Lithium-Sulfur Cathodes for Grid Storage: 14 Bankruptcies, Lyten’s Northvolt Deal, and the 2, 000-Cycle Hurdle (2021 to 2026)

Lithium-Sulfur Commercial Viability Hinges on Bridging Lab Performance with Grid-Scale Durability

Lithium-sulfur (Li-S) adoption for grid-scale energy storage is stalled by a critical gap between the technology’s promising lab-scale energy density and the poor cycle life of commercially relevant cells, preventing it from becoming a bankable alternative to established lithium iron phosphate (LFP) technology. While the theoretical cost advantage of using abundant sulfur is compelling for 4-to-12-hour storage, the inability to deliver thousands of reliable cycles makes its levelized cost of storage (LCOS) uncompetitive for utility projects.

- Between 2021 and 2024, industry focus was on lab breakthroughs, such as a cell reportedly achieving 25, 000 cycles. These results generated significant investor interest but failed to translate into commercially available products that could meet grid-level durability requirements.

- From 2025 to today, a market correction has occurred. While companies like Lyten and Valgotech are establishing production facilities, the primary commercial focus has shifted toward niche, high-energy-density applications like aerospace and defense, which can tolerate a lower cycle life in exchange for reduced weight.

- The commercial hurdle for grid applications is substantial. The industry benchmark for grid-scale battery energy storage systems (BESS), such as those being deployed by Primergy, is a cycle life of 3, 000 to over 10, 000 cycles, typically delivered by LFP batteries. Li-S technology, with a current demonstrated commercial cycle life of 200–500 cycles, does not meet the technical or financial requirements for these long-term infrastructure assets.

- This difficulty in scaling is underscored by the fact that 14 Western battery companies have gone bankrupt since January 2025, despite collectively raising over $20 billion. This trend signals a major market filter, where technologies without a clear and immediate path to commercial bankability are failing.

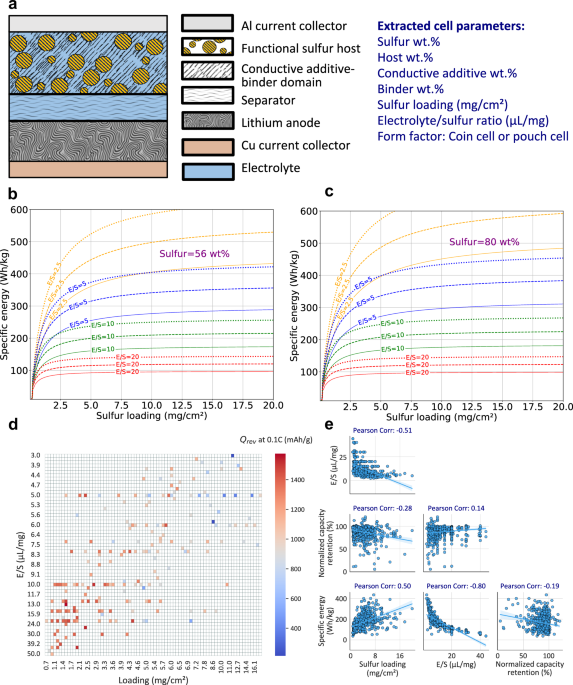

Charts Show Li-S Energy Density vs. Durability Trade-off

The section discusses the gap between lab potential and commercial reality, which is often defined by the trade-off between performance (energy density) and longevity (durability). This chart visualizes that central conflict.

(Source: Nature)

Investment in Lithium-Sulfur Is Defined by Strategic Scaling and Sector-Wide Financial Headwinds

Investment in Li-S is bifurcated, characterized by targeted government and strategic corporate funding for a few promising players, while the broader next-generation battery sector faces a harsh financial reality marked by numerous failures. The capital flowing into the sector is not chasing theoretical performance but is rewarding companies that demonstrate a credible strategy for securing their supply chain and scaling production, even if for initial niche markets.

- Lyten‘s acquisition of Northvolt‘s former battery facility in Sweden in March 2026, following its start of battery-grade lithium metal production in the U.S. in April 2025, demonstrates a strategic push to build a vertically integrated, non-Chinese supply chain. This move has bolstered investor confidence in its ability to execute.

