US Hydrogen 2026, $3/kg 45V Credit Sunset & ARCHES Hub

Blue Hydrogen Economics, Yara International’s $180/ton 45 Q Boost, and 2 Policy Shifts (2025 to 2026)

Policy Uncertainty Stalls Green Hydrogen Projects, Shifts Focus to 45 Q

The 2025 legislative overhaul via the One Big Beautiful Bill Act (OBBBA) created a stark divergence in risk profiles between green and blue hydrogen, making bankable blue hydrogen projects the primary path for near-term industrial decarbonization while stalling new green hydrogen investments. The previous IRA framework, which catalyzed broad interest in all forms of clean hydrogen from 2022 to 2024, has been replaced by a more fragmented and preferential policy environment.

- From 2021 through 2024, the Inflation Reduction Act (IRA) provided a powerful, seemingly stable incentive for green hydrogen via the Section 45 V Production Tax Credit (PTC) of up to $3.00/kg, sparking a wave of project announcements.

- In 2025, the OBBBA fundamentally altered this outlook by terminating the 45 V credit for any project starting construction after December 31, 2026, creating a significant “subsidy cliff” that chilled new investment.

- Simultaneously, the OBBBA enhanced the Section 45 Q tax credit, crucial for blue hydrogen, by increasing the value for utilization to $180 per metric ton of captured CO 2 and extending its availability, thereby providing greater long-term certainty for investors.

- This policy whiplash was compounded by the funding volatility for the US Hubs program, which saw billions in awards rescinded in late 2025 before a partial restoration in 2026, further eroding investor confidence in the stability of federal support.

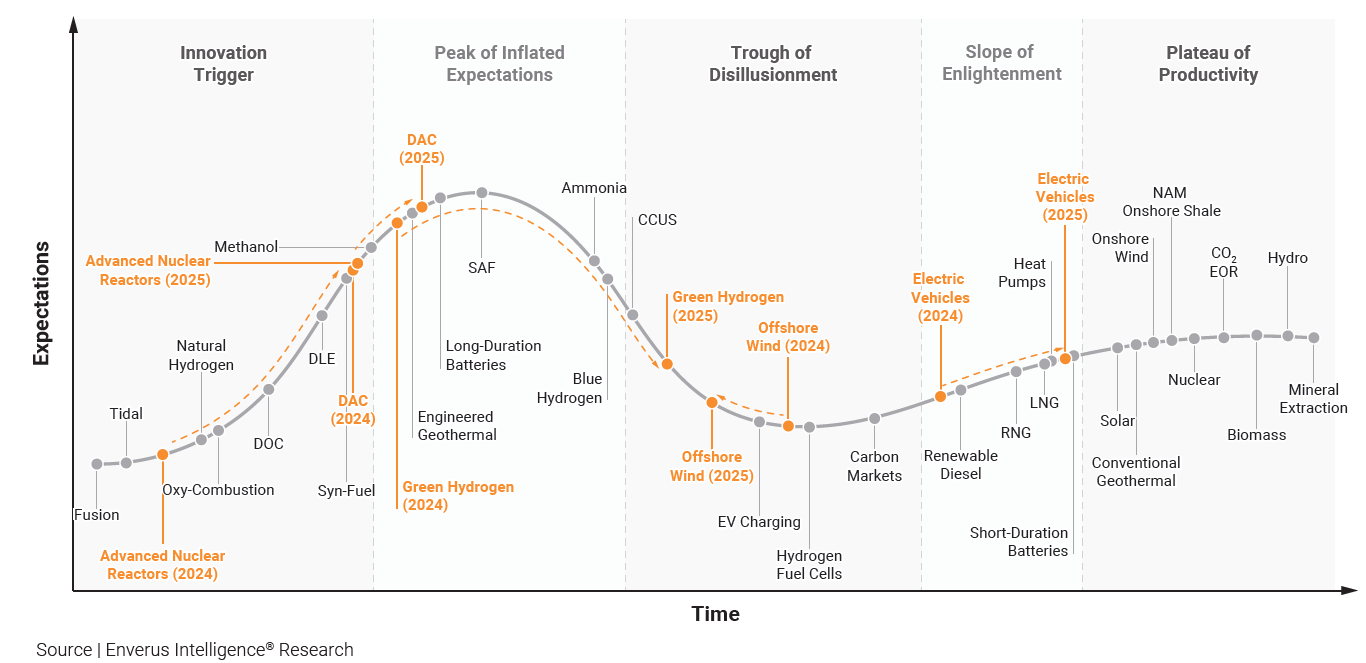

Green Hydrogen Plummets into ‘Trough of Disillusionment’

The section highlights that policy uncertainty is stalling green hydrogen projects. This sentiment is perfectly captured by the Gartner Hype Cycle terminology in the chart, indicating that initial excitement has met with challenges and disillusionment.

