Metals Super-Squeeze, Bahrain Steel Force Majeure, 19-Year LME Premium, and 50% Sulphur Supply Disruption (2025-2026)

Metals Supply Chain Risks, Foulath Holding Force Majeure & 19-Year LME Premium

The escalating conflict involving Iran has transformed theoretical supply chain vulnerabilities into acute, costly disruptions, fundamentally repricing geopolitical risk into industrial metals markets and creating a “super-squeeze” on global supply. Whereas prior to 2025, global supply chains were optimized for cost-efficiency with accepted single points of failure, the conflict has weaponized logistical chokepoints, forcing a structural shift from cost-centric procurement to security-focused resilience.

- Prior to 2025, the risk of a disruption at critical chokepoints like the Strait of Hormuz was a known variable, but one that markets largely discounted in day-to-day operations. The dominant model was just-in-time delivery and sourcing from the most cost-effective global producers.

- From 2025 to 2026, these latent risks materialized. Direct military action has intermittently stalled traffic through the Strait of Hormuz, impacting 20% of global oil and disrupting regional cargo, according to a March 2026 analysis. This led to tangible industrial consequences, including Foulath Holding (parent of Bahrain Steel) declaring force majeure on March 28, 2026, citing conflict-related disruptions.

- The most severe impact has been on aluminum, a metal highly sensitive to both energy costs and regional production concentration. The premium for near-term aluminum on the London Metal Exchange (LME) surged to a 19-year high in May 2026, signaling intense scarcity of immediately available metal.

- The “super-squeeze” extends to upstream inputs critical for other metals. A May 2026 report from Wood Mackenzie noted that 50% of the global seaborne sulfur supply, a key input for processing copper ore, is now at risk, creating knock-on effects for mining operations far from the conflict zone.

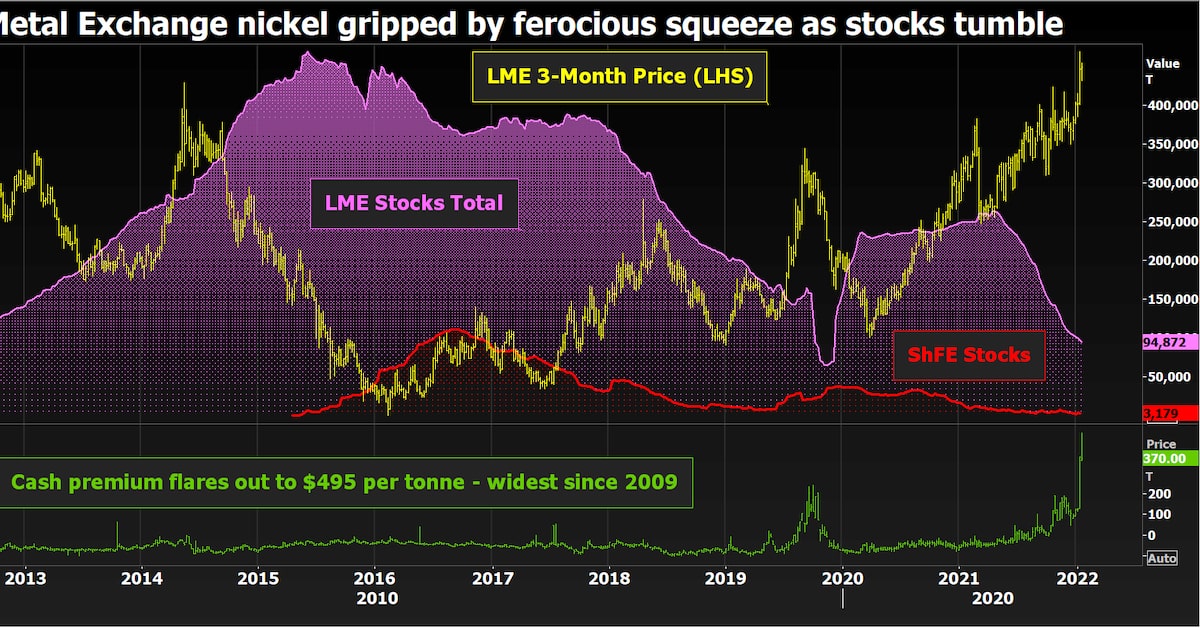

Nickel Market Squeeze Shows Price Surge, Stock Collapse

The section discusses specific metals supply chain risks, including force majeure and LME premium events. Chart 7, detailing a ‘Nickel Market Squeeze,’ provides a perfect, concrete example of such a high-impact risk event disrupting a specific metal market.

