Petro China LNG Strategy, CAD $40 B LNG Canada JV with Shell, 14 MTPA Capacity, and 3 Major Agreements (2025 to 2026)

Petro China LNG Projects and Global Market Diversification

In 2025, Petro China’s liquefied natural gas (LNG) strategy reached a critical execution phase, shifting from project development to operational reality by balancing international supply diversification with aggressive domestic production to enhance China’s energy security. The commissioning of major overseas assets, particularly in North America, marks a deliberate move to de-risk its supply portfolio from geopolitical volatility and reduce exposure to unpredictable spot markets, a strategy that was in the planning and construction stages prior to 2025.

- Prior to 2025, Petro China’s international strategy was characterized by large-scale capital commitments to projects under construction. The focus was on securing future supply through equity stakes and long-term development plans.

- The turning point in 2025 is the operational launch of the LNG Canada project, which shifts the company’s role from an investor in a construction project to an offtaker from a producing asset. First cargo from the facility was shipped in June 2025, marking Canada’s entry as a global LNG exporter.

- This new supply from a stable North American jurisdiction provides Petro China a critical hedge against potential disruptions from other regions. The company’s trading arm, Petro China International, explicitly stated its interest in securing more North American volumes to mitigate market risks.

- Concurrently, Petro China’s parent, CNPC, advanced its African position with the Final Investment Decision (FID) for the Coral North project in Mozambique in October 2025, further diversifying its long-term supply portfolio beyond its established partners.

