Fuel Cell Energy SOFC Data Center Shift, 100 MW Inuverse MOU, 450 MW SDCL Plan, and 2 Major Agreements (2025 to 2026)

The strategic role of hydrogen fuel cells in the data center industry has fundamentally shifted, moving from a niche clean backup power source to a critical enabler of primary baseload capacity. This transition is not driven by the maturation of the green hydrogen economy, but by necessity, as the explosive power demand from artificial intelligence collides with constrained electrical grids. The dominant commercial strategy now involves deploying “hydrogen-ready” Solid Oxide Fuel Cells (SOFCs) that operate initially on natural gas, providing an immediate solution to grid bottlenecks while offering a long-term decarbonization pathway.

Commercial Projects for Fuel Cells in Data Centers

Commercial activity for fuel cells in data centers has accelerated from small-scale backup power validation to large-scale primary power agreements designed to circumvent grid limitations. The period between 2021 and 2024 was characterized by proof-of-concept projects, whereas the period from 2025 to today is defined by multi-megawatt commercial deployments intended for always-on baseload power.

- Prior to 2025, activity centered on demonstrating technical viability for backup power. The most significant milestone was Microsoft‘s 2022 test of a 3 MW hydrogen fuel cell system, which proved it could power a data center segment for 48 consecutive hours, establishing a baseline for replacing diesel generators.

- Starting in 2025, the focus shifted to commercial-scale primary power. In July 2025, Fuel Cell Energy signed a memorandum of understanding with Inuverse to explore deploying up to 100 MW of fuel cell power for hyperscale data centers in South Korea, directly addressing grid constraints in a power-hungry market.

- This momentum continued into 2026. Fuel Cell Energy announced a partnership with SDCL in January 2026 to explore 450 MW in fuel cell deployments targeting data centers. In February 2026, Plug Power executed a $132.5 million definitive agreement with Stream Data Centers to provide hydrogen infrastructure and power solutions.

- Bloom Energy, a leader with over 400 MW deployed, received approval in January 2026 for a major data center project in Wyoming powered by its fuel cells, confirming the commercial model of using on-site generation to enable new builds where grid capacity is unavailable.