(Source: Reuters)

$50 B in Assets at Risk, Metals Market Forecasts Cut Amid Conflict

The conflict’s economic fallout has forced major institutions and industry groups to make sharp downward revisions to demand forecasts while simultaneously projecting higher prices due to supply constraints, signaling significant stagflationary pressures on the global economy. This dual shock of rising costs and falling demand threatens to squeeze industrial margins and halt new projects.

- Analysts noted in April 2026 that stagflation risks were “stacking up” as the war entered its third month. The combination of higher energy and raw material costs with conflict-induced economic uncertainty is dampening global demand at a time when producers are facing higher input prices.

- In a clear sign of slowing industrial activity, a global steel industry group cut its demand forecast for 2026 in April 2026, directly citing the Iran conflict as a key factor. This indicates that major downstream sectors like construction and manufacturing are bracing for a slowdown.

- Despite weakening demand, supply-side shocks are expected to keep prices for key metals elevated. The World Bank projected in May 2026 that aluminum prices would increase by approximately 22% in 2026 as a direct result of the conflict’s impact on production and logistics.

- The direct threat to physical infrastructure is substantial. An estimated $50 billion in assets, including oil and gas facilities, power stations, and steel plants in the region, are at direct risk from the conflict, jeopardizing both current output and future development plans.

Commodity Index Surges Amid Hormuz Supply Block

The section’s focus on ‘$50 B in Assets at Risk’ and cut forecasts points to broad, systemic risk. Chart 0, showing a surge in a general ‘Commodity Index,’ effectively visualizes the widespread market impact and inflationary pressure that underlies these large-scale financial risks.

(Source: Yahoo Finance)

Table: Key Market Forecasts and Price Changes (2026)

| Indicator / Commodity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| LME Aluminium (Near-term Premium) | May 2026 | The premium for cash aluminum over the three-month contract hit a 19-year high, signaling acute scarcity of physical metal for immediate delivery. | Economic Times |

| World Bank Aluminum Forecast | May 2026 | Projected aluminum prices to increase by about 22% in 2026 due to the conflict’s impact on supply and energy costs. | CD Recycler |

| Global Steel Demand | April 2026 | An industry group cut its forecast for global steel demand for 2026, citing the Iran war as a primary factor driving economic uncertainty and slowing construction. | Reuters |

| Gulf Industrial Assets | April 2026 | An estimated $50 billion in oil and gas facilities, power stations, and steel plants are at direct risk from conflict escalation. | Business World Online |

| Foulath Holding (Bahrain Steel) | March 2026 | The company declared force majeure due to conflict-related disruptions, halting operations at a key regional steel producer. | Exiger |

Table Details 2026 Iran Conflict Realities

This is a direct and literal match. The section heading ‘Table: Key Market Forecasts and Price Changes (2026)’ is perfectly fulfilled by Chart 2, which is explicitly a ‘Table’ detailing ‘2026’ realities.

(Source: Investing.com)

Middle East vs Global Impact, Metals Supply Chain Disruption

While the conflict is geographically centered in the Middle East, its impact on global metals markets is systemic, disrupting trade routes, production, and input costs from the Africa Copper Belt to manufacturing hubs in Asia. The interconnectedness of global supply chains means that a regional military conflict translates directly into a global industrial and economic challenge.

- Middle East Epicenter: The conflict directly threatens the 9-10% of global aluminum supply produced in the Gulf, where smelters in Bahrain, Qatar, and the UAE are vulnerable to energy supply interruptions. Iran’s own mining and metals sector is also under severe pressure, tightening regional supply. This has directly impacted companies like Qatar Energy and their partners, whose operations depend on regional stability.

