Aramco DAC Strategy, 9 M Ton Linde CCS Hub, 12 Ton Siemens Pilot, and 2 Key Investments (2024 to 2025)

DAC Infrastructure Risk, Aramco Builds Storage Before Capture

Saudi Aramco’s strategy mitigates the primary adoption risk for Direct Air Capture (DAC) by prioritizing the development of large-scale carbon storage infrastructure before committing significant capital to expensive capture technology. This sequence de-risks future giga-scale DAC projects by ensuring sequestration capacity is established and operational ahead of need, a contrast to market approaches that build capture facilities while facing storage uncertainty.

- Between 2021 and 2024, the strategy focused on laying essential groundwork, culminating in the December 2024 agreement with Linde and SLB to build a 9 million metric ton per year CCUS hub in Jubail, which establishes a bankable offtake for captured CO₂.

- In 2025, the focus shifted to tangible technology testing with the March 2025 launch of a small-scale 12 ton per year DAC pilot in Dhahran, a low-risk R&D project designed to gather operational data and validate materials rather than achieve mass removal.

- This infrastructure-first approach validates a key dependency for the nascent DAC industry, providing a clear pathway for captured carbon and preventing the creation of stranded capture assets, with the Jubail hub targeting a 2027 operational start date.

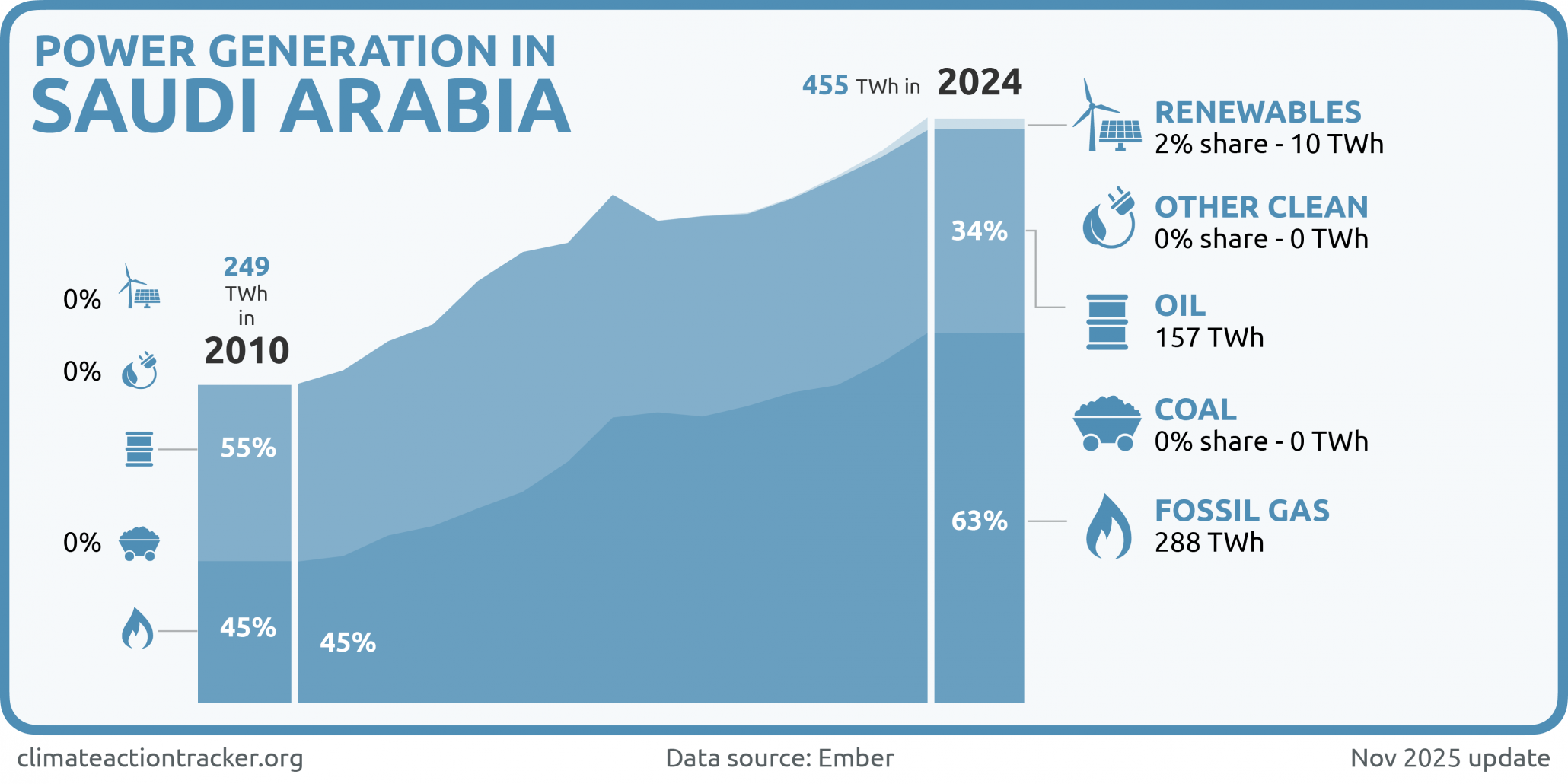

Saudi Power Generation Remains 97% Fossil Fuel-Based

This chart establishes the critical need for carbon management in Saudi Arabia by showing the power sector’s near-total reliance on fossil fuels. This provides the underlying motivation for Aramco’s entire carbon capture infrastructure strategy discussed in the section.

$Multi-Billion Jubail Project, Aramco’s Two-Pronged Investment

Saudi Aramco executes a dual investment strategy, committing multi-billions to mature, large-scale CCS infrastructure while placing smaller, strategic venture bets on next-generation, low-cost DAC technologies. This approach secures near-term infrastructure capacity with proven partners while simultaneously scouting for disruptive technologies that can solve the high-cost barrier of current DAC systems.

