CCUS Policy Risk, $7.5 B DOE Cancellation Impacts 55 Projects Including Exxon Mobil and Calpine (2021 to 2025)

CCUS Project Viability, Over 270 US Projects Face Execution Risk After $7.5 B in DOE Funding Cuts

United States Carbon Capture, Utilization, and Storage (CCUS) project development shifted from a period of accelerated growth driven by policy incentives to a state of high uncertainty following massive federal funding cancellations in 2025. This abrupt change threatens the viability of a project pipeline that had been expanding rapidly, creating significant execution risk for developers and investors who had modeled projects based on stable government co-investment. The policy reversal has fundamentally altered the financial calculus for deploying otherwise technically mature decarbonization technologies.

- Between 2021 and 2024, the US CCUS sector experienced a surge in activity, supported by enhancements to the 45 Q tax credit. This led to the announcement of over 270 projects with a total potential capital investment of $77.5 billion, positioning the country as a global leader in carbon management infrastructure.

- This momentum reversed sharply in 2025 when the U.S. Department of Energy (DOE) canceled billions in funding. A May 30, 2025, announcement rescinded $3.7 billion in awards, impacting companies like PPL Corp., Calpine, Exxon Mobil, and Ørsted. By October 2025, the total figure grew to over $7.5 billion in canceled DOE funding, affecting 55 carbon management-related projects.

- The funding cuts were part of a wider policy shift that saw the termination of 321 financial awards across 223 clean energy projects, including initiatives in the hydrogen sector.

- This instability creates a challenging environment for securing private capital, as the canceled DOE funds were intended to de-risk first-of-a-kind projects and bridge the commercialization gap. The move undermines confidence in the long-term stability of foundational policies like the 45 Q credit, which is essential for project bankability.

