CCUS Industrial Decarbonization, Denmark’s $2.6 B Aalborg Portland Subsidy for 1.25 Mtpa over 15 Years (2021 to 2026)

CCUS Projects Shift from Pilots to Commercial Scale with Government Backing

The carbon capture market is decisively shifting from small-scale pilots to multi-billion-dollar commercial execution, driven by direct government industrial policy designed to de-risk first-of-a-kind projects. The landmark $2.6 billion, 15-year subsidy for Aalborg Portland is the definitive signal that market-based carbon pricing alone is insufficient for heavy industry, requiring long-term contracts to bridge the economic viability gap.

- Between 2021 and 2024, the industry focused on proving technical feasibility and securing early-stage funding. The global project pipeline grew substantially, reaching 244 Mtpa of capacity in development by 2022, but many projects remained stalled awaiting a bankable revenue model beyond volatile carbon market prices.

- The period from 2025 to 2026 marks a turning point where governments have stepped in as the primary financial enablers. Denmark’s contract with Aalborg Portland, finalized in June 2026, provides a fixed payment of approximately $135 per ton of CO 2. This structure is modeled on the successful Contracts for Difference (Cf D) used to scale the offshore wind industry.

- This new model moves beyond tax credits or small grants, offering the long-term revenue certainty needed for a Final Investment Decision (FID) on capital-intensive infrastructure. It validates the core thesis that for hard-to-abate sectors like cement, direct procurement of decarbonization services is the critical enabler for projects to proceed from planning to construction.

- While point-source capture from industry advances, Direct Air Capture (DAC) relies on corporate offtake agreements from buyers like Microsoft and Amazon to secure financing, demonstrating a parallel private-sector-led offtake model for carbon dioxide removal technologies.

