Data Center Regulation Shifts, 2 States Block Cost Pass-Through, 267% Rate Hikes in Hotspots (2021 to 2026)

Data Center Cost Allocation, 22 States Propose Ratepayer Protections

State-level policy is undergoing a decisive shift from an incentive-driven model to a cost-containment model to protect residential ratepayers from the financial impact of explosive data center power demand. This pivot is a direct response to forecasts of demand nearly tripling and instances of electricity prices surging in data center hotspots, fundamentally altering the risk calculus for developers and utilities.

- Between 2021 and 2024, states like Tennessee and Florida primarily used tax incentives to attract data center investment. Tennessee’s SB 2583 (2024) and Florida’s existing sales tax exemptions on equipment and electricity encouraged development but lacked explicit prohibitions on passing grid infrastructure costs to residential customers.

- From 2025 to 2026, a direct legislative pivot occurred with Florida enacting SB 484 in May 2026 and Tennessee passing SB 1682/HB 2061 in June 2026. Both laws explicitly prohibit utilities from recovering the costs of new electrical infrastructure required for data centers from their other retail customers.

- This regulatory shift was driven by the economic reality in data center hubs, where some regions experienced residential electricity price hikes of up to 267%. This created intense political pressure for intervention to ensure energy affordability, especially as 1 in 6 U.S. households was behind on energy bills in 2025.

- The trend is expanding nationally. A bill to protect ratepayers passed the Pennsylvania House in March 2026, and Illinois proposed its “POWER Act” in February 2026, indicating a broad movement toward direct cost allocation for large-load customers.

