Woodside Energy Blue Hydrogen Pivot, $140 M H 2 OK Cancellation, Japan Suiso Energy Mo U, and 2 Project Shifts (2024 to 2026)

Green Hydrogen Commercial Risks, Woodside Energy $140 M Cancellation

The 2025 market forced a reckoning for the green hydrogen sector, as major energy players like Woodside Energy executed a strategic retreat from ambitious, high-cost green hydrogen projects in favor of more commercially viable blue hydrogen initiatives, a pivot driven by capital discipline in the face of escalating costs and uncertain near-term demand.

- Between 2021 and 2024, Woodside Energy pursued a broad portfolio of green hydrogen opportunities, including the H 2 Tas project in Tasmania and the Southern Green Hydrogen project in New Zealand; however, by September 2024, both large-scale projects were halted.

- The strategic shift culminated in July 2025 with the official cancellation of the flagship H 2 OK green hydrogen project in Oklahoma, a decision that mirrored a wider market correction, as competitor Fortescue also scrapped several of its US and Australian green hydrogen plans during the same period.

- In response to these cancellations, Woodside Energy re-scoped its H 2 Perth project, pivoting it from a hybrid green-blue model to a focused blue hydrogen facility using natural gas reforming, a move designed to leverage the company’s existing gas processing expertise and infrastructure.

- This industry-wide recalibration was underpinned by unfavorable economics, with green hydrogen production costs estimated between $6 and $9 per kilogram, rendering it uncompetitive against grey hydrogen produced at an average of $1.50 per kilogram without substantial, long-term subsidies.