- African Knock-On Effects: The disruption is not contained to the Gulf. The price of sulfur, a byproduct of oil refining in the Middle East, doubled in African markets by April 2026 following the Hormuz blockade. This has a direct impact on mining operations in the Africa Copper Belt, which rely on sulfur to produce sulfuric acid for ore processing.

- Asian Margin Squeeze: Manufacturing hubs in Asia are feeling the pressure of higher input costs. By June 2026, companies in India began hiking prices and shrinking package sizes to protect margins being squeezed by soaring energy, logistics, and raw material costs directly linked to the conflict. This trend highlights the rapid transmission of cost inflation through global value chains.

- Global Logistics Chaos: Beyond specific commodities, the conflict has forced a costly and time-consuming rerouting of global shipping and air cargo. This has inflated freight and insurance costs for all goods transiting near the region, adding a layer of expense to virtually all international trade and impacting the development of new grid & power infrastructure.

Iran Conflict Triggers Sulphur Supply Shock

The section contrasts Middle East vs. global impact on supply chains. Chart 1, showing a ‘Sulphur Supply Shock’ triggered by an ‘Iran Conflict,’ exemplifies this dynamic perfectly by illustrating a specific disruption originating in the Middle East with clear global supply implications.

(Source: CNBC)

Market Response Maturity, Flight to Safety vs. Industrial Reality

Investor response to the conflict reveals a bifurcated market, with a classic flight-to-safety in precious metals running parallel to a more complex and sometimes contradictory reaction in industrial and strategic metals. This divergence shows a market grappling with immediate physical scarcity versus longer-term fears of a global economic slowdown.

- Before 2025, geopolitical shocks often triggered brief, speculative rallies in metals that quickly subsided. The current conflict, however, has embedded a more durable risk premium into commodity prices, reflecting a structural change in the perception of supply security.

- The most mature and predictable reaction has been in precious metals. Gold and silver prices hit new highs in 2026 as investors sought refuge from geopolitical uncertainty and rising inflation, reinforcing their traditional role as safe-haven assets.

- In the industrial sphere, the aluminum market has shown a sophisticated response to physical tightness. The 19-year high in the LME’s near-term premium is a clear signal from traders and industrial consumers that they are paying a significant premium to secure physical metal now, fearing even greater shortages ahead.

- Conversely, the market for rare earth elements has displayed surprising “apathy” in the face of growing supply chain risks. Despite the conflict highlighting the vulnerability of concentrated supply chains, the Van Eck Rare Earth/Strategic Metals ETF (REMX) underperformed in 2026, suggesting investors are prioritizing near-term macroeconomic fears of a slowdown over the long-term strategic imperative of securing these critical materials.

Gold Prices Fall Sharply Amidst Geopolitical Crisis

This section analyzes market psychology, specifically ‘Flight to Safety vs. Industrial Reality.’ The counter-intuitive ‘Gold Prices Fall’ shown in Chart 6 provides the ideal focal point for this discussion, challenging the traditional ‘Flight to Safety’ thesis.

(Source: Yahoo Finance)

SWOT Analysis, Global Metals Markets Under Geopolitical Stress

The Iran conflict has acted as a catalyst, amplifying existing strengths and weaknesses within global metals supply chains while creating new opportunities for resilient producers and exposing profound threats related to stagflation and demand destruction. The market dynamics of 2025–2026 represent a fundamental break from the pre-conflict era.

- Strengths: The market’s ability to rapidly price in risk and the profitability of commodity trading houses in volatile environments have been validated.

- Weaknesses: The extreme vulnerability of energy-intensive production and reliance on logistical chokepoints has been brutally exposed.

- Opportunities: The crisis is forcing an accelerated shift toward supply chain resilience, creating opportunities for producers in stable regions and spurring new industrial policies.

- Threats: The primary threat is a prolonged period of stagflation, where high costs destroy industrial demand and lead to a cascading economic slowdown.

Copper Prices Fluctuate Amid Geopolitical Risk

As an introduction to a SWOT analysis on markets under stress, this section needs a scene-setting chart. Chart 4, showing ‘Copper Prices Fluctuate,’ uses a key bellwether metal to visually establish the theme of ‘Geopolitical Stress’ affecting the global metals market.

