Microsoft DAC Strategy, $1.4 B Stockholm Exergi Deal, 6.75 M Tonnes Atmos Clear, and 7 Offtake Agreements (2021 to 2025)

$1.4 B Stockholm Exergi, Microsoft CDR Commercial Projects

In 2025, Microsoft transitioned from exploratory pilot-scale purchases to a strategy of market creation, executing multi-billion-dollar offtake agreements across a diverse Carbon Dioxide Removal (CDR) portfolio to offset its own rising emissions and build a viable global market. This aggressive procurement strategy stands in direct contrast to the 2021-2024 period, which was defined by smaller, technology-proving investments. The current scale is a direct response to the company’s own operational requirements and a deliberate effort to establish the commercial foundations for a gigatonne-scale industry.

- Before 2025, Microsoft’s CDR portfolio consisted of smaller, innovative purchases designed to test a range of technologies, including early-stage Direct Air Capture (DAC) and bio-oil sequestration.

- The strategic shift in 2025 is marked by massive offtake volumes, including a $1.4 billion agreement with Stockholm Exergi for Bioenergy with Carbon Capture and Storage (BECCS), an $800 million deal with Atmos Clear for 6.75 million metric tons of BECCS removal, and an agreement for 18 million tonnes of nature-based credits via Rubicon Carbon.

- This acceleration is driven by a 23.4% surge in Microsoft‘s own emissions, primarily from the energy-intensive expansion of its AI and cloud infrastructure, creating an urgent internal need for a large and reliable supply of high-quality removal credits.

- The company’s strategy is explicitly diversified, funding multiple pathways simultaneously, including BECCS, enhanced weathering, soil carbon, afforestation, and industrial carbon capture, to build a resilient portfolio and avoid dependence on any single technology.

