Blue Hydrogen First: How Aramco’s 2026 Infrastructure Strategy Is Defining the Global Energy Trade

Saudi Aramco’s Hydrogen Projects: Building Commercial Scale Through Blue Ammonia

Saudi Aramco is prioritizing the rapid development of a large-scale blue ammonia export market to establish commercial viability and secure offtake agreements, deliberately deferring major capital allocation into its own green hydrogen production. This strategy focuses on leveraging existing assets and proven technologies to build the foundational infrastructure and supply chains for the future hydrogen economy. By establishing a dominant position in the low-carbon ammonia trade now, the company creates a market that can later incorporate green ammonia as costs decline.

- The period between 2021 and 2024 was defined by establishing the commercial blueprint, evidenced by the successful shipment of a 25, 000-tonne commercial blue ammonia cargo to South Korea in 2022 and the award of EPC contracts for the 1.2 MTPA Jafurah plant in 2023.

- The lack of new major project announcements after January 1, 2025, signals a strategic shift from planning to execution. The primary focus is now on delivering the Jafurah project, which is underpinned by the massive $110 billion development of its source gas field.

- This “blue-first” approach is validated by partnerships with key end-users, including Hyundai Heavy Industries and KNOC in South Korea. These alliances prioritize securing a reliable, large-scale supply of low-carbon fuel today rather than waiting for the uncertain timing of cost-competitive green hydrogen.

