Green Hydrogen Project Viability, $7.56 B DOE Funding Cut, $1.2 B DAC Hub Restoration, and 1 Major Policy Reversal (2025 to 2026)

Industry Risk: Policy Whiplash Stalls Hydrogen Project FIDs and Reshapes Economics

The U.S. clean hydrogen market has shifted from a period of subsidy-driven optimism to one dominated by policy risk and economic rationalization. The passage of the One Big Beautiful Bill Act (OBBBA) in July 2025 and subsequent federal funding volatility have fundamentally altered project economics, creating a stark division between the viability of green and blue hydrogen. Projects without grandfathered status under the original Inflation Reduction Act (IRA) now face a high probability of cancellation or indefinite delay due to the erosion of key incentives.

- Prior to 2025, the IRA’s $3.00/kg 45 V Production Tax Credit (PTC) was expected to make green hydrogen cost-competitive with grey hydrogen. The OBBBA’s accelerated repeal of this credit, terminating it after 2027 and requiring a “begin construction” date before July 5, 2026, eliminated the primary economic driver for new green hydrogen projects.

- The preservation of the Section 45 Q tax credit ($85/ton for industrial carbon capture) has made it the critical remaining federal incentive. This provides a direct advantage to blue hydrogen projects, which can monetize carbon capture, making them more economically viable than unsubsidized green hydrogen. A blue hydrogen project with 90% capture can realize a benefit of approximately $0.77/kg.

- The Department of Energy’s (DOE) termination of $7.56 billion in awards for 223 projects in September 2025, followed by a partial restoration of $1.2 billion in April 2026, has shattered investor confidence in public-private partnerships. This stop-start funding approach, which put major initiatives like the Hy Velocity Hub and DAC hubs at risk, makes it nearly impossible to calculate a reliable Net Present Value (NPV) for projects dependent on federal grants.

- As a result of subsidy uncertainty, the market has pivoted to prioritizing bankable offtake agreements as the most critical de-risking element. Projects without long-term contracts from creditworthy buyers, such as the 20-year agreement secured by Plug Power with Fertiglobe, struggle to reach Final Investment Decision (FID).

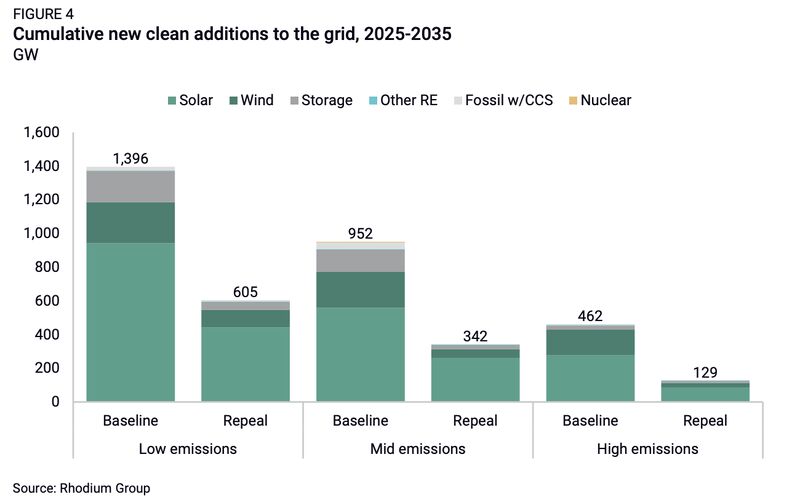

Policy Reversal Slashes Clean Energy Outlook

This chart quantifies the article’s central theme of “policy whiplash” by showing how a policy repeal can drastically cut new clean energy capacity. This directly visualizes the risk of project cancellations mentioned in the section.

(Source: LinkedIn)

Investment Volatility: The $7.56 B DOE Clawback and its Chilling Effect on Private Capital

The sharp reversal in federal funding has introduced a new level of risk for private capital, increasing the cost of capital and forcing a strategic re-evaluation of projects reliant on government support. The DOE’s actions in late 2025 demonstrated that previously awarded funds are not secure, creating a chilling effect on investments that require long-term policy stability. This has disproportionately impacted capital-intensive projects like Direct Air Capture (DAC), which are critical for both decarbonization and the validation of 45 Q credits.

