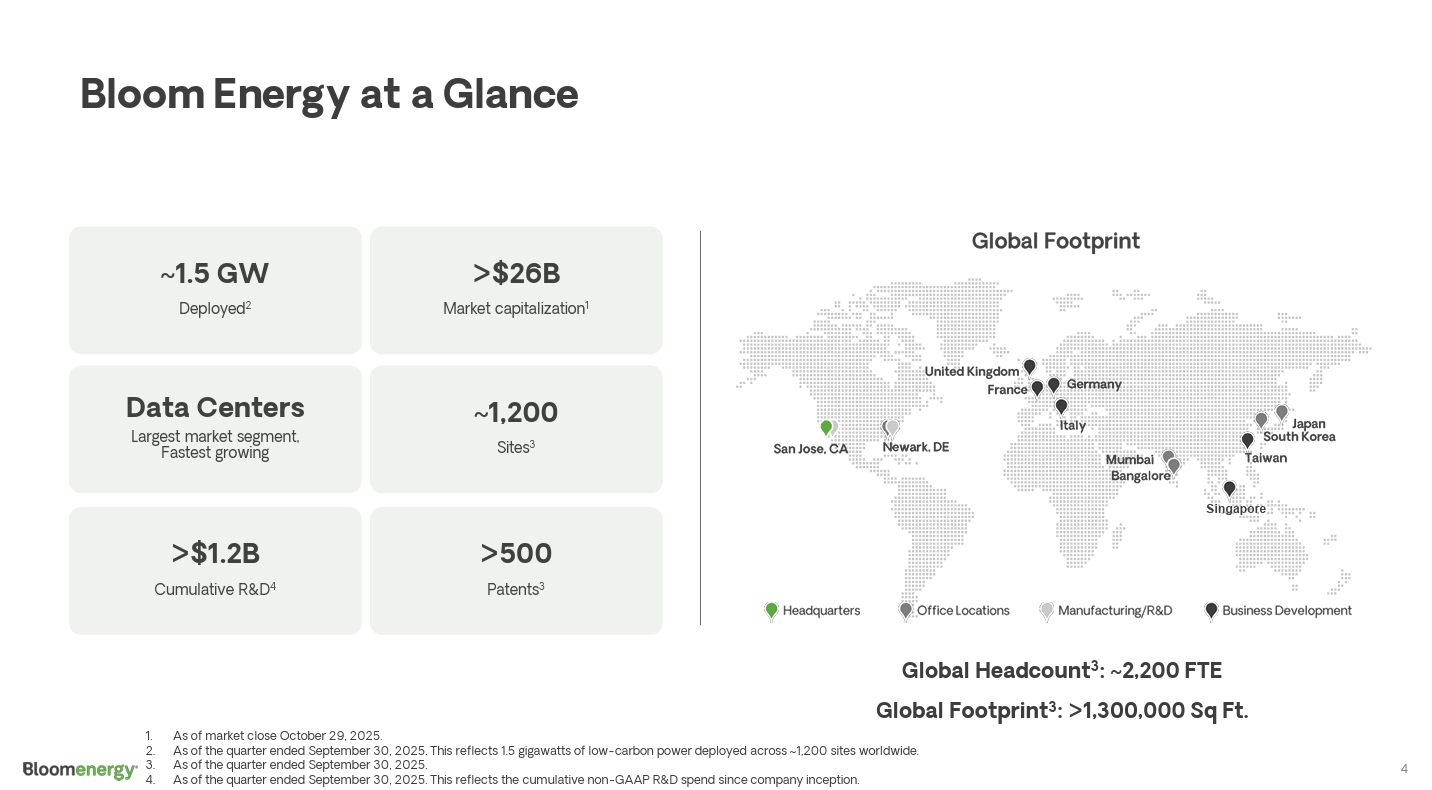

Bloom Energy SOFC Expansion, $2.65 B AEP Offtake, 2.8 GW Oracle Deal, and Major Commercial Agreements (2021-2026)

SOFC Data Center Adoption, Bloom Energy 2.8 GW Oracle Deal

The convergence of artificial intelligence power requirements and systemic grid limitations has elevated Solid Oxide Fuel Cell (SOFC) technology from a niche application to a critical infrastructure component for data centers. Before 2025, SOFC deployments were varied and smaller in scale, but the period since has been defined by multi-gigawatt orders from hyperscale and utility customers who cannot afford multi-year grid upgrade delays.