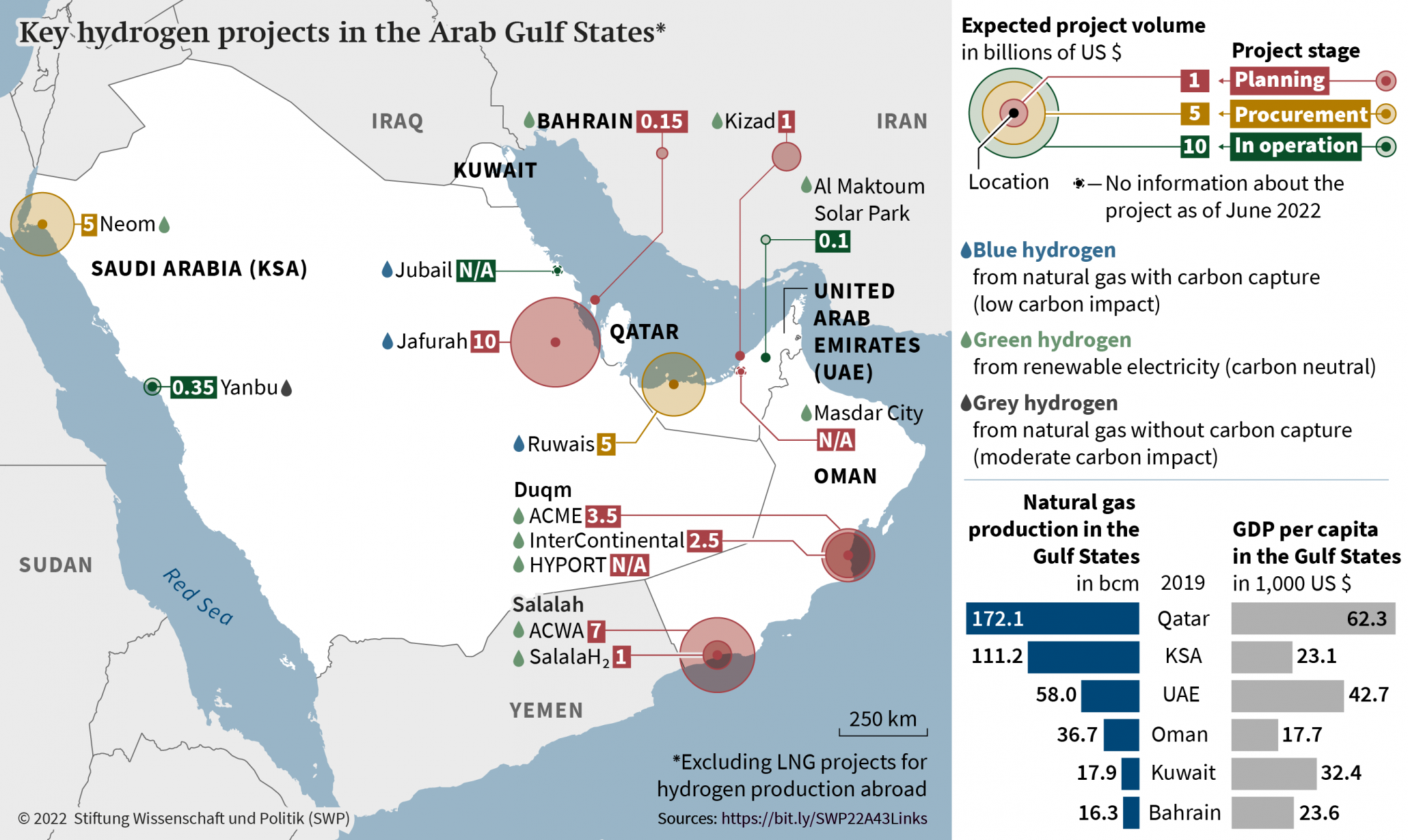

KSA’s Hydrogen Investments Mapped by Type

This map shows Saudi Arabia’s major investments in both blue ($10B) and green ($5B) hydrogen, visually supporting the section’s focus on Aramco’s blue ammonia strategy.

(Source: Stiftung Wissenschaft und Politik)

Capital Allocation Signals a Blue Hydrogen Bridge Strategy

Saudi Aramco’s investment strategy heavily favors leveraging existing hydrocarbon assets to create a blue hydrogen revenue stream, which contrasts sharply with the separate, large-scale greenfield investment in the NEOM green hydrogen project. This dual-track approach allows Saudi Arabia to dominate both near-term and long-term hydrogen markets. Aramco’s capital is directed toward de-risked projects with clear paths to commercial-scale production and profitability.

Hydrogen Is Core to Aramco’s Corporate Strategy

This infographic places hydrogen and ammonia as a key pillar in Aramco’s strategy, directly supporting the section’s analysis of the company’s capital allocation choices.

(Source: Oil & Gas News (OGN))

- The cornerstone investment is the $110 billion Jafurah unconventional gas field, a project designed to provide the low-cost feedstock essential for producing blue hydrogen and ammonia at a globally competitive target price of around $1.50 per kg.

- Aramco launched a $1.5 billion Sustainability Fund in October 2022 to invest in enabling technologies like carbon capture and storage (CCS). This is critical for validating the “blue” designation of its products and ensuring the economic viability of the entire strategy.

- While Aramco’s specific investment in the Jubail blue ammonia plant is pending a Final Investment Decision (FID), it is a core component of the larger Jafurah capital program. This stands in contrast to the $8.4 billion NEOM green hydrogen project, which is a distinct, venture-style investment led by a separate consortium of ACWA Power, Air Products, and NEOM.

Table: Key Hydrogen & Enabler Investments in Saudi Arabia

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| NEOM Green Hydrogen Co. (ACWA, Air Products, NEOM) | 2022 (FID Reached) | $8.4 Billion investment in a world-scale green hydrogen and ammonia facility. Aims to produce 1.2 MTPA of green ammonia starting in 2026, positioning Saudi Arabia as a leader in the future green hydrogen market. | NEOM |

| Saudi Aramco (Aramco Ventures) | Oct 2022 | Launch of a $1.5 Billion Sustainability Fund to invest in technologies supporting net-zero goals, with a key focus on hydrogen and CCS development to enable the blue hydrogen strategy. | Aramco |

| Saudi Aramco | Nov 2021 | $110 Billion total investment in the Jafurah unconventional gas field. This project serves as the foundational feedstock source for Aramco’s plan to produce up to 11 MTPA of blue ammonia by 2030. | Power Technology |

Strategic Alliances De-Risk Hydrogen Infrastructure and Secure Market Access

Aramco mitigates the significant market and execution risks associated with its capital-intensive hydrogen projects by constructing a robust network of international partnerships. These alliances span technology providers, world-class construction firms, and, most importantly, guaranteed offtakers in key target markets. This collaborative model spreads financial exposure and ensures that production capacity is matched with confirmed demand.

NEOM’s Green Hydrogen Value Chain Visualized

This diagram illustrates the end-to-end process for the NEOM Green Hydrogen Company, providing a perfect visual companion to the project’s details listed in the section’s table.

(Source: Inside Saudi)

- For project execution, Aramco contracted Linde Engineering and Samsung Engineering in May 2023 for the engineering, procurement, and construction (EPC) of the Jafurah blue ammonia plant, thereby securing proven technology and reliable delivery capabilities.