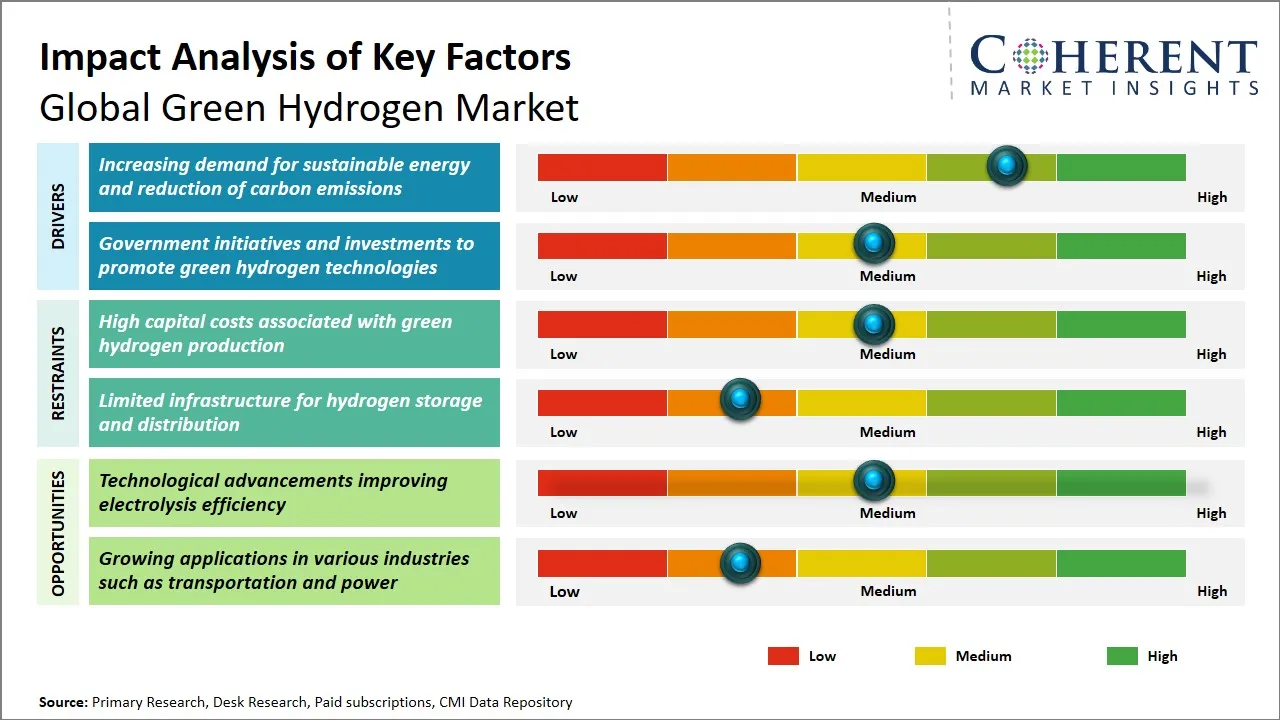

Green Hydrogen Market Faces Key Restraints

This chart’s focus on ‘Key Restraints’ directly aligns with the section’s topic of ‘Commercial Risks,’ providing a market-level explanation for why a company like Woodside might cancel a $140M project.

(Source: Coherent Market Insights)

$140 M Impairment, Woodside Energy Project Cancellations

Woodside Energy’s 2025 financial disclosures reveal a decisive reallocation of capital away from speculative new energy ventures and toward de-risked, gas-based projects that align with its core competencies and near-term commercial realities.

- The cancellation of the H 2 OK project resulted in a significant $140 million pre-tax impairment charge, a clear financial signal of the company’s unwillingness to continue funding projects with unfavorable risk-return profiles.

- This write-down contrasts sharply with the massive ongoing capital commitments to its core LNG business, including the $12.5 billion Scarborough project and the estimated A$48.7 billion (~US$35.3 billion) Browse project, underscoring where the company’s investment priorities lie.

- While Woodside Energy maintains its target to invest US$5 billion in new energy by 2030, the allocation of this capital has shifted, with funds now prioritized for projects with clearer commercial pathways, such as its proposed 1.1 million mt/y blue ammonia plant on the US Gulf Coast.

Table: Woodside Energy Project Cancellations and Core Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Browse Project (LNG) | May 2026 (Cost Update) | Investment in a long-term LNG production asset. The project cost estimate rose to A$48.7 billion, reinforcing the company’s focus on its core gas business. | Guru Focus |

| H 2 OK (Green Hydrogen) | July 2025 (Cancellation) | The project was formally cancelled, resulting in a $140 million write-down. The decision was based on high costs and insufficient customer demand. | Australian Financial Review |

| Scarborough Project (LNG) | July 2024 (Cost Update) | The budget for this giant Australian gas project increased to $12.5 billion, with the first LNG cargo on track for 2026. This demonstrates continued heavy investment in fossil fuel assets. | Upstream |

| H 2 Tas and Southern Green Hydrogen | September 2024 (Halted) | Development was halted on two large-scale green hydrogen projects in Australia and New Zealand, marking the beginning of the strategic retreat from pure-play green hydrogen. | Industrial Info Resources |

Woodside Energy Secures JSE & KEPCO Mo U for Asian Offtake

In 2025, Woodside Energy‘s partnership strategy pivoted from exploring green hydrogen production technologies to securing firm offtake agreements for its revised blue hydrogen projects, prioritizing access to mature and demand-heavy Asian energy markets.

- The most significant development was the September 25, 2025, Memorandum of Understanding (Mo U) signed with Japan Suiso Energy (JSE) and Kansai Electric Power (KEPCO) to establish a liquid hydrogen supply chain from the revised H 2 Perth project to Japan.

- This forward-looking agreement to establish a market contrasts with the September 2024 termination of its partnership with Meridian Energy for the Southern Green Hydrogen project in New Zealand, which was halted before a market was secured.

- The company also has a conditional offtake agreement signed in October 2024 to supply clean liquid hydrogen to Singapore’s Keppel Corporation starting in 2030, further demonstrating a strategic focus on locking in future demand ahead of major capital commitments.

Asia Pacific Leads 2025 Green Hydrogen Market

The chart shows the dominance of the Asia Pacific market. This provides the strategic context for why Woodside is securing offtake agreements with Asian partners (JSE & KEPCO), as mentioned in the section.