- From 2021 to 2024, Bloom Energy‘s projects were characterized by smaller, incremental deployments for a diverse customer base, including industrial and commercial facilities, demonstrating the technology’s reliability and efficiency in various settings.

- The strategic inflection point occurred in 2025-2026, driven by the AI boom, with data centers facing a projected 5-7 GW annual power deficit through 2030. This triggered a fundamental shift, with companies like Oracle and American Electric Power (AEP) securing multi-gigawatt agreements for on-site SOFC power.

- Within a 90-day period in early 2026, Bloom Energy and its competitors secured an estimated $7.65 billion in fuel cell deals specifically for data centers, confirming that SOFCs are now a primary solution for bypassing grid interconnection queues.

- This adoption is underpinned by the technology’s rapid deployment time, high electrical efficiency exceeding 60% on hydrogen, and its fuel flexibility, which provides a clear pathway from natural gas to hydrogen.

Bloom Energy Highlights Data Center Segment Growth

This chart directly illustrates the ‘SOFC Data Center Adoption’ mentioned in the section heading by showing the significant growth in Bloom Energy’s data center segment, a trend largely driven by major deals like the 2.8 GW Oracle agreement.

(Source: Arya’s Substack)

$100 M Factory Expansion, Bloom Energy SOFC Manufacturing Investment

Capital investment has decisively shifted from funding research and development to financing the scaled manufacturing capacity required to meet a validated, multi-billion-dollar order backlog. This strategic pivot reflects the market’s transition from technology validation to supply chain execution, with access to manufacturing capacity becoming the primary constraint on growth.

- Bloom Energy committed approximately $100 million to double its annual manufacturing capacity from 1 GW to 2 GW at its Fremont, California, facility, with a targeted completion by the end of 2026. This investment is a direct response to its substantial order book from data center and utility clients.

- To support this operational scale-up, the company initiated a $2.2 billion capital raise in early 2026. This funding is allocated to finance the factory expansion and provide the working capital necessary to execute its large-scale projects.

- Government support, including a recommendation from the Senate Committee for $30 million in the FY 2026 budget for the solid oxide fuel cell program, provides additional tailwinds for R&D and domestic manufacturing. The U.S. Inflation Reduction Act’s 30% Investment Tax Credit further improves project economics for customers.

Bloom Energy Revenue Surges Past $750M Quarterly

The chart’s depiction of a quarterly revenue surge provides the direct business context for the ‘$100 M Factory Expansion,’ as this investment is necessary to scale manufacturing capacity to meet the rapidly increasing demand shown by the revenue figures.

(Source: TradingKey)

Table: Bloom Energy Strategic Capital Investments

| Project / Investment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Manufacturing Capacity Expansion | 2025 – 2026 | A $100 million investment to expand the Fremont, CA, factory’s annual production capacity from 1 GW to 2 GW. This is essential to fulfill delivery schedules for multi-gigawatt orders from partners like Oracle and AEP. | Seeking Alpha |

| Corporate Capital Raise | 2026 | A $2.2 billion capital raise to finance the manufacturing scale-up and ensure sufficient working capital to manage a rapidly growing pipeline of large-scale projects driven by data center power demand. | AInvest |

| U.S. DOE SOFC Program Funding | 2025 | The Senate Appropriations Committee recommended no less than $30 million for the solid oxide fuel cell program in the FY 2026 budget, signaling continued federal support for the technology’s development and deployment. | Carbon Capture Coalition |

Data Center Capex Dwarfs Historical Megaprojects

This chart provides the macro-economic justification for the ‘Strategic Capital Investments’ detailed in the section’s table. It shows that the data center market is an unprecedented megaproject, justifying the scale of capital being invested by Bloom and its partners.

(Source: Yahoo Finance)

Bloom Energy 1 GW AEP Agreement, Key Data Center Partnerships (2024 to 2026)

Strategic partnerships have evolved from pilot-scale demonstrations to multi-billion-dollar, long-term offtake agreements, providing significant revenue visibility and de-risking capital-intensive manufacturing expansion. These alliances with utility and technology leaders validate SOFC technology as a mainstream component of energy infrastructure for mission-critical operations.

- The partnership model shifted decisively between late 2024 and early 2026. An initial supply agreement option with AEP for up to 1 GW of Bloom Energy fuel cells in November 2024 was converted into a definitive 20-year offtake agreement valued at $2.65 billion just two months later.

