BP BESS Strategy, 13 GW JERA JV, $10 B CCS Deal, and Halts US Offshore Wind Project (2021-2026)

BESS Market Adoption, BP’s Partnership-Led Strategy vs. Record 92 GW Deployments

In 2025, BP’s approach to the Battery Energy Storage System (BESS) market is defined by a cautious, partnership-led strategy that contrasts sharply with the wider industry’s explosive, direct investment-fueled growth. While the global BESS market is experiencing record deployments and plummeting costs, BP is prioritizing large, integrated projects through joint ventures, treating storage as an enabling component rather than a primary investment focus.

- Prior to 2025, BP was steadily building its energy transition portfolio. The period from 2025 onward reveals a strategic shift towards immense, de-risked joint ventures. The company’s most significant moves include forming the JERA Nex bp offshore wind joint venture and advancing the Northern Endurance Partnership for Carbon Capture and Storage (CCS), signaling a preference for sharing risk on capital-intensive projects rather than pursuing standalone BESS developments.

- This contrasts with the broader BESS market, which is undergoing unprecedented expansion. Market forecasts for 2025 project a record 92 GW / 247 GWh in new installations, driven by falling all-in project costs, which dropped to as low as $125/k Wh. This has attracted aggressive investment from pure-play developers and competitors like Tesla Energy, who are moving quickly to capture market share.

- BP’s decision to halt the US Beacon Wind offshore project in October 2025 further highlights its conservative capital allocation. This move away from a project with high policy uncertainty stands in opposition to the strategies of other major utilities like Sempra Energy and Next Era Energy, which are pursuing massive grid modernization plans.

- Ultimately, BP is leveraging its integrated energy company structure to focus on long-term projects where BESS enhances the value of its own generation assets, such as offshore wind. This is a fundamentally different strategy from the rest of the market, which is focused on capturing immediate opportunities presented by the rapid growth of standalone storage.

