Philippines Offshore Wind 2026: How Policy Unlocked a 3.3 GW Auction and What Comes Next

Unlocking 3.3 GW: Philippines’ Offshore Wind Market Shift from Potential to Reality

The Philippine offshore wind market has transitioned from a phase of high-potential studies to a structured, commercial phase defined by the launch of its inaugural 3.3 GW fixed-bottom offshore wind auction. This shift was driven by deliberate government policy actions designed to de-risk market entry and provide a bankable procurement process, turning its vast resource potential into a tangible investment opportunity.

- Prior to 2025, activity centered on foundational analysis, such as the World Bank’s identification of 178 GW of technical potential and the development of policy roadmaps. The primary barrier remained the restriction on foreign ownership, limiting the participation of experienced international developers and capital.

- The period from 2025 to today marks a definitive commercial turn. The Department of Energy (DOE) launched the Green Energy Auction 5 (GEA-5) on November 25, 2025, creating a clear route to market. This was enabled by the earlier removal of foreign ownership caps, which had already attracted nine fully foreign-owned offshore wind service contracts totaling 5, 510 MW before the auction even began.

- The auction design itself signals market maturity. By including non-price criteria like technical readiness and grid connection status, the DOE has moved beyond a purely cost-based competition to one that prioritizes project viability and execution certainty.

Regional Growth Fuels Philippine Wind Market

This chart shows projected growth in the ‘Asia Pacific ex China’ region, providing the investment context for the Philippines’ shift from potential to commercial reality.

(Source: Airswift)

De-Risking Offshore Wind Investment: A Comprehensive Financial Framework for the Philippines’ 3.3 GW Auction

The government established a clear and investor-focused financial framework to ensure the bankability of the first wave of capital-intensive offshore wind projects. The core of this strategy involved setting a sufficiently high price ceiling to attract bidders and protect initial investments, a critical move to build market confidence.

- The Energy Regulatory Commission (ERC) addressed initial investor concerns by revising the auction’s price cap upward. After proposing a preliminary Green Energy Auction Reserve (GEAR) price of ₱10.3859 per kilowatt-hour (k Wh), the ERC finalized the cap at a higher ₱11/k Wh in February 2026.

- This final price cap, while roughly double the average wholesale power prices of the previous year, was a strategic decision to de-risk the nation’s first utility-scale offshore wind ventures and acknowledge the high upfront capital expenditure, which constitutes 70-80% of a project’s total cost.

- Successful bidders in the GEA-5 auction will secure 20-year contracts, providing the long-term revenue certainty necessary for developers to secure financing for projects scheduled to begin commercial operation between 2028 and 2030.

Table: Financial Milestones for the GEA-5 Offshore Wind Auction

| Financial Milestone | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Final Price Cap Set | Feb 2026 | The ERC raised the final Green Energy Auction Reserve (GEAR) price to ₱11.00 per k Wh. This was done to enhance project bankability and attract investment by providing a higher revenue ceiling for the capital-intensive first projects. | Manila Bulletin |

| Initial Price Cap Proposed | Dec 2025 | The ERC initially proposed a GEAR price of ₱10.3859 per k Wh. This figure was noted as the highest reserve price for a renewable energy auction in the country, signaling the government’s intent to support the new sector. | Philstar Global |

| Auction Launch | Nov 2025 | The DOE officially launched the GEA-5 auction for 3.3 GW of fixed-bottom offshore wind capacity with 20-year contracts. This created the first formal, large-scale procurement mechanism for the sector. | Manila Bulletin |

Building a Sustainable Ecosystem: Strategic Partnerships for Philippine Offshore Wind Development

The development of the Philippine offshore wind market is being driven by a coordinated effort between government bodies, multilateral organizations, and early-mover private developers. This collaboration has been essential in shaping policy, establishing technical foundations, and signaling market readiness to international investors.

- Government agencies are leading the market’s structural design. The Department of Energy (DOE) is responsible for the auction program, while the Energy Regulatory Commission (ERC) sets the financial parameters. Concurrently, the Philippine Ports Authority (PPA) is planning crucial infrastructure investments in key ports to support project logistics.

- Multilateral institutions have provided foundational support. The World Bank Group‘s assessment identifying the country’s 178 GW technical potential was instrumental in framing government ambitions and attracting global attention to the market.

- Strong international developer interest is already evident. Even before the GEA-5 auction, the government had awarded nine offshore wind service contracts with a combined potential of 5.51 GW to fully foreign-owned companies, validating the impact of its market liberalization policies.