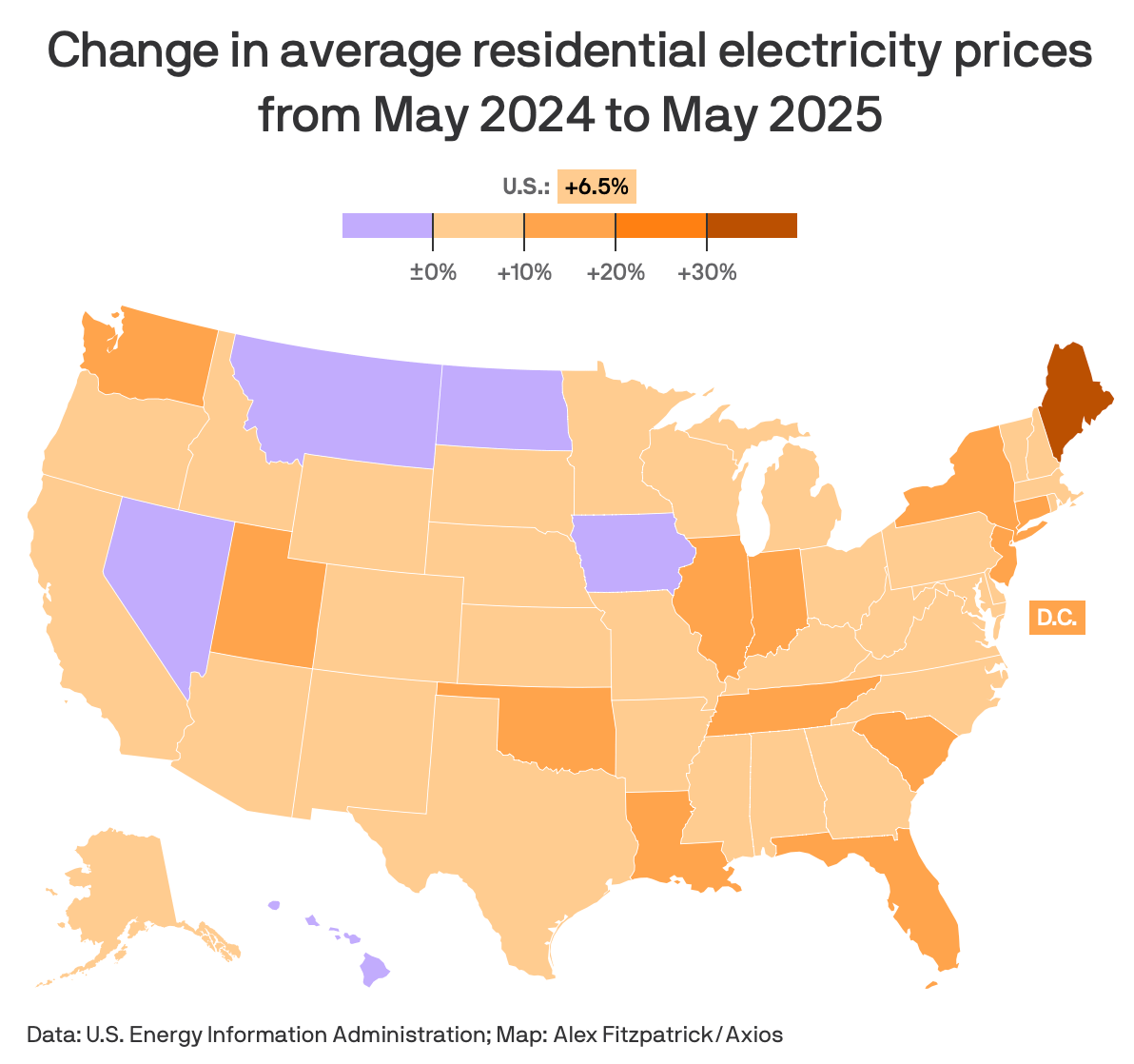

US Residential Electricity Prices Jump 6.5%

This section discusses the need for ‘Ratepayer Protections.’ The chart, showing that residential electricity prices are already increasing, provides the essential context and urgency for why such protections are being proposed to shield consumers from further costs driven by data centers.

(Source: Slow Boring)

$60 B in Rate Hikes, Utility Investment Risk in Data Center Hotspots

The new regulations in Florida and Tennessee directly reallocate billions in future infrastructure costs from residential ratepayers to data center operators, altering project financial models and introducing significant investment risk for both developers and utilities. This forces a strategic recalculation of capital expenditure, project returns, and cost recovery mechanisms in a sector where utilities sought over $60 billion in rate increases nationwide in 2025.

- Data center operators in these states now face increased Capital Expenditure (Cap Ex) as they must finance or directly pay for transmission lines and substations. This directly reduces project Internal Rate of Return (IRR) and lengthens payback periods, making site selection more sensitive to regulatory policy.

- Utilities now face the risk of Stranded Assets. If a utility builds infrastructure for a data center that is later canceled or delayed, these laws prevent them from socializing the unrecovered costs across the general rate base, placing the financial burden on the utility itself.

- This policy shift creates a significant opportunity for providers of onsite power and energy efficiency solutions. With over one-third of data centers expected to use 100% onsite power by 2030, the new cost burden on grid connections directly improves the Return on Investment (ROI) for behind-the-meter generation and advanced cooling technologies.

- Major hyperscalers are showing a willingness to adapt to this new model. Microsoft’s proactive commitment to “pay its way” for electricity costs signals a potential industry-wide acceptance, which could mitigate the risk of investment flight from states with stricter regulations.

Florida and Tennessee vs. Virginia, A Divergence in Data Center Policy

A clear policy divergence is emerging between states like Florida and Tennessee that are mandating direct cost responsibility for data centers and states like Virginia, which historically socialized these costs, creating a new and complex competitive dynamic for site selection. This regulatory fragmentation forces developers to weigh the benefits of lower upfront costs in some states against the long-term stability offered by explicit ’causer-pays’ frameworks in others.

- Between 2021 and 2024, Virginia solidified its position as the world’s largest data center market, partly because utilities like Dominion Energy could recover grid upgrade costs from the general body of ratepayers. This model lowered the initial financial hurdles for developers, accelerating growth.

- In 2025 and 2026, Florida (SB 484) and Tennessee (SB 1682) enacted laws to explicitly block this cost-socialization model. These policies require data centers to bear the “full cost of their service, ” including all associated electrical infrastructure upgrades.

- This creates a potential capital flight risk from Florida and Tennessee toward states that still offer more lenient cost-recovery models. However, it also offers a “first-mover” advantage by establishing regulatory certainty and mitigating public opposition to rate hikes, which could prove more valuable long-term if the model is adopted nationally.

- Other states are already following the Florida/Tennessee model. A Pennsylvania bill passed the House in March 2026, and an Illinois “POWER Act” was proposed in February 2026, demonstrating that this is becoming a key policy battleground influencing future data center investments.

Map Shows High Concentration of Tennessee Data Centers

The section focuses on a geographic comparison of policy between states, including Tennessee. A map showing the high concentration of data centers in Tennessee is the most relevant visual aid, directly illustrating the scale of the issue in one of the key states mentioned.

(Source: WEKU)

Data Center Tariffs, 2 States Validate ‘Causer-Pays’ Model (2025 to 2026)

The regulatory technology for managing data center load is rapidly maturing from broad tax incentives to sophisticated, targeted cost-allocation mechanisms, including specialized tariffs and direct infrastructure cost assignments. This evolution marks a transition from simple investment attraction to sustainable, long-term management of a new class of high-density industrial electricity consumers.

- During the 2021-2024 period, the primary regulatory tool was the provision of broad sales and use tax exemptions, as codified in Tennessee’s SB 2583. While effective at attracting investment, this approach did not directly solve the underlying problem of allocating grid upgrade costs.

- The 2025-2026 period saw a definitive shift to direct legislative intervention. Florida’s SB 484 now directs the Public Service Commission to establish rules for “full cost of service, ” while Tennessee’s SB 1682 mandates full infrastructure payment and detailed electricity usage reporting to the Public Utilities Commission.

