Natural Gas Permitting, EIA 111 Bcf/d Forecast, FERC’s $30 M Ceiling, and 2.5 Bcf/d AI Demand (2025-2026)

Pipeline Permitting Risks: US Natural Gas Faces 4-10 Year Delays

The primary constraint on the U.S. natural gas market’s ability to meet record demand is the protracted and uncertain process for permitting midstream infrastructure. Despite a clear federal push to accelerate approvals in 2025-2026, persistent state-level opposition and legal challenges create a critical timing mismatch between the rapid growth of demand from data centers and LNG exports and the 4-10 year timeline required to bring new pipeline capacity online.

- The 2021-2024 period was defined by significant project stalls, primarily from state-level opposition in the Northeast. New York’s repeated denial of water quality certificates for projects like the Constitution Pipeline highlighted the ability of individual states to block federally approved infrastructure, creating regional supply bottlenecks.

- A strategic shift occurred in 2025-2026 with federal actions designed to shorten timelines. The U.S. House passed a pipeline permitting bill in December 2025, and the Federal Energy Regulatory Commission (FERC) followed with a May 2026 proposal to overhaul its “blanket permitting” process, aiming to expedite construction.

- However, the impact of these reforms is not yet validated. Federal courts have established precedents demanding more rigorous environmental and market need analyses from FERC, a trend that continues to empower legal challenges from environmental groups and landowners, keeping project timelines elongated.

- This creates a structural risk where prolific production from the Appalachia and Haynesville basins could become constrained, unable to reach burgeoning demand centers. This could lead to significant regional price volatility and undercut the economic viability of upstream investments.