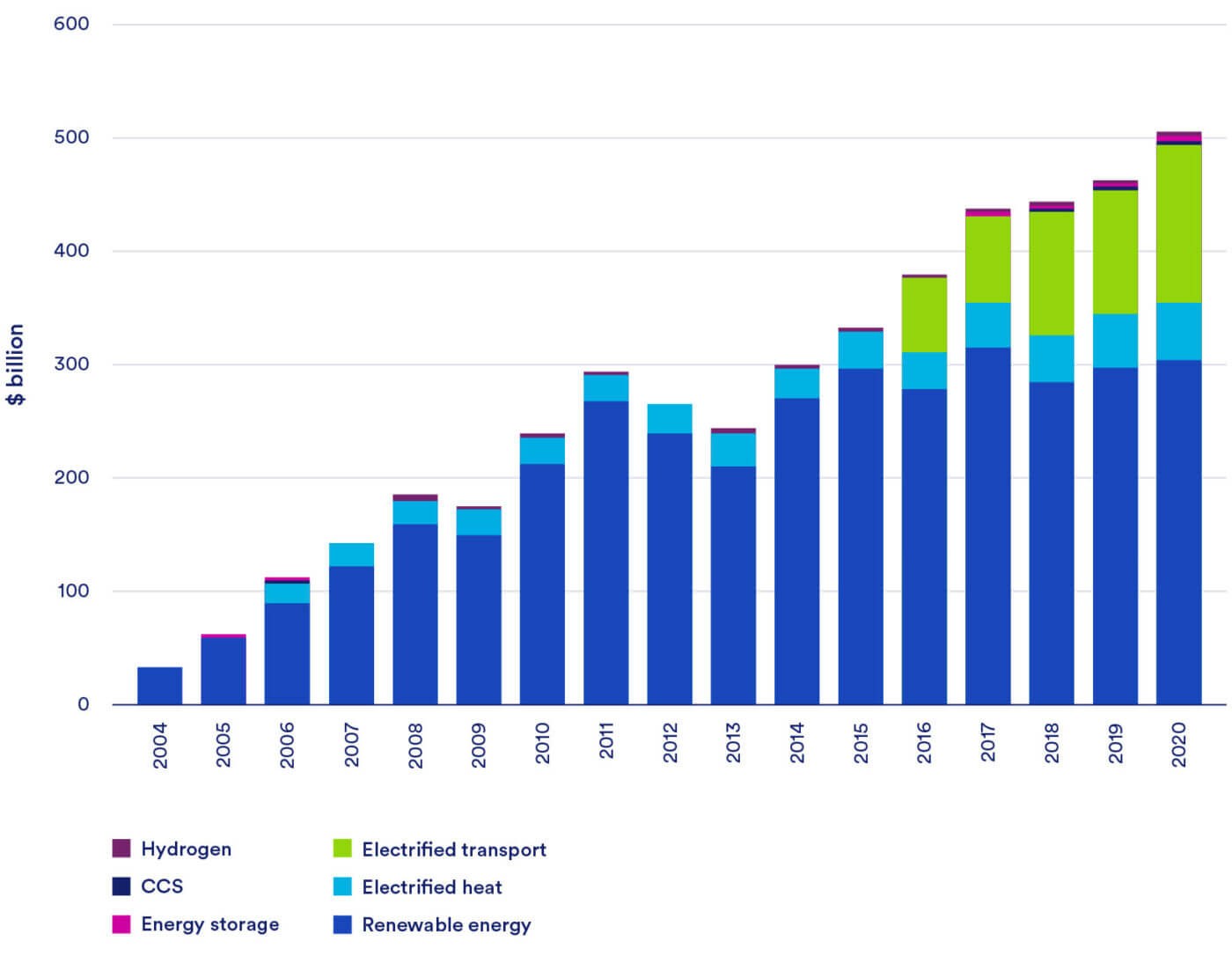

CCS Investment Trails Broader Clean Energy Boom

This chart provides the high-level context for the section’s topic. It illustrates that investment in Carbon Capture and Storage (CCS) has lagged behind the broader boom in clean energy investment. This data directly supports the section’s narrative that government backing is essential for CCUS projects to progress from pilot stages to commercial scale, as market-based investment alone has been insufficient to drive the sector forward at the required pace.

(Source: Clean Air Task Force)

$2.6 B Danish Subsidy Anchors a New Wave of Policy-Driven CCUS Investment

Massive, direct government funding has become the primary catalyst for large-scale CCUS deployment, with multi-billion-dollar programs in Europe and North America creating the financial certainty required to underwrite high capital expenditures. These policy mechanisms are designed to close the gap between the high cost of capture and the revenue available from compliance carbon markets like the EU ETS, which traded around $75 per ton in 2025.

- Denmark’s $2.6 billion contract for the ACCSION project is a direct subsidy that guarantees a fixed price for captured CO 2 over 15 years, effectively removing market risk for Aalborg Portland and its parent company, Cementir Holding.

- The United States’ Inflation Reduction Act (IRA) created a different but equally powerful incentive through the enhanced 45 Q tax credit, offering up to $85 per ton for CO 2 permanently stored from industrial sources. This has spurred a wave of project announcements across the country.

- The UK government has also committed up to £20 billion ($25 billion) for CCUS deployment, creating investable models for industrial clusters on its east coast and in other industrial heartlands.

- These large-scale government commitments are a primary driver for the CCUS market, which is forecast by various analysts to grow from approximately $5-8 billion in 2025 to over $15-30 billion by the mid-2030 s, underpinned almost entirely by such policy support.

Table: Global Carbon Management Policy and Investment Mechanisms

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Aalborg Portland Subsidy | 2026 – 2045 | Provides up to $2.6 billion ($135/ton) via a 15-year Contract for Difference to capture 1.25 Mtpa of CO 2 from a cement plant. The purpose is to de-risk a first-of-a-kind industrial project and meet national climate targets. | Reuters |

| United States 45 Q Tax Credit | 2022 – 2032+ | Offers up to $85/ton as a tax credit for sequestered CO 2 from industrial and power sources. The purpose is to stimulate private investment across a wide range of CCUS applications. | EFI Foundation |

| United Kingdom CCUS Program | 2023 – 2030+ | Commits up to £20 billion ($25 billion) to support the development of industrial CCUS clusters, focusing on shared transport and storage infrastructure to create economies of scale. | Carbon Geo Capture |

| EU Innovation Fund | Ongoing | A major funding instrument for innovative low-carbon technologies. The ACCSION project itself received an additional ~$230 million grant from this fund in March 2025 for its innovative nature. | INNO-CCUS |

Europe vs. North America: Aalborg Portland Highlights Diverging Policy Models

Europe and North America are establishing themselves as the two leading geographies for CCUS deployment, but they are pursuing distinct industrial policy models to stimulate investment. Europe, led by countries like Denmark, is favoring direct, long-term offtake contracts, while the U.S. relies on a broader, tax-based incentive system.

- Between 2021 and 2024, both regions saw a rapid expansion of their project pipelines, but activity in Europe was often linked to developing integrated hubs (e.g., Port of Rotterdam, Norwegian North Sea), whereas U.S. development was more fragmented ahead of the IRA’s implementation.

- The period from 2025 to today has clarified these regional strategies. Denmark’s deal with Aalborg Portland exemplifies the European “Cf D model, ” where the government acts as a direct buyer of decarbonization services to guarantee revenue for a specific, strategic national project. This provides maximum certainty but is highly targeted.

- In contrast, the U.S. 45 Q tax credit acts as a technology-neutral, market-wide incentive available to any qualifying project. This has encouraged a broader range of developments, particularly in areas with favorable geology and industrial concentrations like the Gulf Coast.

- Canada is pursuing a hybrid approach, combining an investment tax credit that covers up to 50% of CAPEX with provincial carbon pricing systems, attracting companies like Deep Sky. The success of each region’s model will depend on its ability to drive down costs and build out shared midstream CO 2 transport and storage infrastructure.

Commercial Scale Confirmed: Aalborg Portland Validates Post-Combustion Capture

The Aalborg Portland deal confirms that amine-based, post-combustion capture technology is considered technically mature and ready for full-scale industrial deployment (TRL 8-9), but its economic viability remains entirely dependent on external financial support. The primary barrier to adoption is not technology but the high cost of capture in flue gas streams with low CO 2 concentrations, such as in cement manufacturing.