Table: Key Partnerships and Stakeholders in the Philippine Offshore Wind Sector

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Philippine Ports Authority (PPA) | 2025–Ongoing | The PPA committed to investing in strategic ports, including Subic, Batangas, and Iloilo, to create the assembly and maintenance hubs required for large-scale offshore wind farm construction and operation. | REGlobal |

| Foreign-Owned Projects | Oct 2025 | Following market liberalization, the DOE awarded nine offshore wind service contracts totaling 5.51 GW to fully foreign-owned entities, demonstrating immediate private sector response to policy reform. | Manila Standard |

| Northern Luzon Offshore Wind Project | Nov 2025 | Feasibility studies commenced for a 2 GW project, highlighting a pipeline of large-scale developments emerging in parallel with the formal auction process. | Offshorewind.biz |

| World Bank Group | Pre-2025 | The World Bank provided the technical assessment that identified the Philippines’ 178 GW of offshore wind potential, providing the data-driven foundation for the government’s energy strategy. | Lexology |

Establishing the Philippines as APAC’s Premier Offshore Wind Hub: Geographic Focus and Opportunities

The Philippines is strategically positioning itself to become a key offshore wind market in the Asia-Pacific region, leveraging its vast coastline and renewable energy targets to attract development. The initial geographic focus is on areas suitable for fixed-bottom technology, with coordinated infrastructure planning intended to support this growth.

Map Pinpoints Offshore Wind Development Zones

This map directly illustrates the article’s ‘Geographic Focus’ by displaying the specific coastal regions designated for offshore wind energy development.

(Source: BVG Associates)

- Prior to 2025, the Philippines was recognized for its resource potential but lagged behind regional leaders like China and Taiwan in terms of operational projects and a structured market. Activity was limited to preliminary site assessments.

- The launch of the GEA-5 auction in late 2025 firmly places the Philippines on the global offshore wind development map, alongside other emerging markets like Colombia and South Korea. This move diversifies the APAC market and creates new opportunities for the regional supply chain.

- The government’s infrastructure strategy is geographically targeted. The commitment by the Philippine Ports Authority to upgrade ports at Subic, Batangas, and Iloilo is designed to create a logistical backbone to serve the first wave of offshore wind projects and establish a domestic supply chain hub. This contrasts with the high costs of offshore wind seen in other regions.

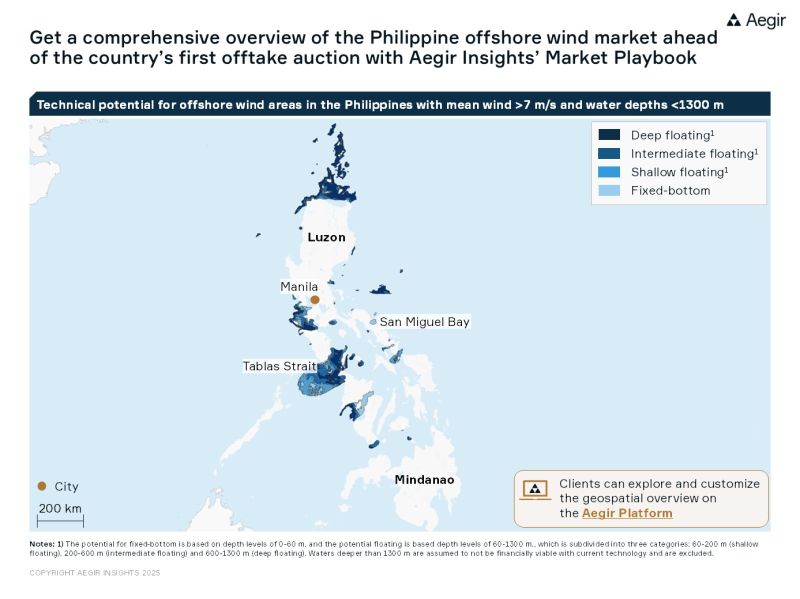

Fixed-Bottom Wind: The Key to Philippine Offshore Wind Market Growth and Technological Advancement

The Philippines is taking a pragmatic, phased approach to technology deployment by focusing its inaugural auction exclusively on fixed-bottom offshore wind. This strategy leverages a mature, commercially proven technology to build initial momentum, establish a local supply chain, and mitigate execution risk before tackling the more complex deep-water resources that require floating wind solutions.

Map Shows Potential for Fixed vs. Floating Wind

This map justifies the strategic focus on fixed-bottom technology by illustrating the country’s resource distribution across different water depths and technology types.

(Source: LinkedIn)

- Between 2021 and 2024, discussions around the Philippines’ offshore wind potential acknowledged that a large portion of its 178 GW resource is in deep waters, requiring next-generation floating wind technology. However, the market lacked a clear mechanism to support any commercial-scale development.

- The GEA-5 auction, launched in November 2025, deliberately targets 3.3 GW of fixed-bottom projects. This aligns with existing technological capabilities and supply chain readiness globally, reducing the risk profile for first-mover developers and financiers.

- This fixed-bottom-first approach serves as a critical stepping stone. By successfully delivering these initial projects, the Philippines can develop the necessary infrastructure, regulatory experience, and local expertise required to eventually commercialize its vast floating wind potential, mirroring the development trajectory seen in pioneering offshore wind projects in Europe.

SWOT Analysis: Strategic Position of the Philippine Offshore Wind Market

The Philippine offshore wind sector’s strategic position has evolved significantly, moving from a status of latent potential to one of active market creation. Key policy changes have amplified its strengths and created new opportunities, while persistent infrastructure and cost challenges remain.

