ADNOC Hydrogen Strategy 2026: How Offtake Risk Shapes its $23 B Global Push

ADNOC’s Commercial Shift: From Hydrogen Pilots to Securing Market Offtake

Abu Dhabi National Oil Company (ADNOC) has strategically evolved its hydrogen initiatives from demonstrating technical feasibility between 2021 and 2024 to an aggressive 2025-2026 focus on executing commercial-scale projects and securing buyers, directly confronting the industry’s primary constraint of insufficient market demand. The company’s actions show a clear recognition that building production capacity alone is insufficient, and that creating and securing bankable offtake is now the most critical activity for unlocking its multi-billion-dollar investments.

- In the 2021-2024 period, ADNOC focused on foundational pilots and market-seeding activities, including a hydrogen mobility pilot with Toyota in 2023 and delivering demonstration cargoes of low-carbon ammonia to Aurubis in Germany and partners in Japan in 2022. This phase validated production concepts and established market relationships.

- The period from January 2025 onward marks a distinct shift toward commercial execution and risk mitigation. This is highlighted by the decision of its joint venture, Fertiglobe, to hold off on a >$1 billion blue hydrogen investment in January 2025 specifically due to a lack of secured offtake agreements with Asian buyers, confirming that market demand is the key gating factor for large-scale capital deployment.

- ADNOC‘s response has been to de-risk its strategy on two fronts: securing feedstock and financing for massive scale-up through an $11 billion deal for the Hail and Ghasha gas fields in December 2025, while simultaneously diversifying its technology base with a world-first turquoise hydrogen pilot launched in January 2025 to create new, potentially more economic, decarbonization pathways.

