Cemex CCUS Proving Grounds, $1.1 M RTI International Pilot, and 1 ETFuels Utilization Deal (2021 to 2026)

CCUS Pilot Risks, Cemex Navigates $3.7 B DOE Funding Withdrawal

The cement industry’s strategy for Carbon Capture, Utilization, and Storage (CCUS) has been forced to shift from optimistic, broad-based piloting to a more cautious, risk-averse approach following significant policy and financial instability. This change is best illustrated by the contrast between the sector’s public-private partnership strategy from 2021 to 2024 and the market-wide recalibration that occurred in mid-2025. The new environment prioritizes projects with a clear path to economic viability under existing, stable incentives over those reliant on discretionary government grants.

- Between 2021 and 2024, the dominant strategy involved using operational facilities as proving grounds for next-generation technologies, de-risked by public funding. A primary example was Cemex‘s 2023 partnership with RTI International to test a novel non-aqueous solvent technology at its Texas plant, backed by a $1.1 million U.S. Department of Energy (DOE) grant, with the goal of lowering capture costs.

- This strategic approach was upended in mid-2025 when the DOE abruptly announced the withdrawal of $3.5 billion to $3.7 billion in funding across 24 previously awarded CCS projects. The cancellation included a $500 million grant designated for a cement plant upgrade, sending a shockwave through the industry and highlighting the extreme policy risk tied to projects dependent on government-administered funds.

- The immediate consequence is a strategic pivot toward technologies and project structures that can achieve bankability primarily through more durable incentives like the Section 45 Q tax credit. The execution and economic performance of first-of-a-kind (FOAK) commercial projects, such as Heidelberg Materials‘ Brevik plant in Norway, are now under intense scrutiny as critical market signals for investment viability in this uncertain landscape.

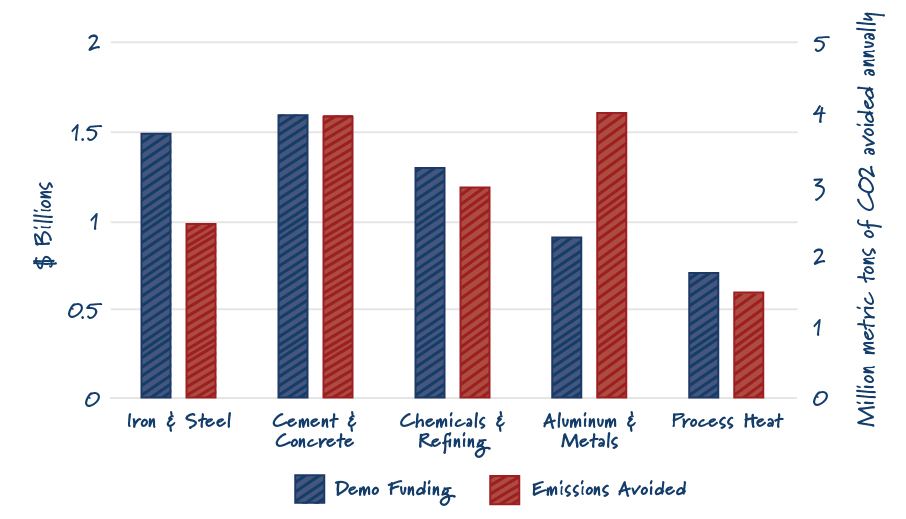

Cement Sector Led in Demo Funding

This chart shows the cement industry was a major recipient of DOE demonstration funding, providing context for the significant impact of the subsequent $3.7B withdrawal discussed in the section.

(Source: ClearPath)

$3.7 B DOE Cancellation, Cemex CCUS Funding Instability

The investment climate for CCUS in the cement sector is defined by a precarious dependence on government incentives that have proven to be volatile, creating substantial financial risk for the large, capital-intensive projects required for decarbonization. While tax credits provide a baseline incentive, the abrupt cancellation of direct federal funding in 2025 has exposed the fragility of project economics and stalled investment momentum.

