2026 Energy Outlook: Why Battery Manufacturing Scale Crushes Offshore Wind Supply Chain Costs

Manufacturing Capacity Drives 2026 BESS Adoption as Offshore Wind Projects Face Supply Chain Risk

The rapid acceleration of Battery Energy Storage System (BESS) deployment is a direct result of manufacturing overcapacity and modular design, which has driven down costs. In contrast, the adoption of offshore wind is now constrained by a capital-intensive and immature supply chain, creating a significant divergence in the commercial viability of new clean energy projects.

- Between 2021 and 2024, both sectors demonstrated strong growth, but the underlying supply chain dynamics were already diverging. BESS manufacturing was scaling rapidly in tandem with the electric vehicle industry, establishing a foundation for cost reduction. Meanwhile, offshore wind projects faced increasing complexity and rising interest rates, exposing the fragility of a supply chain not yet equipped for massive global expansion.

- In 2025, the global benchmark Levelized Cost of Storage (LCOS) for a four-hour BESS project fell 27% to $78/MWh. This sharp decline was primarily caused by a significant expansion of battery manufacturing capacity, particularly in China, coupled with falling prices for key commodities like lithium.

- Concurrently, the Levelized Cost of Energy (LCOE) for offshore wind surged 12% to $100/MWh. This increase is attributed to persistent supply chain bottlenecks for critical components like turbines and foundations, rising raw material costs, and a shortage of specialized installation vessels.

- The economic impact of these opposing trends is clear. The projected $91/MWh LCOE for Dominion Energy’s Coastal Virginia Offshore Wind project reflects the high capital costs of current developments. Conversely, the sub-$80/MWh LCOS for batteries now makes solar-plus-storage a more economically compelling option for providing firm power.

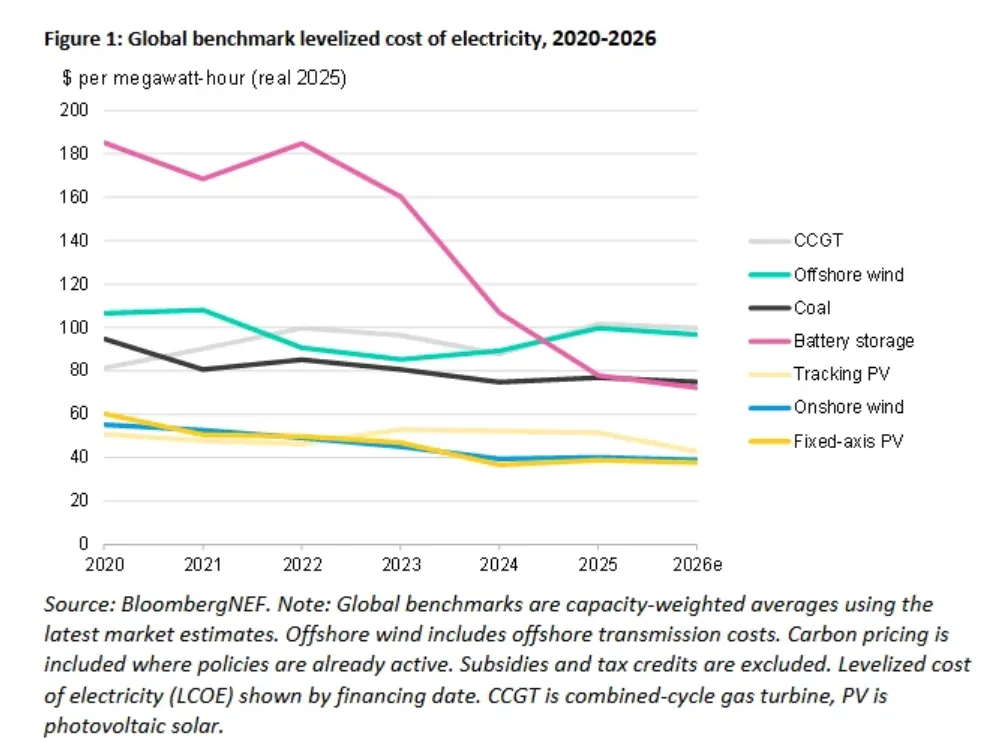

Cost Divergence: BESS vs. Offshore Wind

This chart perfectly illustrates the cost divergence discussed in the section, showing battery storage LCOE plummeting while offshore wind LCOE rises after 2023.

