AI Data Center Grid Constraint, 50 GW Gas Projects, 7-Year Delays, and 38 State Tax Re-evaluations (2021 to 2026)

AI Infrastructure Project Risks, 30% Delays to 2028, and a 7-Year Grid Queue

The expansion of AI infrastructure is now fundamentally limited by physical world constraints, a stark shift from the pre-2025 focus on capital deployment and land acquisition. The primary execution risks are no longer financial but are rooted in the inability to secure sufficient power from an overloaded grid and navigate extreme lead times for critical electrical hardware. This has created a bifurcation where announced projects are delayed or cancelled, forcing a strategic pivot toward direct control over energy generation.

- Prior to 2025, hyperscaler strategy centered on securing tax incentives and signing large-scale renewable Power Purchase Agreements (PPAs). From 2025 onward, the dominant activity has become managing project delays and developing strategies to bypass grid limitations.

- The most severe constraint is the electrical grid, where interconnection queues for new large loads now stretch between five and seven years. This timeline is fundamentally misaligned with the one to three-year construction cycle for hyperscale facilities, creating a significant and persistent project execution gap.

- The mismatch between planned capacity and executable projects is substantial. Industry analysis projects that between 30% and 50% of data center capacity planned for 2026 will be delayed until 2028 or later due to power and supply chain constraints.

- In response, hyperscalers are increasingly acting as energy developers. A defining trend in 2025 was the announcement of approximately 50 GW of behind-the-meter natural gas generation projects specifically to power new AI data centers, signaling a move to secure power directly and avoid public grid bottlenecks.