- This progression signals a move from pilot-phase incentive programs to commercially scaled regulatory frameworks. The new laws are designed to handle the unprecedented load growth, mirroring the clear “causer-pays” principle seen in states like Ohio.

- The validation of this more stringent model was accelerated by stark demand forecasts. Projections showing U.S. data center power demand climbing to 134 GW by 2030 made it clear that the previous, less precise regulatory tools were insufficient to manage the scale of the impending grid strain.

Explosive Growth in Data Center Resource Usage

This section introduces the ‘Causer-Pays’ model. The chart provides the justification for such a policy by visually demonstrating the ’cause’—the explosive growth in resource consumption by data centers—that the tariff model aims to address.

(Source: CSG South)

SWOT Analysis, Data Center Cost Allocation Policy Shift

The shift to a ’causer-pays’ model creates a clear set of strategic trade-offs for states, utilities, and data center operators, balancing the immediate political win of residential ratepayer protection against the long-term economic risk of deterring industrial development. This new policy framework establishes both new market opportunities and significant financial risks that will define the next phase of data center growth in the United States.

Hyperscale & Mega Campuses are 25% of Known Centers

A SWOT analysis requires strategic context about the subject. This chart, which segments the market and highlights the prevalence of massive Hyperscale campuses, perfectly informs the analysis of Threats (grid strain) and Opportunities (large-scale economic investment) related to a policy shift.

(Source: FracTracker Alliance)

Table: SWOT Analysis of Data Center Cost Allocation Policies

| SWOT Category | 2021 – 2024 (Incentive-Led Model) | 2025 – 2026 (‘Causer-Pays’ Model) | What Changed / Validated |

|---|---|---|---|

| Strengths | Successfully attracted rapid data center investment through broad tax incentives and a low barrier to entry for developers. | Protects residential and small business ratepayers from subsidizing industrial growth, creating long-term regulatory stability and social license to operate. | The political and economic unsustainability of socializing massive infrastructure costs was validated, forcing a policy correction. |

| Weaknesses | Exposed general ratepayers to the costs of grid expansion for data centers, leading to rising bills and political backlash. | Creates a potential ‘first-mover disadvantage’ for states like FL and TN; high upfront costs may deter some data center developments. | The direct link between data center load and rising residential rates in states like Illinois (90% Com Ed spike) exposed the weakness of the old model. |

| Opportunities | States competed to attract a booming industry, leading to significant local economic development and tax base expansion. | Drives a new market for onsite power generation (e.g., SMRs, gas with CCUS), energy storage, and advanced efficiency technologies. | The internalization of electricity costs makes the ROI for energy efficiency and behind-the-meter generation much more compelling for data center operators. |

| Threats | Growing public and regulatory opposition to data center projects due to rising electricity bills and environmental concerns. | Capital flight to states with more lenient cost-recovery regulations; risk of grid ‘balkanization’ if large loads move off-grid. | The threat of widespread public opposition became a tangible risk that new legislation aims to proactively manage. |

2027 Projections, Will ‘Pay-Your-Way’ Become the National Data Center Standard?

The critical signal to watch in the next 18-24 months is whether other major data center markets adopt the Florida/Tennessee cost allocation model, which would solidify it as the national standard and force a fundamental repricing of data center development across the U.S. This would shift the industry’s focus from seeking favorable regulatory environments to innovating in energy management and onsite generation.

- If more states with large data center pipelines (e.g., Georgia, Arizona) enact similar ratepayer protection laws, watch for a surge in demand for onsite power solutions like natural gas generation, advanced nuclear, and large-scale energy storage as developers seek to de-risk grid dependency and cost volatility.

- If hyperscalers like Google and Microsoft expand their “pay-our-way” commitments and demand response programs (Google has already signed 1 GW of agreements), this could mean the industry is proactively embracing the new cost model to secure its social license to operate, thereby mitigating the risk of investment flight from stricter states.

- If states that maintain cost-socialization models see continued political fallout from rising residential bills, watch for utilities to propose new tariff structures preemptively. This could mirror moves by utilities like PGE and Pacifi Corp to create specialized rates for large loads, signaling a voluntary industry shift to avoid mandated legislative action.

AI to Drive Explosive Data Center Power Demand

This section is about ‘2027 Projections’ and future standards. A forecast chart showing that AI is the key driver of future explosive power demand directly supports a forward-looking discussion. This projected demand is the reason new standards like ‘Pay-Your-Way’ are being considered.

(Source: Deloitte)

The questions your competitors are already asking

This report covers one angle of the state-level policy shift toward data center cost containment. The questions that matter most depend on your work.

- What is the outlook for similar ratepayer protection laws being passed in other data center hotspots like Virginia and Georgia by 2028?

- What are the opportunities for utilities to create new ‘data center-only’ electricity tariffs under these new regulations?

- Which data center developers are most exposed to this regulatory shift, and how are they adapting their site selection strategies?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.