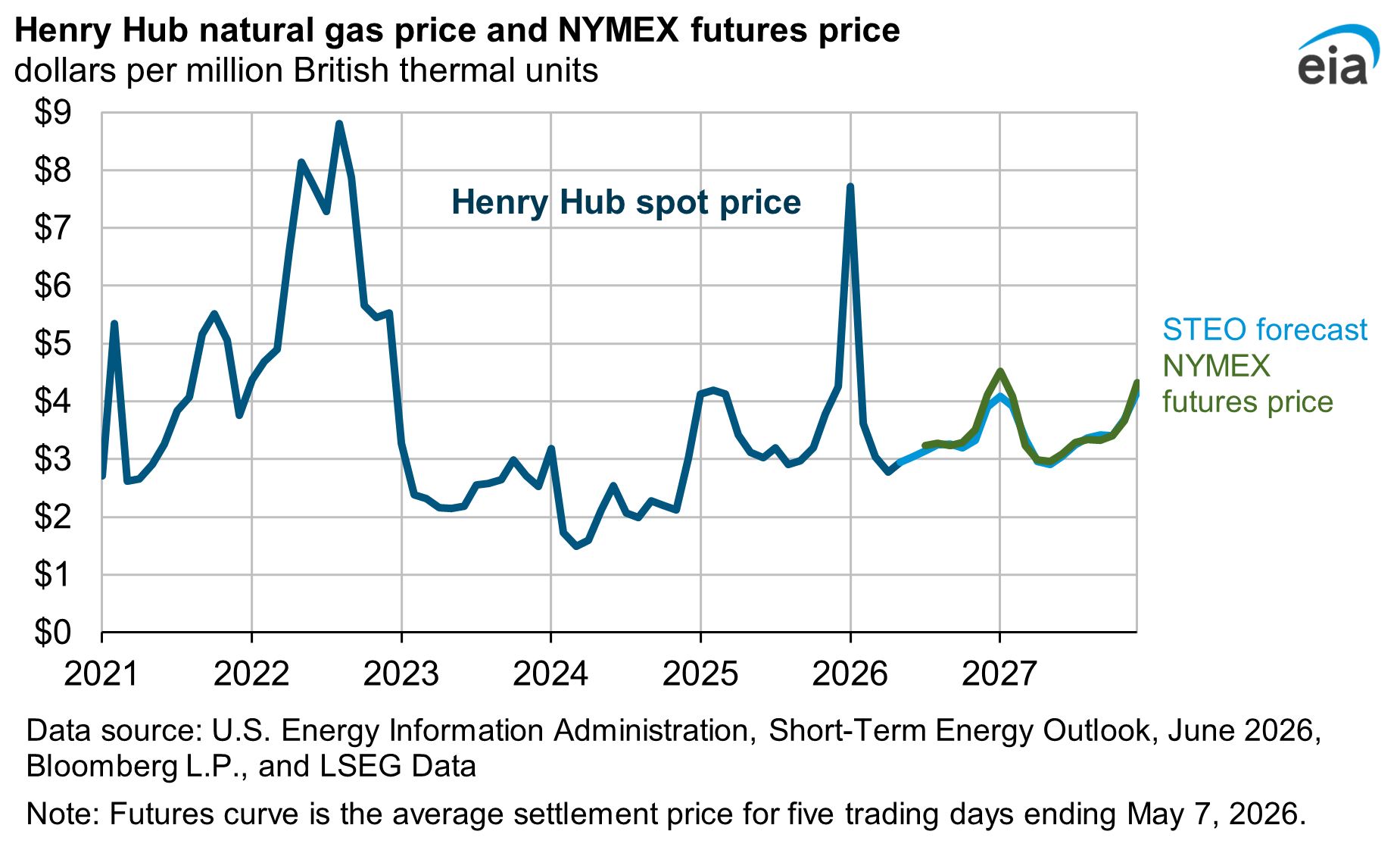

Natural Gas Prices Forecast to Rise Through 2027

This forecast for rising natural gas prices reflects the significant supply constraints expected from pipeline permitting delays of 4-10 years, creating a tighter market.

(Source: EIA)

$30 M FERC Authorization Signals Acceleration in US Natural Gas Pipeline Construction

Capital investment is flowing decisively into natural gas assets, driven by the clear, non-cyclical demand signal from the AI and data center boom. Corporate M&A and midstream capital expenditures are accelerating to secure gas supply for power generation, but the return on these investments is contingent on the successful and timely execution of the pipeline projects needed to move the gas from wellhead to consumer.

- M&A activity in the power sector confirmed this trend, with over 62 GW of natural gas generation assets transacted in 2025, a fourfold increase from the 15 GW transacted in 2024. This activity is directly linked to securing reliable power for new data center load.

- Leading midstream operators are committing capital to expand infrastructure. Enterprise Products Partners is increasing its Permian Basin natural gas processing capacity to 4.6 Bcf/d by 2026 to service growing production volumes.

- Regulatory changes are providing direct financial incentives for smaller projects. FERC’s May 2026 proposal to raise the automatic “blanket permit” cost ceiling for pipeline projects from $14.5 million to $30 million is designed to fast-track the smaller-scale expansions and modifications needed to debottleneck the existing grid.

US LNG Export Capacity to Surge Through 2030s

The acceleration of pipeline construction, signaled by recent FERC authorizations, is essential to service the massive build-out of US LNG export capacity projected in this chart.

(Source: Deloitte)

Table: US Natural Gas Strategic Investments and Regulatory Actions

| Entity / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| FERC | May 2026 | Proposed raising the automatic authorization ceiling for pipeline projects to $30 million. This action aims to accelerate construction of smaller-scale pipeline modifications and upgrades to ease system constraints. | Natural Gas Intelligence |

| Power Generation M&A | 2025 | Over 62 GW of natural gas-fired power generation assets were acquired, a 4 x increase from 2024. The activity was driven by the need to secure reliable power for the expanding data center sector. | Deloitte |

| Enterprise Products Partners | 2025-2026 | Announced expansion of its Permian Basin gas processing capacity to 4.6 Bcf/d by 2026. This investment is a direct response to rising associated gas production from the region. | Enterprise Products |

| U.S. House of Representatives | Dec 2025 | Passed a bill intended to streamline the federal permitting process for interstate natural gas pipelines, seeking to shorten review timelines and provide more regulatory certainty for project developers. | BIPC |

US Natural Gas Sees 2 Key Offtake Agreements for LNG Exports

Strategic offtake agreements for U.S. Liquefied Natural Gas (LNG) projects provide the long-term commercial certainty required to reach Final Investment Decisions (FIDs). These multi-billion-dollar commitments from international buyers validate the cost-competitiveness of U.S. gas but also intensify the pressure to resolve the domestic infrastructure bottlenecks that could threaten supply to these new terminals.