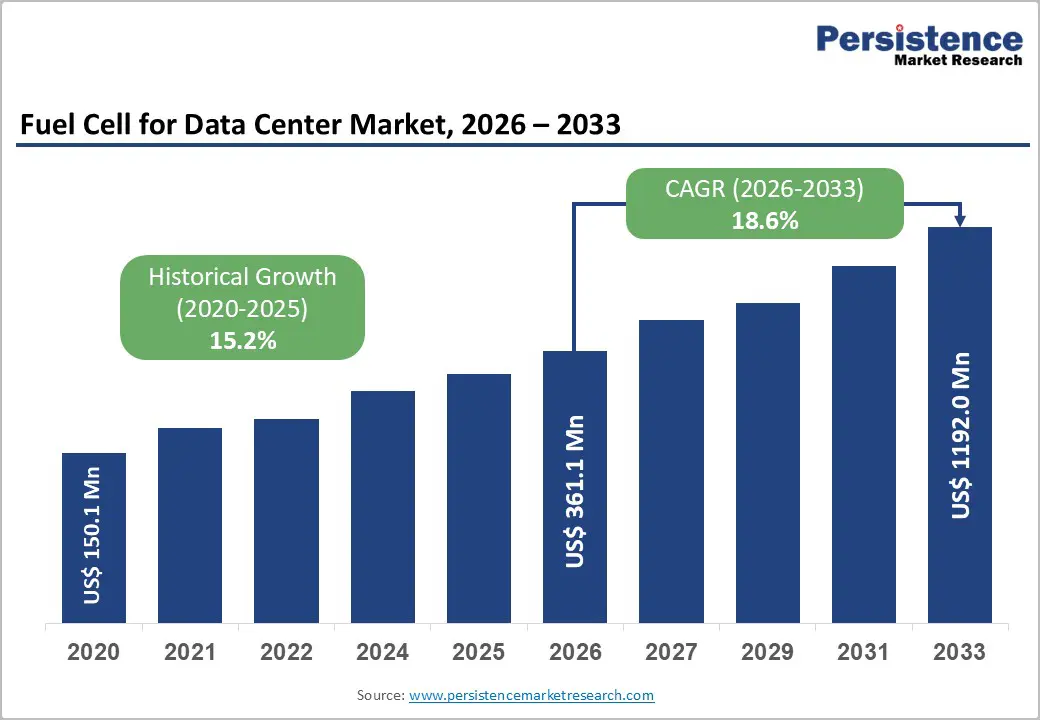

Fuel Cell Data Center Market to Exceed $1.1B

This chart directly quantifies the market size for fuel cells in data centers, providing the essential commercial context for a section discussing specific projects in this area.

(Source: Persistence Market Research)

$3/kg Tax Credits, Fuel Cell Energy Investment Analysis

Investment drivers have shifted from validating technology to enabling commercial deployment at scale, with policy incentives now playing a central role in de-risking capital expenditures. The focus has moved from corporate R&D budgets to project financing structures underwritten by government tax credits and the urgent need for power.

- The U.S. Inflation Reduction Act’s 45 V Production Tax Credit (PTC) is a critical enabler, offering up to $3 per kilogram for clean hydrogen production. The extension of the construction deadline to 2027, passed in June 2025, provides a crucial runway for projects to materialize.

- The “One Big Beautiful Bill Act” of 2025 reinstated the Investment Tax Credit (ITC), providing a 30% credit for fuel cell property. This directly reduces the upfront capital cost for data center operators, making the switch from grid dependency to on-site generation more financially viable.

- However, the supply side faces headwinds. A wave of green hydrogen project cancellations and postponements occurred in 2025 due to rising costs and uncertain offtake agreements, prompting the IEA to cut its 2030 low-emissions hydrogen production forecast by nearly 25%. This reinforces the market’s reliance on a natural gas bridge strategy.

Table: Key Financial and Policy Milestones

| Event / Policy | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power Definitive Agreement | February 2026 | Executed a $132.5 million agreement with Stream Data Centers, marking a major commercial transaction for providing hydrogen infrastructure and power to the data center sector. | Plug Power |

| Green Hydrogen Project Cancellations | July 2025 | A significant number of green hydrogen projects were cancelled or postponed due to rising costs, policy delays, and lack of firm offtake agreements, highlighting supply chain risk. | Reuters |

| “One Big Beautiful Bill Act” of 2025 | July 2025 | Reinstated a 30% Investment Tax Credit for fuel cell property, directly lowering the capital expenditure required for data centers to deploy on-site power generation. | Fuel Cell Energy |

| 45 V Tax Credit Deadline Extension | June 2025 | The U.S. Senate extended the deadline to commence construction for the 45 V clean hydrogen tax credit to the end of 2027, providing a longer runway for project development. | Fuel Cells Works |

Stationary Fuel Cell Market Share by Technology, 2025

A projection of market share by technology type serves as a key forward-looking industry milestone. This data is critical for a table summarizing the financial and policy factors shaping the future of the fuel cell industry.

(Source: Global Market Insights)

Fuel Cell Energy 2 Major Partnerships, Inuverse and SDCL

Partnerships have matured from technology demonstrations with end-users to strategic alliances with infrastructure developers and financiers aimed at deploying hundreds of megawatts. This signals a market transition toward standardized, repeatable project development and financing for fuel cell-powered data centers.

- Early-stage collaborations focused on technical validation. The ongoing work between Microsoft and Caterpillar to test a 3 MW hydrogen system is a prime example, intended to create a proven blueprint for backup power applications.

- In 2025, partnerships shifted to large-scale commercial development. The Fuel Cell Energy and Inuverse MOU from July 2025 to explore 100 MW for South Korean data centers is a strategic move to enter a high-demand, grid-constrained market.