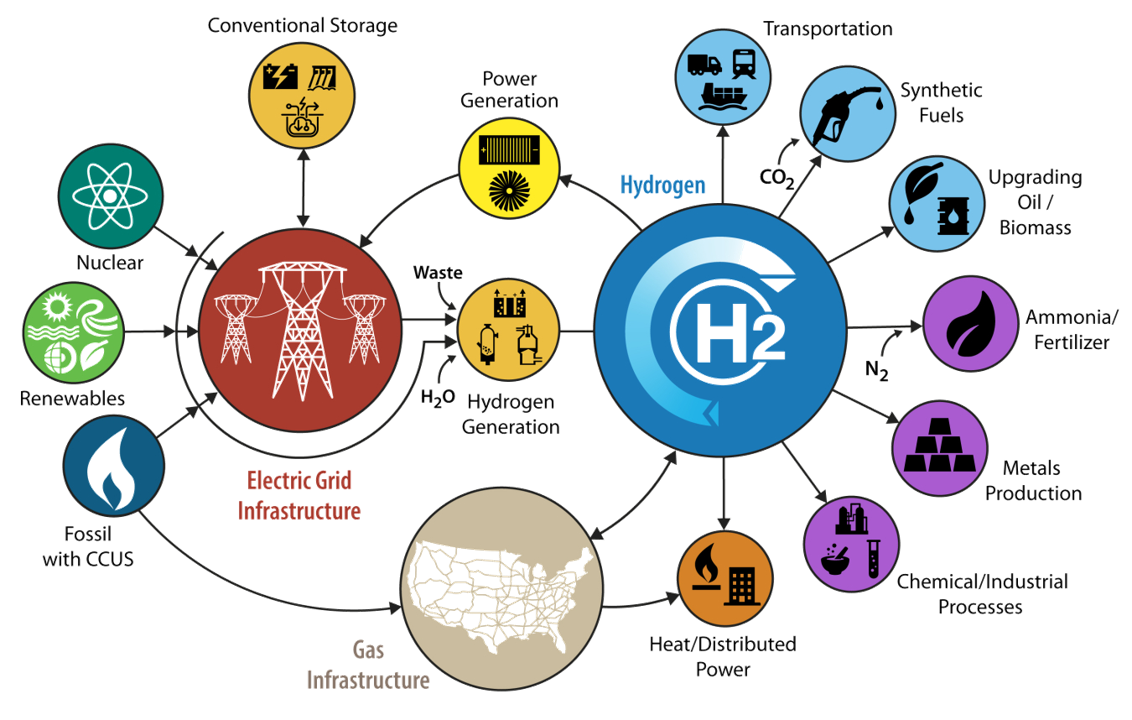

ADNOC Builds Full Hydrogen Value Chain

This chart illustrates the complete hydrogen value chain, from production to securing offtake markets, which directly mirrors ADNOC’s strategic shift described in the section.

(Source: Sandia National Laboratories)

ADNOC’s Capital Allocation: $23 B Directed at De-Risking Hydrogen Production

ADNOC has systematically increased its capital commitment to low-carbon solutions, with a clear focus on deploying capital to build the upstream and midstream infrastructure necessary to produce blue hydrogen at scale. This financial strategy is not just about funding projects, but about making strategic investments in enablers like gas feedstock and carbon capture, thereby reducing the marginal cost of its future hydrogen output.

- The company’s financial commitment escalated significantly, from an initial $15 billion earmarked for its low-carbon portfolio in November 2022 to an increased allocation of $23 billion by December 2023. This enlarged capital pool is designated for a range of initiatives critical to its hydrogen ambitions, including carbon capture, electrification, and renewable energy projects.

- In late 2025, ADNOC executed two pivotal financing transactions that directly underpin its blue hydrogen strategy. It secured up to $11 billion in structured financing for the Hail and Ghasha gas development to guarantee long-term feedstock, and a separate $2 billion green financing agreement backed by K-SURE to fund the broader decarbonization infrastructure that enables low-carbon production.

- The decision by Fertiglobe in January 2025 to pause a >$1 billion project serves as a crucial example of disciplined capital allocation. It demonstrates that major investment decisions are contingent on securing bankable, long-term offtake agreements, preventing the creation of unutilized, large-scale assets and aligning capital expenditure with confirmed market demand.

Table: ADNOC’s Hydrogen-Related Investments and Financing

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Expansion into Venezuelan Gas Markets | Jan 2026 | Strategic investment to access vast gas reserves, securing long-term, low-cost feedstock for future blue hydrogen production. | ADNOC Venezuela Gas Investment: Market Opportunity Analysis |

| K-SURE Backed Green Financing | Dec 2025 | Secured $2 billion in green financing to fund lower-carbon projects, including hydrogen and related decarbonization infrastructure, strengthening ties with the key Korean market. | ADNOC Secures $2 Billion K-SURE Backed Green Financing |

| Hail and Ghasha Gas Development | Dec 2025 | Secured up to $11 billion in financing for a major sour gas project, providing the critical natural gas feedstock for large-scale blue hydrogen and ammonia ambitions. | ADNOC Secures Landmark Structured Financing |

| Increased Low-Carbon CAPEX | Dec 2023 | Increased total allocation to $23 billion for low-carbon projects, including CCS, hydrogen, and renewables, to accelerate its 2030 decarbonization goals. | Reuters |

| Habshan Carbon Capture Project (FID) | Oct 2023 | Final investment decision on a 1.5 MTPA CCS project, a critical enabling technology for its blue hydrogen and ammonia production plans. | ADNOC Announces Final Investment Decision |

| Initial Low-Carbon CAPEX | Nov 2022 | Initial $15 billion allocation (2023-2027) to advance low-carbon solutions, including clean power, carbon capture, and new energies like hydrogen. | ADNOC Driving Decarbonization with $15 Billion Investment |

ADNOC’s Partnership Ecosystem: Building Value Chains from Technology to Offtake

ADNOC has strategically shifted its partnership model from exploratory studies in the 2021-2024 period to forming concrete project development and technology deployment alliances in 2025. This new phase is focused on building complete, resilient value chains that span from upstream technology optimization to securing downstream market access.