- In October 2025, Japanese utilities Tokyo Gas and JERA signed letters of intent for LNG offtake from a proposed Alaska LNG project. This move provides a crucial commercial foundation for the project’s financing and signals Asian market confidence in new U.S. supply sources.

- The expansion of LNG export capacity, projected to add 5 Bcf/d by 2026, solidifies the U.S. as a critical global energy supplier. Companies like Sempra and Cheniere are leading this buildout.

- These long-term international partnerships underscore the urgency of domestic policy. A failure to build the necessary pipelines to connect production from basins like the Permian and Haynesville to Gulf Coast export terminals would jeopardize the ability to fulfill these contracts.

- The financing for projects like Commonwealth LNG is directly tied to securing these binding offtake agreements, linking global demand directly to the success of U.S. infrastructure policy.

US LNG Demand Forecast to Surge Through 2030

The new offtake agreements are a direct corporate response to the surging global demand for US LNG, providing the financial certainty needed to meet this projected growth.

(Source: LinkedIn)

Northeast vs. Gulf Coast: A US Natural Gas Infrastructure Disconnect

A stark geographical divide defines the U.S. natural gas infrastructure landscape, with the Gulf Coast rapidly expanding to serve global markets while the Northeast remains a contested territory where demand growth is stifled by infrastructure opposition. This regional divergence creates significant market inefficiencies and highlights where the battle over the future of natural gas will be fought.

- The U.S. Northeast, a major demand center, remains the epicenter of pipeline opposition. Despite attempts in 2025 to revive projects like the Constitution Pipeline, state-level agencies continue to pose the most significant barrier to connecting abundant Appalachian supply with consumers.

- In contrast, the U.S. Gulf Coast has a more favorable development environment. Major pipeline projects like the Matterhorn Express are advancing to move gas from the Permian Basin to meet growing industrial, power, and LNG export demand in Texas and Louisiana.

- This disconnect means that while the EIA forecasts record national production, consumers in the Northeast can face high prices and supply constraints during peak demand periods, as the gas cannot physically reach them.

- The concentration of new data center development in states like Virginia and Ohio is creating new demand hubs, adding further pressure on the need for new pipeline capacity in the Mid-Atlantic and Midwest regions, away from the traditional Gulf Coast corridor.

Natural Gas Storage Dips Below 5-Year Average

This chart, showing storage dipping below the 5-year average, illustrates the kind of market volatility that arises from infrastructure disconnects between producing and consuming regions like the Gulf Coast and Northeast.

(Source: American Gas Association)

TRL 9 Production Tech: US Natural Gas Focus Shifts to Decarbonization

While the core technologies for extracting natural gas are fully mature at Technology Readiness Level 9 (TRL 9), the industry’s strategic imperative is shifting toward decarbonization. The long-term viability of natural gas as a “bridge fuel” depends on the commercial-scale deployment of technologies that can mitigate its carbon footprint, such as carbon capture and methane pyrolysis.

- The period between 2021-2024 was primarily focused on optimizing established technologies like horizontal drilling and hydraulic fracturing to improve production efficiency and lower breakeven costs in major shale plays.

- Starting around 2025, the industry conversation broadened significantly to include pathways for decarbonization. Methane pyrolysis, a technology that converts methane into hydrogen and solid carbon without CO 2 emissions, is emerging as a promising alternative to traditional steam methane reforming.

- Carbon Capture, Utilization, and Storage (CCUS) is a more near-term option. The cost of capture from concentrated streams in gas processing is relatively low ($15-25 per tonne), making it economically feasible today. However, capturing CO 2 from dilute flue gas at power plants, which use turbines from companies like GE Vernova and Siemens, remains more expensive and has not been deployed at a scale sufficient to decarbonize the power sector. Leading producers like BP are investing in large-scale CCUS projects.