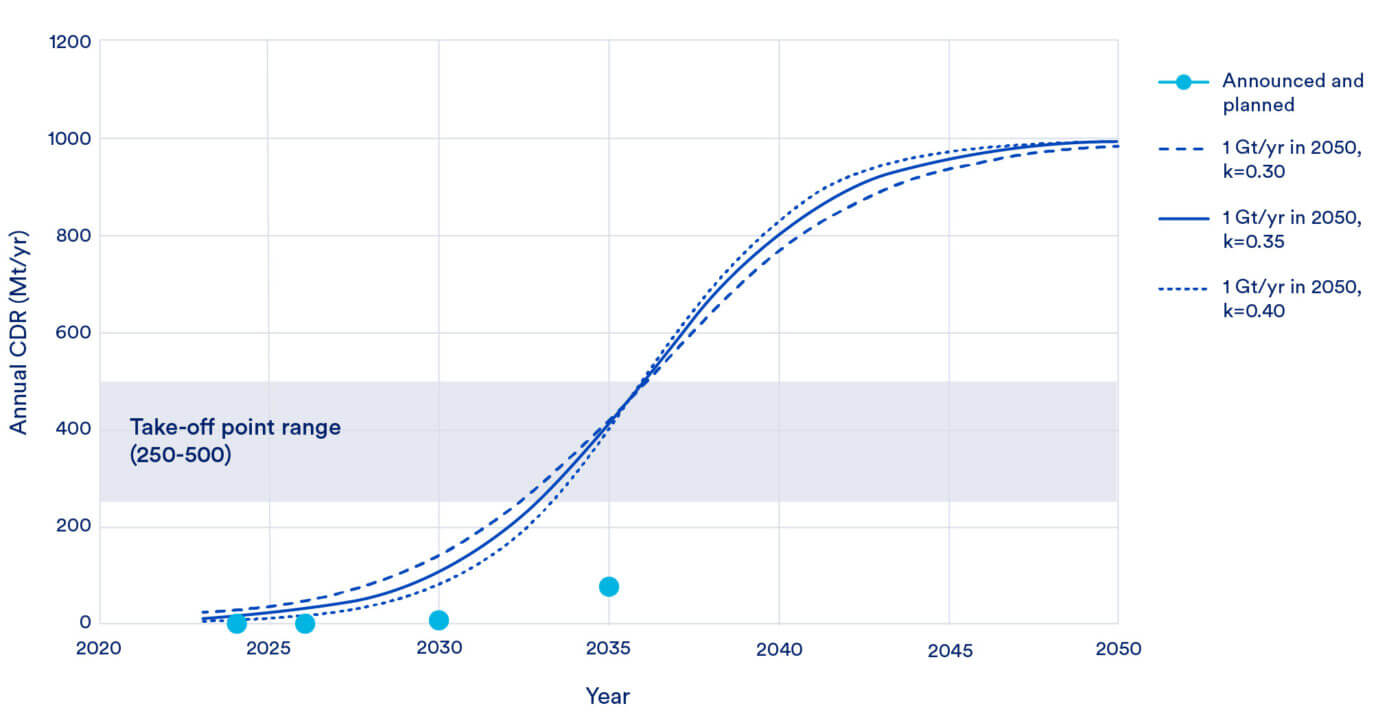

Chart Shows Required Growth for US Carbon Removal

The chart illustrates the significant scale-up of carbon removal required for the US to meet its climate targets. This provides crucial context for the section’s argument that placing over 270 projects at execution risk via funding cuts directly jeopardizes the nation’s ability to achieve this necessary growth.

(Source: Clean Air Task Force)

$22 B in Clean Energy Projects Canceled or Delayed, CCUS Sector Hit by Policy Reversals (2025)

The cancellation of over $7.5 billion in DOE funding for carbon management projects in 2025 represents a significant contraction of public-private partnerships, directly threatening the financial models of numerous large-scale CCUS initiatives. These grants were a critical component of project financing stacks, intended to absorb initial capital risk and accelerate deployment. Their removal has created a financing gap that the private sector may be unable or unwilling to fill without greater long-term policy certainty.

- The impact extends beyond direct CCUS projects, with reports from the first half of 2025 showing that businesses canceled, closed, or scaled back over $22 billion in new clean energy projects and factories due to the shifting policy environment.

- The canceled funds were crucial for helping projects reach Final Investment Decision (FID) by supplementing the 45 Q tax credit, which on its own is often insufficient to cover the high capital costs of capture equipment, especially for industrial retrofits.

- Companies like Exxon Mobil and Calpine were directly affected by the May 2025 cancellation of $3.7 billion, derailing plans for large-scale decarbonization projects that relied on the DOE’s cost-share commitment to prove economic viability.

Global Carbon Capture Project Pipeline Spikes

This chart shows a recent global surge in the CCUS project pipeline, indicating strong international momentum. This serves as a backdrop to the section’s argument that US policy reversals are causing project cancellations, putting the nation out of step with this positive global trend and costing billions in investment.

(Source: Trellis)

Table: Major US Department of Energy (DOE) Funding Cancellations for Carbon Management in 2025

| Date | Canceled Amount (USD) | Details and Strategic Purpose | Source |

|---|---|---|---|

| Oct 24, 2025 | Not Specified (321 awards) | The DOE terminated 321 financial awards supporting 223 clean energy projects two days after a federal government shutdown began. These funds were intended to accelerate commercialization and reduce initial deployment costs. | Carbon Direct |

| Oct 8, 2025 | >$7.5 Billion | The Carbon Capture Coalition identified over $7.5 billion in cancellations for DOE-funded projects, with 55 directly relevant to carbon management. The coalition stated this created “significant risk” for nationwide deployment. | Carbon Capture Coalition |

| Oct 2, 2025 | Not Specified (>300 grants) | A broad cancellation of over 300 grants impacted major initiatives, including hydrogen and direct air capture hubs, disrupting large-scale, coordinated decarbonization efforts. | E&E News |

| Jul 24, 2025 | >$22 Billion (Private Sector) | In the first half of 2025, private companies canceled or scaled back over $22 billion in clean energy projects, citing the negative impact of policy shifts and a deteriorating investment climate. | E 2 |

| May 30, 2025 | $3.7 Billion | The DOE canceled 24 awards, mainly for carbon capture and industrial decarbonization projects. Affected companies included Calpine, Exxon Mobil, and Ørsted, representing a major setback for planned facility retrofits. | ESG Dive |

