Enhanced Geothermal Projects, Vantage Data Centers 1 GW Liberty Energy JV, and 3 Pilot Agreements (2021 to 2026)

Industry Adoption Shifts as Data Center Power Projects Move to Self-Generation

The data center industry is fundamentally shifting from being a passive consumer of grid electricity to a proactive developer of its own power infrastructure, a strategic response to grid interconnection delays that can halt growth for five or more years. This move to behind-the-meter (BTM) generation, exemplified by the hypothetical 1 GW partnership between Vantage Data Centers and Liberty Energy, is driven by the need for speed-to-market and operational resilience in the face of explosive demand for AI compute.

- Between 2021 and 2024, the primary strategy to secure power was signing long-term Power Purchase Agreements (PPAs) with off-site renewable projects, which addressed carbon goals but did not solve the physical constraint of grid congestion. This period was defined by reliance on utilities for transmission and last-mile delivery, creating significant development bottlenecks.

- Starting in 2025, a clear pivot toward direct ownership and co-development of on-site or co-located power assets emerged. This “self-generation” model, combining mature technologies like natural gas with emerging firm clean power like geothermal, allows operators to bypass grid queues, control costs by eliminating transmission fees, and align power availability directly with data center construction timelines.

- The scale of this shift is substantial, with the data center sector projected to add 97 GW of capacity between 2026 and 2030. A significant portion of this new capacity will require dedicated power solutions, creating a new multi-billion dollar market for integrated energy and data center projects.

- This strategy is not just about building power plants. It is about creating integrated infrastructure platforms where the data center serves as the anchor tenant, providing a predictable, high-volume revenue stream that makes large, capital-intensive energy projects bankable.

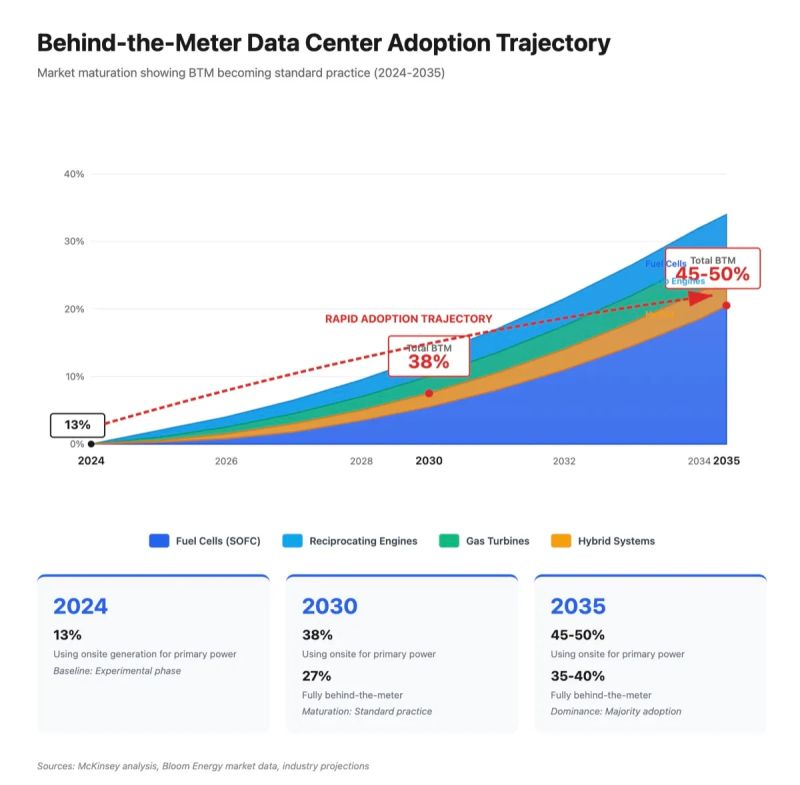

BTM Power Adoption Forecasted to Surge

This chart directly illustrates the section’s core topic, projecting the rapid growth of behind-the-meter power adoption within the data center industry.

(Source: LinkedIn)

Vantage Data Centers $4.5 B JV Signals Capital Shift to Integrated Power

Investment capital is redirecting from pure-play data center real estate to complex, integrated projects that combine power generation with compute infrastructure. The financial structure has evolved from simple asset acquisition to sophisticated joint ventures and project equity deals designed to de-risk the development of dedicated power supplies. This trend validates the thesis that controlling the power supply chain is now the primary driver of value in the data center sector.