- Government support remains critical for pre-commercial technologies. In January 2026, Nex Tech Batteries secured a $1.9 million U.S. Space Force SBIR award to advance its Li-S technology, highlighting its strategic value for defense applications where high energy density is a priority over long-term cycle cost.

- Despite these targeted investments, the broader market for advanced batteries is undergoing a shakeout. The failure of numerous startups since early 2025 indicates that venture capital is shifting away from funding science projects and toward technologies with proven commercial traction, a group that Li-S has not yet joined. The challenges in grid connections and project delays, as seen with Gresham House Energy Storage, further favor mature, proven technologies.

Li-S Research Surges Despite Technical Hurdles

A surge in research activity, as depicted in the chart, is a direct indicator of increased interest and investment in the technology, providing context for the section’s financial discussion.

(Source: Nature)

Table: Strategic Investments and Corporate Moves in Lithium-Sulfur (2025 – 2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Valgotech LLC | April 2026 | Opened a new production facility in Noblesville, Indiana, to scale up manufacturing of its Li-S batteries, signaling a move from R&D to production. | IBJ |

| Lyten, Inc. | March 2026 | Acquired a former Northvolt battery facility in Skellefteå, Sweden. This move provides Lyten with existing infrastructure to accelerate its scale-up plans and establish a European manufacturing footprint. | Ny Teknik |

| Nex Tech Batteries | January 2026 | Was selected for a $1.9 million U.S. Space Force SBIR Phase II award to advance its Li-S battery technology for high-energy-density applications. | Nex Tech Batteries |

| Lyten, Inc. | April 2025 | Began U.S. production of battery-grade lithium metal. This is a critical step in creating a domestic, China-free supply chain for its Li-S batteries. | Lyten |

U.S. and Europe Drive Li-S Development, Focused on Supply Chain Security and Niche Applications

The United States leads Li-S commercialization efforts, driven by a strategic imperative to build a domestic battery supply chain independent of China, while European activity reflects a similar goal through strategic asset acquisitions. The geographic focus is less on immediate grid deployment and more on securing the intellectual property and manufacturing capability for a technology that could provide long-term geopolitical and cost advantages.

- In the period from 2021 to 2024, Li-S research and development was geographically dispersed and largely confined to academic and corporate labs without a clear commercialization center.

- From 2025 to today, the United States has emerged as a hub for Li-S scale-up initiatives. Lyten is actively building its supply chain in the U.S., and Valgotech launched its Indiana production facility in April 2026. This activity is supported by government funding aimed at fostering domestic advanced technology manufacturing.

- European strategic interest is demonstrated through targeted acquisitions. Lyten‘s purchase of the former Northvolt facility in Sweden is the most significant recent example, providing an immediate pathway to establish a European production presence.

- The primary driver for this geographic focus is supply chain resilience. The established Li-ion supply chain is heavily dependent on China, which controls over 80% of some critical mineral processing. The development of massive projects like Grenergy‘s 11, 000 MWh Oasis de Atacama relies on these supply chains, dominated by giants like CATL. Li-S, using abundant and domestically available sulfur, offers a potential long-term alternative to this dependency.

Technology Readiness for Lithium-Sulfur Remains Pre-Commercial for Grid Applications

Li-S technology remains at a low Technology Readiness Level (TRL 4-6) for grid storage applications, stuck between component validation and system-level prototyping. The persistent and unresolved issue of the polysulfide shuttle effect, which causes rapid capacity degradation, is the primary failure mechanism preventing the technology from advancing to a commercially bankable stage for the grid sector.

- The period from 2021 to 2024 was characterized by lab-scale breakthroughs that promised high cycle life and energy density. However, these results were often achieved under idealized laboratory conditions, using configurations that were not viable for mass production or real-world operation.

- From 2025 to the present, the technology has hit a commercialization wall for grid use. While companies are now producing cells, their demonstrated cycle life of 200–500 cycles is a non-starter for project financiers and utilities who require asset lifetimes of 10–20 years.

- The fundamental scientific challenge remains the polysulfide shuttle, where intermediate sulfur compounds dissolve into the electrolyte and migrate to the anode, causing a continuous loss of active material and rapid battery failure. Until this is solved in a scalable and cost-effective manner, Li-S cannot achieve the thousands of cycles needed for grid projects.

- The immaturity of Li-S contrasts sharply with the progress of other chemistries. Established LFP continues to improve, while emerging sodium-ion technology, which does not suffer from the same degradation mechanism, is proving to be a more direct and near-term competitor for stationary storage.