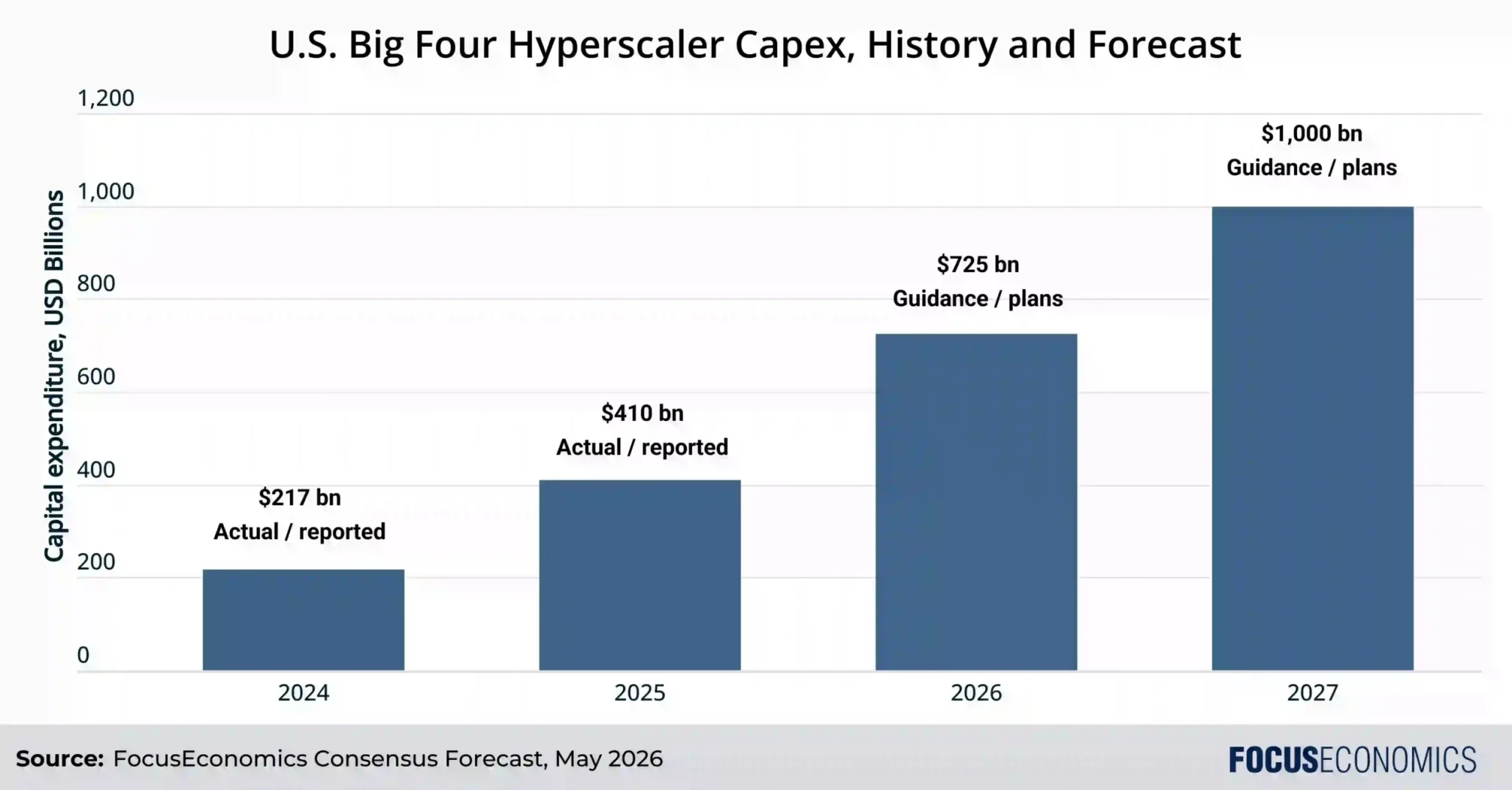

Hyperscaler Capex Forecasted to Reach $1T by 2027

This section discusses risks, delays, and grid limitations. The chart’s ambitious ‘$1T by 2027’ forecast provides a stark contrast and highlights the scale of what is at stake, making the discussion of potential roadblocks more impactful.

(Source: Focus Economics)

Hyperscaler Capex $725 B in AI Spending, Credit Sights and Dell’Oro Forecasts

Hyperscaler capital expenditure is expanding at an exponential rate, with multiple analyst forecasts projecting that aggregate spending will surpass $600 billion annually by 2026. This unprecedented capital deployment is the primary driver of demand across the energy and semiconductor sectors, creating intense competition for a finite pool of physical resources and specialized labor.

- Analyst consensus confirms the scale of the investment. Credit Sights projects that capex for the top five hyperscalers alone will reach $602 billion in 2026, a 36% increase over 2025.

- Broader market forecasts are even larger. Dell’Oro Group estimated that global data center capex would reach $726 billion in 2025, a 57% year-over-year increase, directly attributable to the AI build-out.

- This financial outlay translates directly into physical demand. S&P Global forecasts that data center grid-power demand in the U.S. will rise 22% in 2025 and nearly triple by 2030, while the IEA projects a 15% compound annual growth rate for global data center energy consumption through 2030.

- The capital is also fueling a massive expansion of the semiconductor market. Marketsand Markets forecasts the data center semiconductor market will grow from $86.8 billion in 2024 to $265.8 billion by 2029.

Table: Hyperscaler and Data Center Capex Forecasts

| Forecast Provider | Market Segment | 2024 Capex ($B) | 2025 Capex ($B) | 2026 Capex ($B) | Source |

|---|---|---|---|---|---|

| Credit Sights | Top 5 Hyperscalers | 256 | 443 | 602 | Credit Sights |

| Dell’Oro Group | Global Data Center | – | 726 | – | Network World |

| KKR | Top 4 Hyperscalers | – | 350 | – | KKR |

| S&P Global | Aggregate Data Center | – | 425 | – | S&P Global |

| Silicon Analyst | AI Capex | – | 380 | – | Silicon Analyst |

Hyperscaler 500 MW PPA with Linea Energy and the Shift to On-Site Power

While hyperscalers continue to sign large-scale renewable PPAs to meet sustainability goals, the defining strategic shift is toward direct investment in on-site, dispatchable power generation. This move is a direct response to grid saturation and interconnection delays, representing a fundamental change in how these companies procure and manage energy for their core operations. Control over power generation is now a competitive necessity.

- The traditional PPA model remains a part of the strategy. For example, Google announced a 500 MW solar PPA with Linea Energy to supply its Texas data centers, and Meta continues to be a major procurer of renewable energy.

