Oregon Data Center Tariffs: How New Rate Classes Shift $210 M in Infrastructure Costs from Ratepayers (2024-2026)

Data Center Projects Face New Risks as Oregon Adopts Cost-Causer Pays Model

Oregon’s regulatory shift from a socialized cost model to a “cost-causer pays” framework fundamentally alters the risk profile and project economics for data center development, ending an era of implicit ratepayer subsidies. This new paradigm, crystalized between 2024 and 2026, forces data center operators to internalize the full cost of the grid infrastructure their facilities require, introducing significant new financial and operational risks.

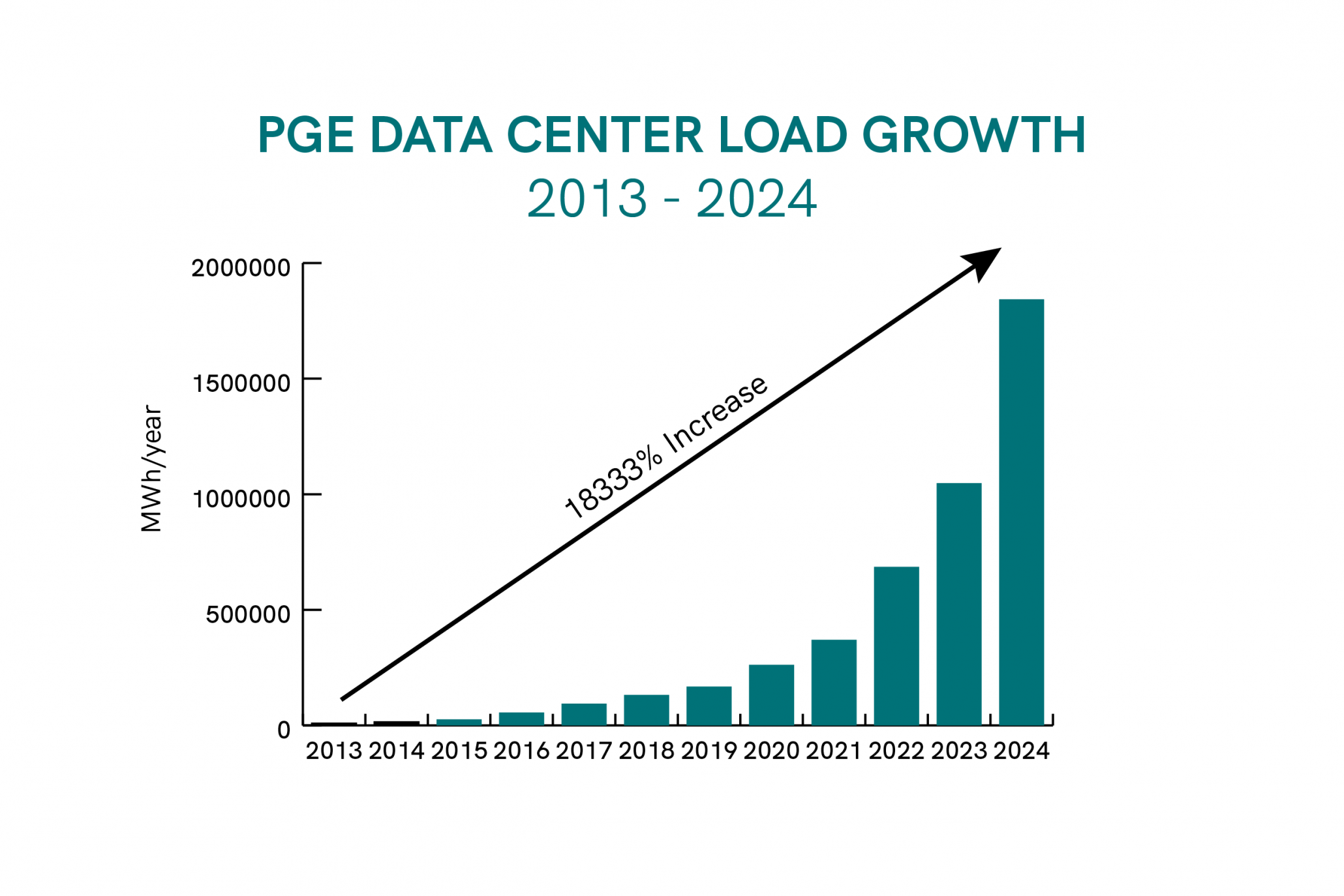

- Between 2021 and 2024, Oregon’s favorable tax incentives and historically low-cost power attracted massive data center investment, with industrial customers (including data centers) driving a 34% increase in power demand on Portland General Electric’s (PGE) system alone. During this period, infrastructure costs were socialized across all ratepayers, effectively subsidizing the industry’s growth.

- The legislative and regulatory landscape changed dramatically starting in 2025 with the passage of the POWER Act. This was followed by the Oregon Public Utility Commission’s (OPUC) December 2024 approval of new tariffs for Pacifi Corp and PGE’s subsequent framework approval in May 2026, which applies to new or expanding loads over 20 MW.