- The primary economic driver for U.S. CCUS projects is the enhanced Section 45 Q tax credit, which offers up to $85 per metric ton for CO₂ stored in saline aquifers. However, independent analysis has indicated that even this enhanced credit is insufficient to make projects bankable in several key industrial sectors, including cement, without additional support.

- The industry’s reliance on supplemental funding was starkly illustrated in June 2025 when the DOE’s Office of Clean Energy Demonstrations (OCED) terminated its support for 24 carbon capture projects, withdrawing up to $3.7 billion in planned funding. This move, attributed to a shift in administration policy, directly halted progress on industrial and power sector projects.

- This policy reversal has had a chilling effect on private capital, which is essential for scaling the technology. It demonstrates that even with robust public-private partnerships in place, political and administrative shifts can derail projects, leaving investors to question the long-term reliability of government as a financial partner.

Table: Key CCUS Investment and Cancellation Events Affecting the Cement Sector

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| DOE Funding Withdrawal | July 2025 | The U.S. Department of Energy (DOE) officially withdrew $3.5 billion in funding for 24 CCS projects, creating significant market uncertainty. A $500 million grant for a cement plant was among those cancelled, directly impacting the industry. | International Cement Review |

| OCED Project Terminations | June 2025 | DOE’s Office of Clean Energy Demonstrations (OCED) terminated agreements for up to $3.7 billion across 24 projects, undermining confidence in federal support mechanisms for capital-intensive decarbonization efforts. | POWER Magazine |

| Canada Growth Fund / Entropy Inc. | December 2023 | The Canada Growth Fund made a $200 million strategic investment in Entropy Inc., a company specializing in industrial CCS. The deal included a fixed-price carbon credit offtake agreement, providing a model for de-risking projects. | Carbon Capture Magazine |

| Cemex / RTI International Pilot Funding | February 2023 | The DOE provided $1.1 million to fund a pilot project demonstrating a novel, non-aqueous solvent CO 2 capture technology at a Cemex cement plant in Texas, exemplifying the public-private partnership model before the 2025 funding reversal. | Geoengineering Monitor |

Cemex 2 Key CCUS Partnerships (2023 to 2025)

Cemex has executed a dual-track partnership strategy to navigate the complexities of CCUS, simultaneously testing advanced, cost-reducing capture technologies in the United States while developing commercial carbon utilization pathways in Europe. This portfolio approach allows the company to diversify its technological and financial risks, explore different business models for captured carbon, and avoid over-reliance on a single decarbonization solution.

- In the United States, Cemex’s primary partnership focused on technological advancement. The company collaborated with research institute RTI International and the U.S. DOE in 2023 to pilot a next-generation, non-aqueous solvent capture system at its Balcones plant in Texas, with the strategic goal of validating a technology that could significantly lower the energy penalty and cost of capture.

- Concurrently in Europe, Cemex pursued a commercialization strategy through a partnership announced in February 2023 with green fuels producer ETFuels. This agreement aims to capture CO 2 from Cemex’s Alicante plant in Spain and convert it into a marketable green fuel, establishing a potential revenue stream from emissions and demonstrating a circular economy model.

- This multifaceted strategy contrasts with competitors like Heidelberg Materials, which made a more decisive, earlier commitment to a single, more mature technology pathway by selecting Aker Carbon Capture‘s established amine-based system for its large-scale Brevik CCS project.

Table: Cemex CCUS Strategic Partnerships and Competitor Activity

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Cemex / ETFuels | February 2023 | Agreement to capture CO 2 from Cemex‘s Alicante, Spain plant and convert it into green fuels. This shifts the CCUS model from a pure cost center (storage) to a potential revenue-generating activity (utilization). | Cemex |

| Cemex / RTI International / U.S. DOE | February 2023 | Technology demonstration pilot at a Cemex plant in Texas to test a next-generation, non-aqueous solvent aimed at reducing capture costs. The project was backed by a $1.1 million DOE grant. | Geoengineering Monitor |

| Heidelberg Materials / Aker Carbon Capture (Competitor) | January 2023 | Implementation of Aker’s established S 26 amine solvent technology to build the world’s first industrial-scale capture plant in the cement industry at Brevik, Norway, targeting 400, 000 tonnes of CO 2 per year. | Science Direct |