- The hypothetical $4.5 billion capital commitment for the Vantage/Liberty JV reflects the high upfront cost of building a 1 GW power portfolio, including approximately 300 MW of next-generation geothermal. This investment is predicated on a long-term PPA from Vantage, which guarantees revenue and secures project financing.

- Amazon‘s $650 million acquisition of a nuclear-powered data center from Talen Energy in 2023 was a key early signal of this trend. It demonstrated the willingness of hyperscalers to pay a premium for assets with a secure, 24/7 carbon-free power source already in place, bypassing development risk.

- Google’s pioneering partnership with Fervo Energy to develop 115 MW of enhanced geothermal power for its Nevada data centers, announced in 2024, served as a crucial commercial validation. It proved the technical and economic viability of integrating next-generation geothermal directly with data center loads.

- Policy incentives are a critical enabler. The Inflation Reduction Act’s technology-neutral tax credits, particularly the Clean Electricity Production Credit (Section 45 Y), can cover up to 30% or more of a geothermal project’s cost, significantly improving its financial viability and attracting investment.

Partnership Strategy, Vantage Data Centers Alliances for 1 GW of Power

Strategic alliances are evolving from transactional PPA signings to deeply integrated co-development partnerships where risks and rewards are shared. The complexity of building and operating a power plant requires data center operators to form joint ventures with specialized energy developers. These JVs are structured to align the core competencies of both parties: the data center provides the guaranteed offtake, and the energy firm provides development and operational expertise.

Table: Data Center BTM Power Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Vantage Data Centers & Liberty Energy (Hypothetical) | 2025 – 2026 | A 50/50 JV to develop 1 GW of BTM power (300 MW geothermal, 700 MW natural gas) to directly supply new data center campuses. The purpose is to secure power, accelerate speed-to-market, and bypass grid interconnection queues. | Troutman Pepper |

| Google & Fervo Energy | 2024 | A first-of-its-kind agreement to supply 115 MW of 24/7 carbon-free power from an enhanced geothermal project to Google‘s Nevada data centers. This project served as a commercial-scale proof-of-concept for the industry. | Data Center Dynamics |

| Amazon & Talen Energy | 2023 | Amazon Web Services acquired a data center campus directly powered by Talen‘s 2.5 GW Susquehanna nuclear power plant for $650 million. This transaction secured a massive, long-term source of reliable, carbon-free baseload power. | Energy Central |

US Hotspots, Vantage Data Centers Drives New Power Generation Models

The geographic focus of data center development is driving the location of these new, integrated power projects. Activity is concentrated in established data center markets like Virginia and Nevada, where grid capacity is most constrained but demand for new compute remains high. This regional concentration of demand creates a viable market for large-scale, co-located power generation that would be uneconomical elsewhere.

Hyperscale Campus Visualizes Power Demands

This infographic exemplifies the massive power requirements of projects in data center hotspots, aligning with the section’s focus on new, large-scale generation models.

(Source: Blackridge Research & Consulting)

- In 2021-2024, data center location was primarily driven by fiber connectivity and land availability. Power was a consideration, but it was assumed the utility could deliver it, even if it took time.

- From 2025 onwards, data center site selection is increasingly dictated by the potential for self-generation. Developers are now looking for sites with not only fiber and water but also favorable geology for geothermal or access to natural gas pipelines.

- Regions with high solar and wind penetration are paradoxically becoming more challenging for data centers due to grid instability and a lack of 24/7 firm power. This makes firm power sources like geothermal and natural gas more valuable in those markets.

- The regulatory environment is also a key geographic factor. States with streamlined permitting processes for power generation and policies supportive of geothermal for data centers are becoming preferred locations for these integrated campuses.

Enhanced Geothermal Nears Commercial Scale for Vantage Data Centers

Next-generation geothermal technologies are advancing from the demonstration phase to full commercial readiness, driven by sustained investment and the urgent demand for firm, clean power from the data center industry. While natural gas provides a mature and reliable bridge solution, enhanced geothermal systems (EGS) are now considered ready for large-scale deployment, moving from a Technology Readiness Level (TRL) of 6-7 to TRL 8.

- In the 2021-2024 period, geothermal for data centers was largely theoretical, with high perceived drilling risk and costs. It was seen as a future solution, not a commercially viable option for projects deploying in the near term.