- The primary capital commitment is the multi-billion dollar Jubail CCS hub, a joint venture announced in December 2024, which creates a physical asset for CO₂ sequestration at a scale capable of supporting regional industrial decarbonization.

- Concurrently, through Aramco Ventures, the company made an investment in May 2024 in Spiritus, a US-based startup developing a novel DAC method targeting capture costs below $100 per ton.

- This dual approach addresses both ends of the commercialization spectrum, locking in capacity for today’s point-source capture technology while hedging against the high costs of current DAC systems, which range from $400 to $700 per ton.

Saudi Vision 2030 Energy Transition Framework

This chart places Aramco’s significant investment in the Jubail project within the broader national strategic context of Saudi Vision 2030’s energy transition goals, demonstrating alignment with top-level national priorities.

(Source: ScienceDirect.com)

Table: Saudi Aramco Strategic Carbon Management Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Jubail CCS Hub | Dec 4, 2024 | Multi-billion dollar joint venture with Linde and SLB to develop a CCS hub with a planned capacity of 9 million metric tons of CO₂ per year. The project creates essential storage infrastructure for future DAC deployment. | Carbon Herald |

| Spiritus (via Aramco Ventures) | May 22, 2024 | Strategic investment in a DAC startup to accelerate development of a passive capture technology targeting costs below $100/ton. The investment provides a stake in a potentially disruptive, low-cost technology pathway. | Carbon Capture Magazine |

Aramco 3 Key Partnerships for CCS and DAC (2024 to 2025)

Saudi Aramco’s partnerships in 2024 and 2025 reveal a deliberate strategy of collaborating with industrial giants for infrastructure scale and with technology specialists for research, development, and future innovation. This separates the risks of infrastructure execution from early-stage technology development.

- The most significant partnership is the December 2024 joint venture with Linde and SLB to build the Jubail CCS hub, leveraging their respective global leadership in industrial gases and subsurface technology for a world-scale infrastructure project.

