framework for imports. | Fuel Cells Works |

| Statkraft | May 08, 2025 | Announced it would stop developing new green hydrogen projects globally, citing slow market development and persistent uncertainty. | Statkraft |

| Repsol | Feb 2025 | The Spanish energy company drastically scaled back its 2030 green hydrogen production target by up to 63%, reducing its electrolyzer capacity goal from 2.5 GW to a range of 0.7-1.2 GW. | U.S. News & World Report |

UK Policy Drives Regional Focus for Plug Power and Carlton Power

The United Kingdom has emerged as a key geography for green hydrogen development, with its clear policy frameworks and subsidy auctions creating a stable investment environment that attracts technology providers like Plug Power and developers like Carlton Power. While global ambition was widespread between 2021 and 2024, the 2025-2026 period has shown that progress is concentrated in regions with robust, bankable government support.

- From 2021 to 2024, hydrogen strategies were announced globally, but many lacked the specific mechanisms needed to de-risk private investment. The UK’s Hydrogen Production Business Model (HPBM) and its Hydrogen Allocation Rounds (HARs) moved beyond ambition to provide the revenue certainty that projects need to reach FID.

- The 30 MW Barrow project is a direct result of this supportive environment. It, along with other planned sites in Trafford and Plymouth, forms a strategic portfolio for Plug Power and Carlton Power, targeting industrial clusters to ensure offtake and minimize infrastructure hurdles.

- The UK’s success contrasts with setbacks in other regions. Air Products‘ cancellation of its UK import terminal highlights a critical policy distinction: the UK is prioritizing domestic production over imports, a strategy that benefits local projects like Barrow.

- Other European nations and regions are also advancing. Topsoe‘s inauguration of Europe’s largest SOEC factory in Denmark, Lhyfe‘s decentralized projects in France, and RWE’s large-scale offtake agreement in Germany show that tangible progress is being made where policy aligns with industrial demand.

Plug Power Confirms 30MW UK Green Hydrogen Project

The chart provides a specific example that aligns perfectly with the section’s focus on Plug Power’s activities and regional focus within the UK.

(Source: YouTube)

PEM Electrolyzer Technology Reaches Commercial Scale Amid Cost Headwinds

Proton Exchange Membrane (PEM) electrolysis has firmly established itself as a commercially mature technology (TRL 9), chosen for its operational flexibility and compact design, as demonstrated by its selection for the 30 MW Barrow project. The period from 2021 to 2024 saw PEM technology validated in smaller-scale deployments, while the 2025-2026 period is seeing it deployed at industrial scale, even as cost and material concerns remain a primary focus for the industry.

- Between 2021 and 2024, the debate often centered on the relative merits of PEM, Alkaline (AWE), and Solid Oxide (SOEC) technologies. PEM’s ability to ramp quickly to match intermittent renewable generation was identified as a key advantage for green hydrogen production.

- From 2025 onwards, the focus has shifted to execution. Plug Power‘s delivery of six 5 MW containerized PEM units for the Barrow project shows the technology is now a modular, scalable solution ready for commercial deployment. This follows earlier successes, such as the company securing a 223-project pipeline.

- The primary challenge for PEM technology remains its high capital cost, driven by the use of precious metal catalysts like iridium and platinum. This creates a significant “green premium” over both grey hydrogen and AWE systems, which use more abundant materials like nickel.

- Competitors are pushing alternative technologies forward. For example, Topsoe launched Europe’s largest SOEC manufacturing facility in October 2025, promoting its technology’s superior electrical efficiency, especially when integrated with industrial waste heat. This creates a competitive dynamic where technology choice depends on the specific project economics and operating conditions.

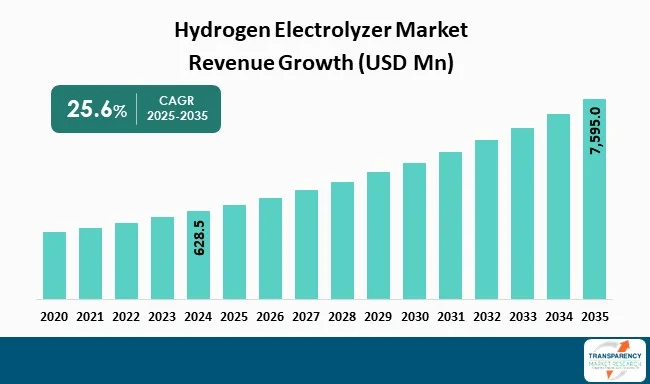

Electrolyzer Market Forecasts Strong Growth to 2035

The section discusses electrolyzer technology reaching commercial scale, and this chart provides quantitative, forward-looking data that supports the theme of market expansion and commercialization.

(Source: Transparency Market Research)

Scenario Modelling: Barrow’s Success Formula Becomes Industry Standard

The primary strategic action for the hydrogen sector in the year ahead is the replication of the “Barrow model, ” where projects are built on the foundation of secure government subsidies and binding, long-term offtake agreements with creditworthy industrial partners. If developers and technology providers can successfully assemble this trinity of success factors, the industry will see a steady flow of FIDs for projects in the 20-100 MW range. Watch for subsidy auction results and new industrial partnerships as the leading indicators of which projects will move forward.

- If offtakers like Kimberly-Clark and Total Energies continue to sign long-term, fixed-price or indexed supply contracts, this will unlock project financing for dozens of similar industrial decarbonization projects. The key signal is the willingness of industrial buyers to commit to green hydrogen despite its premium price.

- Watch the outcomes of the UK’s next Hydrogen Allocation Rounds (HAR). The volume of projects awarded and the clearing price of the subsidies will be a direct measure of the health and competitiveness of the UK’s domestic hydrogen market.

- These developments could be happening: a consolidation among project developers, with those like Carlton Power who have a proven track record of securing offtake and navigating subsidy processes becoming prime acquisition targets for larger energy companies seeking to build a hydrogen portfolio.

- The competitive landscape will intensify. As Western PEM suppliers like Plug Power build out their project portfolio, the threat of low-cost electrolyzers from Chinese manufacturers will grow, potentially putting pressure on margins and forcing a greater focus on integrated project solutions and operational services.

The questions your competitors are already asking

This report covers one angle of green hydrogen project execution and bankability. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the UK green hydrogen market?

- Is Plug Power a good investment at this stage of the green hydrogen market cycle?

- What is the outlook for PEM electrolyzer deployment in UK industrial clusters by 2030?

- Which industrial operators, besides Kimberly-Clark, are adopting green hydrogen from mid-scale UK projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.