$14T Market Context for ADNOC’s Investments

This chart projects a $14 trillion low-carbon market, providing the high-level strategic context for the specific large-scale investments and financing deals detailed in the accompanying table.

(Source: ExxonMobil)

- The early 2021-2023 period was characterized by foundational Memorandums of Understanding (Mo Us) and joint studies with partners like Japan’s JERA and ENEOS to explore supply chain concepts. In contrast, February 2025 saw a major project development partnership with Exxon Mobil to build what is planned to be the world’s largest low-carbon hydrogen facility, signaling a move from exploration to execution.

- Starting in 2024, ADNOC broadened its alliances to include critical enabling technologies. A January 2024 agreement with Santos targets carbon management solutions like CCS and direct air capture (DAC), while 2025 partnerships with SLB and Microsoft focus on using AI to optimize production efficiency and lower the carbon intensity of its hydrogen feedstock.

- A pivotal strategic addition in January 2025 was the deployment of a turquoise hydrogen pilot with UK-based Levidian. This collaboration moves methane pyrolysis technology from R&D to an operational setting, diversifying ADNOC’s technology risk beyond the conventional blue/green hydrogen dichotomy and creating an entirely new production pathway.

- The company also expanded its collaboration with Italian energy company Eni in February 2025, focusing on renewables and green transition efforts, including synergies related to electricity supply for data centers and green hydrogen production.

Table: ADNOC’s Key Hydrogen and Clean Tech Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SLB | Nov 2025 | Launched Ai PSO, an AI-powered solution to optimize upstream production, enhancing feedstock efficiency for blue hydrogen. | ADNOC and SLB Launch Transformative AI-Powered Solution |

| Microsoft | Oct 2025 | Joint report on integrating AI into the energy sector to drive efficiency and support energy transition goals, including hydrogen. | ADNOC and Microsoft Powering Possible Report |

| Exxon Mobil | Feb 2025 | Partnership to develop the world’s largest low-carbon hydrogen production facility, leveraging expertise in large-scale projects and CCS. | Decarbonfuse |

| Levidian | Jan 2025 | Installed a world-first turquoise hydrogen pilot at an operating gas plant, validating methane pyrolysis as a new production pathway. | Hydrogen Insight |

| Santos | Jan 2024 | Strategic collaboration to jointly develop carbon management technologies, including CCS and DAC, to support low-carbon fuel production. | ADNOC and Santos to Collaborate |

| JERA | May 2023 | Joint feasibility study for a large-scale clean ammonia production facility in Abu Dhabi focused on supplying the Japanese market. | ADNOC and JERA to Explore Collaboration |

ADNOC’s Global Reach: From Domestic Production Hub to Asian and European Markets

While the UAE remains the strategic core for production, ADNOC‘s geographic focus has sharpened significantly, moving from broad international outreach to a concentrated effort on developing Asia and Europe as primary offtake markets. More recently, the company has expanded its geographic footprint upstream, securing overseas gas resources to ensure the long-term cost-competitiveness of its blue hydrogen exports.

GCC Hydrogen Export Market Opportunity

As ADNOC expands its global reach to Asia and Europe, this chart quantifies the value of the regional export market it operates in, projecting growth to over $2 billion.

(Source: P&S Intelligence)

ADNOC Visualizes Carbon Capture Ambition

This visualization of large-scale carbon capture technology directly corresponds to the partnerships listed in the table, such as the ExxonMobil collaboration on a major CCUS project.

(Source: EnkiAI)

- Between 2021 and 2024, ADNOC focused on establishing the UAE, particularly the TA’ZIZ industrial hub in Ruwais, as its central production base. Early partnerships with Japanese entities and demonstration cargoes to Germany were designed to test logistics and build relationships in these key future import regions.

- The period from 2025 has brought this geographic strategy into sharp relief. The pause on the Fertiglobe project explicitly identified “Asian buyers” as the critical missing piece, reinforcing Asia’s energy security needs as the primary driver for demand. Furthermore, the $2 billion K-SURE financing deal in December 2025 deepens financial and strategic ties with South Korea, another key target market.