North America, US CCUS Leadership at Risk Amidst Policy Whiplash and 321 Award Terminations

While North America established itself as the global leader in CCUS project development through 2024, accounting for 35.1% of the market, the abrupt cancellation of federal support in the United States in 2025 threatens to cede this advantage. The policy whiplash has introduced a level of sovereign risk that complicates investment decisions and contrasts sharply with more stable, long-term policy environments in other regions.

- Through 2024, the United States was the clear epicenter of CCUS activity, with a pipeline of over 270 projects representing $77.5 billion in potential investment. States like Texas and Louisiana became focal points for developing integrated carbon management hubs.

- The 2025 policy reversal, including the termination of 321 separate financial awards, has injected chaos into this ecosystem. This has cast doubt on the long-term bankability of projects that are years in development and rely on a stable fiscal framework.

- Despite the federal headwinds, some commercial momentum persists. In April 2025, 1 Point Five signed a 25-year sequestration agreement with CF Industries, and in May 2025, CO 280 secured an offtake agreement with JPMorgan Chase. These deals show that private sector demand remains, but such projects now face a higher-risk environment.

- This contrasts with Europe, where projects like the Northern Lights venture, backed by Total Energies, Equinor, and Shell, benefit from consistent government backing. This stability makes Europe an increasingly attractive destination for capital that might have otherwise been deployed in the US.

North American CCS Market Forecast to Grow Steadily

The chart’s forecast of steady growth for the North American CCS market highlights the region’s potential. The section uses this projection as a point of contrast, arguing that this growth and the US’s leadership role within it are now at significant risk due to domestic policy instability and award terminations.

(Source: Fortune Business Insights)

CCUS Technology, Mature Capture Methods (TRL 9) Confront Commercial Viability Gaps Without Stable Policy

Although foundational post-combustion and pre-combustion CCUS technologies reached full commercial maturity (Technology Readiness Level 9) by 2025, their economic deployment is now challenged by the removal of government support. This highlights a persistent gap between technical readiness and financial bankability, which targeted public funding was designed to bridge. The policy shift makes it significantly harder to finance even proven technologies at scale.

- By 2025, established solvent-based capture methods were considered fully proven (TRL 9), meaning the core technology risk is low. However, the cost of capture remains a significant commercial barrier, with estimates ranging from $50-$100 per ton of CO₂ for conventional power plants.

- The financial models for these projects typically stacked the 45 Q tax credit with DOE grants to close the viability gap. The removal of the grant component makes many projects uneconomic, as the tax credit alone is not sufficient to justify the high upfront capital expenditure.

- Emerging technologies, such as membraneless electrochemically mediated amine regeneration (EMAR), show promise for reducing the levelized cost to around $69.7 per tonne. However, the uncertain policy environment makes it more difficult to secure funding for the pilot and demonstration projects needed to scale these next-generation solutions.

- This situation creates a paradox where the technology is ready for deployment, but the commercial and policy framework is not, stalling progress on industrial-scale decarbonization in key sectors like cement, steel, and power generation.

Decarbonization Imperatives Across Heavy Industries

This chart establishes the critical need for decarbonization solutions in heavy industries. It provides the ‘demand’ context for the section, which explains how mature CCUS technologies (TRL 9), despite being ready to meet this demand, face commercial viability gaps due to a lack of stable policy.

(Source: MarketsandMarkets)

SWOT Analysis for US CCUS Projects Post-2025 DOE Funding Reversals

A SWOT analysis reveals that while the US CCUS sector possesses strong underlying assets in technology and infrastructure, its trajectory has been fundamentally altered by the 2025 policy reversals. This has introduced major external threats and exposed deep-seated financial weaknesses that were previously masked by anticipated government support. The investment thesis for CCUS in the US now hinges less on technology and more on navigating extreme political risk.