- To guarantee future revenue and project bankability, the company established a Memorandum of Understanding (Mo U) with major South Korean industrial players, including Hyundai H.I. Group and KNOC, to build a comprehensive supply chain and secure long-term buyers.

- Aramco is also investing downstream through a planned joint venture with automotive giants Geely and Renault. This move aims to support the development of synthetic fuels and next-generation hydrogen powertrain technologies, effectively creating future captive demand for its low-carbon fuel products.

Table: Aramco’s Hydrogen Partnership Ecosystem

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Linde Engineering & Samsung Engineering | May 2023 | Awarded EPC contracts for the 1.2 MTPA Jafurah blue ammonia plant. This secures the technical expertise needed to build the production and carbon capture facilities at industrial scale. | Reuters |

| Geely & Renault | Mar 2023 | Letter of intent for Aramco to become a minority stakeholder in a new powertrain company. The purpose is to develop synthetic fuels and hydrogen technologies, stimulating future demand. | Aramco |

| Hyundai H.I. Group & KNOC | Oct 2022 | Mo U to co-develop a complete blue hydrogen and ammonia supply chain from Saudi Arabia to South Korea. This de-risks the project by securing a major export market early. | Aramco |

| SABIC & Lotte Fine Chemical | Oct 2022 | Successful delivery of the world’s first certified, commercial-scale blue ammonia cargo (25, 000 tonnes) to South Korea, demonstrating the viability of the entire supply chain. | Aramco |

Saudi Arabia Establishes a Hydrogen Export Hub Targeting Asian Markets

Saudi Arabia is systematically constructing a production and export hub for low-carbon ammonia, with all major commercial activity and infrastructure development concentrated within the Kingdom. This strategy is aimed squarely at energy-importing nations in Asia that have established national decarbonization mandates. By creating a centralized, large-scale production base, the Kingdom can optimize costs and control a significant portion of the emerging global low-carbon fuel trade.

Saudi Arabia’s Hydrogen Export Roadmap to 2050

This timeline details the kingdom’s long-term hydrogen strategy, showing a clear phase for ‘Production and exportation’ that aligns with the ‘export hub’ concept discussed in the section.

(Source: ScienceDirect.com)

- Between 2021 and 2024, all significant project development, including the Jafurah Gas Field and the planned Jubail Blue Ammonia Plant, was geographically centered in Saudi Arabia’s Eastern Province to leverage existing industrial infrastructure and export terminals.

- The strategic focus on exports is demonstrated by commercial shipments and offtake agreements targeting South Korea and Japan. Concerns over Asia’s energy security and decarbonization goals make these nations reliable long-term customers for low-carbon ammonia.

- The absence of new international production project announcements from Aramco after January 1, 2025, reinforces this hub-and-spoke model. This approach solidifies Saudi Arabia’s role as the central production hub, strengthening its control over the nascent global supply chain for low-carbon fuels.

Blue Ammonia Moves to Commercial Scale While Green Hydrogen Remains in Development

Saudi Aramco’s strategy validates that blue ammonia production technology, which combines conventional processes with carbon capture, is ready for immediate commercial-scale deployment. This allows the company to enter the market years ahead of large-scale green hydrogen projects. While green hydrogen represents the ultimate zero-emission goal, its underlying technology ecosystem still requires further maturation and significant cost reduction to compete with blue alternatives at scale.

Green Hydrogen Projects Face Global Cancellations

The sharp increase in green hydrogen project cancellations globally provides strong evidence supporting the section’s point that the technology remains in development compared to commercial-ready blue ammonia.

(Source: Energy Connects)

- The period from 2021-2024 confirmed the technical readiness and commercial viability of the entire blue ammonia value chain. This was proven by the progression from a 40-tonne pilot shipment to Japan in 2020 to a full-scale 25, 000-tonne commercial cargo to South Korea in 2022.

- The award of EPC contracts to Linde Engineering and Samsung Engineering for the 1.2 MTPA Jubail plant demonstrates a definitive shift from pilot phase to industrial scale. This project relies on established steam methane reforming (SMR) and proven carbon capture technologies, minimizing technical risk, although the energy cost for carbon capture remains a key operational variable.

- In contrast, while the NEOM green hydrogen project aims for a 2026 start date, it represents a first-of-its-kind deployment of electrolysis technology at such a massive scale. Aramco’s blue hydrogen approach provides a faster and less technologically risky path to capturing market share.

