Vaulted Deep Bi CRS Strategy, 4.9 M Tonne Microsoft Deal, $32 M Funding, and 2 Major Offtakes (2025)

Carbon Removal Adoption, Vaulted Deep 4.9 M Tonne Microsoft Deal Signals Market Shift

The carbon removal sector experienced a critical divergence in 2025, as market realities separated pragmatic, scalable business models from capital-intensive, policy-dependent technologies. While a wave of cancellations hit the clean-tech industry, Houston-based Vaulted Deep validated its Biomass Carbon Removal and Storage (Bi CRS) strategy by securing major commercial offtake agreements. This performance demonstrates a market pivot toward solutions that can deliver verifiable, permanent carbon removal tonnes today, rather than banking on the future cost-down curves of nascent technologies.

- Before 2025, the market narrative was dominated by high-tech approaches like Direct Air Capture, which attracted significant media and venture capital attention despite being largely in pilot or demonstration phases with high projected costs.

- In 2025, Vaulted Deep demonstrated a different path to scale by repurposing mature oil and gas slurry injection technology to sequester organic waste. This approach leverages existing infrastructure and waste streams, creating a significant cost and readiness advantage.

- The market validated this execution-focused model through two landmark offtake agreements: a deal with Microsoft for up to 4.9 million tonnes of CO₂ removal and a partnership with Google for 50, 000 tonnes.

- This commercial success occurred as Bi CRS suppliers, including Vaulted Deep, Graphyte, and Charm Industrial, accounted for approximately 99% of all delivered durable Carbon Dioxide Removal (CDR) tonnes in the first quarter of 2025, confirming the technology’s readiness for deployment at scale.

