Gresham House Energy Storage 2026, £150M UK Delay, CATL

BESS Grid Queues in Europe, 455 GW Stalled Projects, €100 B in Frozen Investment, and 8 Affected Countries (2021 to 2026)

455 GW in Grid Queues, BESS Project Adoption Meets Systemic Barriers

The rapid, market-driven adoption of commercially viable battery energy storage systems (BESS) across Europe has collided with systemic failures in grid infrastructure and regulatory processes, creating a 455 GW project queue that represents a significant barrier to the energy transition. This logjam, which also includes 375 GW of renewable energy projects, turns a compelling growth narrative into a story of systemic risk, where investment-ready assets are unable to reach the market due to decades of underinvestment in the continent’s electrical grids.

- Between 2021 and 2024, falling technology costs and strong policy signals for decarbonization fueled a surge in BESS project applications across Europe. Developers responded with a robust pipeline now exceeding 130 GW across more than 3, 000 utility-scale projects, demonstrating clear market readiness and investor appetite.

- By 2025 and 2026, this momentum has hit a hard ceiling. The focus has shifted from project origination to the critical, and often impassable, hurdle of securing a grid connection. The issue is exemplified by companies like Gresham House Energy Storage, which was forced to delay a £150 million earnings target after two of its battery projects received connection dates pushed out as far as 2029.

- This gridlock has led to predictions that annual BESS installations, despite strong underlying demand, will decline in 2027 before flattening from 2028. The disconnect between project viability and grid availability is now the single largest constraint on the European BESS market’s growth.

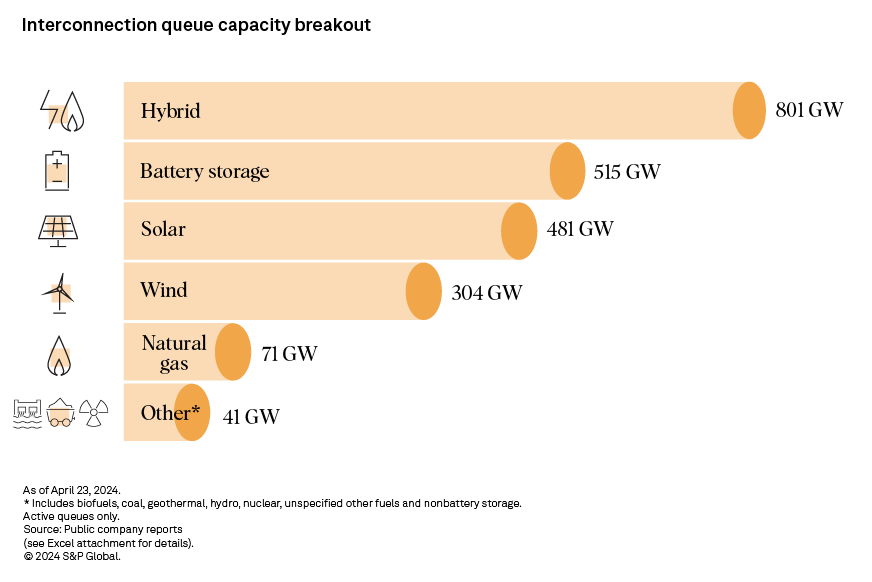

515 GW of Battery Storage Awaits Grid Connection

The chart directly quantifies the battery storage grid queue, which is the central topic of this section. The chart’s data point (515 GW) is closely aligned with the section’s headline figure (455 GW), illustrating the same core problem.

(Source: S&P Global)

Investment Risks from Grid Delays, €100 B in Capital Stalled by Queues

The primary financial risk for European BESS projects has fundamentally shifted from technology and offtake uncertainty to the inability to secure a grid connection, freezing an estimated €100 billion in capital and undermining the economic case for new development. The paradox is that this is occurring just as BESS technology has become more cost-effective and bankable than ever, with connection risk now negating technological and manufacturing gains.

- The economic viability of BESS improved dramatically into 2025, with the global average price of a turnkey system falling 31% year-over-year to as low as $117/k Wh. Other analyses confirm this trend, with battery pack prices hitting a record low of $70/k Wh in late 2025, declines that should accelerate deployment.