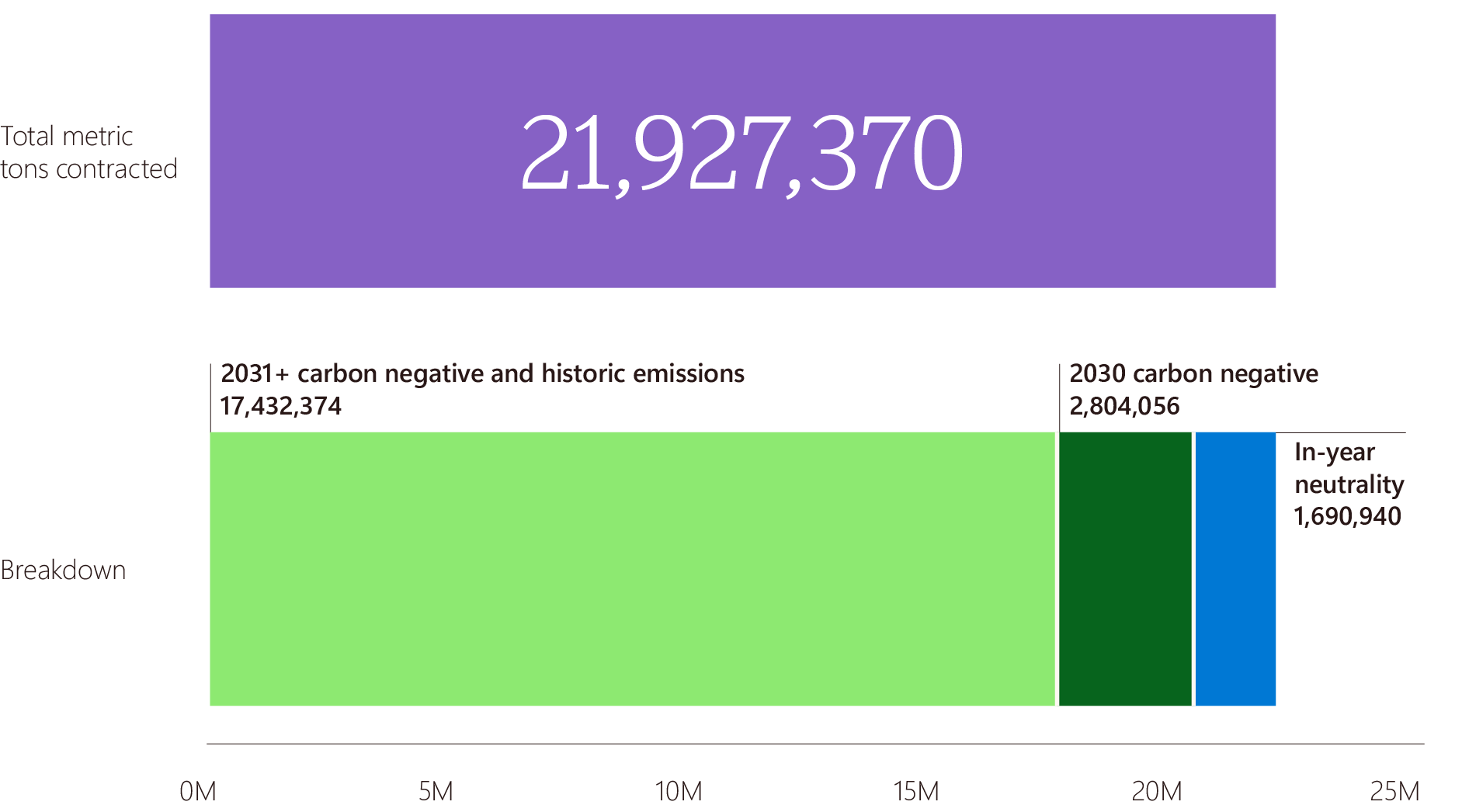

Microsoft Contracts 21.9M Tons of Carbon Removal

This section discusses Microsoft’s large-scale commercial projects, anchored by the Stockholm Exergi deal. The chart provides the total contracted volume of 21.9M tons, setting the overall scale for Microsoft’s portfolio of which the Stockholm Exergi project is a significant part.

(Source: Microsoft)

Microsoft 7 Major Investments, Atmos Clear to Agoro Carbon (2025)

Microsoft’s 2025 investment strategy uses large-scale, long-term procurement as a direct financing mechanism, providing the revenue certainty that CDR project developers require to secure the necessary capital for constructing capital-intensive facilities. These offtake agreements function as catalytic capital, de-risking projects for traditional investors and pulling nascent technologies toward commercial viability. This model is a deliberate intervention in a market where early-stage venture funding has contracted.

- The company’s Climate Innovation Fund, which had committed over $800 million across 67 investments as of September 2025, provides targeted, early-stage capital to bridge technologies toward mainstream financial backing.

- The primary investment tool in 2025 became large-scale procurement, exemplified by the $1.4 billion Stockholm Exergi deal and the nearly $800 million Atmos Clear agreement. These agreements effectively underwrite the construction of new BECCS facilities.

- Portfolio depth is demonstrated through deals like the $200 million offtake with CO 280, which supports CDR deployment in the U.S. pulp and paper industry, creating a new pathway for industrial carbon removal.

- This aggressive corporate-led financing is crucial in a cooling investment climate, as evidenced by a more than 60% drop in venture capital funding for U.S.-based DAC startups in Q 1 2025.

Microsoft Contracts 45M Tonnes of Carbon Removal in 2025

The section details Microsoft’s seven major investments for 2025. This chart’s headline figure of 45M tonnes contracted in 2025 directly quantifies the cumulative impact of these specific investments discussed in the section.

(Source: LinkedIn)

Table: Microsoft 2025 Key Carbon Removal Investments via Offtake Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Stockholm Exergi | May 2025 | $1.4 billion agreement for BECCS-based carbon removal, representing a major investment in a mature, deployable technology to secure large volumes of durable credits. | Carbon Credits |

| Atmos Clear | April 2025 | An estimated $800 million deal for 6.75 million metric tons of CO₂ removal credits from a BECCS project, setting a record for the largest single CDR offtake. | Carbon Credits |

| CO 280 | April 2025 | $200 million agreement for 3.69 million tons of CDR credits generated from capturing and storing biogenic CO₂ in the U.S. pulp and paper industry. | Resource Wise |

| Indian Afforestation Project (Vast) | March 2025 | A 30-year deal to purchase 1.5 million tonnes of credits, or 50% of the project’s total output, supporting large-scale, nature-based solutions in Asia. | ESG Today |

DAC Purchase Volume Trends from 2022-2025

While the section is a table of 2025 investments, this chart provides crucial historical context. It illustrates the growth trend of Direct Air Capture (DAC) purchases leading up to 2025, showing the momentum that culminates in the significant offtake agreements detailed in the table.