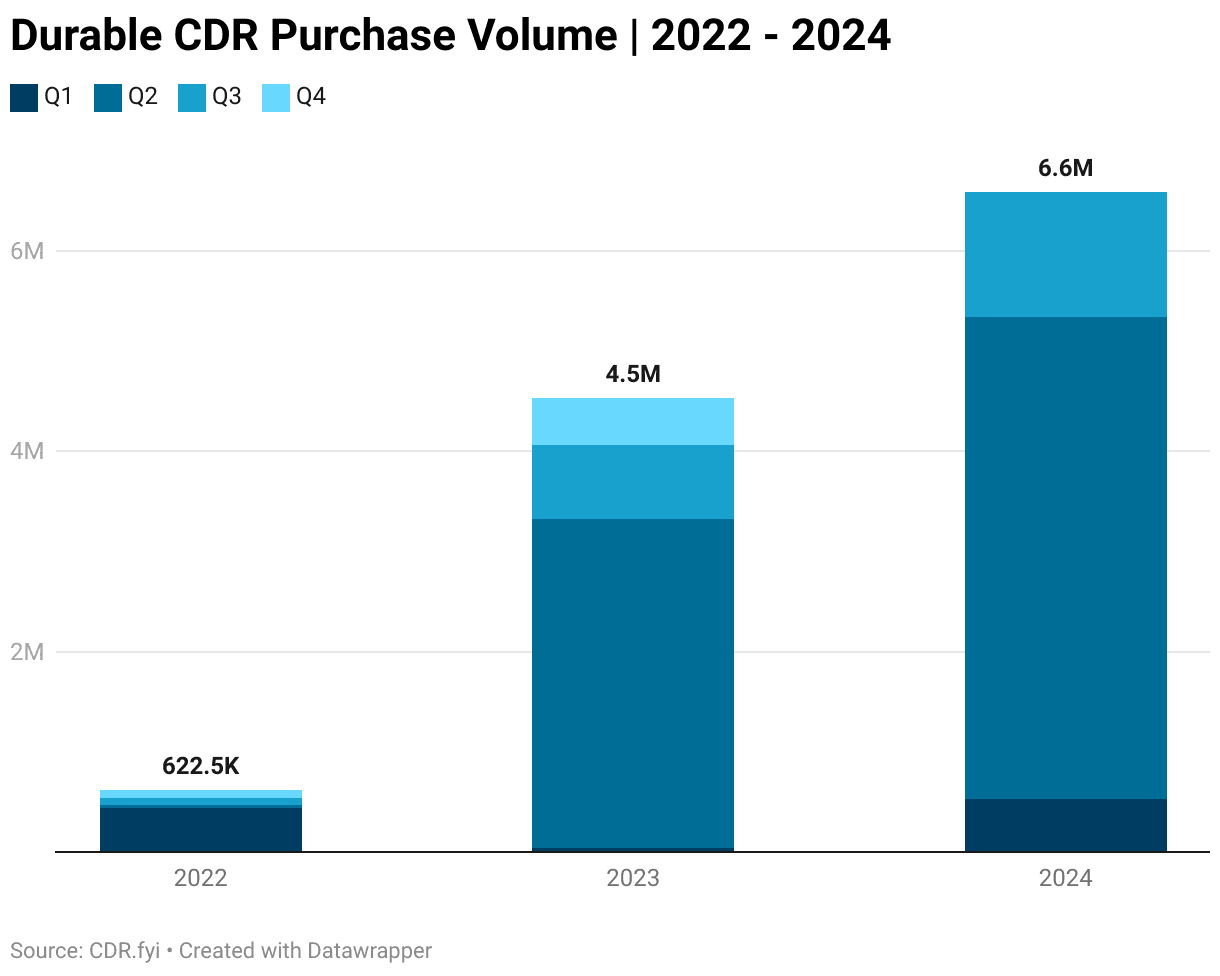

Durable CDR Purchase Volume Reached 6.6M Tonnes

The section discusses a 4.9M tonne deal signaling a market shift. This chart provides the total market context (6.6M tonnes), highlighting the significance of this single large deal and validating the ‘market shift’ narrative.

(Source: CDR.fyi)

$3.7 B in Cancellations, US Policy Reversal Rewrites Clean Tech Investment Rules

A sudden shift in U.S. federal policy in 2025 triggered a wave of project cancellations and exposed the acute vulnerability of capital-intensive clean energy projects dependent on government subsidies. This market disruption underscored the strategic value of business models with resilient, independent economics, further highlighting the strength of Vaulted Deep’s commercial strategy, which thrived amid the turmoil.

- In May 2025, the U.S. Department of Energy (DOE) terminated awards for 24 clean energy demonstration projects, rescinding over $3.7 billion in federal funding previously allocated for carbon capture and industrial decarbonization.

- The policy reversal extended to renewables, with the administration halting leases for five major offshore wind farms totaling approximately 7 GW and the Department of the Interior canceling large-scale solar projects on public lands.

- In sharp contrast, Vaulted Deep successfully raised $32 million in funding in May 2025. This investment, secured during a period of intense market uncertainty, signaled strong investor confidence in its low-cost, scalable Bi CRS model.

- The broader fallout included the cancellation of dozens of green hydrogen projects globally and the abandonment of facilities like Kore Power’s $1.2 billion battery plant in Arizona, which paused after the freeze on Inflation Reduction Act (IRA) funding.

Carbon Capture Costs Exceed Federal Tax Credits

This chart directly explains the ‘US Policy Reversal’ and ‘$3.7B in Cancellations’ mentioned in the section. It visualizes the economic pressure where project costs are higher than policy incentives, leading to cancellations.

(Source: decarbonfuse.com)

Table: Major Clean Technology Project Cancellations (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Suspension of 5 Offshore Wind Farms | Dec 2025 | The U.S. administration paused ~7 GW of offshore wind projects from Ørsted, Avangrid, and others, citing national security concerns and creating massive industry uncertainty. | Reuters |

| BP’s H 2 Teesside Plant | Dec 2025 | BP scrapped its 1.2 GW blue hydrogen project in the UK, a major setback for the country’s low-carbon hydrogen ambitions. | Business Green |

| DOE Clean Energy Demonstrations | May 2025 | The Department of Energy canceled $3.7 billion in awards for 24 carbon capture and industrial decarbonization projects to generate “taxpayer savings.” | U.S. Department of Energy |

| Ørsted’s UK Offshore Wind Farm | May 2025 | Ørsted canceled a major offshore wind farm in the UK due to a significant jump in project costs, highlighting persistent economic headwinds. | Energy Connects |

| Air Products’ Massena Plant | Feb 2025 | Air Products exited its green liquid hydrogen project in New York as part of a strategic review to reduce its capital outlay. | Air Products |

Vaulted Deep 2 Major Offtake Agreements with Microsoft and Google (2025)

In 2025, Vaulted Deep secured its market leadership not through speculative venture funding but by signing two of the largest-ever durable carbon removal offtake agreements. These multi-year contracts with corporate climate leaders provide the bankable, long-term revenue certainty required to finance and develop the company’s expanding network of geologic sequestration infrastructure.