- However, the limitations of intermittent renewables and grid congestion are forcing a new approach. Big Tech drove a record wave of PPAs in 2024, but S&P Global notes this model is now under strain, pushing hyperscalers to pursue 24/7 carbon-free energy through direct investment.

- The most significant validation of this shift is the surge in on-site natural gas projects. In 2025 alone, approximately 50 GW of such projects were announced as a primary strategy to power new AI data centers, effectively creating private microgrids to ensure operational reliability.

- This trend extends to long-term bets on advanced nuclear. Though still in early development stages, the pursuit of small modular reactors (SMRs) is now a core part of the long-term AI data center energy strategy to secure reliable, carbon-free baseload power.

US vs. Global, AI Infrastructure Development and Regulatory Pushback

While the United States remains the epicenter of the AI data center build-out, the immense strain on local grids, water supplies, and budgets is triggering significant regulatory and community pushback. The period from 2025 onward is characterized by a growing friction between developers and local governments, a sharp contrast to the more welcoming environment of previous years.

- Between 2021 and 2024, growth was driven by states offering generous tax incentives to attract investment, with Virginia, Texas, and Georgia becoming major hubs. In this period, 38 states established such incentive programs.

- Starting in 2025, this trend began to reverse. In February 2026, Illinois suspended its tax incentive program for two years, citing grid and budget pressures. An Arizona task force recommended eliminating its tax breaks entirely, and lawmakers in several other states are now reconsidering their programs.

- Community opposition has become a material risk. Between May 2024 and March 2025, over $64 billion in planned data center projects were delayed or canceled due to organized local resistance concerned with noise, resource consumption, and the visual impact of high-voltage transmission lines.

- This evolving geographic risk profile is forcing hyperscalers to engage more directly in infrastructure development. In March 2026, hyperscalers signed a White House pledge to help fund grid upgrades, acknowledging that they can no longer be passive consumers of public infrastructure.

Hyperscaler Capex Rivals Historical National Projects

The section’s theme of ‘US vs. Global’ development and regulation is well-contextualized by comparing the immense scale of private AI infrastructure spending to government-led ‘Historical National Projects,’ framing the topic in geopolitical terms.

(Source: Reddit)

AI Infrastructure Technology, TRL 9 Components Meet TRL 6 Power Solutions

While the core compute and networking components for AI data centers are commercially mature (TRL 9), the unprecedented power density of these systems is forcing the adoption of new cooling technologies and creating urgent demand for less mature, long-term power solutions. The technology stack is now a mix of mature silicon and emerging infrastructure, where the latter is becoming the gating factor for deployment.

- Commercially mature (TRL 9) technologies deployed at scale include custom ARM-based processors like AWS Graviton and Microsoft Cobalt, as well as advanced power electronics using Gallium Nitride (Ga N) and Silicon Carbide (Si C) to increase server rack power density.

- The power consumption of modern GPUs has made liquid cooling a mandatory, enabling technology (TRL 8-9) rather than a niche option. Direct-to-chip and immersion cooling systems are now essential for managing the thermal loads of AI servers, driving a market projected to grow from $5.3 billion in 2025 to over $32 billion by 2032.

- The primary technology gap is in power generation. To achieve 24/7 carbon-free operations, hyperscalers are investing in solutions with lower technology readiness levels, most notably small modular reactors (SMRs), which are currently at TRL 5-6 for commercial deployment.

- A similar dynamic exists in the semiconductor supply chain. While GPU designs are mature, their production is constrained by the limited capacity for advanced packaging (Co Wo S) and the oligopolistic supply of High Bandwidth Memory from firms like SK Hynix, creating structural bottlenecks.

AI Capex Forecasts Revised Sharply Upward

This section describes a technological mismatch between mature components (TRL 9) and less-developed power solutions (TRL 6). This imbalance leads to unforeseen costs, which directly explains why ‘AI Capex Forecasts’ would be ‘Revised Sharply Upward’.