(Source: Investing.com)

Table: SWOT Analysis for Global Metals Markets

| SWOT Category | 2021 – 2024 (Pre-Conflict Baseline) | 2025 – 2026 (Conflict-Driven Shift) | What Changed / Validated |

|---|---|---|---|

| Strengths | Efficient, cost-optimized global supply chains. Low-cost energy in Gulf region supports competitive aluminum production. | Price volatility drives record profits for commodity traders. Precious metals act as effective safe-haven assets for investors. | The value of market liquidity and the safe-haven status of gold/silver were validated. Traders like those on the LME benefit from fractured markets, as noted by the Financial Times. |

| Weaknesses | High geographic concentration of production (e.g., Gulf aluminum). Known dependence on logistical chokepoints like the Strait of Hormuz. | Extreme vulnerability to energy price shocks. Lack of readily available and scalable alternative supply routes and production capacity. | Theoretical vulnerabilities became kinetic realities. Dependence on the Strait of Hormuz, which impacts 50% of seaborne sulfur, proved to be a critical failure point. |

| Opportunities | Further cost optimization through globalization. Accessing new, low-cost production centers. | Accelerated investment in supply chain resilience (near-shoring, friend-shoring). A “green premium” emerges for secure, low-risk supply. Rise of strategic industrial policy (e.g., EU Industrial Accelerator Act). | Governments are now actively intervening to secure supply chains, shifting the focus from pure market efficiency to national security. UNCTAD noted a sharp rise in trade measures in 2025. |

| Threats | Cyclical economic downturns. Standard trade disputes and tariffs. | Stagflation (high costs, low demand) becomes the primary macroeconomic risk. Cascading industrial shutdowns due to input cost/availability. Permanent demand destruction in some sectors. | The threat shifted from a cyclical to a structural one. Stagflationary risks, once hypothetical, were “stacking up” by April 2026, according to Reuters. |

Scenario Modelling: Prolonged Hormuz Disruption & Global Manufacturing

The single most critical variable for 2026–2027 is the duration and severity of disruption at the Strait of Hormuz, which will determine whether the current “super-squeeze” evolves into a full-blown global manufacturing crisis. The market is now balanced on a knife’s edge, with initial corporate responses indicating a trend toward passing on costs, a strategy that is unsustainable in the face of falling demand.

- If this happens: If significant disruptions to shipping through the Strait of Hormuz persist for another 6-12 months…

- Watch this: …watch for a wave of force majeure declarations from downstream manufacturers in the automotive, aerospace, and construction sectors, particularly in energy-poor regions like Europe. This would be followed by a sharp increase in industrial insolvencies and the likely implementation of export controls on domestically produced metals and other critical goods, even among allied nations seeking to protect their own industries.

- These could be happening: Early signals of this scenario are already present. The actions of India Inc. to shrink package sizes are a classic response to margin pressure. The cut to global steel demand forecasts is a forward-looking indicator of slowing activity. The EU’s proactive move with its Industrial Accelerator Act shows policymakers are already shifting to a defensive, protectionist footing. The market’s inability to properly price risk in adjacent markets, like rare earths, suggests a lack of preparedness for a wider systemic crisis.

Iran War Scenarios Show Tumbling Global GDP

The section topic is ‘Scenario Modelling’ and its impact on ‘Global Manufacturing.’ Chart 3, which presents ‘Iran War Scenarios’ and their effect on ‘Global GDP,’ is a direct visualization of the concepts discussed in the section heading.

(Source: bne IntelliNews)

The questions your competitors are already asking

This report covers one angle of the commercial impact of geopolitical conflict on industrial metals supply chains. The questions that matter most depend on your work.

- What is the status of the Foulath Holding/Bahrain Steel force majeure since the March 28, 2026 announcement?

- What is the outlook for aluminum physical premiums on the LME through 2026?

- Which industrial metals consumers are adopting security-focused procurement to counter logistical chokepoint risks?

- Which metals producers are gaining or losing ground as the Strait of Hormuz is repriced as a critical geopolitical risk?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.