SWOT Analysis: Saudi Aramco’s Blue Hydrogen Strategy

Aramco’s blue hydrogen strategy effectively leverages its immense strengths in low-cost feedstock and industrial project execution. However, it faces external threats from the accelerated maturation of green hydrogen technologies and the potential for shifting policy preferences in key import markets. The success of this strategy hinges on flawless execution of its large-scale carbon capture infrastructure.

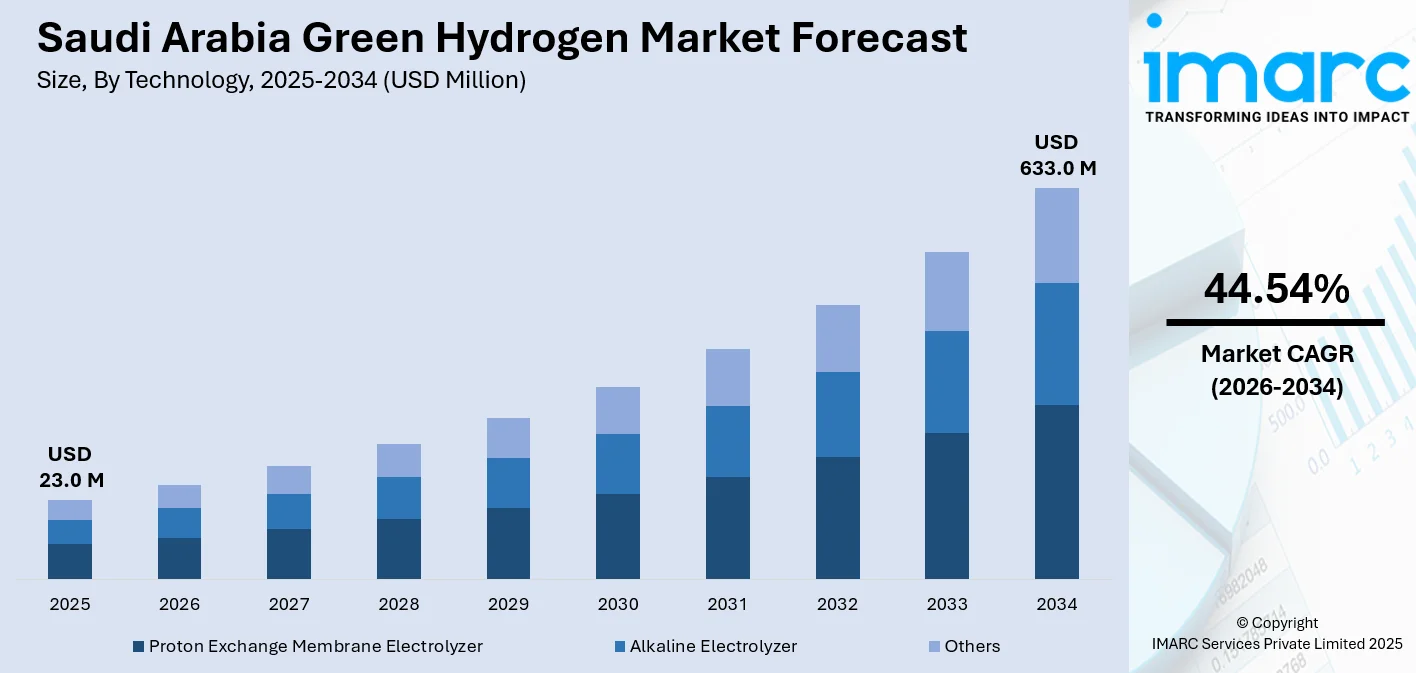

Green Hydrogen Market Growth Poses Future Threat

The forecast of massive growth in the green hydrogen market directly quantifies the competitive threat from maturing green technologies mentioned in the SWOT analysis summary.

(Source: IMARC Group)

Table: SWOT Analysis for Saudi Aramco’s Blue Hydrogen Initiative

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Access to vast, low-cost natural gas reserves from the Jafurah field. Deep institutional expertise in managing mega-projects. | Leveraging gas reserves to secure EPC partners (Linde, Samsung) for a world-scale ammonia plant. | The strategy was validated by translating feedstock advantage into concrete construction contracts, confirming the technical and commercial plan for large-scale production. |

| Weaknesses | The entire “low-carbon” value proposition was theoretical and dependent on unbuilt, large-scale carbon capture (CCS) infrastructure. | Focus on planning the 9 MTPA Jubail CCS hub. The project’s success is still a future dependency. | The dependency on CCS was not resolved but was defined as a concrete project. The risk shifted from a concept to a specific, albeit massive, execution challenge. |