- From 2021 to 2024, the industry narrative focused on the high costs and energy penalties of capture, with many pilot projects demonstrating feasibility but failing to scale due to unfavorable economics. Cost estimates for cement CCUS varied widely, from $50 to over $200 per ton.

- The $2.6 billion subsidy in 2026 serves as a definitive validation point. By awarding a contract at $135/ton, the Danish government implicitly accepts this cost level as the current price of decarbonizing cement and chooses to pay it directly to achieve its climate goals.

- This contrasts with industries like ethanol or ammonia production, where high-purity CO 2 streams allow for much lower capture costs (often below $35/ton), making projects in those sectors viable with lower incentives like the U.S. 45 Q credit alone.

- The key takeaway is that the technology for capturing CO 2 from cement is “ready, ” but the business case is not. The Aalborg Portland deal proves that with sufficient policy support, execution can begin immediately, shifting the critical bottleneck from capture technology to the build-out of CO 2 transport and storage networks.

SWOT Analysis: Aalborg Portland CCUS Project and Market Implications

The Aalborg Portland project represents a pivotal execution of industrial decarbonization policy, with its strengths rooted in government backing and its primary risks tied to long-term economic sustainability and execution complexity. Its success or failure will send strong signals to Carbon Capture & DAC Leaders and policymakers globally.

- Strengths: The project’s greatest strength is the 15-year, inflation-indexed government contract, which eliminates market price risk and makes the project bankable.

- Weaknesses: The primary weakness is its complete dependence on the subsidy, creating a “subsidy cliff” in 2045 when its viability will depend on a sufficiently high market price for carbon.

- Opportunities: It provides Aalborg Portland with a powerful first-mover advantage in the emerging market for low-carbon building materials and catalyzes the development of a shared CO 2 infrastructure value chain in the North Sea.

- Threats: Significant threats include project execution risks such as construction delays and cost overruns, as well as the risk that the broader CO 2 transport and storage infrastructure is not developed on time.

Table: SWOT Analysis for the Aalborg Portland CCUS Subsidy Model

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | Technology readiness of post-combustion capture was demonstrated in pilots (e.g., Heidelberg Materials‘ Brevik project). | Massive, long-term government financial backing ($2.6 B over 15 years) is confirmed, making a full-scale project bankable. | The key strength shifted from technical feasibility to financial certainty. The Danish government’s contract provides a de-risking model for the entire industry. |

| Weakness | Extremely high cost of capture for cement (est. $50-$200/ton) made projects non-viable with existing carbon prices (EU ETS). | The “subsidy cliff” becomes a defined risk. The project’s economics are unsecured after the 15-year contract term expires in 2045. | The financial weakness was solved for the short-to-medium term but institutionalized as a long-term structural risk dependent on future carbon prices. |

| Opportunity | Potential for “green cement” markets and creating industrial clusters around shared CO 2 infrastructure was largely theoretical. | The project creates a concrete path for Aalborg Portland to become a premium supplier of low-carbon cement and anchors a new CO 2 value chain in Denmark. | The opportunity moved from a conceptual strategy to an executable business plan, with a clear first-mover advantage established by the subsidy. |

| Threat | The primary threat was the lack of a viable business model, leading to project cancellations and a stalled pipeline. | The threat shifts from financing to execution. Major risks now include construction delays, cost overruns, and failure to meet the 1.25 Mtpa capture target. | The core threat evolved from “Can we finance it?” to “Can we build and operate it on time and on budget?” The project is now exposed to physical and operational risks. |

Aalborg Portland’s FID is the Next Catalyst for European CCUS

The most critical signal to watch in the coming year is the Final Investment Decision (FID) for the ACCSION project by Aalborg Portland‘s parent company, Cementir. This decision will be the definitive confirmation that the government subsidy model has successfully translated policy into action, triggering a new phase of project execution and competitive response across Europe’s industrial sector.

- If an FID is announced in late 2026 or early 2027, watch for other European governments, particularly Germany and France, to accelerate their own industrial decarbonization tenders to prevent their national champions like Heidelberg Materials from falling behind.

- This could be happening: A race to secure CO 2 storage capacity in the North Sea. With multiple large-scale capture projects now moving toward execution, the availability and cost of transport and storage will become the next major bottleneck. Monitor investments in CO 2 shipping, pipeline projects, and storage site licensing.

- Watch this signal: Competitor responses from other cement majors. The Aalborg Portland deal puts pressure on competitors to finalize their own large-scale decarbonization plans, potentially leading to a new wave of major CCUS project announcements in 2027.

The questions your competitors are already asking

This report covers one angle of financing commercial-scale industrial decarbonization. The questions that matter most depend on your work.

- What is actually happening with the Aalborg Portland carbon capture project since the $2.6 billion subsidy was finalized?

- What is the outlook for CCUS deployment in the European cement sector by 2030, following Denmark’s subsidy model?

- Which other European cement operators are adopting large-scale point-source capture, and what funding models are they pursuing?

- What is the full cost breakdown for a large-scale cement CCUS project beyond the ~$135/ton subsidy?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.