(Source: CDR.fyi)

Market Infrastructure, Microsoft 3 Strategic Partnerships

Recognizing that a functioning market requires more than just transactions, Microsoft‘s 2025 partnerships focused on constructing the market’s underlying architecture by establishing quality standards, fostering buyer coalitions, and pioneering novel financial instruments. These actions go beyond simple credit procurement and are designed to build a credible and scalable voluntary carbon market (VCM) for the long term. This represents a significant evolution from the 2021-2024 period, which was more focused on individual technology partnerships.

- The updated “Criteria for High-Quality Carbon Dioxide Removal, ” released in July 2025 with partner Carbon Direct, serves as a public playbook for the entire industry, setting rigorous benchmarks for permanence, verification, and additionality.

- By joining forces with Amazon and Exxon Mobil in February 2025, Microsoft helped form a powerful buyer’s coalition committed to contracting up to 20 million tons of nature-based credits by 2030, signaling unified demand for higher standards in the VCM.

- The creation of a $210 million carbon loan facility with JPMorgan in July 2025 introduced a sophisticated financial product to de-risk CDR projects from market price volatility, aiming to attract more conservative institutional capital.

CDR Market Purchase Volume Grows Excluding Key Players

This section focuses on building market infrastructure. The chart powerfully demonstrates the success of such efforts by showing that the market is maturing and diversifying, evidenced by its ability to grow even without its largest buyers, a key indicator of a healthy infrastructure.

(Source: CDR.fyi)

Table: Microsoft 2025 Strategic Market-Building Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| JPMorgan | July 2025 | Backed a $210 million carbon loan facility to insulate CDR projects from market volatility, creating a new model to attract project finance. | Carbon Credits |

| Carbon Direct | July 2025 | Co-developed and released updated public criteria for high-quality CDR, establishing a transparent framework for market-wide quality control. | ESG Dive |

| Amazon & Exxon Mobil | February 2025 | Formed a coalition to improve VCM standards and aggregate demand, with a collective goal to contract for up to 20 million tons of nature-based credits. | Carbon Herald |

CDR Market Growth Driven by High-Integrity Offsets

This section presents a table of strategic market-building partnerships. The chart complements it by showing that market growth is concentrated in high-integrity offsets, validating the focus and effectiveness of the partnerships listed in the table which aim to build a quality market.

(Source: CarbonCredits.com)

US vs. Europe, Microsoft CDR Geographic Focus (2025)

In 2025, Microsoft‘s procurement strategy matured into a global portfolio, diversifying geographically beyond the North American and European technology hubs that characterized its earlier investments. Major agreements were executed for projects in Europe (Sweden), the United States (industrial CDR), and Asia (India), reflecting a strategy to source removals where they are most scalable and cost-effective, leveraging regional strengths in policy, resources, and industry.

- The $1.4 billion agreement with Stockholm Exergi anchors Microsoft‘s European strategy in Sweden, leveraging the country’s district heating infrastructure and policy support for large-scale BECCS.

- The United States remains a core focus, with deals like the $200 million CO 280 offtake targeting the U.S. pulp and paper industry and the Sublime Systems agreement supporting low-carbon cement production, capitalizing on industrial integration opportunities and incentives like the 45 Q tax credit.

- A significant expansion into Asia is marked by the 30-year, 1.5 million tonne afforestation deal in India, demonstrating a commitment to large-scale, nature-based solutions in developing economies as part of a diversified portfolio.

- This global approach contrasts with the 2021-2024 period, which was more concentrated on technology developers in specific hubs like Switzerland (Climeworks) and the US, and signals a shift toward sourcing from large-scale operational projects worldwide.

US Leads in Planned Direct Air Capture Projects

The section heading explicitly mentions a ‘US vs. Europe’ geographic focus. This chart directly addresses that theme by showing US leadership in planned Direct Air Capture projects, visually representing the geographic concentration of development in this key CDR technology.

