Petro China BESS Supply Chain, >100 GW Market, 140 GWh Pipeline, and New Metals Trading Unit (2025)

BESS Supply Chain Risks, Petro China Enters Metals Trading Amid 100 GW Market Growth

Petro China executed a strategic pivot in 2025 by entering the battery metals market, a calculated “picks and shovels” approach designed to capitalize on China’s explosive energy storage growth while sidestepping direct project development and technology risks. This move signals a recognition by the state-owned energy giant that significant value in the energy transition lies in controlling the upstream supply chain for critical materials like lithium and copper, leveraging its formidable commodity trading expertise for a new asset class.

- Prior to 2025, Petro China‘s efforts in new energy were secondary to its core oil and gas operations. The company’s 2025 decision to establish a trading desk for battery metals marks a definitive entry into the BESS value chain, prompted by a domestic market that is scaling at an unprecedented rate.

- The scale of this domestic opportunity is staggering. China’s installed BESS capacity surpassed 70 GW at the start of 2025 and exceeded 100 GW by mid-year, a 110% year-over-year increase. By August 2025, the country was adding capacity at a rate of 2.9 GW / 7.97 GWh per month.

- This strategic shift allows Petro China to profit from the booming demand for batteries without competing in the increasingly crowded and commoditized BESS integrator market. The move aligns with China’s national action plan (2025-2027) to bolster the new energy storage sector, effectively guaranteeing demand for the materials Petro China now trades.

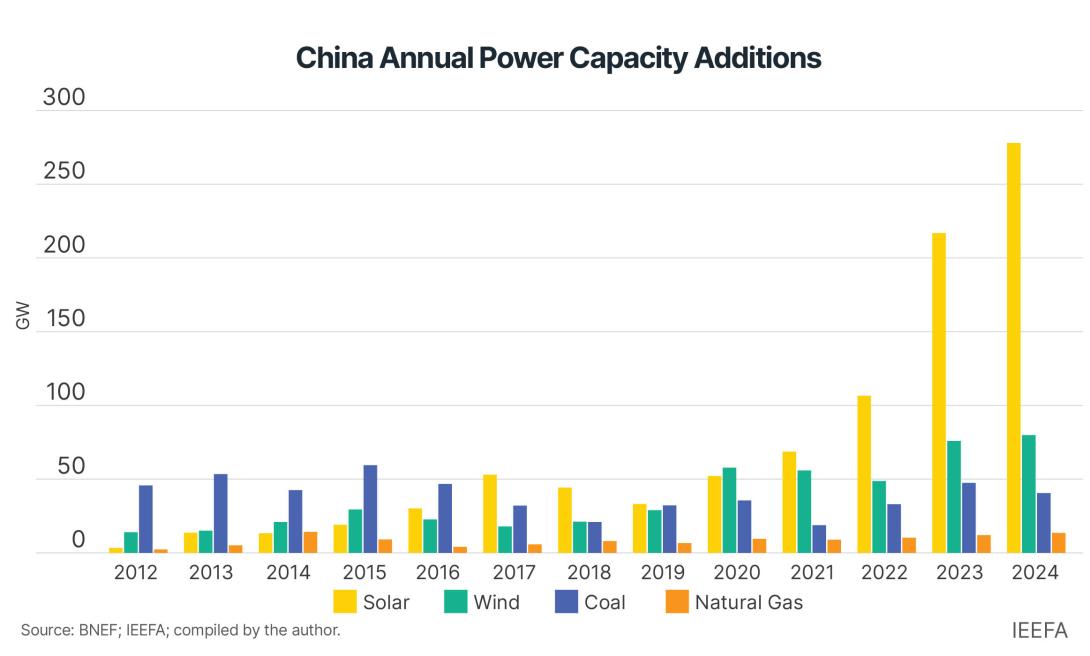

China’s Solar Capacity Additions Explode Post-2022

This chart’s headline about exploding solar capacity additions directly substantiates the ‘100 GW market growth’ mentioned in the section heading. The rapid expansion of intermittent renewable energy like solar is the primary driver for large-scale Battery Energy Storage System (BESS) demand, providing the market context for Petro China’s strategic entry.

(Source: IEEFA)

$80 B Battery Investments, Petro China’s Upstream Materials Play

Petro China‘s move into battery materials trading is a direct strategic response to the immense capital flowing into China’s battery manufacturing infrastructure, positioning the energy firm to supply a new industrial base built on approximately $80 billion in recent investments. While specific figures for its new trading unit are not public, the strategy is to insert itself as a key supplier to the numerous manufacturers scaling up production.

- Over the past five years, Chinese electric vehicle and battery manufacturers have committed an estimated USD 80 billion to build and expand factories, creating a massive and sustained demand for raw materials that underpins Petro China‘s new venture.

- The company’s 2025 Annual Report confirms that significant capital expenditure continues to flow into its traditional oil and gas business to secure national energy supply. This indicates a dual strategy: fortifying its core business while making a capital-light, expertise-heavy entry into the foundational elements of the new energy economy.

- China’s national policy is increasingly directing financing toward clean technology manufacturing and supply chains. By establishing a presence in lithium and copper trading, Petro China aligns its commercial activities with this national trend, securing a role in the country’s energy transition framework.

Distributed Energy Storage Market to Hit $16.26B

The chart projects significant financial growth in the energy storage market. This projected market value provides the rationale for the massive ‘$80 B Battery Investments’ mentioned in the section heading, justifying the scale of Petro China’s strategic financial commitment to its upstream materials play.