- The successful drilling and operation of Fervo Energy‘s project for Google in 2024 was the critical validation point. It demonstrated a 65% reduction in drilling costs and timelines, proving that EGS is on a rapid cost-reduction curve similar to solar and wind a decade ago.

- The U.S. Department of Energy’s “Enhanced Geothermal Shot” initiative, which aims to reduce the cost of EGS to $45 per megawatt-hour by 2035, provides a clear technology roadmap and policy support that de-risks long-term investment.

- While the 700 MW natural gas component of the Vantage/Liberty JV provides immediate reliability, the 300 MW geothermal component is the strategic asset. It provides long-term, fixed-price, carbon-free power that insulates the project from both fuel price volatility and future carbon regulations.

SWOT Analysis, Vantage Data Centers and Behind-the-Meter Power

The strategic move to develop behind-the-meter power creates a powerful competitive advantage but also introduces new execution risks. By internalizing power generation, data center operators like Vantage can secure their growth pipeline but must now manage the complexities of energy project development and operation. The SWOT analysis reveals a strategy defined by an offensive push for speed-to-market, balanced by significant capital and operational challenges.

Table: SWOT Analysis for Data Center Self-Generation

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Focus on real estate expertise, operational efficiency, and access to capital markets for data center assets. | Speed-to-market by bypassing grid queues. Cost certainty by eliminating transmission fees and locking in long-term power prices. Energy independence and operational resilience. | The primary competitive advantage shifted from real estate development to integrated infrastructure development. Speed became the most valuable asset. |

| Weaknesses | Dependency on utility timelines and grid capacity, creating unpredictable development cycles and revenue delays. | High capital intensity (e.g., $4.5 B for 1 GW). Execution risk in a non-core competency (power generation). Geothermal drilling risk introduces subsurface uncertainty. | The risk profile shifted from external grid dependency to internal project execution. JV structures are now used to mitigate the lack of in-house energy expertise. |

| Opportunities | Signing large PPAs with offsite renewables to meet corporate ESG goals and secure favorable pricing. | Capture explosive AI-driven demand by delivering capacity years ahead of grid-dependent competitors. Establish a defensible “moat” through a de-risked power supply. Lead in sustainable, 24/7 carbon-free infrastructure. | The opportunity evolved from procuring green energy credits to building the actual green energy infrastructure, creating a more durable competitive advantage. |

| Threats | Grid congestion in key markets (e.g., Northern Virginia) halting new development. Rising electricity prices from utilities. | Commodity price volatility (natural gas). Regulatory changes to IRA tax credits. Public and regulatory opposition to new power plant construction (especially gas-fired). New utility tariffs could challenge BTM economics. | Threats shifted from being a passive victim of grid failures to actively managing market, policy, and permitting risks associated with being a power producer. |

Vantage Data Centers 2026 Outlook: Geothermal Drilling Results Are Key

The single most critical catalyst for the self-powered data center model is the real-world performance of the first large-scale, next-generation geothermal projects. The flow rates and costs from initial EGS production wells will validate the financial models underpinning these multi-billion-dollar investments. A successful outcome will trigger a wave of similar JVs across the industry, while any setbacks could cause a temporary retrenchment to more conventional power sources.

- If drilling results from initial projects are positive and costs align with projections, watch for a rapid acceleration of investment in geothermal-backed data centers. Competitors like Digital Realty and Equinix will be compelled to announce similar large-scale BTM power JVs to keep pace.

- Watch for the project financing terms of the first major integrated deals. The syndicate of banks involved and the interest rates secured will signal the financial market’s true assessment of the integrated model’s risk profile and bankability.

- Monitor for any long-term decarbonization plans for the natural gas components of these projects. Announcements related to hydrogen conversion or carbon capture will be critical for managing long-term ESG risk and maintaining a positive reputational narrative.

The questions your competitors are already asking

This report covers one angle of the data center industry’s strategic shift to self-generation power. The questions that matter most depend on your work.

- Which data center operators are adopting behind-the-meter power solutions combining natural gas and geothermal?

- What is the outlook for enhanced geothermal deployment to power AI data centers by 2030?

- Are partnerships between data center operators like Vantage and energy firms like Liberty Energy progressing from concept to GW-scale deployment?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.