- For its first DAC project, Aramco partnered with Siemens Energy to launch the Dhahran pilot in March 2025, accessing established engineering expertise to accelerate the R&D timeline and validate technology in a controlled environment.

- The partnership model extends to venture collaborations, such as the May 2024 agreement with Spiritus, which provides Aramco with direct access to early-stage, potentially cost-disruptive DAC technology without the overhead of internal development.

Saudi Arabia’s Historical Per Capita CO2 Emissions

The chart illustrates the scale and historical context of Saudi Arabia’s emissions challenge. This underscores the necessity for collaborative, partnership-based approaches to effectively address a problem of this magnitude, which is the focus of this section.

(Source: CarbonCredits.com)

Table: Saudi Aramco Carbon Capture Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Siemens Energy | Mar 20, 2025 | Technology collaboration for the development and launch of Saudi Arabia’s first DAC pilot test unit in Dhahran. The project serves as an R&D platform to test capture materials in the local climate. | Reuters |

| Linde & SLB | Dec 4, 2024 | Shareholders’ agreement to form a joint venture for the development of a major CCS hub in Jubail. This partnership builds the foundational infrastructure required for large-scale CO₂ sequestration. | Carbon Herald |

Saudi Arabia Focus, Aramco Builds Foundational DAC Infrastructure

Saudi Aramco’s carbon capture activities are geographically concentrated in Saudi Arabia, a strategy focused on building a domestic circular carbon economy and testing technologies under local climatic conditions before any potential international expansion. All major physical projects are located in the Kingdom’s Eastern Province, the center of its industrial operations.

- From 2024 to 2025, all major physical projects, including the planned Jubail CCS hub and the operational Dhahran DAC pilot, are located in Saudi Arabia, demonstrating a commitment to in-Kingdom value creation and alignment with Vision 2030.

- The Dhahran pilot’s specific objective is to validate capture materials in the Kingdom’s high-temperature, high-humidity climate, a critical step for developing bespoke regional solutions rather than relying on off-the-shelf technologies designed for different environments.

- While physical assets are domestic, venture investments like the one in US-based Spiritus show a global approach to technology scouting, with the clear intent of importing leading innovations back into the Kingdom to accelerate its national decarbonization goals.

DAC Technology Risk, Aramco Deploys Pilot to Validate Costs

Saudi Aramco acknowledges the commercial and technical immaturity of Direct Air Capture by initiating a small-scale pilot, a deliberate choice to de-risk the technology at the pilot and demonstration level (TRL 6-7) before committing to capital-intensive commercial plants. This confirms that the company views current DAC technology as not yet ready for at-scale deployment in its operating environment.

- Before 2025, Aramco’s carbon capture efforts were primarily focused on mature, point-source CCUS technology, for which front-end engineering and design (FEED) for its Accelerated Carbon Capture and Sequestration (ACCS) project was completed.

- The launch of the Dhahran DAC pilot in March 2025 marks a formal entry into the less mature DAC space, which is still in the demonstration phase globally, as evidenced by its high costs of $400-$700 per ton compared to $50-$250 per ton for point-source capture.

- The pilot’s focus on testing new sorbents and materials signals a strategic priority on R&D to drive down the cost curve, a necessary step before DAC can contribute meaningfully to the national goal of capturing 44 million tons of CO₂ annually by 2035, as outlined in the carbon capture and DAC leaders 2026 market analysis.

VC Investment in DAC Tech Normalizes After 2022 Peak

This chart highlights the perceived technology and market risk in DAC, as evidenced by normalizing VC investment. This data supports Aramco’s cautious strategy of deploying a pilot project to validate costs and de-risk its investment.