- The new framework ends what was estimated to be over $210 million in ratepayer subsidies for tech companies. It requires operators to directly fund their own transmission and energy infrastructure, significantly increasing upfront capital expenditures and negatively impacting project investment returns compared to markets like Virginia.

- A new layer of operational risk was introduced with Pacifi Corp’s tariff, which mandates that large customers forecast their annual energy needs with at least 95% accuracy. Failure to meet this threshold results in an “Excess Demand Charge, ” placing the financial burden of forecasting errors squarely on the data center operators.

PGE Data Center Power Demand Soars Pre-Regulation

This chart provides specific historical context for a major Oregon utility (PGE), showing the demand growth that prompted the regulatory changes and new risks discussed in this introductory section.

(Source: Oregon Citizens’ Utility Board)

$210 M Subsidy Shift: PGE and Pacifi Corp Rate Cases Alter Investment Calculus

The OPUC’s December 2024 decisions on rate cases for Pacifi Corp and PGE served as the primary catalyst for reallocating infrastructure costs, creating a subsidy cliff that reshapes the financial models for data center investment in the state. While general rate hikes were approved, the rulings’ most significant long-term impact comes from the creation of a new “very large load” customer class designed to wall off infrastructure costs from residential and small commercial customers.

- The OPUC approved an overall 8.5% rate increase for Pacifi Corp customers and a 5.5% to 7.7% increase for PGE customers, effective in 2025. However, the new tariff structures ensure that future capital costs for grid expansions needed to serve data centers will be borne directly by those facilities, not the general rate base.

- PGE’s CEO publicly acknowledged that residential customers had been subsidizing the load growth of large industrial clients, a practice the new tariffs are explicitly designed to terminate. This confirms the policy’s intent to correct a structural imbalance in cost allocation.

- The material impact of this financial shift was evidenced by strong opposition from the tech industry. Meta, which operates a large data center campus in Prineville, argued against the new charges, highlighting the financial risks and forecasting difficulties the policies impose on its operations.

PGE Rate Hikes Disproportionately Hit Households

This chart directly illustrates the ‘subsidy’ issue at the heart of the PGE rate case, showing how residential ratepayers previously bore a greater burden, which the new ‘cost-causer’ model aims to rectify.

(Source: Oregon Citizens’ Utility Board)

Table: Oregon Utility Regulatory Decisions (2024)

| Utility / Decision | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Portland General Electric (PGE) | Dec 2024 / May 2026 | OPUC approved a large-load tariff framework in May 2026 for new loads over 20 MW, mandating direct payment for infrastructure. The decision followed a general rate case approval in Dec 2024. | Utility Dive |

| Pacifi Corp (Pacific Power) | Dec 2024 | OPUC approved a new tariff structure for very large load customers, including a capacity reservation charge and an excess demand charge for inaccurate load forecasting (less than 95% accuracy). | Data Center Dynamics |

| Consumer Advocacy (CUB) | Dec 2024 | The Citizens’ Utility Board (CUB) supported the new tariffs, arguing they protect residential customers from unfairly subsidizing infrastructure built for a few large industrial clients. | Portland Business Journal |

Oregon vs. Virginia: New Tariffs Create a Competitive Disadvantage for the Pacific Northwest

Oregon’s new tariff structure creates a significant competitive cost disadvantage compared to leading data center markets like Northern Virginia, fundamentally shifting the state’s value proposition away from low-cost power and toward a model emphasizing energy self-sufficiency and regulatory predictability. This policy may slow the pace of new hyperscale development in the state as operators re-evaluate total project costs.

- Prior to 2024, Oregon was a premier destination for data centers, with communities like Hillsboro and Prineville becoming major hubs due to a combination of tax incentives, a skilled workforce, and cheap, socialized grid costs.

- Post-2025, the “all-in” cost of power in Oregon is now significantly higher for new projects, as it must include the amortized cost of new substations and transmission lines. This contrasts sharply with Virginia, which continues to offer highly competitive commercial electricity rates between $0.06 and $0.08 per k Wh without a similar direct funding mandate.

- The regulatory action in Oregon provides a blueprint for other regions facing similar challenges. As data center demand strains grids nationally, states are beginning to review their policies. For example, Texas regulators are evaluating how new market structures on the ERCOT grid could enhance reliability amid soaring demand, showing a nationwide trend toward addressing the impacts of large, concentrated loads.

- This policy divergence positions Oregon as a pioneer in sustainable grid management but risks ceding new growth to states that continue to socialize infrastructure costs. The long-term effect may be a bifurcation of the market, with some operators prioritizing low initial Cap Ex in other states while others invest in Oregon for its clear, long-term regulatory framework.

Policy Maturity: Oregon’s Cost-Causer Model Sets a National Precedent for Grid Management

Oregon’s regulatory framework has rapidly matured from a legislative concept in 2025 to a fully implemented, commercially tested policy model by mid-2026, establishing a new standard for managing hyperscale energy demand that other state utility commissions are now closely watching. This policy directly incentivizes the adoption of mature, commercially available technologies to offset its financial impacts.