(Source: Metals and Miners | Substack)

SWOT Analysis, AI Infrastructure Strengths and Supply Chain Weaknesses

The AI infrastructure market’s core strength is its immense capital backing and clear, quantifiable demand from AI workloads. However, this strength is critically undermined by weaknesses in physical supply chains for energy and hardware, coupled with external threats from regulatory friction and community opposition. The opportunity lies in vertically integrating to solve these physical constraints.

Hyperscaler Capex Surpasses GDP of Nations

A high-level SWOT analysis is effectively introduced by a chart that provides a powerful sense of scale. Comparing capex to the ‘GDP of Nations’ dramatically illustrates the financial ‘Strength’ of the AI infrastructure sector.

(Source: LinkedIn)

Table: SWOT Analysis for AI Data Center Infrastructure

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strength | Access to low-cost capital and generous state tax incentives drove rapid expansion. Focus was on land acquisition and securing cloud market share. | Massive capex budgets ($725 B+ projected annually) and clear ROI from AI services. Hyperscalers possess market power to influence entire supply chains. | The limiting factor shifted from capital to physical constraints, validating the strategic importance of securing power and hardware. |

| Weakness | Growing reliance on a few key data center hubs (e.g., Northern Virginia). Early signs of supply chain constraints in specialized hardware. | Extreme lead times for critical grid components (transformers, switchgear). Grid interconnection queues of 5-7 years. Dependency on oligopolies for HBM and advanced chip packaging. | Physical bottlenecks in the power grid and semiconductor supply chain were validated as the primary system-level weaknesses. |

| Opportunity | Large-scale renewable PPAs were the primary strategy to secure clean energy and meet ESG goals. | Vertical integration into power generation (on-site gas, SMRs). Adoption of efficiency tech (liquid cooling). Using AI to manage energy loads and grid stability. | The failure of public infrastructure to keep pace created a massive market opportunity for private infrastructure development and new energy technologies. |

| Threat | Concerns about energy and water consumption were present but not a primary blocker for most projects. | Widespread community opposition ($64 B in projects delayed). States reconsidering or suspending tax incentives (Illinois, Arizona). Grid instability from high-density loads. | The “NIMBY” (Not In My Backyard) phenomenon and regulatory backlash have become material, quantifiable threats to project pipelines and financial models. |

AI Infrastructure 2026, Hyperscalers Navigate Grid and Supply Constraints

The defining scenario for 2026 is a market bifurcation driven by access to power. Projects with secured grid connections and hardware allocations will proceed, creating pockets of hyper-growth. However, a significant portion of announced capacity will remain stalled in interconnection queues, forcing hyperscalers to intensify their transformation into vertically integrated energy developers.

- If grid interconnection queues remain at five-plus years, watch for an acceleration of on-site natural gas deployments as the default bridging solution and a surge in direct corporate investment into SMR and advanced geothermal development companies.

- If lead times for high-voltage transformers and electrical switchgear do not decrease, these specific components will become the primary physical gating factor for connecting new data centers and substations, superseding even GPU availability.

- The trend of states rolling back tax incentives is gaining momentum. Watch for other major data center states to launch legislative reviews, potentially increasing the cost basis for new projects and shifting development to regions with more supportive industrial policies.

- As liquid cooling becomes standard, water consumption will emerge as the next major environmental and regulatory battleground, particularly in water-scarce but high-growth regions like Arizona and Texas.

Hyperscaler Capex Forecast to Hit $727B by 2026

This forward-looking section on the 2026 landscape is best anchored by a chart providing a key forecast for that specific year. The ‘$727B by 2026’ figure serves as the central data point for the section’s discussion on navigating future constraints.

(Source: MSN)

The questions your competitors are already asking

This report covers one angle of the physical-world constraints limiting the AI data center build-out. The questions that matter most depend on your work.

- What is actually happening with announced hyperscale data center projects given the 7-year grid interconnection queue?

- What is the outlook for AI data center capacity deployment by 2028, given that 30-50% of projects face delays?

- Which hyperscalers are most aggressively pursuing on-site gas power generation to bypass grid constraints?

- What are the opportunities for electrical hardware suppliers and energy developers as hyperscalers become their own utilities?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.