(Source: Precedence Research)

Table: Woodside Energy Hydrogen-Related Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Japan Suiso Energy (JSE), Kansai Electric Power Co. (KEPCO) | September 2025 | Signed an Mo U to develop a liquid hydrogen supply chain from the H 2 Perth project to Japan, securing a potential anchor market for the revised blue hydrogen facility. | Hydrogen Insight |

| 1414 Degrees | May 2025 | Entered a collaboration to work on a green hydrogen development project, indicating continued interest in novel technologies, though at a much smaller, exploratory scale. | Fuel Cells Works |

| Meridian Energy | September 2024 | Terminated the partnership for a proposed green hydrogen and ammonia project in New Zealand, a key early signal of its strategic withdrawal from large-scale greenfield projects. | Industrial Info Resources |

Australia and US, Woodside Energy Geographic Hydrogen Strategy

Woodside Energy‘s geographic strategy in 2025 consolidated around leveraging Australia’s abundant natural gas reserves for blue hydrogen export and the US Gulf Coast’s industrial infrastructure for blue ammonia, while systematically exiting more speculative green hydrogen plays in other regions.

- From 2021 to 2024, the company pursued a geographically diverse strategy, exploring green hydrogen projects in Tasmania (H 2 Tas), Western Australia, New Zealand (Southern Green Hydrogen), and the US (H 2 OK in Oklahoma).

- The year 2025 marked a sharp consolidation, with the formal cancellation of the Oklahoma project and the earlier halting of its Tasmanian and New Zealand ventures, effectively narrowing its focus to two key strategic regions.

- The revised strategy prioritizes Western Australia for the export-oriented H 2 Perth blue hydrogen project, aimed at serving Asian markets, and the US Gulf Coast for a blue ammonia plant designed to tap into an established industrial market.

Refining, Ammonia Dominate 2025 Green Hydrogen Use

This chart identifies key end-user industries for hydrogen. A geographic strategy for Australia and the US would be heavily informed by the location and concentration of these industries, making the chart relevant to the section.

(Source: Precedence Research)

Blue Hydrogen Technology, Woodside Energy’s Commercial Pivot

Woodside Energy‘s 2025 strategy validates that while emerging technologies like green hydrogen electrolysis are progressing, they are not yet commercially mature for unsubsidized, large-scale deployment, compelling a strategic pivot to established technologies like natural gas reforming coupled with carbon capture.

- In the period from 2021 to 2024, Woodside Energy actively explored electrolysis-based green hydrogen for its planned H 2 OK and H 2 Tas projects, aligning with the industry’s focus on purely renewable pathways.

- The 2025 pivot saw the company explicitly select natural gas reforming, a mature and cost-effective technology, as the production method for its downsized H 2 Perth project, de-risking the venture from a technology-readiness standpoint.

- This shift moves the primary technological challenge from production to logistics, with the company’s partnership with JSE and KEPCO now focused on developing the complex and capital-intensive infrastructure for a large-scale liquid hydrogen (LH₂) supply chain.

- The startup of the smaller Hydrogen Refueller @H 2 Perth, targeted for Q 4 2025, will serve as the company’s first operational testbed for hydrogen infrastructure and local market development before committing to a larger facility.

Blue Hydrogen More Cost-Effective Than Green Hydrogen

The section describes a ‘Commercial Pivot’ to blue hydrogen. This chart provides the direct commercial rationale for such a pivot by illustrating the cost-effectiveness of blue hydrogen compared to green.

(Source: Enverus)

SWOT Analysis, Woodside Energy Hydrogen Strategy Shift

Woodside Energy’s strategic pivot in 2025 leveraged its core strengths in gas processing to pursue a pragmatic, near-term low-carbon business, but also exposed the company to risks associated with the long-term viability of carbon capture and the market acceptance of blue hydrogen.

- The shift from green to blue hydrogen plays directly to the company’s strengths in natural gas processing and large project execution.

- However, it creates a potential weakness by increasing reputational risk and dependence on the successful, cost-effective deployment of Carbon Capture and Storage (CCS) technology.