| Opportunities | Potential to be a first-mover in the global low-carbon ammonia trade by leveraging proven SMR technology for faster deployment than green hydrogen. | Securing Mo Us with key Asian buyers (Hyundai, KNOC) and delivering a commercial-scale cargo to South Korea. | Market appetite was validated. The opportunity moved from a theoretical export plan to a proven commercial pathway with identified, high-potential customers. |

| Threats | Risk that green hydrogen costs would fall faster than expected, making blue hydrogen uncompetitive. Potential for policy shifts in import markets (e.g., EU) favoring green H 2. | The $8.4 B FID on the competing NEOM green hydrogen project confirmed a viable, large-scale green alternative will exist in-country by 2026. | The threat of green hydrogen competition was validated and localized. Aramco’s blue project now directly competes for resources and market attention with a major green project inside Saudi Arabia. |

2026 Outlook: Focus Shifts to Execution and Securing Offtake Agreements

The single most critical signal to watch for in the year ahead is the Final Investment Decision (FID) for the Jubail blue ammonia plant. This decision will be the definitive trigger for a cascade of construction activity and the formalization of offtake contracts, ultimately confirming the bankability of Saudi Arabia’s entire blue hydrogen export model. Its approval would signal that the market is ready to move from planning to building the global hydrogen economy.

Fossil Fuel Dominance Is Blue Hydrogen’s Strength

This chart’s depiction of a gas-dominated power mix visually confirms the primary ‘Strength’ listed in the SWOT table: access to vast, low-cost natural gas feedstock.

- If the Jubail Plant FID is announced, watch for the immediate formalization of binding, long-term offtake agreements with partners like KNOC and Hyundai, which would move these relationships beyond the initial Mo U stage and lock in revenue for decades.

- Monitor all progress reports related to the planned 9 million tonne per year CCS hub at Jubail. Any announced delays, cost overruns, or technical challenges in this parallel project present a direct and material risk to the blue ammonia strategy’s “low-carbon” credentials and timeline.

- The current lack of new major project announcements from Aramco itself suggests a period of intense internal focus on project delivery. Therefore, new market signals are more likely to emerge from its EPC and offtake partners, or from the parallel NEOM green hydrogen project, which is scheduled to begin production in 2026.

Frequently Asked Questions

What is Saudi Aramco’s primary hydrogen strategy?

Saudi Aramco is pursuing a “blue-first” strategy, prioritizing the rapid development of a large-scale blue ammonia export market. This approach leverages existing natural gas assets and proven technologies to build foundational infrastructure and secure commercial offtake agreements, establishing a dominant market position that can later incorporate green hydrogen as its cost declines.

How is Saudi Arabia involved in both blue and green hydrogen?

The country is using a dual-track approach. Saudi Aramco is leading the blue hydrogen initiative, centered on the $110 billion Jafurah gas field to produce blue ammonia. Separately, the $8.4 billion NEOM project, a joint venture between ACWA Power, Air Products, and NEOM, is developing a world-scale green hydrogen facility. This allows Saudi Arabia to lead in the near-term blue hydrogen market while simultaneously positioning itself for the future green hydrogen economy.

Why is the Jafurah gas field project so important to this strategy?

The $110 billion Jafurah unconventional gas field is the cornerstone of Aramco’s strategy. It is designed to provide the massive, low-cost natural gas feedstock required to produce blue hydrogen and ammonia at a globally competitive price. Without this feedstock source, the entire plan to produce up to 11 MTPA of blue ammonia by 2030 would not be economically viable.

Who are some of Aramco’s key international partners in its hydrogen plan?

Aramco has built a robust partnership ecosystem. For project execution, it awarded EPC contracts to Linde Engineering and Samsung Engineering. To secure market access and offtake, it has signed MOUs with major South Korean industrial players like Hyundai H.I. Group and KNOC. It is also partnering with automotive companies Geely and Renault to help create future demand for synthetic and hydrogen-based fuels.

What is the biggest risk to Aramco’s blue hydrogen strategy?

The single biggest risk is the dependency on the successful and timely execution of its large-scale carbon capture and storage (CCS) infrastructure. The entire “low-carbon” value proposition of blue hydrogen relies on capturing the CO2 generated during production. Any delays or failures in developing the planned 9 million tonne per year CCS hub at Jubail would directly threaten the project’s timeline, cost, and environmental credentials.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.