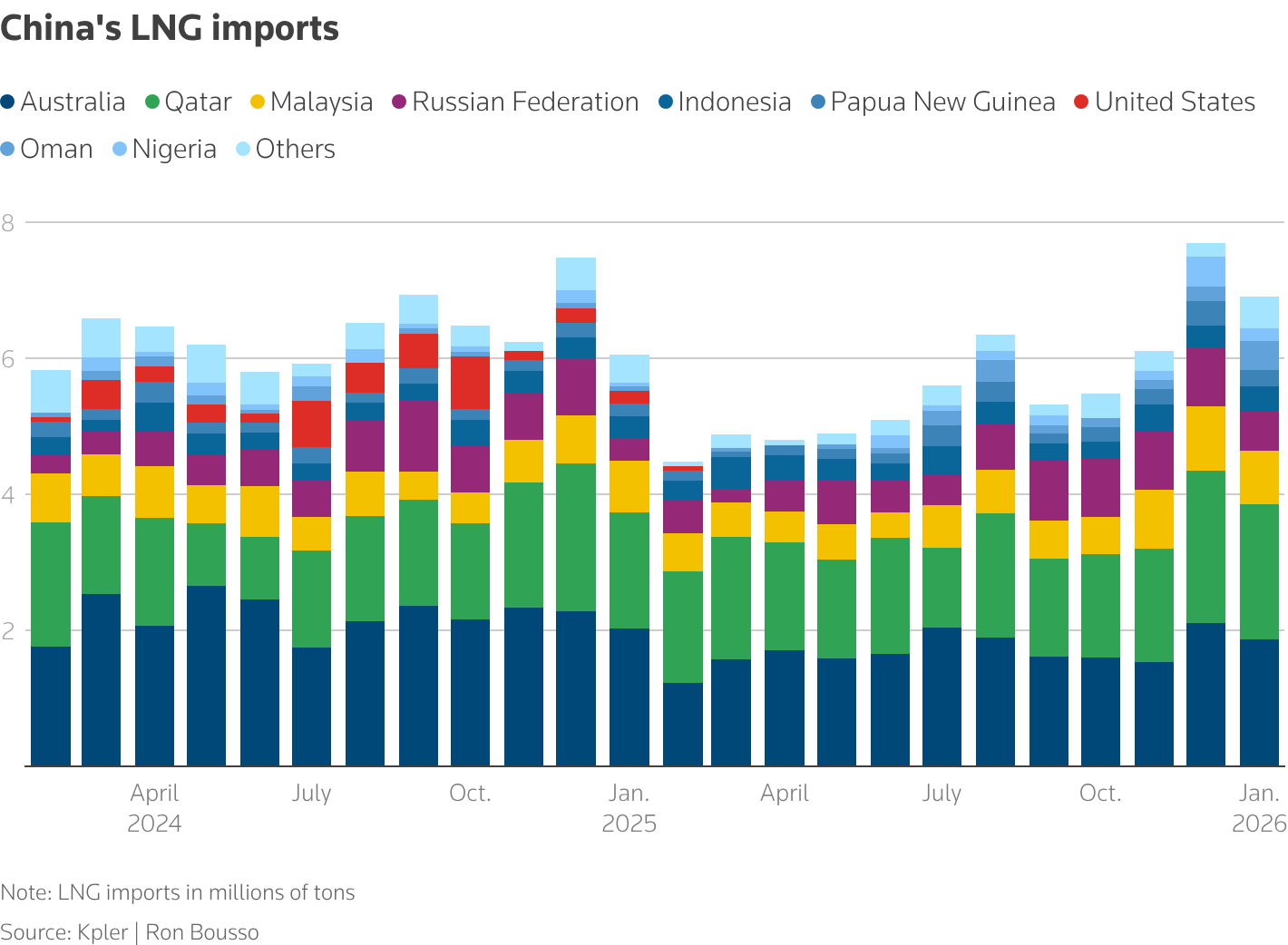

China’s LNG Imports Show Diverse Supplier Mix

This chart visually represents the concept of market diversification from the perspective of PetroChina’s home market, providing context for the company’s own diversification strategy discussed in this section.

(Source: The Columbia Emerging Markets Review)

$38 B in CAPEX, Petro China LNG Infrastructure Investments

Petro China is directing substantial capital towards solidifying its control over the entire natural gas value chain, with a disciplined 2025 capital expenditure plan funding both international offtake projects and crucial domestic infrastructure. These investments are designed to absorb new international supplies and fortify the national energy grid against demand surges and price shocks, a clear strategic priority for the year.

- Petro China allocated a total capital expenditure of RMB 275.8 billion (approximately $38 billion) for 2025, with a significant portion targeted at its gas and new energy businesses to support production and infrastructure growth.

- The most significant international investment to come online is the CAD $40 billion Phase 1 of the LNG Canada project, which began commercial operations in mid-2025 and provides Petro China its equity share of 14 MTPA in capacity.

- Following the successful launch, the joint venture is now evaluating a CAD $33 billion Phase 2 expansion, which would double the facility’s production capacity and deepen Petro China’s North American supply access.

- Competitors are also advancing major projects, with Total Energies reaching FID on the 9.6 MTPA Ruwais LNG project in the UAE in May 2025, highlighting the global push to secure future liquefaction capacity.

Global LNG Infrastructure Market to Exceed $116B

The chart provides the macro-level context for PetroChina’s specific $38B CAPEX by showing the total size of the global LNG infrastructure market, highlighting the scale of the sector.

(Source: Market.us)

Table: Petro China Key LNG Project Investments (2025)

| Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| LNG Canada Phase 2 (Proposed) | Post-2025 | A potential CAD $33 billion expansion that would double the plant’s production capacity, further securing long-term North American LNG supply for Petro China and its partners. | Canadian Indigenous Investment Forum |

| Full Year 2025 Capital Expenditure | 2025 | Petro China planned a disciplined RMB 275.8 billion (~$38 B) CAPEX for 2025 to fund oil, gas, and new energy segments, including domestic infrastructure and international LNG projects. | Petro China |

| LNG Canada Phase 1 | Mid-2025 | The CAD $40 billion project began commercial operations, with the first cargo shipped in June 2025. It provides 14 MTPA of LNG capacity, with Petro China offtaking its equity share. | PR Newswire |

Petro China 3 Major LNG Joint Ventures and Agreements

Petro China leverages strategic joint ventures with global energy majors to secure its international LNG supply, with the LNG Canada partnership serving as the prime example of this model in 2025. These alliances grant Petro China direct equity in production assets, providing more stable, long-term supply compared to relying on the volatile spot market.