- A notable strategic expansion occurred in January 2026 with ADNOC’s move to invest in Venezuela’s vast gas markets. This upstream diversification is a long-term play aimed at securing access to low-cost international feedstock, providing a hedge against domestic resource constraints and maintaining a competitive edge in the global hydrogen export market.

Hydrogen Technology Diversification: From Blue Hydrogen Scale-Up to Turquoise Pilots

ADNOC‘s technology strategy is defined by a pragmatic, multi-pathway approach, prioritizing the maturation of blue hydrogen to achieve near-term commercial scale while actively piloting next-generation technologies like turquoise hydrogen. This diversifies its portfolio and hedges against future technological disruptions, cost fluctuations, and evolving regulations in import markets.

- In the 2021-2024 timeframe, the company’s efforts centered on validating the blue ammonia production process through its Fertiglobe joint venture and advancing the critical enabling technology of carbon capture, culminating in the FID for its Habshan CCS project in 2023. Green hydrogen remained at a small, 15 MW pilot scale, focused on gaining operational experience.

- The year 2025 marked an inflection point towards large-scale deployment. The partnership with Exxon Mobil to develop a world-scale blue hydrogen facility demonstrates a commitment to move blue hydrogen technology into full commercial operation, leveraging established expertise in industrial gas processing and carbon management.

- The most significant technological shift was the January 2025 launch of the Levidian turquoise hydrogen pilot. This project moves methane pyrolysis from an R&D concept (explored with Baker Hughes) to operational testing, validating a novel production pathway that splits methane into hydrogen and solid carbon (graphene), thus avoiding the need for geological CO 2 storage.

SWOT Analysis: ADNOC’s Evolving Hydrogen Strategy

ADNOC‘s hydrogen strategy has successfully leveraged its incumbent strengths in hydrocarbon resources and access to capital. However, the defining shift from 2021 to 2025 has been the transition of its primary challenge from internal technology development to managing external market offtake risk, a weakness it is now addressing with a more diversified and commercially-focused approach.

- Strengths: The company converted its potential strength of capital access into a demonstrated ability to secure massive, multi-billion-dollar financing for complex energy projects.

- Weaknesses: The central weakness evolved from internal technology gaps in areas like green hydrogen to an external market vulnerability, proven by the inability to secure bankable offtake for blue ammonia projects.

- Opportunities: The opportunity set expanded from simply exporting a new fuel to creating additional value streams through technology diversification, such as producing graphene from turquoise hydrogen.

- Threats: The abstract threat of weak market demand materialized into a tangible business obstacle, forcing a direct strategic response and validating concerns about the commercial readiness of global hydrogen markets.

Table: SWOT Analysis for ADNOC’s Hydrogen Initiatives

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Access to vast natural gas reserves; strong sovereign financial backing; existing large-scale industrial infrastructure. | Demonstrated ability to secure complex, multi-billion-dollar financing ($11 B for Hail/Ghasha); partnerships with energy supermajors (Exxon Mobil). | The company’s strength shifted from latent potential (access to capital) to proven execution (securing specific, large-scale financing for its hydrogen feedstock strategy). |

| Weaknesses | Limited operational experience in green hydrogen electrolysis; reliance on scaling up CCS technology for blue hydrogen. | Inability to secure bankable long-term offtake agreements for blue ammonia, leading to major project delays (Fertiglobe‘s >$1 B investment hold). | The primary weakness pivoted from an internal technology/experience gap to an external market failure, validating that production capability is outpacing firm demand. |

| Opportunities | First-mover advantage to capture future demand in Asian (Japan, Korea) and European (Germany) markets. | Diversifying the technology portfolio with turquoise hydrogen (Levidian pilot), creating a new revenue stream from solid carbon (graphene) and an alternative to CCS. | The opportunity evolved from selling a single product (hydrogen/ammonia) to creating a diversified technology and product portfolio that is more resilient to market shifts. |

| Threats | Potential for “green-only” import regulations (e.g., EU’s Carbon Border Adjustment Mechanism) to disadvantage blue hydrogen; competition from other low-cost producers. | The theoretical threat of weak demand became a commercial reality, as evidenced by the lack of buyers willing to sign binding offtake for the Fertiglobe project. | The risk of relying on fossil-based hydrogen was validated not by regulation, but by market hesitancy, confirming that securing buyers is the most immediate threat to the business case. |