- The January 2026 partnership between Fuel Cell Energy and SDCL to explore 450 MW of deployments specifically targets the data center market, indicating a move to build a programmatic pipeline of projects rather than one-off deals. This structure is essential for attracting institutional capital.

Larger Power Units Require More Redundancy

This chart illustrates a fundamental engineering and financial challenge directly relevant to the large-scale projects enabled by major partnerships, such as the 100 MW Inuverse MOU. It speaks to the complexities involved in executing such a deal.

(Source: SemiAnalysis)

Table: Strategic Partnerships and Alliances

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fuel Cell Energy / SDCL | January 2026 | Announced a partnership to explore 450 MW in fuel cell deployments, targeting the data center market with a focus on creating a large-scale project pipeline. | Yahoo Finance |

| Fuel Cell Energy / Inuverse | July 2025 | Signed an MOU to explore deploying up to 100 MW of fuel cell power for hyperscale data centers in South Korea, signaling international expansion into grid-constrained regions. | Fuel Cell Energy Investors |

| Microsoft / Caterpillar | Ongoing (2022-Present) | Collaborating on a 3 MW hydrogen fuel cell demonstration to validate the technology for providing over 48 hours of continuous backup power for large data centers. | Introl |

US vs. South Korea, Fuel Cell Energy Geographic Focus

The United States is the primary market for fuel cell-powered data centers, driven by the sheer scale of its AI-driven power demand and severe grid interconnection delays. However, international markets like South Korea are emerging as key growth areas where similar power constraints and industrial policy create strong demand signals.

- The U.S. is the epicenter of the trend, where utilities are forecasting unprecedented load growth. Data center power consumption is projected to grow from approximately 30 GW in 2025 to 90 GW by 2030. Grid interconnection queues can exceed five years, making on-site generation a necessity, not an option.

- Activity is concentrated in established data center hubs and new regions with available land and natural gas infrastructure. Bloom Energy‘s project in Wyoming is an example of developing data centers in new locations by bringing power generation on-site.

- South Korea represents a key international growth market. The Fuel Cell Energy and Inuverse MOU for 100 MW highlights how the same grid constraints plaguing the U.S. are creating opportunities for fuel cell deployments in other technologically advanced, power-dense nations.

Texas Grid Overwhelmed by New Power Demand

This chart provides a specific, compelling example of grid instability in the US, a key market for Fuel Cell Energy. It effectively illustrates the market driver behind the company’s geographic focus in the US over other regions.

(Source: SemiAnalysis)

Technology Maturity for Hydrogen Fuel Cells as Baseload Power

The core SOFC technology is commercially mature for providing high-efficiency baseload power, but the ecosystem required for a fully green hydrogen-powered data center remains in its infancy. The critical shift is the market’s acceptance of natural gas as a pragmatic bridge fuel, separating the deployment of the fuel cell asset from the maturation of the green hydrogen supply chain.

- Between 2021 and 2024, technology validation focused on the fuel cell’s ability to run on pure hydrogen for backup power, as demonstrated by Microsoft. This proved technical feasibility but tied its fate to a non-existent hydrogen supply chain.

- The period from 2025 to today is defined by a pragmatic commercial model. Fuel cell providers are selling fuel-flexible SOFCs that can run on natural gas now with over 60% electrical efficiency, far surpassing traditional generators, and switch to hydrogen later.

- The primary technological and logistical hurdle remains the green hydrogen value chain. A 2025 wave of project cancellations and downward revisions of 2030 production forecasts by the IEA confirmed that a large-scale, cost-effective green hydrogen supply is still years away.

- This reality validates the “natural gas now, hydrogen later” strategy. It allows data center operators to solve their immediate power crisis while retaining a credible path to future decarbonization, satisfying both operational needs and corporate ESG goals.

Data Center Onsite Power Adoption to Reach 50% by 2035

The projected adoption rate of on-site power is a key indicator of market acceptance and technology maturity, making this chart a perfect illustration for a section discussing the readiness of fuel cells for baseload power.