Roadmap Outlines Li-S Cathode Development and Targets

The section assesses the current pre-commercial status of Li-S. A technology roadmap chart perfectly illustrates this by showing the planned progression from the current state through development stages to future commercial targets.

(Source: ScienceDirect.com)

SWOT Analysis: Lithium-Sulfur’s Cost Advantage vs. Critical Durability Weaknesses

Lithium-sulfur technology holds immense strength in its potential use of low-cost, abundant raw materials, offering a clear path to a lower-cost battery. However, this strength is fundamentally undermined by a critical weakness in cycle life and durability, which exposes it to significant market threats from more mature chemistries and creates an opportunity only if the durability hurdle can be decisively overcome.

Table: SWOT Analysis for Lithium-Sulfur Cathodes in Grid Storage

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High theoretical energy density (2, 600 Wh/kg). Cathode material (sulfur) is abundant and low-cost (<$200/ton). | Same core strengths. Potential for a non-China supply chain becomes a more prominent strategic advantage. | The fundamental material advantages were validated, but the focus shifted to their strategic importance for supply chain security. |

| Weaknesses | Poor cycle life due to polysulfide shuttle. Low technology readiness level (TRL). High cost of early-stage manufacturing. | Cycle life remains the critical bottleneck (200–500 cycles commercially). The high cost and difficulty of scaling led to 14 battery company bankruptcies. | The weakness in cycle life was validated as a hard commercial barrier, not just a technical challenge, as demonstrated by widespread market failures. |

| Opportunities | Growing demand for long-duration energy storage (LDES). Potential to achieve significantly lower LCOS than Li-ion if technical issues are solved. | Government incentives like the ITC favor domestic production. Niche markets (aerospace, defense) provide early revenue streams. | The LDES market opportunity grew, but incentives were validated to favor mature, bankable technologies, making the path for Li-S harder in the short term. |

| Threats | Competition from declining LFP costs. Competition from other next-gen chemistries like flow batteries. | Sodium-ion batteries emerged as a more immediate, lower-risk competitor for stationary storage. Potential for sulfur price shocks due to export bans (Russia). | The competitive threat intensified, with sodium-ion validating itself as a more mature and direct challenger to LFP for stationary applications. |

2027 Outlook: Lyten’s Pilot Data Is the Key Catalyst for Lithium-Sulfur’s Grid Future

The viability of Li-S for grid storage in the near term hinges on a single, critical catalyst: the public release of third-party validated data from a leading company like Lyten that demonstrates a commercial-format cell achieving at least 2, 000 deep-discharge cycles without significant capacity fade. Without this proof point, the technology will remain locked out of the mainstream grid storage market.

- If this happens: Should a company publish validated data showing a cycle life of over 2, 000 cycles, expect a rapid influx of strategic investment and the announcement of the first utility-scale pilot projects, likely in the 1–10 MWh range, as developers seek to test the technology’s bankability.

- Watch this: In the coming year, monitor announcements from Lyten, Sion Power, and other leaders. Disregard claims about energy density and focus exclusively on validated cycle life data and projected LCOS figures relevant to grid applications.

- This could be happening: If no such data emerges by 2027, Li-S will likely be cemented as a technology for niche aerospace and defense markets. Meanwhile, sodium-ion and advanced LFP chemistries will solidify their control over the stationary storage market, effectively closing the window for Li-S to become the immediate successor to LFP for grid-scale applications.

Lab Test Shows Li-S Battery Stable for 4000 Cycles

The section anticipates key pilot data. This chart, showing a concrete and impressive lab result for cycle stability, exemplifies the type of data the industry is waiting for and provides a benchmark for what the pilot data needs to demonstrate at scale.

(Source: ScienceDirect.com)

The questions your competitors are already asking

This report covers one angle of the commercial hurdles facing lithium-sulfur batteries for grid storage. The questions that matter most depend on your work.

- How does lithium-sulfur compare to LFP on a levelized cost of storage (LCOS) basis for 4-to-12-hour grid storage?

- Which companies are gaining ground in the lithium-sulfur market by pivoting from grid storage to niche applications like aerospace and defense?

- What is the outlook for lithium-sulfur deployment in grid-scale BESS by 2026, considering the 2,000-cycle hurdle?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.