- Hyperscale data center operators have become anchor customers. In April 2026, Bloom Energy expanded its agreement with Oracle to deploy up to 2.8 GW of its systems, establishing a clear framework for powering global AI and cloud infrastructure.

- The scale of these partnerships is unprecedented in the fuel cell industry, including a separate agreement with another major cloud provider for up to 2.45 GW of capacity, making Bloom its sole on-site power solution.

Fuel Cells Scale to 1GW Faster Than Other Power Tech

The chart provides a compelling technical rationale for the ‘Bloom Energy 1 GW AEP Agreement’ by demonstrating that fuel cells are the fastest technology to scale to the 1 GW level, directly aligning with the size and strategic importance of the deal discussed in the section.

(Source: OutspokenGeek – Substack)

Table: Bloom Energy Major Commercial Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Oracle | April 2026 | Expanded an existing partnership to deploy up to 2.8 GW of SOFC systems, providing clean and reliable power for Oracle‘s rapidly growing global AI and cloud data center infrastructure. | MLQ.ai |

| American Electric Power (AEP) | January 2026 | An unregulated AEP subsidiary executed a 20-year offtake agreement valued at $2.65 billion to supply power to data centers, converting a portion of a previously secured 1 GW supply option into a firm contract. | Yahoo Finance |

| Taiwanese Data Center Operators | November 2024 | Collaboration with partners in Taiwan to provide on-site SOFC power solutions to accelerate AI data center development, addressing the region’s critical power supply challenges and grid constraints. | Digitimes |

| FPM Development | November 2024 | A 20 MW utility deal to rapidly install SOFC systems to fortify grid resilience in California, showcasing the technology’s ability to quickly add capacity for grid stability. | Bloom Energy Investor Relations |

Sentiment Spikes Amid Major Bloom Energy Deals

This chart visually complements the section’s ‘Table: Bloom Energy Major Commercial Partnerships’ by showing the positive market and public reaction to these major deals, quantifying their impact on brand and investor sentiment.

(Source: LinkedIn)

US vs Asia, Bloom Energy Geographic Focus for SOFC Deployment

The geographic focus of SOFC deployment has consolidated around major U.S. data center markets, representing a strategic shift from the more diversified international presence seen in prior years. While early market development was strong in Asia, the recent surge in AI-driven power demand has made the U.S. the undisputed center of gravity for large-scale SOFC projects.

- Between 2021 and 2024, South Korea and Taiwan were key growth markets, driven by government incentives and industrial energy needs. Bloom Energy established a significant presence, including an 80 MW installation with its partner SK ecoplant, the world’s largest at the time.

- Starting in late 2024 and accelerating through 2026, the focus pivoted sharply to the United States. The primary driver is the extreme power demand from AI data centers concentrated in utility territories unable to meet new load requirements, such as those served by AEP.

- California remains a critical market, not just for data centers but also for grid resilience. The 20 MW deal with FPM Development highlights the use of SOFCs as a rapid-deployment solution to fortify an aging and strained grid infrastructure.

- Manufacturing remains centered in the U.S. at facilities in Fremont, California, and Newark, Delaware. This domestic production base is a key advantage for serving U.S. customers and benefiting from federal incentives like the IRA.

US Data Center Energy Use to Surge

The chart directly supports the section’s topic of ‘Bloom Energy Geographic Focus’ by illustrating the surging energy demand in the U.S. data center market, explaining why the U.S. is a primary target for SOFC deployment.

(Source: Vested Finance)

SOFC Commercial Scale, Bloom Energy >60% Efficiency Validation

Solid Oxide Fuel Cell technology has achieved full commercial maturity, a status validated by its adoption for mission-critical, gigawatt-scale power infrastructure by the world’s largest technology companies. The period from 2025 onward is defined not by questions of technical viability but by the technology’s proven ability to outperform traditional power generation on key metrics like efficiency, deployment speed, and fuel flexibility.

- The technology sits at a Technology Readiness Level (TRL) of 7 to 9, signifying it is commercially available and operationally proven. Over 1.5 GW of Bloom Energy’s SOFC systems have been deployed globally.

- In 2024, Bloom Energy achieved a landmark 60% electrical efficiency while running on hydrogen, a performance level that rivals large-scale combined-cycle gas turbines but in a modular, rapidly deployable format.