(Source: Precedence Research)

China’s BESS Market, Petro China’s Domestic Supply Chain Focus

In 2025, Petro China‘s energy storage activities became sharply focused on the domestic Chinese market, where state policy has catalyzed the world’s largest and most rapidly expanding BESS sector. This marks a strategic shift from its prior international energy ventures, such as the Ksi Lisims LNG project, toward capturing value from the immense build-out happening within its home market.

- Before 2025, Petro China‘s diversification efforts were often linked to its global oil and gas footprint. The decision to enter battery metals trading is a pivot to serve a purely domestic manufacturing and deployment boom, driven by China’s energy security and decarbonization goals.

- The sheer velocity of China’s market growth dictates this focus. In July 2025 alone, the country registered 1, 468 new energy storage project applications, adding nearly 140 GWh of capacity to the national development pipeline, representing a massive addressable market for material suppliers.

- This domestic concentration is underpinned by robust policy support. A national action plan for 2025-2027 aims to strengthen the entire energy storage value chain, while a compensation standard of RMB 0.35/k Wh for standalone storage projects ensures their economic viability and, by extension, the demand for raw materials.

China’s Annual Solar Additions Surge to 315 GW

This section focuses specifically on ‘China’s BESS Market’ and a ‘Domestic Supply Chain Focus’. The chart, showing a massive surge in China’s domestic solar additions, quantifies the primary driver creating demand within that specific market, making it the perfect illustration for this section.

(Source: Green Finance & Development Center)

BESS Maturity, Petro China Targets Supply Chain over Integration

The rapid commercialization of BESS technology in China by 2025 created a market dynamic that led Petro China to target the upstream supply chain for materials rather than enter the crowded field of system integration. The company’s strategy suggests an assessment that as BESS technology becomes commoditized, sustainable profit margins will be found in the less mature, more constrained segments of the value chain, such as mineral supply.

- Between 2021 and 2024, BESS technology rapidly advanced, but market structures were still developing. By 2025, the technology was sufficiently mature to enable mass deployment, as evidenced by stable prices for DC blocks and installations surpassing 100 GW.

- This maturity has led to intense price competition among BESS manufacturers and integrators. Petro China‘s 2025 entry into metals trading is a strategic choice to avoid these thin margins and instead focus on the upstream market, where supply bottlenecks create pricing power.

- This “picks and shovels” strategy is a classic response to a technology gold rush. Instead of mining for gold (operating BESS projects), Petro China is selling the essential equipment (raw materials), a business model that leverages its core competency in global commodity trading.

Battery Makers Announce Larger, More Powerful Cells

The chart’s headline is direct evidence of the ‘BESS Maturity’ described in the section. The development of larger, more powerful cells indicates that the core technology is advancing and standardizing, which supports Petro China’s strategic decision to focus on the supply chain rather than competing on fundamental technology integration.

(Source: Energy-Storage.News)

Petro China BESS Strategy SWOT Analysis (2025)

Petro China‘s 2025 pivot into the battery supply chain leverages its core commodity trading strengths and vast capital to seize a high-growth opportunity, yet it also introduces new dependencies on volatile global mineral markets and potential conflicts with its primary fossil fuel identity.

Table: SWOT Analysis for Petro China BESS Supply Chain Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strength | World-class global oil and gas trading infrastructure and expertise in commodity markets. | Leverages existing trading infrastructure and expertise to enter the lithium and copper markets. | The company validated it could apply a core competency to a new, high-growth energy market, de-risking its entry. |

| Weakness | Minimal to no experience in renewable energy or BESS project development and operations. | The strategy deliberately avoids direct operations, mitigating this weakness but not developing new capabilities. | The weakness of operational inexperience in new energy remains, confirming the strategy is a financial and trading play, not a technological one. |

| Opportunity | Broad, undefined goals related to the long-term energy transition and diversification. | The specific, massive opportunity of China’s >100 GW BESS market, backed by the 2025-2027 national action plan. | The opportunity became concrete, quantifiable, and policy-backed, providing a clear business case for entry into the battery supply chain. |

| Threat | Long-term risk of declining global demand for fossil fuels and associated stranded assets. | New, more immediate risks: price volatility of battery metals, geopolitical risks in mineral supply chains, and intense competition from established metals traders. | The company traded a long-term existential risk for a new set of immediate, high-stakes market and geopolitical risks. |

Vertical Integration, Petro China’s Next Step in BESS Supply Chain

Having established its presence in battery metals trading in 2025, the critical development to monitor is Petro China‘s potential move toward vertical integration by acquiring stakes in physical mining or processing assets. Such a move would signal a deeper, long-term commitment to the battery supply chain and a strategy to secure physical control over resources, mirroring its historical approach in the oil and gas sector.

- If Petro China‘s initial trading operations prove successful and profitable, this will build the business case for deeper integration.

- Watch for announcements of joint ventures, offtake agreements, or direct acquisitions involving lithium, copper, or nickel mining operations, particularly in regions like South America, Africa, and Australia.

- These could be happening if Petro China intends to compete directly with established mining and trading houses that have extensive upstream asset ownership, which provides a physical hedge against market volatility. The ability to manage a modern grid will rely on such stable supply chains.

- A secondary signal would be the expansion of its trading book beyond lithium and copper to include other critical battery materials like nickel, cobalt, and graphite, positioning it as a comprehensive supplier to battery manufacturers.

The questions your competitors are already asking

This report covers one angle of PetroChina’s strategic entry into the battery energy storage supply chain. The questions that matter most depend on your work.

- What is actually happening with PetroChina’s new battery metals trading unit since its launch in 2025?

- What is the outlook for China’s BESS deployment, and will the market sustain the growth rate needed to absorb a 140 GWh pipeline?

- Which BESS integrators and battery manufacturers are the primary customers for PetroChina’s upstream critical metals strategy?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.