- However, the value of these cost reductions is nullified by connection delays. As a result, project financing is adapting to this new risk. Lenders are increasingly requiring long-term offtake agreements, such as tolling contracts or revenue floors, to mitigate the merchant risk exacerbated by unpredictable commissioning dates.

- The stalled capital and rising connection risk are creating a high-risk environment for developers and investors. The situation threatens to derail market growth, with forecasts showing the European BESS market was expected to grow from $24.22 billion in 2026 to $52.72 billion by 2031, a projection now at risk.

Nearly 700 GW Renewables Await EU Grid Connection

This chart illustrates the massive scale of the overall grid connection problem. This large queue of projects is the direct cause of the ‘investment risks’ and ‘stalled capital’ that the section heading describes.

(Source: Saur Energy)

Table: Key BESS Financial and Project Delays

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Gresham House Energy Storage | April 2026 | The company delayed a £150 million earnings target after two of its UK battery projects were assigned grid connection dates as late as 2029. This event signals that even established developers are exposed to extreme delays, making future revenue forecasts unreliable. | Quoted Data |

| EU Project Developers | June 2026 | An estimated €100 billion in renewable energy and storage investments is stalled due to grid connection bottlenecks across Europe. The figure highlights the immense scale of capital that is ready for deployment but blocked by infrastructure and regulatory constraints. | Anadolu Agency |

Europe’s BESS Gridlock, 8 Nations Report 455 GW in Stalled Projects

The grid connection crisis is a continent-wide issue, with the 455 GW figure originating from a study of just eight major European nations, indicating the full scale of the problem is likely even larger. While specific national policies offer minor relief, the lack of a coordinated, EU-wide strategy for grid modernization and regulatory harmonization remains the core of the problem, affecting major manufacturers like CATL and others dependent on the European market.

- The period from 2021 to 2024 saw countries like Germany, the UK, Spain, and Italy become hotspots for BESS project applications, driven by ambitious national renewable targets. By 2026, these same countries are now epicenters of the gridlock, with their transmission and distribution operators overwhelmed by the volume of requests.

- Individual member states have begun to react. Germany confirmed in February 2026 that BESS projects commissioned by mid-2029 will be exempt from grid fees, while Romania approved a reform in July 2025 to eliminate double taxation on storage assets.

- Despite these national efforts, they remain fragmented and insufficient to address the systemic challenge. Developers still face a patchwork of different regulations, connection standards, and queue management processes, creating significant friction and uncertainty for cross-border investment and deployment.

Commercial-Scale BESS Maturity, Technology Viability vs. Infrastructure Failure

BESS technology is fully mature, cost-competitive, and ready for mass commercial deployment, but its market implementation is being artificially suppressed by immature grid infrastructure and outdated regulatory frameworks. The current crisis is not one of technological or financial readiness but of a physical and administrative system unprepared for the pace of the energy transition. This reality check is crucial for understanding the difference between market potential and deployed reality in battery storage.

- In the 2021-2024 timeframe, the industry’s primary goals were demonstrating BESS bankability, driving down costs through manufacturing scale, and establishing reliable supply chains. These objectives were largely achieved, setting the stage for exponential growth.

- By 2025-2026, the central challenge has shifted entirely. With all-in project costs cited as low as $125/k Wh and battery pack prices falling further, the technology’s commercial case is proven. The primary constraint is now the physical and administrative capacity of the grid to interconnect new assets.

- Market confidence in the technology remains high, as shown by projections for a sixfold increase in Europe’s cumulative BESS capacity to nearly 120 GWh by 2029. However, these forecasts are fundamentally at odds with the physical barrier represented by the 455 GW connection queue, highlighting a deep disconnect between ambition and reality.

Batteries Displacing Gas for Peak Power Demand

This chart perfectly demonstrates the ‘Commercial-Scale BESS Maturity’ and ‘Technology Viability’ mentioned in the section by showing that batteries are already competitive enough to displace traditional gas peaker plants.

(Source: Reddit)

SWOT Analysis for European BESS, Strengths Undermined by External Threats

The European BESS market exhibits strong internal fundamentals, including declining costs, proven technology, and supportive high-level policies, but these strengths are being directly neutralized by the overwhelming external threat of grid unavailability and regulatory inertia. This dynamic creates a high-stakes environment where immense opportunity is counteracted by severe execution risk.

- The market’s primary strengths are its compelling economics and alignment with EU climate goals, which create powerful demand-side pull.