- Strengths have been validated and enhanced. The country’s massive 178 GW potential is now coupled with a strong, investor-friendly policy framework, making it far more attractive.

- Weaknesses, particularly the lack of port infrastructure and high initial project costs, are now being actively addressed through targeted government investment plans and a high price cap in the GEA-5 auction.

- Opportunities have crystallized around first-mover advantages for developers who win in the initial auction and the potential for long-term supply chain and export hub development.

- Threats related to investment risk have been mitigated through policy, although competition for capital and supply chain resources from other established APAC markets remains a factor.

Table: SWOT Analysis for the Philippines Offshore Wind Sector

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | High theoretical wind potential (178 GW) identified by the World Bank. Long coastline. | Strong government support via the DOE; a clear route to market with the GEA-5 auction; 20-year contracts providing revenue certainty. | The theoretical potential was validated by a concrete, bankable procurement mechanism, transforming a resource into a market. |

| Weaknesses | Foreign ownership restrictions limited investment; lack of port infrastructure; no clear offtake mechanism. | High initial project costs persist; port infrastructure is still in development; grid integration remains a challenge. | While foreign ownership was resolved, physical infrastructure and cost hurdles became the primary focus. The government is now actively addressing these via port investment plans and higher price caps. |

| Opportunities | Potential to become a regional leader in renewable energy and reduce reliance on fossil fuel imports. | First-mover advantage for GEA-5 winners; development of a local supply chain; potential to become an export hub for components and services. | The launch of a structured auction created tangible commercial opportunities for developers and the supply chain that did not exist before. |

| Threats | Policy uncertainty and regulatory risk; competition from established RE sources like solar and onshore wind. | Global supply chain bottlenecks; competition for investment from other APAC markets; risk of an undersubscribed auction if the price cap was too low. | The primary threat shifted from internal policy risk to external market and execution risks. The government mitigated the auction risk by raising the price cap to ₱11/k Wh. |

2026 Offshore Wind Outlook: Insights and Trends to Watch Following the Philippines’ Historic 3.3 GW Auction

The success of the 3.3 GW GEA-5 auction will be the single most critical signal for the future trajectory of the Philippine offshore wind market. If the auction is fully subscribed, it will validate the government’s de-risking strategy and trigger a new phase of investment focused on infrastructure and supply chain build-out.

Wind Power to Surge in Future Energy Mix

Matching the section’s ‘Forward Outlook’ theme, this chart visualizes the significant projected growth of wind power in the Philippines’ energy mix through 2040.

(Source: Watson Farley & Williams)

- If the auction is successful, watch for accelerated infrastructure development. A fully subscribed auction will provide the market certainty needed for private and public investment to flow into the announced upgrades for the ports of Subic, Batangas, and Iloilo. Monitor for firm timelines and contracts related to these port projects.

- Look for a clear roadmap for future auctions, including floating wind. A successful GEA-5 will embolden the DOE to schedule subsequent auction rounds. The key signal will be whether the next auction introduces a specific tranche for floating offshore wind technology to begin unlocking the country’s deep-water resources.

- Monitor the formation of local-international joint ventures. As winning bidders move toward project execution, expect a wave of partnerships between established international offshore wind companies and local engineering, construction, and maritime firms. The structure of these partnerships will reveal the initial strategy for local content development.

Frequently Asked Questions

What is the Green Energy Auction 5 (GEA-5)?

The GEA-5 is the Philippines’ inaugural offshore wind auction, launched by the Department of Energy in November 2025. It is designed to award 3.3 GW of fixed-bottom offshore wind capacity through 20-year contracts, creating a structured, commercial route to market for developers.

What key policy change enabled the recent growth in the Philippine offshore wind market?

The most critical policy change was the removal of foreign ownership restrictions. This allowed experienced international developers to fully own and invest in projects, which directly led to the award of nine fully foreign-owned service contracts totaling 5,510 MW even before the GEA-5 auction was launched.

How is the government making the first offshore wind projects financially attractive to investors?

The government is de-risking investment in two main ways: by setting a high final price cap of ₱11.00 per kWh to ensure a sufficient revenue ceiling for capital-intensive first projects, and by offering long-term, 20-year contracts that provide the revenue certainty developers need to secure financing.

Why is the first auction focused only on fixed-bottom technology?

The first auction focuses on fixed-bottom technology as a pragmatic strategy to catalyze the market. By using a mature and commercially proven technology, it reduces execution risk for first-mover developers, helps establish a local supply chain, and builds regulatory experience before the country tackles its more complex, deep-water resources that require floating wind solutions.

After the first auction, what are the key developments to watch for?

Following a successful auction, the key developments to monitor are: 1) Accelerated investment into upgrading key ports like Subic, Batangas, and Iloilo; 2) The release of a clear roadmap for future auctions, which may include a tranche for floating wind; and 3) The formation of joint ventures between winning international developers and local Philippine companies to begin project execution.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.