2026 Outlook: ADNOC’s Success Hinges on Converting Projects into Contracts

If ADNOC can secure at least one major, binding long-term offtake agreement for its blue ammonia in 2026, it will trigger a final investment decision on its flagship TA’ZIZ plant and validate its entire large-scale blue hydrogen strategy. Without it, the company will likely prioritize its more flexible, technologically diversified pilot projects while it waits for the global market to mature.

- The primary signal to watch is a Final Investment Decision (FID) on the 1 MTPA TA’ZIZ blue ammonia facility. This action would confirm that the offtake risk has been sufficiently mitigated through one or more bankable contracts, unlocking major construction.

- Monitor for official announcements of binding, multi-year purchase agreements with entities in Japan, South Korea, or Germany. A shift from non-binding Mo Us and single demonstration cargoes to firm contracts is the clearest indicator of market confidence. The $2 billion K-SURE financing strongly suggests South Korea is a priority target.

- Track the technical and economic performance of the Levidian turquoise hydrogen pilot. A successful outcome demonstrating reliable production of hydrogen and high-quality graphene could prompt a rapid scale-up decision, fundamentally altering ADNOC‘s long-term technology roadmap and providing a powerful alternative to CCS-dependent production.

Frequently Asked Questions

What is the biggest challenge currently facing ADNOC’s hydrogen strategy?

The biggest challenge for ADNOC is securing bankable, long-term offtake agreements from buyers. The article explicitly states that the primary constraint on the industry is “insufficient market demand.” This was confirmed when its joint venture, Fertiglobe, paused a project worth over $1 billion specifically because it could not secure purchase agreements with Asian buyers.

Why is ADNOC investing in turquoise hydrogen if its main focus is on blue hydrogen?

ADNOC is investing in a turquoise hydrogen pilot with Levidian to diversify its technology portfolio and hedge against risks. Turquoise hydrogen, made through methane pyrolysis, splits natural gas into hydrogen and solid carbon (graphene), avoiding the need for geological CO2 storage required for blue hydrogen. This creates a new, potentially more economic production pathway and an additional revenue stream from selling graphene.

How is ADNOC using its $23 billion low-carbon fund to support its hydrogen goals?

ADNOC is deploying the $23 billion to de-risk its hydrogen production by investing in critical enabling infrastructure. This includes securing long-term natural gas feedstock through the $11 billion Hail and Ghasha project, funding carbon capture facilities like the Habshan CCS project, and financing other decarbonization efforts that lower the overall carbon intensity and marginal cost of its future blue hydrogen output.

What is the main difference between ADNOC’s strategy from 2021-2024 and its strategy from 2025 onwards?

Between 2021 and 2024, ADNOC focused on demonstrating technical feasibility through pilot projects and demonstration cargoes. From 2025 onwards, its strategy has shifted aggressively towards commercial execution, risk mitigation, and securing market offtake. The focus is no longer on proving the technology but on securing the binding contracts needed to justify large-scale capital investments.

What would be the most important sign of success for ADNOC’s hydrogen strategy in 2026?

The most important sign of success would be a Final Investment Decision (FID) on its 1 MTPA TA’ZIZ blue ammonia facility. This action would only be triggered if ADNOC successfully secures at least one major, binding long-term offtake agreement, which would validate its entire large-scale blue hydrogen strategy by confirming that market demand has been secured.