Climeworks DAC Procurement, 40, 000 Ton Morgan Stanley Deal, 10-Year TD Bank Pact, and 5 Key Offtake Agreements (2021 to 2026)

CDR Procurement Shifts, Climeworks and TD Bank’s Portfolio Strategy

The carbon removal market has decisively shifted from speculative, single-technology spot purchases before 2025 to strategic, long-term portfolio procurements, a model now being adopted by major financial institutions to de-risk net-zero commitments. This evolution reflects a growing sophistication among buyers who are moving beyond simple offsetting to actively financing the infrastructure required for a net-zero economy.

- In the 2021-2024 period, the market was defined by pioneering but singular deals, such as Swiss Re‘s $10 million, 10-year agreement with Climeworks in August 2021. These early agreements were crucial for establishing the concept of long-term offtakes for pre-commercial technologies.

- The model evolved significantly by 2026. TD Bank Group‘s agreement with Climeworks Solutions on June 1, 2026, for a 10-year, North America-focused portfolio is a primary signal of this change. The deal intentionally includes a mix of Direct Air Capture (DAC), biochar, and enhanced weathering to manage technology and delivery risk.

- This portfolio strategy is mirrored by market leader Microsoft, which contracted for a total of 45 million tonnes of Carbon Dioxide Removal (CDR) in FY 2025 across a diverse range of technologies. This approach allows sophisticated buyers to balance cost, scalability, and permanence across a maturing but still uncertain technology landscape.

- The emergence of integrated project developers like Deep Sky further validates this market segmentation. Deep Sky bundles various DAC technologies from different startups and secures large offtake agreements with buyers like TD Bank and Lufthansa Group, acting as a crucial link between technology innovation and market demand.

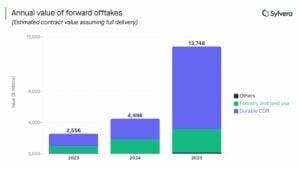

Forward Offtake Value Skyrockets Past $13.7B

The chart’s headline about skyrocketing forward offtake value directly illustrates the major ‘procurement shifts’ toward long-term, high-value agreements mentioned in the section heading.

(Source: CarbonCredits.com)

Over 49 M Tons Contracted, Climeworks and Microsoft Lead DAC Offtakes

Major corporations are catalyzing the carbon removal industry by signing multi-year, multi-million-ton offtake agreements, providing the revenue certainty required to secure project financing for capital-intensive DAC facilities. These deals are shifting from symbolic purchases to bankable contracts that underpin the construction of large-scale infrastructure.

- Prior to 2025, landmark deals were primarily valued by their duration and total financial commitment. Key examples include Swiss Re‘s $10 million, 10-year commitment to Climeworks (2021) and the buyer-led consortium Frontier‘s $41 million offtake agreement for bioenergy with carbon capture (BECC) with Reverion (2025).

- Since early 2026, the scale of these agreements has increased dramatically in terms of volume. Microsoft set a new benchmark by securing a 1.8 million tonne, 15-year reforestation credit deal with Terraformation and announcing a total contracted portfolio of 45 million tonnes of CDR in FY 2025.

- The financial sector’s direct participation is a key accelerator. This is marked by TD Bank‘s back-to-back 10-year deals in June 2026, first with Climeworks for a diversified portfolio and then with Deep Sky for over 18, 000 DAC credits, treating carbon removal as a new class of bankable assets.

- Even without publicly disclosed volumes, long-term partnerships such as the 10-year agreement between 1 Point Five and Amazon (2023) and Climeworks‘ 40, 000-ton deal with Morgan Stanley (2024) provide the foundational financial commitments necessary to build multi-hundred-million-dollar DAC facilities.

Durable CDR Purchase Volume Skyrockets Post-2022

The chart visualizes the dramatic increase in CDR purchase volume, providing the market context for the section’s specific data point on ‘Over 49 M Tons Contracted’ and the leadership role of companies like Climeworks and Microsoft.

(Source: Carbon Removal Updates – Substack)

Climeworks Major Corporate CDR Offtake Agreements

| Announcement Date | Buyer | Supplier(s) | Duration (Years) | Volume (Tonnes CO₂e) | Key Technologies | Source |

|---|---|---|---|---|---|---|

| Jun 1, 2026 | TD Bank Group | Climeworks Solutions | 10 | Not Disclosed | DAC, Biochar, Enhanced Weathering | DOB Energy |

| May 1, 2026 | NTT Data | Climeworks | Not Disclosed | Not Disclosed | DAC | Energy Intelligence |

| Mar 3, 2026 | Microsoft | Terraformation | 15 | 1, 800, 000 | Nature-Based Removals | Carbon Credits.com |

| Oct 24, 2024 | Morgan Stanley | Climeworks | Until 2037 | 40, 000 | DAC | Wall Street Journal |

| Mar 21, 2023 | Microsoft | Climeworks | 10 | 10, 000 | DAC | Climeworks |

| Aug 25, 2021 | Swiss Re | Climeworks | 10 | $10, 000, 000 (Value) | DAC | Swiss Re |

Microsoft’s Carbon Removal Contracts Surge

As Microsoft is one of Climeworks’ most significant corporate partners, this chart detailing the surge in Microsoft’s offtake agreements serves as a prime case study for the section’s focus on major corporate deals.

(Source: CarbonCredits.com)

North America vs. Europe, Climeworks’ Focus on US & Canadian Projects

While Europe, particularly Switzerland and Iceland, pioneered early DAC deployments, the market’s center of gravity for large-scale projects and procurement is shifting decisively to North America, driven by favorable policy incentives and a growing ecosystem of sophisticated buyers and project developers.