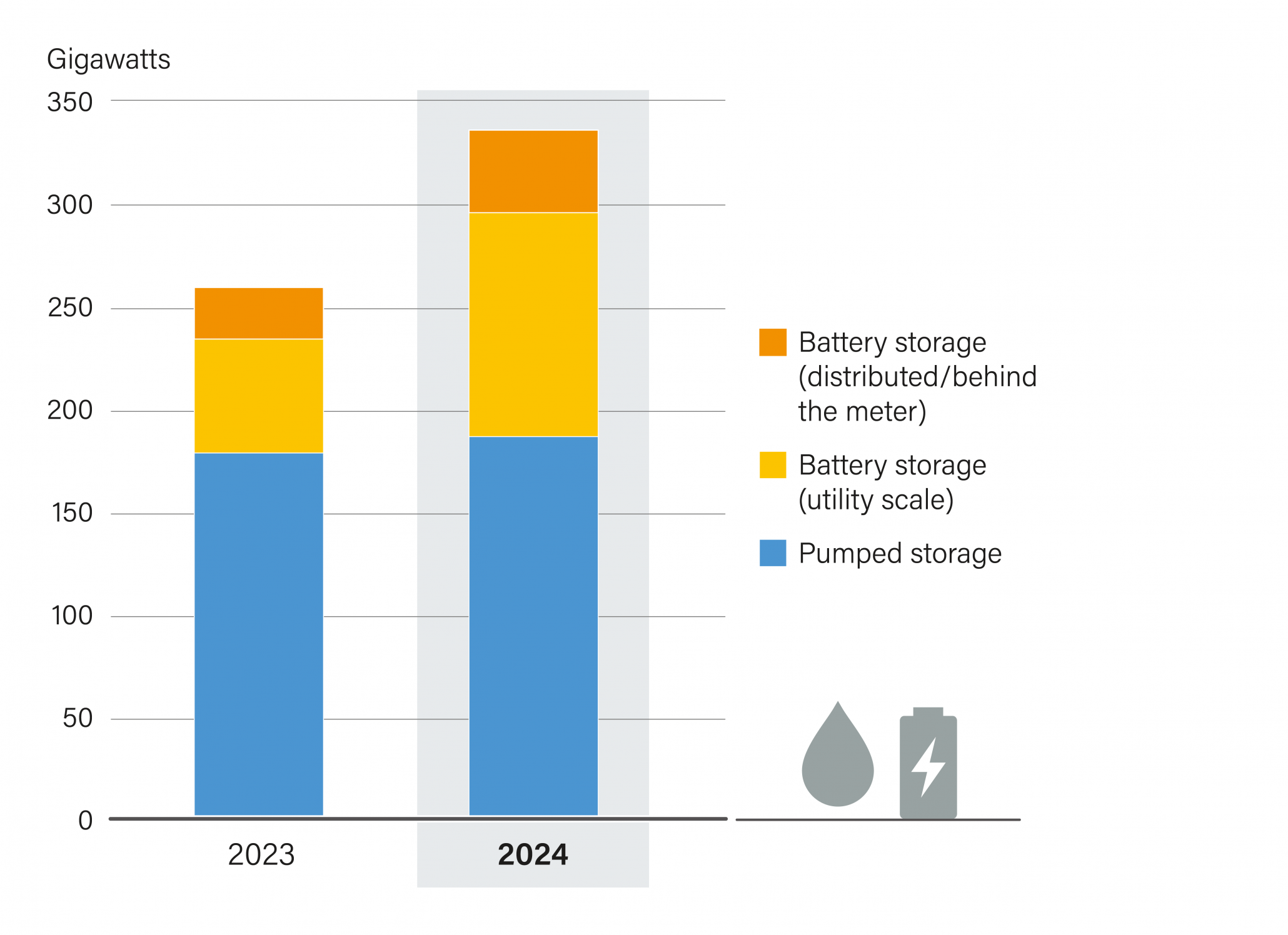

Battery Storage Drives Energy Capacity Growth

This chart highlights that battery storage is a primary driver of new energy capacity, which quantitatively supports the section’s premise of rapid BESS market adoption and the “Record 92 GW Deployments” mentioned in the heading.

(Source: REN21)

$10 B+ in Financing, BP Focuses on CCS While Halting US Offshore Wind

In 2025, BP’s capital activity was characterized by a major financing success in carbon capture and a significant project cancellation in renewables, signaling a strategic reallocation of capital away from uncertain markets and towards government-backed decarbonization initiatives. This demonstrates a disciplined, if conservative, investment posture in a volatile energy transition landscape.

- A primary example of this strategy is the Northern Endurance Partnership, a CCS joint venture with Equinor and Total Energies. In 2025, the project successfully secured over $10 billion in debt financing, underscoring BP’s commitment to industrial-scale decarbonization as a key pillar of its transition strategy, a field also being pursued by specialized firms like Deep Sky.

- Conversely, BP’s joint venture, JERA Nex, halted development of the Beacon Wind offshore project in the US in October 2025. Citing the lack of a “viable path for development, ” this major cancellation marks a strategic retreat from a key US renewables market, freeing up capital that could be redeployed to projects with more favorable risk profiles.

- Further reinforcing its preference for a partnership-based model, BP announced in February 2025 its intention to bring a strategic partner into its BESS business. This move is designed to leverage external capital and expertise for growth, rather than committing its own balance sheet to large-scale, direct investments in battery storage.

Table: BP Investment & Cancellation Highlights (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| JERA (JERA Nex JV) | Oct 2025 | Cancellation: Halted development of the Beacon Wind offshore project in the US, citing economic and policy inviability. This represents a significant strategic exit and capital reallocation from the US offshore wind market. | Recharge |

| Equinor, Total Energies | Jun 2025 | Investment: As part of the Northern Endurance Partnership, secured over $10 billion in debt financing for the UK’s East Coast Cluster CCS project, demonstrating a major capital commitment to industrial decarbonization. | IEA |

| Unspecified Partner | Feb 2025 | Strategic Search: Announced intent to bring a strategic partner into its BESS business to accelerate growth. This signals a preference for leveraging external capital over direct organic investment. | bp Annual Report 2024 |

Renewable Electricity Share Grew Across Sectors 2012-2022

This chart’s breakdown of historical renewable energy growth across different sectors provides a rationale for the specific investment and cancellation decisions by BP that are detailed in this section’s table.