(Source: Internationale Politik Quarterly)

SWOT Analysis, Microsoft CDR Market Leadership Risks

Microsoft’s aggressive procurement strategy in 2025 solidified its position as the indispensable market-maker for the CDR industry, providing the demand signal necessary for technology to scale. However, this strength creates a systemic weakness, as the nascent market’s health has become overly dependent on the actions and continued commitment of a single corporate buyer. The company’s actions are both creating the market and exposing its structural fragility.

- The core strength is Microsoft’s financial capacity and willingness to sign multi-billion-dollar, multi-year offtake agreements, which directly de-risk capital-intensive projects for developers and financiers.

- A primary weakness is the market’s heavy reliance on one entity; any reduction in Microsoft‘s procurement volume could have a chilling effect on the entire CDR sector, which currently lacks a diverse base of large-scale buyers.

- A key opportunity lies in leveraging its leadership to attract other corporations into forming a broader buyers’ coalition, distributing the financial burden and creating a more resilient, multi-customer market.

- The most significant threat is internal: with its emissions growing 23.4% due to AI expansion, Microsoft faces a scenario where its own carbon footprint could outpace the supply of high-quality CDR it is trying to build, jeopardizing its own net-zero goals.

Scope 3 Emissions Comprise 97% of Total

This section on SWOT analysis and leadership risks is perfectly matched with a chart illustrating Microsoft’s core challenge. The overwhelming proportion of Scope 3 emissions is the fundamental driver for Microsoft’s CDR strategy and represents a major risk and vulnerability.

(Source: CarbonCredits.com)

Microsoft 2026 Outlook, AI Emissions vs. CDR Scaling

The defining tension for 2026 is whether the global CDR supply, catalyzed by Microsoft, can scale rapidly enough to meet the company’s own accelerating emissions from AI and cloud services. The company’s success depends on its ability to stimulate a market that grows faster than its own footprint, while simultaneously encouraging other major corporations to step in as buyers to create a more stable and diversified ecosystem. The signals to watch are not just Microsoft‘s next moves, but how the rest of the market responds.

- The primary signal to watch is the emergence of new, large-scale corporate buyers. If other Fortune 500 companies do not begin signing multi-million-tonne deals in 2026, the market’s dependence on Microsoft will become a critical systemic risk.

- The operational results from the pilot to integrate DAC with waste heat from its data centers will be crucial. A successful outcome could significantly alter the economics of DAC and trigger a wave of co-located projects.

- The stability of the U.S. 45 Q tax credit and the implementation of new policies like the OBBBA will heavily influence project financing and deployment speed in North America, a key region for many CDR technologies.

- Given the staggering power demand and emissions growth associated with AI, monitor whether Microsoft announces even larger offtake agreements or diversifies its portfolio further into additional engineered pathways to keep pace with its internal carbon liability.

Direct Air Capture Market Projects Explosive Growth

The section looks to the future, contrasting AI emissions with CDR scaling. This chart, which projects ‘explosive growth’ for the DAC market, directly supports the ‘CDR Scaling’ part of the narrative and provides a forward-looking perspective on the potential to meet future challenges.

(Source: P&S Intelligence)

The questions your competitors are already asking

This report covers one angle of Microsoft’s commercial strategy for carbon dioxide removal. The questions that matter most depend on your work.

- Which carbon removal companies are gaining ground in the corporate offtake market based on Microsoft’s portfolio strategy?

- What is the outlook for BECCS and DAC deployment for corporate offsetting by 2030, following Microsoft’s billion-dollar offtake agreements?

- What are the opportunities for DAC and BECCS project developers in the corporate offtake market now that Microsoft has established a new procurement benchmark?

- Microsoft’s activities in carbon removal: Is the shift from pilot projects to billion-dollar offtakes a model other tech companies can follow to meet their own net-zero targets?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

CDR Market Purchases Grew Fourfold in 2025

This concluding section considers questions from competitors. The stunning data point that the entire market quadrupled in a single year is a major market signal that would be top of mind for any competitor, highlighting the accelerating pace and competitive urgency in the CDR space.

(Source: Carbon Removal Updates – Substack)