- The agreement with Microsoft, signed in July 2025, is for the removal of up to 4.9 million tonnes of CO₂ over a 12-year period through 2038. It stands as one of the largest durable CDR purchases in history and provides a crucial demand signal to the entire market.

- In September 2025, Vaulted Deep announced a partnership with Google to remove 50, 000 tonnes of CO₂ by 2030. This deal, certified by the registry Isometric, also focuses on advancing methane emissions quantification from organic waste management.

- These large-scale purchase agreements are strategically vital as they de-risk project financing for new injection sites and allow Vaulted Deep to scale its operations to meet committed deliveries, moving the company from pilot-scale to industrial-scale removals.

Chart Shows Carbon Removal Revenue Streams

The section heading focuses on ‘Major Offtake Agreements,’ which are a primary revenue stream for carbon removal companies. This chart visually explains the business model that these agreements support.

(Source: Clean Air Task Force)

Table: Vaulted Deep Commercial Offtake Agreements

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Sep 2025 | Offtake agreement to remove 50, 000 tonnes of CO₂ by 2030. The partnership also aims to advance methane emissions quantification and reduction. | ESG News | |

| Microsoft | Jul 2025 | A landmark 12-year agreement for the removal of up to 4.9 million tonnes of CO₂. The deal provides long-term revenue to finance infrastructure expansion. | PR Newswire |

US Market Shakeout, Vaulted Deep’s Strategy Thrives Amid Policy Instability

While the 2025 U.S. policy reversal stalled numerous clean-tech projects dependent on federal incentives, Vaulted Deep’s core strategy proved uniquely resilient. By building its business model around existing waste management streams and mature oil and gas infrastructure, primarily concentrated in regions with deep industrial expertise, the company insulated itself from the political volatility that crippled other sectors.

- Between 2021 and 2024, federal policies like the IRA and Bipartisan Infrastructure Law encouraged a wide range of clean energy investments across the United States, from offshore wind on the East Coast to solar projects in the Southwest.

- In 2025, this geographic diversification became a liability, as project cancellations followed federal funding cuts. Projects were halted in Texas (Calpine’s carbon capture), the Northeast (offshore wind), and Nevada (Esmeralda 7 solar project).

- Vaulted Deep’s Houston-based operations and reliance on established oil and gas drilling technology provided a key advantage. The company leverages a pre-existing industrial ecosystem and regulatory framework for underground injection, reducing both costs and political risk associated with novel infrastructure development.

Chart Illustrates Technology Market Adoption S-Curve

The S-curve provides a classic theoretical framework for understanding the ‘US Market Shakeout’ phase of a new technology. It illustrates the competitive dynamics as a market moves from early adopters to the majority.

(Source: Clean Air Task Force)

Bi CRS vs DAC, Vaulted Deep Proves Commercial Readiness at Scale

In 2025, the carbon removal market demonstrated a clear difference in technological readiness, where Vaulted Deep’s Bi CRS method, built on mature TRL 8-9 components, began delivering tonnes at scale. This contrasted sharply with most Direct Air Capture (DAC) technologies, which largely remained at TRL 6-7 and continued to face significant cost and energy hurdles that constrained their commercial deployment.

- Prior to 2025, DAC technologies were the primary focus of media and venture investment, but their real-world contribution to carbon removal was minimal, with high costs ranging from $250 to over $1, 000 per tonne.

- The 2025 market data revealed a different story. Bi CRS methods from companies like Vaulted Deep were responsible for the vast majority of delivered durable CDR, demonstrating a viable, cost-effective pathway to scale using existing technology.

- Vaulted Deep’s process of turning organic waste into a slurry and injecting it into deep geologic formations repurposes proven technologies from the waste management and oil and gas industries, giving it a TRL of 8-9 and a structural cost advantage estimated to be well under $200 per tonne.

- The company’s win as a second runner-up in the $100 million XPRIZE for Carbon Removal in April 2025 provided further third-party validation of its technology’s scalability, permanence, and commercial viability.

Carbon Removal Technologies Compared by Cost and Permanence

The section heading explicitly calls for a comparison of ‘Bi CRS vs DAC.’ This chart directly serves that purpose by comparing different technologies on the key metrics of cost and permanence, which are central to proving commercial readiness.