(Source: REN21)

Europe vs. US, BP Doubles Down on UK/EU Projects While Exiting US Wind

BP’s geographical focus for its energy transition projects sharpened considerably in 2025, with a clear prioritization of European markets, particularly the UK and Germany, while the company executed a strategic retreat from a major US renewable power project due to perceived policy and economic instability.

- The most significant positive developments for BP’s low-carbon business in 2025 are concentrated in Europe. The Northern Endurance Partnership, a cornerstone of its CCS strategy, is a UK-based project that achieved a major milestone by securing over $10 billion in financing. This deepens BP’s investment in its home market.

- In Germany, BP’s offshore wind joint venture, JERA Nex bp, is in active negotiations with the government regarding the development of the 4 GW Oceanbeat project in the North Sea as of June 2026. A successful outcome would solidify its position as a major player in the European offshore wind market, a sector also being heavily contested by competitors like RWE.

- This European focus is starkly contrasted by the decision in October 2025 to cease development of the Beacon Wind project in the United States. The move, attributed to an “unviable path for development, ” suggests that BP views the US market, despite its incentives, as carrying a higher level of risk compared to the more familiar regulatory environments of Europe. This retreat comes as US grid operators like PJM grapple with massive interconnection queues for new generation and storage projects.

Renewables Grew to 32% of Global Power in 2024

This chart establishes the significant and growing share of renewables in the global power mix, providing the macro-level context for why BP is making major strategic realignments in its renewables portfolio, such as the geographic shift from the US to Europe.

(Source: REN21)

BESS Commercial Scale, BP Favors Integrated Application Over Standalone Projects

While BESS technology achieved full commercial maturity and unprecedented cost reductions in 2025, BP’s strategy treats it as an essential but subordinate component of larger energy systems, rather than a standalone investment class. The company is focused on integrating storage to enhance its own large-scale generation assets, not competing with pure-play developers on standalone battery projects.

- The BESS market in 2025 confirmed its commercial readiness, with turnkey project costs falling to as low as $125/k Wh and core equipment prices from China reaching approximately $75/k Wh. This has made standalone battery storage a highly attractive asset class for many investors and developers.

- BP’s actions, however, do not reflect a rush to develop standalone BESS projects. Instead, its future storage deployments are implicitly tied to the needs of its massive offshore wind pipeline, such as the 13 GW portfolio targeted by its JERA Nex bp joint venture. Storage here is an enabler, not the end product.

- The company’s significant investment in CCS also demonstrates a diversification of capital towards other mature decarbonization technologies. These technologies, along with emerging solutions like green hydrogen from companies such as Plug Power, compete with BESS for a finite pool of investment capital within BP’s portfolio.

- This integrated approach leverages BP’s strengths as a large, complex energy company. It allows the company to deploy storage strategically to firm up its own renewable generation and participate in grid services, creating value that may not be accessible to developers focused solely on standalone battery projects.

Energy Storage Technologies Mapped by Application

The chart visually maps different energy storage technologies to their commercial applications, directly illustrating the section’s topic of how BP is favoring integrated applications over standalone projects for its commercial-scale BESS strategy.

(Source: ScienceDirect.com)

SWOT Analysis, BP’s BESS Strategy and Market Positioning

BP’s BESS strategy leverages its core strengths in executing large, complex projects and forming powerful partnerships, but it also creates potential weaknesses related to a slower pace of adoption in a rapidly expanding market. The company’s approach is shaped by significant external opportunities, such as falling technology costs, and formidable threats from agile competitors and policy volatility.