- The primary financial shock came on September 30, 2025, when the DOE announced the termination of 321 financial awards across 223 projects, citing a need for “increased accountability.” This move was framed as saving $7.56 billion but simultaneously undermined the financial foundation of numerous clean energy ventures that had based their models on this committed funding.

- This uncertainty was amplified in October 2025, when reports emerged that the two largest DAC hubs, Project Cypress in Louisiana and the South Texas DAC Hub, were being considered for termination. This created months of instability for developers and their partners, including Climeworks and Battelle.

- Although the DOE restored $1.2 billion in funding in April 2026 for DAC hubs and five hydrogen projects, the damage to investor confidence was already done. The period of uncertainty caused project delays, increased borrowing costs, and forced developers to seek more expensive private financing alternatives, fundamentally altering project IRRs.

Table: Key Funding and Policy Reversals (2025-2026)

| Event | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| DOE Restores Partial Funding | April 2026 | In a reversal, the DOE restored $1.2 billion for DAC hubs and five hydrogen projects, signaling a potential but uncertain renewal of support. This left developers to manage the financial fallout from the preceding pause. | decarbonfuse.com |

| DAC Hub Funding Termination Considered | October 2025 | Reports confirmed the two largest US DAC hubs were under consideration for funding cuts, creating severe uncertainty for projects central to the 45 Q credit’s value proposition for DAC. | Carbon Herald |

| DOE Terminates 223 Projects | September 2025 | The DOE announced the termination of awards for 223 projects, saving a reported $7.56 billion. This action dismantled the financial assumptions of numerous clean energy projects. | energy.gov |

| One Big Beautiful Bill Act (OBBBA) Passed | July 2025 | The OBBBA significantly rolled back IRA incentives, notably accelerating the sunset of the 45 V hydrogen tax credit and tightening deadlines for the 45 Q carbon capture credit. | Columbia SIPA |

US Regional Focus: Blue Hydrogen Corridors Gain an Edge in the Post-IRA Landscape

The dramatic shift in federal policy has created a new geographic and technological sorting mechanism in the United States, strongly favoring regions positioned for blue hydrogen. The curtailment of the 45 V PTC has diminished the universal appeal of green hydrogen, elevating the importance of regional assets like low-cost natural gas and favorable geology for carbon sequestration. This effectively concentrates near-term hydrogen development in industrial corridors along the Gulf Coast and other areas with established fossil fuel infrastructure.

Blue Hydrogen Gains Cost and Investment Edge

The chart provides the economic data for the section’s argument, showing blue hydrogen is significantly cheaper and projected to attract far more capital than green. This directly supports the headline “Blue Hydrogen Corridors Gain an Edge”.

(Source: Enverus)

- Before 2025, the IRA framework encouraged a geographically diverse build-out of green hydrogen, driven by renewable resource availability. The OBBBA’s policy changes have now tilted the economic landscape toward states like Texas and Louisiana, which possess both extensive natural gas infrastructure and geological formations suitable for CO 2 storage, a key requirement for monetizing the 45 Q credit.

- The focus on industrial clusters where producers and offtakers are co-located has intensified. These clusters minimize the high costs and logistical risks of building new hydrogen and CO 2 transportation infrastructure, making projects within them more bankable. The viability of projects like Arcelor Mittal‘s steel decarbonization efforts increasingly depends on access to such localized hydrogen supply.

- The political and financial whiplash surrounding the DOE’s DAC and hydrogen hubs has highlighted the vulnerability of even large-scale, regionally significant projects. The uncertainty over the Texas and Louisiana DAC hubs demonstrates that even in geographies with clear strategic advantages, sovereign risk has become a primary concern for investors.

- The policy instability in the U.S. risks driving capital and technology leadership to regions with more stable and ambitious frameworks. Nations like Germany and countries with large-scale projects like those in Egypt are positioning themselves as more reliable partners for long-term investment, potentially drawing capital away from the U.S. market.