- The critical technology gap is not in producing natural gas, but in producing it and using it at scale with a near-zero carbon footprint. The success of these emerging decarbonization technologies will determine the role of gas beyond 2030.

US Natural Gas Price Forecasts to 2027

The forecast for sustained higher prices provides the economic incentive for producers to invest in advanced TRL 9 production technologies, including those focused on decarbonization, to meet market and regulatory demands.

(Source: Natural Gas Intelligence)

SWOT Analysis: US Natural Gas Strengths and Permitting Threats

The U.S. natural gas market is positioned for significant growth, underpinned by a massive low-cost resource base and new, structural demand from the digital economy. However, this strength is directly counteracted by the persistent threat of infrastructure permitting delays, which could strand supply and cede market share to competing energy sources.

Planned Gas Capacity Shows Huge On-Site Power Demand

This chart illustrates a key ‘Opportunity’ within the SWOT analysis, as the significant and growing demand for natural gas in power generation represents a core strength for the market.

(Source: RBC Capital Markets)

Table: SWOT Analysis for US Natural Gas Market (2025-2026)

| SWOT Category | Analysis (2025-2026 Data) | Supporting Evidence / Source |

|---|---|---|

| Strengths | Record production levels, globally competitive pricing, and new, non-cyclical demand from AI data centers provide a strong foundation for growth. | EIA forecasts production at 111 Bcf/d in 2026; Henry Hub prices are competitive vs. global benchmarks; Data centers to add 2.5 Bcf/d of demand. (investing.com) |

| Weaknesses | Extreme dependence on new pipeline infrastructure, which faces significant political and legal opposition, creating a high risk of project delays and cancellations. | Permitting timelines average 4-10 years; states like New York have historically blocked federally approved pipelines. (APGA) |

| Opportunities | Massive expansion of LNG export capacity to serve global markets, displacement of remaining coal-fired power generation, and growth as the primary fuel for reliable data center power. | LNG export capacity is forecast to increase by 5 Bcf/d by 2026; Over 40% of data center power is met by natural gas. (Earth Rights International) |

| Threats | Protracted permitting timelines creating a mismatch with demand growth, rising ESG pressure on investors leading to financing headwinds, and long-term competition from accelerating renewable energy deployment. | Investor and lender scrutiny of fossil fuel projects is increasing; FERC’s environmental reviews face growing legal challenges. (NRDC) |

Bull vs. Bear Scenario: The US Natural Gas Infrastructure Race

The forward trajectory of the U.S. natural gas market will be decided by a race between exponential demand growth and the on-the-ground reality of building infrastructure. The single most critical factor to monitor is whether federal permitting reforms can translate into meaningfully shorter approval timelines for the interstate pipelines needed to connect supply with demand.

- If FERC’s May 2026 permitting reforms demonstrably reduce approval timelines for new pipeline applications over the next 12-18 months, then watch for an acceleration of Final Investment Decisions on key midstream projects aimed at debottlenecking the Permian and Haynesville basins.

- If state-level opposition and legal challenges continue to stall major projects in the Northeast and Mid-Atlantic despite federal streamlining efforts, then watch for sustained regional price disparities, potential shut-ins of Appalachian production, and a slowdown in data center development in constrained regions.

- The key signal to monitor is the progress of bellwether projects, including the revived efforts for the Constitution Pipeline in New York and new pipeline proposals designed to serve the massive data center alley in Virginia. Their success or failure will serve as a direct indicator of whether infrastructure can keep pace with demand.

US Natural Gas Storage Forecast to Remain Healthy

This chart’s projection of healthy storage levels represents the ‘Bull’ scenario outcome in the infrastructure race, where pipeline construction successfully keeps pace with demand to ensure market stability.

(Source: EIA)

The questions your competitors are already asking

This report covers one angle of the midstream infrastructure constraints facing the U.S. natural gas market. The questions that matter most depend on your work.

- What is actually happening with FERC’s May 2026 blanket permitting reform since the announcement?

- What is the outlook for new natural gas pipeline capacity to serve AI data center demand by 2026?

- Which data center operators are adopting natural gas to power their AI workloads?

- What are the opportunities for midstream developers in the Haynesville and Appalachia basins given the permitting risks?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.