Renewables Grow But Fossil Fuels Remain Dominant

This chart perfectly frames a core dynamic of the SWOT analysis: it illustrates both the “Opportunity” of growing renewables and the “Threat” of continued fossil fuel dominance for an energy major like BP.

(Source: REN21)

Table: SWOT Analysis for BP’s BESS Strategy (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong balance sheet and project management experience. Growing portfolio through Lightsource bp. | Demonstrated ability to execute massive JVs (JERA, NEP). Disciplined capital allocation by exiting non-viable projects (Beacon Wind). | The 2025 strategy validated BP’s ability to leverage its scale for large partnerships, but also its willingness to exercise capital discipline, a key strength in a volatile market. |

| Weaknesses | Pace of transition and BESS deployment perceived as slow compared to peers. Dual-investment message (oil & gas vs. renewables). | Strategic reset in Feb 2025 re-emphasizing hydrocarbons sent mixed signals. Lack of major standalone BESS project announcements risks ceding market share. | The 2025 strategic pivot confirmed that BESS is not the primary growth driver, making BP a cautious follower rather than a market leader and potentially slowing its capture of early-mover advantages. |

| Opportunities | Growing global demand for grid storage. Policy support like the US Inflation Reduction Act (IRA). | Record-low BESS costs ($125/k Wh all-in). Massive market growth (projected 92 GW in 2025). Opportunity to integrate storage with EV charging (bp pulse). | The dramatic drop in BESS costs in 2025 created a massive opportunity that BP appears to be addressing cautiously, primarily through its Lightsource bp solar pipeline, rather than through aggressive, direct investment. |

| Threats | Competition from pure-play storage developers and other integrated energy companies. Supply chain constraints. | Intense price competition and margin erosion from oversupply of Chinese equipment ($75/k Wh). Policy uncertainty leading to project cancellations (Beacon Wind). | The 2025 cancellation of Beacon Wind validated the real-world impact of policy uncertainty. Intense market competition from both established players and new entrants became a more acute threat as market growth accelerated. |

BP 2026 Outlook, Watch for BESS Partner and Capital Redeployment

The primary indicator of BP’s commitment to the BESS market over the next 12 to 18 months will be its success in securing a strategic partner for its storage business and how it chooses to redeploy capital following its exit from the US offshore wind market.

- If this happens: BP announces a major acquisition of a BESS developer or a series of large-scale, direct investments in solar-plus-storage projects via its subsidiary Lightsource bp.

Watch this: This would signal a significant strategic shift towards aggressively capturing market share and a renewed commitment to competing directly with pure-play storage developers. - If this happens: A strategic partner for BP’s BESS business is announced in the coming year.

Watch this: The identity of the partner is critical. A technology firm could signal a focus on innovation, while a large financial player would suggest an emphasis on scaling up deployment through project financing. - If this happens: BP’s capital allocation in its next annual report continues to heavily favor CCS, hydrogen, or new hydrocarbon projects over renewables and storage.

Watch this: This would confirm that the 2025 strategic pivot remains firmly in place and that BESS will continue to be a secondary, albeit important, component of its broader energy transition strategy. The development of new technologies like lithium-sulfur batteries by companies such as Lyten could also influence long-term investment decisions.

Energy Storage Market Projects Strong Growth

The chart’s strong growth projection for the energy storage market underscores the urgency and importance of BP’s 2026 outlook, highlighting why moves like securing BESS partners and redeploying capital are critical to capturing future value.

(Source: Precedence Research)

The questions your competitors are already asking

This report covers one angle of BP’s capital allocation strategy in the energy transition. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the utility-scale BESS market?

- Is BP’s de-risked, partnership-led strategy a good investment compared to the direct BESS deployment models of competitors?

- What is actually happening with the JERA Nex bp offshore wind joint venture since the announcement?

- What is the outlook for US offshore wind projects following BP’s halt of the Beacon Wind project?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.