(Source: Energy Industry Insights from Avanza Energy – Substack)

SWOT Analysis of Fuel Cell Energy’s Data Center Strategy

The strategic position of fuel cells for data centers has strengthened considerably, as acute grid constraints have transformed their value proposition from a clean backup alternative into a mission-critical enabler for industry growth. The analysis below shows how market forces have amplified strengths and created new opportunities, while the core weakness has been pragmatically addressed.

Gas Engine Orders for Data Centers Surge

The rise of a competing technology like gas engines represents a direct and significant ‘Threat’ in the market. This is a critical data point for a SWOT analysis of Fuel Cell Energy’s specific data center strategy.

(Source: Energy Industry Insights from Avanza Energy – Substack)

Table: SWOT Analysis for Hydrogen Fuel Cells as Data Center Primary Power

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | High reliability and zero on-site emissions for backup power applications. | High electrical efficiency (>60%) and fuel flexibility for baseload power on natural gas. | The value proposition shifted from clean backup to efficient, grid-independent primary power, a much larger market. |

| Weakness | High dependency on a non-existent, expensive green hydrogen supply chain. | Reliance on natural gas as a bridge fuel, creating stranded asset risk and continued emissions. | The market accepted natural gas as a necessary bridge, making the business case viable today instead of waiting for a future hydrogen economy. |

| Opportunity | Corporate ESG goals and diesel displacement mandates created a pull for clean backup. | Severe grid constraints and 5+ year interconnection queues make on-site generation a necessity for new data center builds. | The market driver evolved from a “nice-to-have” sustainability goal to a “must-have” solution for a crippling infrastructure bottleneck. |

| Threat | Uncertainty over long-term policy support for hydrogen. | Green hydrogen project cancellations and supply chain immaturity reinforce reliance on volatile natural gas markets. | Policy like the IRA firmed up, but the physical supply chain risk for hydrogen became more pronounced, validating the natural gas-first strategy. |

Data Centers Drive 833% Spike in Grid Costs

This chart perfectly illustrates the core ‘Opportunity’ in a SWOT analysis. The massive strain data centers place on the grid is the primary problem that hydrogen fuel cells as a primary power source are positioned to solve.

(Source: Energy Industry Insights from Avanza Energy – Substack)

Scenario Modelling, Fuel Cell Energy 100 MW Inuverse MOU

The critical path for scaling fuel cells as baseload power for data centers through 2027 depends entirely on the successful execution of the “natural gas now, hydrogen later” strategy. The primary signal to monitor is the conversion of large MOUs, like the Fuel Cell Energy/Inuverse agreement, into firm, financed projects with secured natural gas supply agreements.

- If these multi-hundred-megawatt projects reach final investment decision (FID) and begin construction, it will validate the commercial model and unlock a significant project pipeline. Watch for announcements of long-term power purchase agreements (PPAs) between fuel cell providers and data center operators.

- Conversely, if these large MOUs stall due to challenges in project financing or securing natural gas access, it would signal that even the bridge strategy faces significant implementation hurdles. This would slow the transition and force data center developers to pursue other, potentially less clean, on-site power solutions.

- A leading indicator of success will be the ability of Bloom Energy and Fuel Cell Energy to report a growing backlog of firm orders specifically for baseload data center applications, moving beyond pilot projects to a repeatable, scalable business model.

Stationary Fuel Cell Market Growth Projected

This chart’s macro-level projection of market growth provides a foundational assumption for any scenario model, lending credibility and context to the specific 100 MW MOU analysis.

(Source: Global Market Insights)

The questions your competitors are already asking

This report covers one angle of the commercial shift making fuel cells a primary power source for data centers. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the fuel cell market for data center primary power?

- Fuel Cell Energy activities in data centers. Is the 100 MW Inuverse MOU progressing from agreement to deployment?

- What is the outlook for SOFC deployment as primary power in AI data centers by 2026?

- Which data center operators are adopting on-site SOFCs for baseload power to bypass grid constraints?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.