- The LNG Canada joint venture, which became operational in mid-2025, is Petro China’s most significant partnership. It joins Shell, PETRONAS, Mitsubishi Corporation, and KOGAS in a project that secures 1.8 Bcf/d of Canadian LNG for its members.

- In October 2025, Petro China’s parent CNPC (20% stake) joined a consortium led by Eni (50%) that reached a Final Investment Decision on the Coral North LNG project in Mozambique, expanding its long-term supply footprint in Africa.

- To enhance its trading capabilities, Petro China International partnered with BP in September 2025 to acquire long-term regasification and storage capacity at the Gate LNG terminal in Europe, giving it a foothold in the continent’s liquid market.

Global LNG Market Growth Forecast to 2034

The long-term market growth forecast shown in this chart provides the strategic rationale for PetroChina forming major joint ventures and agreements to secure future LNG supply.

(Source: Polaris Market Research)

Table: Petro China Strategic LNG Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Eni, Kogas, ENH, XRG (ADNOC) / Coral North Project | Oct 2025 | CNPC (Petro China’s parent) holds a 20% stake in this Mozambique LNG project, which reached FID. It diversifies supply with assets in the Rovuma Basin. | Eni |

| BP / Gate LNG Terminal | Sep 2025 | Petro China acquired long-term regasification and storage capacity in Europe, enhancing its global trading flexibility and ability to optimize its LNG portfolio. | S&P Global |

| Shell, PETRONAS, Mitsubishi, KOGAS / LNG Canada | Jun 2025 | This JV began commercial operations, exporting 1.8 Bcf/d. Petro China secures a stable supply of North American LNG, diversifying away from other regions. | ACCC |

North America vs. Asia, Petro China Geographic Focus

Petro China’s geographic strategy in 2025 pivoted from a primary focus on Asian and Russian pipeline supply to actively operationalizing a new, major supply corridor from North America. While China remains the core demand center, the company’s activities demonstrate a clear intent to build a globally balanced portfolio, with assets in Canada providing a counterweight to its existing supply routes and new infrastructure in Europe enabling a more dynamic trading presence.

- From 2021-2024, Petro China’s geographical efforts were concentrated on developing Russian pipeline connections (Power of Siberia) and securing contracts from traditional LNG suppliers like Qatar and Australia.

- In 2025, North America became a physical supply source, not just an investment destination. The launch of LNG Canada in British Columbia establishes a trans-Pacific route that diversifies supply away from the Strait of Hormuz and other potential chokepoints.

- Simultaneously, Petro China is expanding its domestic infrastructure in China to absorb these new international volumes. The company is a key driver of China’s plan to add over one-third of Asia’s new regasification capacity by 2030.

- Europe also became a new operational hub in 2025. By securing capacity at the Gate terminal in the Netherlands, Petro China established a strategic outpost to trade LNG and serve European customers, capitalizing on regional price differentials.

North America to Lead LNG Market Through 2035

This chart directly supports the section’s theme by quantifying North America’s leading role in the LNG market, explaining why it is a key geographic focus for PetroChina’s strategy.

(Source: Market Research Future)

SWOT Analysis, Petro China LNG Strategy

Petro China’s LNG strategy in 2025 is validated by the successful commissioning of long-term projects, yet it also faces market volatility and high capital demands. The strategic shift towards a more diversified and resilient supply chain is evident when comparing the pre-2025 development period with the operational realities of 2025.

- Strengths: Diversified supply portfolio and direct equity ownership in key international production assets.

- Weaknesses: High capital intensity of large-scale LNG projects and long investment return cycles.