(Source: Enverus)

Hydrogen Hub Funding, $7.5 B in Cancellations and a Partial Reversal

Federal funding for hydrogen and Direct Air Capture (DAC) hubs experienced significant volatility starting in late 2025, with widespread cancellations followed by a partial, strategic restoration that signaled a clear preference for projects with established commercial pathways and technology readiness. This period of uncertainty caused significant project delays across the sector.

- The initial disruption occurred in October 2025 when the Department of Energy announced the cancellation of 321 financial awards, including many of the original 223 projects, totaling approximately $7.56 billion in planned federal spending.

- This action specifically impacted the hydrogen sector by rescinding $2.2 billion in awards that had been designated for the California (ARCHES) and Pacific Northwest hydrogen hubs, two regions heavily focused on green hydrogen production.

- Following a multi-month review, the DOE reversed course in April 2026, restoring funding for five of the seven original hydrogen hubs and two major DAC hubs, preserving billions in federal support but not before introducing significant delays and planning challenges for developers.

Infrastructure Energy Deals Plummet in 2024-2025

The section details specific, large-scale funding cancellations for Hydrogen Hubs. This chart provides the broader market context, showing a general downturn in energy infrastructure deals, of which the hub cancellations are a contributing factor or symptom.

(Source: LinkedIn)

US Gulf Coast, The Epicenter of Blue Hydrogen Investment Under New 45 Q Rules

While the IRA initially spurred green hydrogen interest nationwide between 2022 and 2024, the 2025 policy shift has concentrated new large-scale investment in the U.S. Gulf Coast. This region’s existing natural gas infrastructure, extensive pipeline networks, and favorable geology for carbon sequestration make it the ideal location to capitalize on the enhanced 45 Q tax credit for blue hydrogen.

- The U.S. Gulf Coast’s access to low-cost natural gas and established industrial corridors provides a significant competitive advantage for blue hydrogen production, which was further amplified by the OBBBA’s enhancement of the 45 Q credit.

- In contrast, regions like California, which were poised to lead in green hydrogen, faced setbacks. The cancellation of the $1.2 billion award to the ARCHES hub in 2025 underscored the shifting federal priorities and created a significant funding gap for West Coast projects.

- The unsubsidized cost of blue hydrogen on the U.S. Gulf Coast is already competitive at approximately $2.00/kg, and the enhanced 45 Q credit can reduce this to below $1.50/kg, making it one of the most cost-effective sources of low-carbon hydrogen globally.

- International energy firms and industrial gas producers are now prioritizing the Gulf Coast for new investment, leveraging the policy certainty of 45 Q over the truncated 45 V credit available elsewhere.

LNG Export Capacity Growth Projected Through 2030

The section identifies the US Gulf Coast as the epicenter for blue hydrogen investment. This chart, showing massive growth in LNG exports, illustrates the extensive existing natural gas infrastructure and expertise in that same region, which is a key reason why it is a hub for blue hydrogen development.

(Source: Enverus)

SMR with CCS Achieves Commercial Bankability, PEM Electrolysis Faces Headwinds

The 2025 policy changes effectively fast-tracked the commercial bankability of blue hydrogen produced via Steam Methane Reforming with Carbon Capture and Sequestration (SMR+CCS) by providing durable financial incentives. In contrast, these same changes pushed large-scale green hydrogen from electrolysis back into a phase of dependency on niche markets and further technology-driven cost reductions, as the primary federal subsidy became unreliable for long-term planning.

- The business case for SMR+CCS is now anchored by the stable, long-term 45 Q credit, making projects more attractive to debt and equity financiers. The primary variables are natural gas feedstock costs and CO 2 transport and storage availability.

- Green hydrogen from electrolysis remains highly dependent on the 45 V tax credit. The accelerated 2026 sunset for new projects makes it difficult for developers to secure the 10-15 year offtake agreements necessary for project financing.

- This has a direct impact on the manufacturing supply chain. Global electrolyzer manufacturing capacity reached 25 GW per year in 2026, but Western producers like those making PEM electrolyzers see low utilization rates of 10% to 20% due to the slow pace of Final Investment Decisions (FIDs) on large green hydrogen projects.