Global CCUS Market to Reach $17.75B by 2030

The chart quantifies a significant global market growth, which represents a key ‘Opportunity’ in the SWOT analysis framework. It underscores the financial incentive for US projects, while the section details the ‘Threats’ and ‘Weaknesses,’ like funding reversals, that jeopardize the US’s ability to capitalize on this trend.

(Source: MarketsandMarkets)

Table: SWOT Analysis for US Carbon Capture Initiatives

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Vast geological storage capacity; mature TRL 9 capture technologies; extensive project pipeline (270+); skilled oil & gas workforce. | These underlying strengths remain but are now overshadowed by sovereign risk. The private sector is still pursuing deals (e.g., 1 Point Five, CO 280) based on these assets. | The core technical and geological foundations of the US CCUS industry were validated as strong, but insufficient on their own to drive growth without stable policy. |

| Weaknesses | High capital costs for capture; heavy reliance on 45 Q and other subsidies; long permitting and development timelines. | The reliance on subsidies became a critical vulnerability. The removal of DOE grants exposed the fact that 45 Q alone is not enough to make many projects bankable. | The weakness of “policy dependence” was validated in the most direct way possible. The financial models of an entire sector were broken by the policy shift. |

| Opportunities | Decarbonizing hard-to-abate industries (cement, steel); creating CO₂-based products; growing corporate demand for carbon removal credits. | Private-sector demand for carbon removal continues to grow (e.g., JPMorgan Chase deal). However, the opportunity to decarbonize heavy industry at scale is now severely constrained by a lack of viable projects. | The opportunity in voluntary carbon markets was validated as a separate, albeit smaller, driver. The larger opportunity in industrial decarbonization was put on hold. |

| Threats | Policy and political instability; public opposition to CO₂ pipelines; competition from cheaper decarbonization options. | The primary threat of policy instability materialized into a full-blown crisis for the sector, with billions in funding explicitly canceled. This became the dominant market reality. | The theoretical threat of “political risk” was validated as the single most important factor determining the future of the US CCUS industry. |

US CCUS Investment Scenarios, Project FIDs Hinge on 45 Q Certainty After $7.5 B Cancellation

The path forward for United States CCUS projects now depends almost entirely on the perceived stability and longevity of the 45 Q tax credit, as developers can no longer rely on federal grants to de-risk capital-intensive projects. Future Final Investment Decisions will be driven by a company’s tolerance for political risk and its ability to secure long-term, private-sector contracts that can withstand policy volatility.

- If this happens, watch this: If the 45 Q tax credit is reaffirmed with strong bipartisan support, confidence may slowly return. The key signal to watch will be if major energy companies make FIDs on large industrial or power-sector projects without direct DOE grants, relying solely on the tax credit and private financing. This would signal a new, more resilient investment thesis.

- These could be happening: The most likely near-term scenario is a market fragmentation. Projects with low capture costs (e.g., from ethanol or ammonia production) and those with secured private offtake agreements will move forward cautiously. Meanwhile, more complex and expensive retrofits for power plants, cement, and steel facilities will be indefinitely postponed. Watch for a wave of project cancellations and asset write-downs in corporate earnings reports through 2025 and 2026.

- If this happens, watch this: A worst-case scenario involves further erosion of the 45 Q credit, either through legislative changes or adverse regulatory interpretations. This would trigger a flight of capital and expertise from the US to more stable jurisdictions in Europe, Canada, and the Middle East, effectively ending America’s leadership in the CCUS sector.

The questions your competitors are already asking

This report covers one angle of the US CCUS market’s response to significant policy and funding changes. The questions that matter most depend on your work.

- Which CCUS project developers are most at risk after the 2025 DOE funding cuts?

- What is actually happening with the Exxon Mobil and Calpine CCUS projects since the DOE funding was canceled?

- What is the outlook for the US CCUS project pipeline now that federal funding is uncertain?

- Is the 45Q tax credit alone enough to ensure CCUS project viability without DOE co-investment?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.