- The 2021-2024 period was defined by a reactive and immature regulatory environment where utilities struggled to manage exponential load growth using outdated tariff structures, resulting in growing ratepayer risk and cross-subsidization.

- The POWER Act, passed in 2025, represented a critical maturation point, creating the legal authority to design and implement a more equitable cost-allocation model. This moved the solution from a recognized problem to a formal policy initiative.

- By May 2026, with the OPUC’s approval of PGE’s tariff framework, the policy reached full maturity. It is now an enforceable commercial mechanism that creates a strong business case for on-site power and energy efficiency, as these investments directly mitigate the new infrastructure charges.

- The policy accelerates the market for data center efficiency technologies. With cooling accounting for up to 40% of energy use, the global data center liquid cooling market, valued at $6.65 billion in 2025 and projected to grow at a 20.1% CAGR, will see accelerated adoption in Oregon as operators work to lower their Power Usage Effectiveness (PUE) and operating costs.

POWER Act Aims to Protect Ratepayers From Data Center Costs

As this section discusses Oregon’s policy as a national precedent, a chart on a federal act with similar goals demonstrates the issue’s national significance, reinforcing Oregon’s pioneering role.

(Source: Climate Solutions)

SWOT Analysis: Oregon’s Data Center Policy and Market Outlook

The new policy framework introduces major financial risks for data center operators by increasing upfront costs, but it simultaneously creates significant strengths for Oregon’s long-term grid stability and new market opportunities for clean technology providers. This shift redefines the state’s role in the national data center market, trading low-cost energy for regulatory clarity and a focus on sustainability.

Data Center Power Demand to Nearly Triple

This forecast of massive demand growth is a fundamental component of a SWOT analysis, representing both a major ‘Opportunity’ for the market and a ‘Threat’ to grid stability and affordability.

(Source: ElectricChoice.com)

Table: SWOT Analysis for Oregon’s New Data Center Rate Class

| SWOT Category | 2021 – 2024 (Pre-Policy) | 2025 – 2026 (Post-Policy) | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Low-cost power and favorable tax incentives attracted major tech investment (Meta, Amazon). | Protects residential ratepayers from subsidizing industrial growth. Creates regulatory certainty for utilities (PGE, Pacifi Corp) and a stable grid. | The policy resolved the issue of cross-subsidization, validating the “cost-causer pays” principle as a viable grid management strategy. |

| Weaknesses | Exponential load growth (34% on PGE) strained the grid and created future ratepayer risk. | Higher upfront Cap Ex and “all-in” energy costs for data centers reduce Oregon’s price competitiveness against states like Virginia. | The state’s primary weakness shifted from grid strain risk to reduced market attractiveness based on upfront project costs. |

| Opportunities | Continued expansion of data center campuses in Hillsboro and Prineville due to favorable conditions. | Creates a multi-gigawatt market for on-site power (solar, BESS) and energy efficiency solutions like liquid cooling (20.1% CAGR market). | The policy itself created a new, captive market for clean technologies by making them economically necessary to offset higher costs. |

| Threats | Risk of rolling blackouts or extreme rate hikes as demand outpaced infrastructure investment. | Data center developers may select alternative states with lower initial costs. Legal and political challenges from the tech industry. | The primary threat shifted from physical grid failure to capital flight, as developers weigh the new costs against locating elsewhere. |

Scenario Modelling: On-Site Power Adoption in Oregon’s Data Center Market

The most critical strategic response to Oregon’s new regulations will be an accelerated shift by data center operators toward developing on-site power generation and deploying advanced energy efficiency technologies to mitigate exposure to direct grid infrastructure costs. The policy makes energy self-sufficiency a financial necessity rather than an environmental choice.

- If this happens: Data center operators begin filing for permits to co-locate renewable generation and battery storage at their Oregon campuses. Watch this: An increase in announcements from major operators like Meta and Amazon detailing their strategies for on-site power to comply with the new tariffs.

- If this happens: The business case for on-site power and efficiency becomes overwhelmingly positive. Watch this: A surge in partnerships between data center operators and energy technology providers specializing in solar, battery storage, and advanced liquid cooling systems in Oregon.

- These could be happening: The POWER Act’s tax incentive for co-located power generation is already creating a direct financial driver. The combination of avoiding direct infrastructure funding and benefiting from tax incentives makes the ROI for on-site projects compelling. This signals a clear pathway for developers to de-risk their Oregon investments.

Grid Capacity Heavily Underutilized Outside Peak Hours

This chart illustrates a key technical variable—grid underutilization—that would be a critical input for the scenario modelling of on-site power adoption discussed in this section.

(Source: Information Technology and Innovation Foundation (ITIF))

The questions your competitors are already asking

This report covers one angle of the shifting economics for data center development in Oregon. The questions that matter most depend on your work.

- What is actually happening with PGE and PacifiCorp’s new data center tariffs since the OPUC’s approval?

- What is the impact of the new ‘cost-causer pays’ model on data center project investment returns and upfront capital expenditures in Oregon?

- How does the cost structure for new data center grid interconnections in Oregon now compare to competing markets like Virginia?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.