(Source: Global Corporate Venturing)

Aramco SWOT Analysis for DAC and CCS Strategy (2024 to 2025)

Saudi Aramco’s strength lies in its ability to fund and execute massive infrastructure projects, while its primary weakness remains the high cost and unproven scalability of DAC technology. The opportunity is to establish regional leadership in carbon management, but this is threatened by the slow pace of technological cost reduction and potential competition from more mature decarbonization pathways.

- Strengths are defined by access to massive capital and deep project management expertise, which enables the simultaneous development of multi-billion dollar infrastructure like the Jubail hub and a portfolio of venture technology bets.

- Weaknesses center on the high dependency on an economically challenging DAC technology, where current costs prevent immediate commercial scaling without significant subsidies or a breakthrough in capture efficiency.

- Opportunities include positioning the company as the dominant player in the Middle East’s emerging carbon management market and creating new value chains from a circular carbon economy aligned with Saudi Vision 2030.

- Threats arise from the risk that venture investments fail to achieve their low-cost targets or that internal R&D does not yield cost reductions fast enough, potentially delaying large-scale deployment past national targets.

Table: SWOT Analysis for Saudi Aramco’s Carbon Capture Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strength | Financial capacity to plan large projects. | Execution capability demonstrated by moving from agreement (Jubail Hub) to operational pilot (Dhahran). | The company validated its ability to execute on both large-scale JV agreements and smaller, technical R&D projects simultaneously. |

| Weakness | High theoretical cost of DAC technology was a known barrier. | The launch of a small 12-ton pilot confirms that current DAC technology is not commercially viable at scale for Aramco. | The company’s actions validated that the technology is still in an R&D and cost-reduction phase, not a deployment phase. |

| Opportunity | Ambition to meet national decarbonization goals (Net Zero by 2060). | Creation of tangible assets (Jubail hub, Dhahran pilot) that form the foundation of a new domestic carbon management industry. | The strategy shifted from ambition to the creation of foundational infrastructure, solidifying the opportunity to lead the regional market. |

| Threat | Risk of being outpaced by global DAC leaders developing lower-cost technologies. | The investment in Spiritus is a direct hedge against this threat, but performance of its own pilot remains a key uncertainty. | Aramco is now actively managing this threat through its venture arm, but the core risk of high costs and slow R&D progress remains. |

9 M Ton Hub by 2027, Aramco’s Next Move Hinges on Pilot Data

If the Dhahran DAC pilot validates a viable cost-reduction pathway for its proprietary sorbents within the next 18-24 months, watch for Saudi Aramco to announce a larger, pre-commercial DAC plant directly linked to the Jubail CCS hub. The performance data from this pilot is the single most critical gating factor for the company’s next investment decision in direct air capture.

- The critical signal to monitor is any announcement from Aramco or Siemens Energy regarding the performance, degradation, and operational costs of the sorbent materials being tested at the Dhahran pilot.

- Progress on the Jubail CCS hub, which is scheduled to be operational by 2027, will dictate the timeline for any large-scale DAC deployment, as available and affordable storage is the key enabler.

- Further venture investments by Aramco Ventures in carbon removal technologies will indicate which alternative technological pathways the company is considering to hedge against the risks of its current DAC approach and its dependency on a single pilot project’s outcome.

Carbon Removal Market to Exceed $3B by 2035

The chart provides the forward-looking market rationale for Aramco’s ambitious 9 M ton hub. It shows a significant future market for carbon removal that justifies the large-scale investment and strategic planning contingent on pilot data.

(Source: Precedence Research)

The questions your competitors are already asking

This report covers one angle of Saudi Aramco’s infrastructure-first DAC commercialization strategy. The questions that matter most depend on your work.

- Saudi Aramco activities in carbon management. Is the Siemens pilot a precursor to giga-scale DAC deployment?

- Aramco investments and funding. Is the 9 million ton Jubail CCUS hub on track for its 2027 operational target?

- What are the opportunities for DAC technology companies in the Aramco partnership ecosystem?

- What is the outlook for DAC deployment in Saudi Arabia by 2030, given Aramco’s infrastructure-first strategy?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.