- Opportunities: Leveraging new, flexible North American cargoes for global trading and expansion into new markets.

- Threats: Global economic slowdown impacting LNG demand and price volatility affecting profitability.

Global LNG Demand Forecasted to Outstrip Supply

This forecast of demand outstripping supply perfectly encapsulates a primary Opportunity (unmet demand) and Threat (supply competition) for PetroChina, which are core components of a SWOT analysis.

(Source: Canada LNG Group)

Table: SWOT Analysis for Petro China’s LNG Initiatives

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong balance sheet and government backing for large-scale, long-term investments. Established pipeline gas relationships (e.g., Russia’s Gazprom). | Operational control of diversified supply from North America (LNG Canada) and Africa (Mozambique FID). Increased domestic gas output (+5% in 2024) and massive storage investments ($3.6 B with Pipe China). | The strategy to build a diversified portfolio was validated. Petro China is no longer just reliant on pipeline gas and traditional LNG suppliers; it now has physical equity barrels from North America. |

| Weaknesses | High capital expenditure on projects under construction (e.g., LNG Canada) with no immediate return. Exposure to construction delays and cost overruns. | Continued high CAPEX (~$38 B in 2025). Exposure to market price risk as new volumes (14 MTPA from LNG Canada) come online. | The weakness shifted from construction risk to market risk. The company now has to profitably place its new equity volumes in a complex global market. |

| Opportunities | Anticipated growth in China’s domestic gas demand. Potential to diversify supply sources by investing in new liquefaction projects. | Securing flexible, destination-free North American LNG for global trading. Potential FID on LNG Canada Phase 2. Expected 25% rebound in Chinese LNG import growth in 2026. | The opportunity moved from theoretical to actual. With LNG Canada operational, Petro China can now actively trade and optimize a global portfolio, not just procure for domestic use. |

| Threats | Geopolitical tensions impacting existing suppliers. Volatility in global LNG spot prices affecting import costs. | Global market tightness expected in 2025 due to strong European demand. Increased competition for available LNG cargoes. Potential for slower-than-expected Chinese demand recovery. | The threat of supply chain disruption from traditional sources was mitigated by diversification. The new primary threat is increased competition and price volatility in the global market where it now actively participates as a major seller. |

Petro China LNG Canada Phase 2 and Future Offtake Agreements

The most critical variable for Petro China’s LNG strategy beyond 2025 is whether the joint venture proceeds with the Final Investment Decision for LNG Canada’s Phase 2 expansion. This single decision will determine if the company doubles down on its North American supply base, significantly altering its long-term portfolio and capital allocation priorities.

- If this happens: The LNG Canada partners approve the CAD $33 billion Phase 2 expansion.

- Watch this: Announcements from Shell (the project operator) or Petro China regarding progress on front-end engineering and design (FEED) work and securing commercial offtake for the new volumes.

- These could be happening: Petro China could be actively negotiating new long-term contracts with North American LNG projects beyond LNG Canada, seeking flexible terms to build out its trading portfolio in anticipation of a larger global presence. The company’s stated interest in destination-free cargoes is a key signal of this intent.

Operational LNG Terminals Increase Through 2027

As this section discusses the LNG Canada Phase 2 project, this chart provides relevant context by showing the global trend of increasing operational LNG terminals to meet rising demand.

(Source: Panda Perspectives – Substack)

The questions your competitors are already asking

This report covers one angle of PetroChina’s LNG project execution and market strategy. The questions that matter most depend on your work.

- Which national oil companies are gaining or losing ground in the race to secure long-term LNG supply from North America?

- PetroChina’s investments in LNG Canada. Is the project on track to meet its 14 MTPA Phase 1 capacity target?

- What is the market impact of LNG Canada’s first cargo, and is PetroChina successfully hedging against spot market volatility?

- What are the opportunities for other North American and African LNG projects to secure long-term agreements with Chinese buyers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.