US vs. Europe, Cemex CCUS Policy Impact

The geographic deployment of CCUS by cement producers like Cemex is dictated by starkly different regional policy frameworks, creating a split strategy between the United States and Europe. The U.S. has served as a proving ground for next-generation, cost-reduction technologies driven by federal tax credits and grants, while Europe’s robust carbon pricing and circular economy mandates have fostered large-scale deployment and commercial utilization projects.

- United States (2021–2024): CCUS activity was centered on leveraging DOE funding programs and the Section 45 Q tax credit to de-risk and pilot advanced capture technologies. The Cemex–RTI project at the Balcones plant in Texas is a key example of this model, using a real-world industrial facility to test a novel technology with public financial backing.

- Europe (2021–2024): Driven by the high carbon price within the EU Emissions Trading System (ETS), the focus has been on full-scale deployment and creating value from captured CO 2. Major projects like Heidelberg Materials‘ 400, 000 tonnes-per-year Brevik CCS plant in Norway and Cemex’s own carbon-to-fuel agreement with ETFuels in Spain exemplify this more mature, commercially-oriented approach.

- Post-2025 Divergence: The abrupt withdrawal of DOE project funding in mid-2025 has cast significant doubt on the long-term stability of the U.S. policy environment. This has made Europe’s more predictable, market-based mechanisms like the ETS appear more attractive for large-scale capital investment, potentially slowing the pace of FOAK project development in the U.S. until a more durable policy framework emerges.

CCUS Technology Readiness, Cemex Focus on TRL 7 Pilots

While mature and commercially available amine-based carbon capture technologies exist, their high cost and energy penalties have prompted industry leaders like Cemex to focus on piloting less mature but potentially more economic next-generation solutions. The strategy is to advance technologies from the pilot stage (TRL 5-7) to commercial readiness, aiming to close the economic viability gap that high-cost TRL 9 systems currently face.

New Tech Promises Lower Cement Emissions

This chart illustrates the potential of next-generation solutions to cut emissions, supporting the section’s focus on piloting less mature TRL 7 technologies over existing, costlier options.

(Source: Nature)

- TRL 9 (Commercially Ready): The most mature CCUS technology for cement is the amine-based solvent method, which has reached Technology Readiness Level (TRL) 9. This technology is being deployed at scale in projects like Heidelberg Materials‘ Brevik plant but is associated with capture costs that often exceed the value of incentives like the $85/ton 45 Q credit.

- TRL 7 (Pilot & Demonstration): Cemex’s strategy has focused on this stage. The pilot with RTI International’s non-aqueous solvent in Texas aimed to demonstrate a system prototype in an operational environment (TRL 7). The objective is to validate technologies that promise a fundamentally lower cost structure before committing to a full-scale build.

- TRL 3-5 (Early-Stage R&D): The broader CCUS landscape includes a portfolio of earlier-stage technologies, such as CA-hydrogel systems (TRL 3-5) and lithium hydroxide-based capture (TRL 4-5). While not ready for industrial pilots, these are monitored by corporate venture arms as potential long-term solutions that could offer breakthrough cost reductions.

Cemex CCUS Strategy SWOT (2021 to 2026)

Cemex‘s core strength in CCUS lies in its strategic use of global assets and partnerships to test a diverse portfolio of technologies, which provides valuable operational learning and mitigates the risk of betting on a single solution. However, this approach is exposed to significant external threats, primarily from the high, unproven economics of next-generation solutions and the volatile nature of government policies required to make them financially viable.