- Its core weaknesses stem from a lack of coordinated, forward-looking infrastructure planning and harmonized regulations across member states.

- The greatest opportunity lies in unlocking the €100 billion of stalled capital through targeted grid modernization, which would unleash a wave of new construction and economic activity.

- The most significant threat is the gridlock itself, which risks causing a cascade of project cancellations, investment flight to other regions, and a failure to meet legally binding 2030 energy and climate targets.

Battery Storage Costs Have Collapsed Sharply

The chart’s depiction of collapsing battery costs directly illustrates a key ‘Strength’ in the ‘SWOT Analysis for European BESS,’ making it a perfect conceptual match for the section.

(Source: Green Fuel Journal)

Table: SWOT Analysis of Europe’s BESS Market Amid Grid Queues

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Demonstrated cost reduction curves for lithium-ion batteries. Growing developer interest and project pipeline creation. | BESS CAPEX falls to record lows ($70-$125/k Wh). Strong policy drivers like the EU’s 42.5% renewables target for 2030 create clear demand. | The technology’s economic viability and bankability were validated. The market has proven it can supply projects faster than the grid can absorb them. |

| Weaknesses | Fragmented regulations across member states. Lack of a clear legal definition for energy storage in some jurisdictions. | Under-resourced grid operators are unable to process the surge in applications. A “first-come, first-served” queue system proves ineffective and creates speculative backlogs. | The weakness shifted from regulatory uncertainty to administrative and physical incapacity. The system is not designed for the high volume of applications. |

| Opportunities | Potential to access new revenue streams via grid services. Co-location with solar and wind projects to improve economics. | €100 billion in stalled capital can be unlocked with grid reform. The crisis forces the adoption of smart grid technologies and flexible interconnection rules. | The crisis itself creates a powerful business case for massive, continent-wide grid modernization and investment in grid-enhancing technologies. |

| Threats | Supply chain disruptions and raw material price volatility for batteries. Competition from other grid-balancing technologies. | The 455 GW grid connection queue creates multi-year delays (e.g., to 2029). Risk of mass project cancellations and investment flight. Failure to meet 2030 climate targets becomes highly probable. | The primary threat was validated and has shifted from market/technology risk to a systemic, infrastructure-based risk that is outside of a single developer’s control. |

European Grid Reforms, 455 GW Queue Highlights Urgent Policy Needs (2026)

The critical factor determining the European BESS market’s trajectory over the next three years is the speed and effectiveness of grid connection and queue management reforms. Without decisive, coordinated action to clear the existing logjam and streamline future applications, a period of project cancellations, industry consolidation, and capital flight is almost certain, fundamentally altering the battery storage market.

- If member states fail to reform their “first-come, first-served” queue systems in favor of models that prioritize commercially mature and financially secured projects, watch for a wave of M&A activity in 2027-2028. Smaller developers with stalled projects will be forced to sell to larger players with the capital and political leverage to navigate the gridlock.

- If the EU’s Grids Package, announced in late 2025, is swiftly implemented at the national level, watch for a gradual improvement in processing times beginning in late 2027. However, the physical construction of new grid capacity will still lag by several years, meaning the backlog will shrink slowly.

- These could be happening now: Developers are actively shifting strategies to mitigate interconnection risk. Watch for a pivot toward co-located solar-plus-storage projects that can use existing grid connections and a surge in investment in the commercial, industrial, and residential BESS segments, which are less dependent on utility-scale transmission access.

EU Grid Faces 120 GW Renewable Capacity Shortfall

The chart’s focus on a major capacity shortfall directly supports the section’s call for ‘Urgent Policy Needs’ and ‘European Grid Reforms’ by visualizing a clear failure to meet targets.

(Source: LinkedIn)

The questions your competitors are already asking

This report covers one angle of the systemic investment risks created by Europe’s grid connection crisis. The questions that matter most depend on your work.

- What is the outlook for BESS deployment in Europe through 2030, considering the massive grid connection queues?

- What is the status of the 455 GW of energy projects and €100 billion in investment stalled in Europe’s grid queues?

- Which BESS asset owners, like Gresham House Energy Storage, are losing ground due to multi-year connection delays?

- What are the opportunities for grid-enhancing technologies and policy reforms to unlock Europe’s stalled energy projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.