- The key opportunity is to enter the hydrogen market sooner and at a lower cost point than green-focused competitors, capturing early demand in Asia, though this is threatened by long-term competition from pure-play green hydrogen producers as costs fall.

Hydrogen Generation Market to Surpass $285B by 2035

A SWOT analysis evaluates opportunities. This chart’s forecast for the entire hydrogen generation market (including blue hydrogen) represents a significant ‘Opportunity’ that would be a core component of a SWOT analysis on Woodside’s strategy shift.

(Source: Precedence Research)

Table: SWOT Analysis for Woodside Energy’s Hydrogen Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Expertise in large-scale LNG projects and access to gas reserves were seen as a bridge to a future green hydrogen business. | Core competencies in gas processing and project management became the central pillar of the near-term low-carbon strategy itself. | The company validated that its most bankable path to the hydrogen economy was through leveraging its existing business, not by creating a new one from scratch. |

| Weaknesses | High carbon intensity of core LNG business; perceived slow movement on pure-play renewables compared to some competitors. | Increased reputational risk for abandoning green hydrogen projects; heavy reliance on the technical and commercial viability of CCS. | The pivot made the company’s low-carbon claims entirely dependent on the success of CCS, a technology with its own history of challenges. |

| Opportunities | Lead the development of large-scale green hydrogen export hubs in Australia (e.g., H 2 Tas). | Capture near-term hydrogen demand in Japan and Korea with cost-competitive blue hydrogen via the H 2 Perth project and its partnership with JSE and KEPCO. | The market opportunity shifted from being a first-mover in green hydrogen to a pragmatic, early supplier of blue hydrogen, prioritizing revenue over renewable purity. |

| Threats | High capital cost and slow development of commercial-scale electrolyzer projects. | Long-term competition from government-subsidized green hydrogen; potential for CCS projects to fail or underperform; negative public perception of “blue” hydrogen. | The primary threat of high green hydrogen cost was validated, leading to the strategic shift. A new threat emerged: being outcompeted if green hydrogen costs fall faster than expected. |

Scenario Modelling, Woodside Energy’s FID on H 2 Perth

The single most critical event to watch for Woodside Energy is a Final Investment Decision (FID) on the revised H 2 Perth blue hydrogen project, as this will validate the commercial viability of its strategic pivot and the bankability of its Asian offtake agreements.

- If an FID is announced in the next 12-18 months, watch for the specific capital expenditure figures and the terms of the binding offtake agreements with JSE and KEPCO. This would confirm market confidence in blue hydrogen.

- If the FID is delayed or the project is downsized further, this could signal continued difficulty in securing profitable long-term contracts or unresolved technical and financial hurdles with the required CCS component.

- Concurrently, watch for an FID on the US blue ammonia plant. Progress on this project would confirm that Woodside Energy is successfully executing its two-pronged, gas-based low-carbon strategy.

- A key external factor to monitor is the impact of government incentives like Australia’s Hydrogen Production Tax Incentive. If subsidies become generous enough to close the cost gap with blue hydrogen, it could force Woodside Energy to re-evaluate green hydrogen projects once again.

Hydrogen Demand Projected to Surge Post-2030

This section concerns ‘Scenario Modelling’ for a Final Investment Decision (FID). A long-term demand projection, such as the post-2030 surge shown in the chart, is a crucial input for such financial and strategic modelling.

(Source: PwC)

The questions your competitors are already asking

This report covers one angle of the commercial recalibration of the hydrogen market, as seen through Woodside Energy’s pivot from green to blue hydrogen projects. The questions that matter most depend on your work.

- Which energy majors, besides Woodside, are gaining ground by pivoting from green to blue hydrogen projects?

- What is the outlook for large-scale green hydrogen deployment by 2030, given the recent project cancellations by Woodside Energy and Fortescue?

- What is actually happening with Woodside Energy’s H2Perth project since the pivot to a blue hydrogen-only facility?

- Woodside Energy activities in Japan. Is the MoU with Japan Suiso Energy progressing toward a firm offtake agreement for blue hydrogen?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.