(Source: Clean Air Task Force)

SWOT Analysis, Vaulted Deep’s Bi CRS Model Amidst 2025 Market Turmoil

Vaulted Deep’s 2025 performance validates its core strengths in leveraging existing infrastructure and securing bankable offtake agreements. However, the company’s ability to scale will depend on navigating operational bottlenecks and broader market threats, including policy instability that affects corporate climate spending.

Durable CDR Market 2024 Year in Review

A SWOT analysis requires broad market context. A ‘Year in Review’ chart provides the perfect backdrop, summarizing the market conditions and trends that inform the Strengths, Weaknesses, Opportunities, and Threats for Vaulted Deep.

(Source: CDR.fyi)

Table: SWOT Analysis for Vaulted Deep’s Bi CRS Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | The business model was based on the theory of using mature O&G technology and low-cost waste feedstock. | Demonstrated ability to use mature technology to secure massive, multi-year offtake deals with Microsoft and Google. Won the XPRIZE for Carbon Removal. | The model was validated commercially. The company proved it could sign bankable contracts that enable financing for scaled infrastructure, shifting from theory to execution. |

| Weaknesses | Relatively unknown technology compared to DAC. Scalability was unproven, and securing injection permits was a theoretical risk. | Potential operational bottlenecks in sourcing sufficient waste and rapidly permitting new injection sites to meet large contract obligations. | The core weakness shifted from technology risk to operational execution risk. The challenge is no longer proving the concept but scaling the physical infrastructure fast enough. |

| Opportunities | A growing voluntary carbon market and corporate net-zero pledges created a potential demand pool. | The market for high-quality, durable CDR credits is projected to reach $14 billion by 2035. The collapse of other clean tech projects creates a market opening. | The demand signal became concrete and massive. Vaulted Deep is now positioned as a primary supplier to fill the gap left by stalled, higher-cost projects. |

| Threats | Regulatory uncertainty around carbon accounting and long-term storage permanence for a novel method. Competition from high-profile DAC companies. | Broader economic downturn could reduce corporate climate budgets. Policy volatility could impact regulations for underground injection or waste management. | The primary threat shifted from technology competition to macro-level risks. Policy instability, which benefited Vaulted Deep by sidelining competitors, could also become a direct threat. |

Vaulted Deep 2026 Outlook, Securing Injection Sites is the Critical Path

To successfully deliver on the ambitious removal volumes committed to Microsoft and Google, Vaulted Deep’s most critical task for 2026 is the rapid and successful permitting of new geologic injection sites across the United States. This expansion of physical infrastructure is the primary gating factor for its growth.

- If this happens, watch for company announcements of new operational injection sites in multiple states and partnerships with large municipal waste providers. This would signal that scaling is on track.

- These could be happening, such as an acceleration of delivery schedules for its major offtake partners, further cementing its leadership position and potentially leading to a new, larger funding round to fuel even faster expansion.

- If this stalls, watch for reports of permitting delays, challenges from local opposition groups, or a slowdown in hiring for operational roles. This would indicate a significant scaling constraint.

- This could mean that while the Bi CRS model is cost-effective, its physical deployment faces logistical and regulatory hurdles, potentially creating an opening for other durable CDR pathways to capture market share.

Chart Compares Scaling Limits of CDR Solutions

The section identifies ‘Securing Injection Sites’ as the ‘Critical Path’ for the 2026 outlook. This chart, which compares ‘Scaling Limits,’ directly visualizes the type of bottleneck that defines a critical path for growth.

(Source: Carbon Removal Updates – Substack)

The questions your competitors are already asking

This report covers one angle of the strategic divergence in the carbon removal market. The questions that matter most depend on your work.

- Which carbon removal companies are gaining ground based on delivered tonnes versus those still in the pilot phase?

- How does Biomass Carbon Removal and Storage (Bi CRS) compare to Direct Air Capture (DAC) for cost, readiness, and scalability?

- What do the Vaulted Deep offtake agreements with Microsoft and Google signal for corporate carbon removal procurement strategies?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.

Run your first brief in Enki Brief Pro

R&D and Scale Drive Down Carbon Removal Costs

This chart addresses one of the most fundamental ‘questions your competitors are already asking’: how will costs evolve with scale and technological improvement? It illustrates a key strategic dynamic in the industry.

(Source: Clean Air Task Force)