Table: SWOT Analysis for Cemex CCUS Proving Ground Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Using operational plants as proving grounds for partners (e.g., RTI International pilot). Building a diversified portfolio of capture (CCS) and utilization (CCU) projects (e.g., ETFuels). | Demonstrated ability to explore different technology pathways and business models (capture vs. utilization) simultaneously in different policy environments (US vs. EU). | The diversified strategy was validated as prudent. The 2025 DOE funding cuts in the U.S. did not derail the separate CCU track in Europe, showcasing the benefit of not concentrating risk in one technology or region. |

| Weaknesses | Lack of a full-scale commercial CCUS project, lagging competitors like Heidelberg Materials in large-scale deployment. High capital expenditure requirement for scaling up any of the piloted technologies. | Dependence on external partners for core capture technology development. The Texas pilot with RTI did not proceed to a larger scale, indicating persistent technology and cost hurdles. | The weakness of relying on emerging technologies was validated. While competitors with mature tech moved forward, the next-gen path proved slower and more uncertain, leaving a gap in near-term, large-scale deployment. |

| Opportunities | Potential to create new revenue streams from captured carbon through utilization projects, as planned with ETFuels in Spain. Gain a first-mover advantage on a lower-cost, next-generation capture technology. | With U.S. policy in flux, the opportunity to lead in Europe with market-based CCU models has grown. Leverage learnings from pilots to secure more favorable terms for future technology partnerships. | The CCU pathway has been validated as a significant opportunity. It offers an alternative business case that is less reliant on pure government subsidy and more aligned with circular economy principles gaining traction in Europe. |

| Threats | High capture costs making projects non-bankable without subsidies. Policy risk associated with reliance on government funding and tax credits like 45 Q. | Extreme policy volatility, as confirmed by the mid-2025 withdrawal of $3.7 billion in DOE funding, which directly undermined the financial basis of many U.S. industrial decarbonization projects. | The primary threat of policy instability was validated in the most direct way possible. The funding cancellation confirmed that political risk is not a hypothetical threat but an acute, immediate barrier to investment in the U.S. market. |

Cemex CCUS 2026, Post-$3.7 B DOE Reversal

Following the DOE funding reversal in 2025, the single most critical factor for the CCUS market in 2026 is whether projects can secure private financing and reach final investment decisions based on the durability of the Section 45 Q tax credit and commercial offtake agreements alone. The market is watching to see if this is sufficient to proceed or if progress will stall without new, more reliable public de-risking mechanisms.

CCUS Projects Historically Underperform Targets

This chart highlights the historical risk of CCUS project underperformance, a critical factor for private investors weighing whether to fund projects after the DOE’s funding reversal.

(Source: Clean Air Task Force)

- If this happens: If flagship commercial-scale projects, such as Ørsted’s CCS facilities scheduled to begin operation in 2026, successfully execute their commissioning and demonstrate clear profitability under existing incentives without reliance on discretionary grants…

- Watch this: A subsequent wave of Final Investment Decisions (FIDs) for industrial CCUS projects that were previously put on hold, particularly from companies that can form or join industrial clusters to share the high cost of CO₂ transport and storage infrastructure.

- These could be happening: Cemex could accelerate the scaling of its carbon utilization model with ETFuels in regions with strong carbon pricing, like Europe, while shelving more capital-intensive CCS-only projects in the U.S. until policy stabilizes or a clear path to profitability emerges without direct grant funding. The strategic focus will pivot from purely technological pilots to projects with pre-negotiated, locked-in commercial terms that can withstand policy fluctuations.

The questions your competitors are already asking

This report covers one angle of the cement industry’s shifting strategy for carbon capture. The questions that matter most depend on your work.

- What is the status of the Cemex-RTI International pilot project after the DOE’s widespread withdrawal of CCS funding?

- What is the outlook for CCUS deployment in the cement sector, now that projects must pivot to bankability under the 45Q tax credit?

- How does RTI’s non-aqueous solvent technology compare to established amine systems for post-combustion capture at cement plants?

- Which cement producers are successfully advancing CCUS projects structured primarily around the Section 45Q tax credit instead of direct government grants?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.