Technology Maturity: Commercial Viability, Not TRL, Is Now the Primary Hydrogen Bottleneck

While key hydrogen production technologies are commercially mature, the recent policy reversals have exposed that technological readiness is no longer the main barrier to deployment. The primary constraint has shifted to economic viability in a less certain subsidy environment. The market now faces a situation where proven technologies like alkaline and PEM electrolyzers (TRL 9) are at risk of being underutilized due to unfavorable project economics for new builds.

Hydrogen Market Enters ‘Trough of Disillusionment’

This chart perfectly illustrates the section’s argument that the bottleneck has shifted from technology to economics. It visually represents the end of the “hydrogen hype” as the market confronts the economic challenges of commercial viability.

(Source: Enverus)

- From 2021 to 2024, the industry focus was on scaling manufacturing and demonstrating the technical readiness of various electrolyzer technologies. Alkaline Water Electrolysis (AWE) and Proton Exchange Membrane (PEM) reached Technology Readiness Level (TRL) 9, confirming their suitability for large-scale deployment.

- The post-2025 reality is that the Levelized Cost of Hydrogen (LCOH) for a new green hydrogen project, at $4.50-$5.00/kg, is uncompetitive without the $3.00/kg 45 V credit. The LCOH for a blue hydrogen project benefiting from the 45 Q credit is approximately $1.43/kg, creating a clear market advantage.

- Emerging technologies like Solid Oxide Electrolyzer Cells (SOEC) and Anion Exchange Membrane (AEM) electrolyzers, which promise higher efficiency or lower costs, now face a more difficult path to commercialization. The reduction in deployment incentives slows the feedback loop of learning-by-doing that drives down costs for next-generation systems like those from Thyssenkrupp.

- This policy-induced shift creates an opening for projects that can leverage unique geological or resource advantages, such as producing hydrogen from depleted fields as proposed by companies like Eclipse Energy, which may offer a different economic profile than conventional green or blue hydrogen pathways.

2026 Scenarios: Watch for a Flight to Quality as Speculative Projects Are Culled

The U.S. hydrogen market in 2026 will be defined by a flight to quality, where only the most resilient projects survive. Investment will narrow to focus on ventures that are insulated from policy volatility. The “hydrogen hype” of the early 2020 s is over, replaced by a period of pragmatic execution and consolidation. The key signal to watch is which projects can reach a Final Investment Decision in this new, more challenging environment.

Investors Show ‘Flight to Quality’ via Late-Stage Projects

This chart exemplifies the “flight to quality” by showing strong investor interest in late-stage, de-risked projects. This represents the type of resilient, less speculative investment that will survive the market culling described in the section.

(Source: Deloitte)

- If this happens: The market will bifurcate sharply. Projects with grandfathered status under the original IRA rules will be fast-tracked to capture their value before deadlines expire. Simultaneously, a wave of cancellations and indefinite delays will hit speculative projects that were banking on the continuation of the full IRA incentives.

- Watch this: The progress of blue hydrogen projects in the Gulf Coast. Their ability to secure financing and offtake agreements will be the leading indicator of market direction. Their success will validate the thesis that 45 Q is now the most important driver of clean hydrogen investment in the U.S.

- These could be happening: Electrolyzer manufacturers may see order books shrink as green hydrogen developers pause plans. This could lead to industry consolidation or a pivot to more stable overseas markets. Conversely, carbon capture technology providers and pipeline operators aligned with blue hydrogen projects will see their market opportunity grow.

The questions your competitors are already asking

This report covers one angle of how U.S. policy volatility is reshaping the economics of green and blue hydrogen. The questions that matter most depend on your work.

- How does blue hydrogen with the $85/ton 45Q tax credit compare to unsubsidized green hydrogen on a levelized cost basis?

- What is the outlook for new green hydrogen projects to reach Final Investment Decision (FID) before the July 5, 2026 ‘begin construction’ deadline?

- Which project types are gaining or losing ground due to the policy shift from the 45V production tax credit to the 45Q carbon capture credit?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.