- While earlier deployments in the 2021-2024 period proved the technology’s reliability in commercial and industrial settings, the multi-gigawatt agreements with Oracle and AEP in 2026 serve as the ultimate validation of its capacity to function as a utility-scale power source.

- The platform’s fuel flexibility, enabling operation on natural gas today with a seamless transition to green hydrogen, is a critical feature that provides customers a credible and practical decarbonization pathway without requiring infrastructure replacement.

Bloom Energy Revenue Climbs to $2.45B

This chart demonstrates the financial success resulting from the technical achievements described in the section. Achieving ‘>60% Efficiency’ and ‘Commercial Scale’ are the enablers for the significant revenue growth to $2.45 billion shown in the chart.

(Source: AOL.com)

Strengths vs. Execution Risks, Bloom Energy SOFC SWOT Analysis

Bloom Energy’s strategic position has solidified around its ability to provide a rapid, scalable power solution to the AI industry, shifting its primary challenge from proving market demand to executing a massive industrial scale-up. The company’s future success now depends on its operational capacity to deliver on its multi-billion-dollar backlog.

Bloom Energy Earnings Surge on AI Data Center Pivot

This chart directly illustrates a key ‘Strength’ for the ‘SWOT Analysis’ in the section. The earnings surge shown is a tangible result of the successful strategic pivot to the AI data center market, a core positive point for the company.

(Source: Yahoo Finance)

Table: SWOT Analysis for Bloom Energy SOFC Expansion

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Proven SOFC technology, high efficiency, strong intellectual property portfolio with over 500 patents, and established manufacturing base in Delaware. | Validated at multi-gigawatt scale by hyperscalers (Oracle) and utilities (AEP). Achieved >60% electrical efficiency. Beneficiary of IRA tax credits. | The technology’s value proposition was validated as a mission-critical solution for the AI power crisis, moving it from a “clean energy alternative” to essential infrastructure. |

| Weaknesses | High capital expenditure compared to alternatives, reliance on natural gas for most deployments, and limited manufacturing scale for massive projects. | Operational execution risk for the 2 GW capacity expansion becomes the primary vulnerability. Managing a complex global supply chain for materials like scandium at scale. | The core challenge pivoted from market creation to industrial-scale manufacturing and project delivery. The weakness is no longer demand, but the ability to supply. |

| Opportunities | Grid constraints, corporate decarbonization goals, and growth in the hydrogen economy. The data center market was a growing segment. | The explosive, non-discretionary power demand from AI has created a massive, urgent market. Grid-level power bottlenecks are now measured in years, making on-site power essential. | The AI boom transformed the data center market from a significant opportunity into the central driver of the company’s growth, orders of magnitude larger than previously forecast. |

| Threats | Competition from other fuel cell technologies (PEM, MCFC), volatility in natural gas prices, and potential shifts in government subsidy policies. | Competitors like Ceres Power are also scaling with partners like Doosan. Delays in the 2 GW factory expansion could lead to loss of market share and customer confidence. | The competitive threat is now centered on which company can manufacture and deploy at gigawatt-scale fastest. Bloom’s large backlog provides a moat, but only if it can be delivered. |

Big Tech AI Capex Projected to Skyrocket

This chart highlights the primary ‘Opportunity’ that would be detailed in the ‘Table: SWOT Analysis for Bloom Energy SOFC Expansion.’ The skyrocketing capex from Big Tech on AI represents the massive addressable market driving Bloom’s expansion strategy.

(Source: MSN)

2026 Scenario, Bloom Energy 2 GW Capacity Execution

The single most critical factor for Bloom Energy‘s success in the coming year is its ability to execute the expansion of its Fremont factory to 2 GW of annual production capacity. Meeting this milestone on schedule and on budget is the necessary condition for realizing the value of its historic order backlog.

- If the factory expansion progresses on schedule toward a late-2026 completion, watch for announcements of initial production runs from the new lines and updates on supply chain readiness for the increased volume. This would signal that the company is on track to meet its Oracle and AEP delivery timelines.

- With the new capacity coming online, the key metric to monitor will shift to project deployment velocity. Watch the rate at which megawatts are installed and commissioned at customer sites through 2027 and 2028, as this will test the company’s logistics and service infrastructure at an unprecedented scale.

- A parallel development to watch is the sourcing of fuel for these large-scale deployments. Any significant pilot or commitment to blend green hydrogen into the fuel mix for a major data center project would represent a major step toward the company’s long-term decarbonization promise and unlock further value from policies like the hydrogen production tax credit.