(Source: Saur Energy)

Strategic Alliances in 2026: Offshore Wind Seeks Innovation as BESS Leverages Mature Supply Chains

Offshore wind developers are forming targeted R&D partnerships to mitigate project risks and drive future cost reductions, a clear signal of a sector grappling with technological and logistical hurdles. Battery storage, by contrast, benefits from a mature, commoditized supply chain where competition is based on price and scale, not foundational technology development.

- Offshore wind players are focused on de-risking early-stage development. The partnership between Ocean Winds and Innovate UK to develop advanced 3 D site survey methods is a direct response to the need to reduce unforeseen costs and delays that have plagued recent projects.

- Digital optimization is another key focus. Siemens Energy is utilizing high-performance computing from AMD to run complex simulations for wind farm design, aiming to maximize energy yield and improve financial returns before construction begins.

- Hardware robustness remains a challenge, prompting targeted product innovation. Hitachi Energy’s launch of its Oceani Q portfolio, engineered specifically for harsh offshore environments, indicates that standard components are insufficient and that specialized, more costly equipment is required to ensure reliability.

Geographic Divergence in 2026: China’s Manufacturing Dominance Lowers Global BESS Costs, While Regional Wind Markets Face Price Hikes

China’s industrial strategy has created a global battery manufacturing surplus that is directly responsible for the dramatic fall in BESS costs. In contrast, offshore wind LCOE is experiencing significant negative regional variations, with Western markets facing acute cost inflation due to localized supply chain and policy factors.

- China’s massive expansion in battery production has created intense price competition, becoming the single largest driver of the global decline in LCOS for utility-scale storage projects.

- In North America, the Commercial & Industrial BESS market was forecast to add 16.3 GWh of new capacity in 2025, demonstrating strong demand. However, US offshore wind projects like Dominion’s CVOW show high initial capital costs, though long-term projections from NREL suggest costs will eventually fall significantly.

- European markets are facing severe offshore wind cost pressures. In the UK, costs are now reportedly 69% higher than five years ago, undermining project economics and forcing developers to seek revised offtake agreements. This highlights the region’s exposure to supply chain constraints and inflation.

- The Australian market illustrates the revenue potential for storage in volatile grids. While not an LCOE figure, the average clearing price for battery power reached $445/MWh in August 2023, showing the immense value placed on the flexibility that batteries provide.

Technology Maturity in 2026: BESS Achieves Commercial Scale While Offshore Wind Navigates Large-Component Integration Challenges

Battery storage has achieved a state of modular, mass-produced maturity that enables rapid cost reductions and simplified deployment. Offshore wind’s technological advancement, however, is coupled with significant logistical complexity and manufacturing challenges related to its immense, non-standardized components, which hinders its cost-down trajectory.

- A key signal of BESS maturity is the industry trend towards larger battery cell sizes and integrated, containerized systems exceeding 5 MWh. This standardization at the system level, driven by leading manufacturers, simplifies project design and reduces balance-of-system costs.

- The BESS sector’s cost curve benefits directly from mature manufacturing processes and R&D spillovers from the electric vehicle industry. This includes advances in battery chemistry and production automation that are already proven at scale.

- Offshore wind remains focused on solving fundamental deployment challenges. The continued development of floating wind platforms, as demonstrated in projects like the European Hi PRwind initiative, shows the industry is still working to unlock new resource areas, a sign of a technology not yet fully commoditized.

- The offshore wind industry’s path to lower costs relies heavily on the successful deployment of next-generation turbines in the 15-20 MW class. This dependence on technology that is not yet fully scaled or integrated into the supply chain creates significant near-term execution risk and cost uncertainty.

SWOT Analysis: BESS vs. Offshore Wind Cost Dynamics in 2026

This analysis confirms that BESS’s primary strength is its manufacturing scale, which has successfully driven down costs. Offshore wind’s core weakness is its underdeveloped and inflationary supply chain, creating distinct strategic opportunities and threats for each technology in the current market.

Cost Trends Underpin SWOT Analysis

This chart provides the visual evidence for the SWOT analysis, clearly showing the falling cost strength of BESS versus the stagnating cost weakness of offshore wind.