Blue Hydrogen More Cost-Competitive Than Green Hydrogen

The section discusses how SMR with CCS (blue hydrogen) is achieving bankability while PEM electrolysis (green hydrogen) faces headwinds. This chart directly supports that claim by visualizing the cost-competitiveness of blue hydrogen over green.

(Source: Enverus)

Hydrogen SWOT Analysis, Policy Shifts Define Strengths and Threats (2021 to 2026)

A SWOT analysis reveals that the core strength of the U.S. clean hydrogen market has shifted from the broad potential of green hydrogen under the IRA to the specific certainty of blue hydrogen under the post-2025 legislative framework. Policy instability has consequently emerged as the single greatest external threat to long-term, multi-pathway growth.

Chart Outlines Macro Trends in Energy & Infrastructure

The section provides a high-level SWOT analysis of the hydrogen market. A chart outlining macro trends in the broader energy and infrastructure sector serves as an effective introduction or contextual backdrop for this strategic analysis.

(Source: Citrini Research)

Table: SWOT Analysis for US Clean Hydrogen Economics

| SWOT Category | 2021 – 2024 (IRA Dominance) | 2025 – 2026 (Post-OBBBA) | What Changed / Validated |

|---|---|---|---|

| Strengths | Potent, technology-neutral 45 V PTC ($3/kg) made the U.S. the most attractive market for green hydrogen investment globally. | Enhanced and durable 45 Q credit ($180/ton) provides a highly bankable incentive for blue hydrogen. Existing natural gas infrastructure offers a rapid deployment pathway. | The source of market strength shifted from greenfield green hydrogen potential to brownfield-adjacent blue hydrogen certainty. |

| Weaknesses | High CAPEX for electrolyzers and reliance on new renewable energy build-out. Nascent supply chains and infrastructure for green hydrogen. | Dependence on volatile natural gas prices for blue hydrogen. Public and regulatory opposition to CO 2 pipelines and long-term storage liability. | The core weakness shifted from technology cost for green H 2 to commodity price exposure and public acceptance for blue H 2. |

| Opportunities | IRA incentives positioned the U.S. to build a dominant, vertically integrated green hydrogen supply chain from manufacturing to export. | Rapidly decarbonize existing industrial hydrogen users (refining, ammonia) with cost-competitive blue hydrogen. Leverage CCS expertise to become a global leader. | The market opportunity narrowed from transformative green energy leadership to pragmatic, near-term industrial decarbonization using existing fossil fuel infrastructure. |

| Threats | Potential for future political change to undermine the IRA. Delays in Treasury guidance for 45 V creating uncertainty. | Extreme policy volatility (e.g., OBBBA, H 2 Hub funding pause) creates massive investor risk and stalls FIDs. The 45 V “subsidy cliff” discourages new green hydrogen projects. | The theoretical threat of policy change became a realized event, validating policy risk as the primary threat to capital-intensive energy projects. |

The Blue Hydrogen Bridge, Watch Offtake Agreements for 45 Q Projects

For the next two years, the critical signal to watch is the conversion of blue hydrogen project announcements into firm, long-term offtake agreements, which will validate the bankability of the enhanced 45 Q credit and determine the pace of U.S. industrial decarbonization. The policy environment now heavily favors a “Blue Hydrogen Bridge” strategy for the remainder of the decade.

- Developers with access to natural gas and sequestration sites are expected to accelerate FIDs on blue hydrogen projects to capitalize on the certainty of the 45 Q credit, with partners like Yara International and Fertiglobe being key offtakers.

- Green hydrogen developers must now either rush to begin construction before the end of 2026 to secure the 45 V credit or pivot to smaller, niche applications where buyers are willing to pay a green premium without federal subsidies.

- International investors who were drawn to the U.S. by the IRA’s aggressive green hydrogen incentives are re-evaluating capital allocations, with some potentially redirecting investments to regions with more stable long-term green hydrogen policies, such as the EU or projects in the Middle East with partners like Thyssenkrupp.

The questions your competitors are already asking

This report covers one angle of hydrogen project economics under new US policy. The questions that matter most depend on your work.

- What is the outlook for bankable blue hydrogen projects now that the 45Q credit is $180/ton?

- How do the project economics for blue hydrogen with the $180/ton 45Q credit compare to green hydrogen facing the 45V subsidy cliff?

- What is actually happening with the US Hydrogen Hubs program after the 2025 funding cancellations and partial reversal?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.