(Source: TaiyangNews)

Table: SWOT Analysis for BESS and Offshore Wind Economic Divergence

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | BESS: Rapidly scaling alongside EV market. Offshore Wind: High capacity factor in prime locations. | BESS: Global manufacturing overcapacity, modularity, and falling commodity prices. Offshore Wind: Ability to deliver bulk, carbon-free power to coastal load centers. | The cost-reduction potential of BESS manufacturing scale was validated, while offshore wind’s value as a bulk power source remains despite cost issues. |

| Weakness | BESS: High costs, dependence on lithium/cobalt. Offshore Wind: High CAPEX, emerging supply chain concerns. | BESS: Limited duration (typically 4 hours), potential for future commodity price swings. Offshore Wind: Extreme sensitivity to interest rates, severe supply chain bottlenecks, and high installation costs. | Offshore wind’s supply chain weakness fully materialized into significant cost inflation. BESS weakness shifted from high cost to duration limitations, a problem addressable with different system designs. |

| Opportunity | BESS: Grid stabilization. Offshore Wind: Decarbonization of power grids. | BESS: Enabling highly competitive solar-plus-storage projects, capturing high-value grid service revenue. Offshore Wind: Securing long-term government subsidies (Cf Ds), powering green hydrogen production. | BESS’s opportunity shifted from a niche grid service to a core enabler of firm renewable power. Offshore wind’s opportunity is now more dependent on policy support to bridge the economic gap. |

| Threat | BESS: Competition from gas peaker plants. Offshore Wind: Permitting delays, environmental opposition. | BESS: Market saturation for certain ancillary services in mature markets. Offshore Wind: Project cancellations due to unviable economics, direct competition from cheaper solar-plus-storage hybrids. | The primary threat to offshore wind became its own cost structure, making it uncompetitive against alternatives. The threat to BESS evolved into ensuring profitability in increasingly competitive markets. |

2026 Strategic Outlook: Watch for Capital Shift to Hybrid Solar+Storage Projects

If the LCOS for battery storage remains below $80/MWh and offshore wind LCOE holds near $100/MWh, expect a pronounced shift in capital allocation away from standalone intermittent renewables and toward hybrid solar-plus-storage projects, which now offer superior risk-adjusted returns and access to more diverse revenue streams.

BESS Cost Drops Below Key Threshold

This chart confirms the section’s premise, showing battery storage LCOE dropping below the $80/MWh threshold by 2026 while offshore wind remains near $100/MWh.

(Source: x.com)

- If this happens: BESS costs continue their downward trend while offshore wind supply chains remain constrained. Watch this: A surge in Power Purchase Agreement (PPA) announcements for solar-plus-storage projects, with developers explicitly marketing their ability to provide firm, dispatchable capacity.

- If this happens: Offshore wind developers cannot secure higher offtake prices to cover their increased LCOE. Watch this: A rise in public announcements of project delays, cancellations, or renegotiations for major offshore wind farms in the US and Europe.

- This could be happening: Offshore wind leaders will intensify efforts to industrialize their supply chains, potentially through vertical integration or long-term, high-volume contracts with key suppliers to regain cost control and project certainty.

- This could be happening: Grid operators and regulators will introduce or expand market mechanisms, such as capacity auctions, that explicitly reward the flexibility and reliability of assets like BESS, further strengthening the investment case for storage-enabled projects.

Frequently Asked Questions

Why are battery storage (BESS) costs falling while offshore wind costs are rising?

Battery storage costs are falling due to a massive overcapacity in global manufacturing, especially from China, and a modular design that scales easily. In contrast, offshore wind costs are rising because its supply chain is immature and facing severe bottlenecks for large, specialized components like turbines, foundations, and installation vessels, coupled with rising raw material and interest costs.

What are the specific cost figures comparing BESS and offshore wind?

In 2025, the global benchmark Levelized Cost of Storage (LCOS) for a four-hour BESS project fell to $78/MWh. Concurrently, the Levelized Cost of Energy (LCOE) for new offshore wind projects increased to around $100/MWh. This makes solar-plus-storage projects a more economically compelling option for providing firm power.

What is the main strategic prediction for 2026 based on these trends?

The outlook predicts a significant shift in capital investment away from standalone intermittent renewables like offshore wind and toward hybrid solar-plus-storage projects. Because storage costs are low, these hybrid projects now offer superior risk-adjusted returns and the ability to provide dispatchable, firm power, making them more attractive to investors.

How are the two industries responding to these challenges and opportunities?

The offshore wind industry is forming R&D partnerships to de-risk development and innovate on technology, such as improving site surveys and component durability. The BESS industry, by contrast, is leveraging its mature, commoditized supply chain where competition is based on manufacturing scale and price, not foundational technology development.

What role does China play in the BESS cost reduction?

China’s industrial strategy and massive expansion in battery production have created a global manufacturing surplus. This has led to intense price competition, which is identified as the single largest driver behind the dramatic global decline in the Levelized Cost of Storage (LCOS) for utility-scale battery projects.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.