- In the 2021-2024 period, market leadership was centered in Europe. Climeworks launched its Orca plant in Iceland and secured foundational partnerships with European firms like Swiss Re, establishing the region as the initial hub for DAC innovation and deployment.

- By 2026, North America dominates new project announcements and deal flow. The Climeworks–TD Bank deal specifically targets North American projects to align with TD’s operational footprint and capitalize on regional policy support.

- The U.S. Inflation Reduction Act’s Section 45 Q tax credit, which provides up to $180/ton for DAC with geologic sequestration, is a primary catalyst. This policy has attracted major project developments from companies like 1 Point Five (Texas), Carbon Capture Inc. (Wyoming), and Heirloom Carbon (funded by the DOE).

- Canada is rapidly emerging as a complementary hub for carbon removal. Project developers like Deep Sky are building infrastructure and attracting international technology partners, supported by offtake commitments from major Canadian entities like TD Bank, creating a robust and integrated North American market.

Climeworks’ Tech Maturation, From TRL 6-7 DAC to Diversified Portfolios

The carbon removal industry is advancing beyond a singular focus on maturing Direct Air Capture (TRL 6-7) by integrating more established methods like biochar (TRL 7-9) into commercial offerings, creating blended portfolios that balance technological readiness, cost, and durability for corporate buyers.

- Before 2025, the market narrative was dominated by the race to scale discrete DAC technologies. Leaders like Climeworks (solid sorbent) and Carbon Engineering/1 Point Five (liquid solvent) focused primarily on demonstrating their core technologies at pioneering facilities like the Orca plant in Iceland.

- By 2026, the commercial strategy has matured significantly. Climeworks Solutions, the entity that structured the TD Bank deal, now operates as a technology-agnostic portfolio manager, bundling its own high-permanence DAC with lower-cost, market-ready solutions like biochar.

- This portfolio approach pragmatically addresses the high current cost of pure DAC ($600-$1, 200/tonne). By blending it with more affordable options like biochar ($100-$400/tonne) and emerging technologies like enhanced weathering ($50-$200/tonne), suppliers can offer buyers a more accessible price point for durable removal.

- The market now clearly differentiates technologies based on their distinct profiles: DAC for maximum durability and verifiability, biochar for immediate volume at a lower cost, and enhanced weathering for future scalability, allowing buyers to construct a time-diversified climate action strategy.

CDR Market Vulnerable Due to Lack of Diversity

This chart explains the core problem—market vulnerability from a lack of technology and supplier diversity—which provides the strategic rationale for Climeworks’ move toward the ‘Diversified Portfolios’ mentioned in the section heading.

(Source: Carbon Removal Updates – Substack)

SWOT Analysis, Climeworks’ Strengths and DAC Market Execution Risks

Climeworks and the broader DAC sector leverage strong corporate demand and supportive government policies, but face significant headwinds from high capital costs and the operational challenge of scaling physical project delivery to meet contracted volumes.

- Strengths are rooted in established technology leadership and a growing pipeline of bankable, long-term offtake agreements from blue-chip companies, transforming DAC from a concept into a financeable asset class.

- Weaknesses remain the high cost per ton and significant energy requirements, which constrain near-term profitability and scalability without robust subsidies and continued technological innovation.

- Opportunities are expanding rapidly with the adoption of the portfolio model, which opens new revenue streams, and the entry of new buyer segments from the finance and aviation industries.

- Threats include competition from lower-cost CDR methods if durability is not adequately valued by the market, and the significant risk of project delays that could damage buyer confidence and slow momentum.

Chart Shows Widening Carbon Removal Gap to 2050

This chart quantifies the ‘widening gap,’ which represents the core market Opportunity in a SWOT analysis. The sheer scale of this gap also highlights the ‘Market Execution Risks’ of failing to scale, a key theme of the section.

(Source: Carbon Removal Updates – Substack)

Climeworks and DAC Market SWOT Analysis

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | First-mover advantage with operational Orca plant; secured first major 10-year deal with Swiss Re (2021). | Securing large-volume, multi-year offtakes (e.g., Morgan Stanley for 40, 000 tons); establishing a portfolio management arm (Climeworks Solutions). | The business model has been validated, shifting from a pure technology demonstrator to a bankable asset manager with a proven ability to secure nine-figure equivalent contracts. |

| Weaknesses | Extremely high cost of removal (>$600/ton) limited the market to a few niche buyers; small scale of physical removal (thousands of tons). | Costs remain high, and energy intensity is a major bottleneck for scaling. Physical delivery of credits (4.2% market-wide in 2024) significantly lags behind credit sales. | The fundamental economic challenge persists, but it is now being actively managed through portfolio blending and long-term contracts rather than waiting solely for technology cost-downs. |

| Opportunities | Early adoption by corporate climate leaders like Microsoft, which served as crucial anchor customers. | Expansion into new, large customer segments like financial services (TD Bank, Morgan Stanley) and aviation (Lufthansa Group); leveraging powerful policy like the U.S. 45 Q tax credit. | The addressable market has broadened significantly beyond big tech. Financial services companies are now a primary demand driver, bringing new rigor to the market. |

| Threats | Competition from low-cost, low-quality carbon offsets; lack of standardized Measurement, Reporting, and Verification (MRV) protocols. | Competition from other durable CDR methods (e.g., biochar, BECCS) on a cost-per-ton basis; major project execution risks and potential for construction delays. | The competitive threat has shifted from low-quality offsets to a more sophisticated contest between different types of high-quality removal, and the operational risk of building gigaton-scale infrastructure is now the primary concern. |

Durable CDR Investment Peaked at $1.2B in 2023

The investment landscape is a critical component of a SWOT analysis. This chart, showing a peak in investment, provides a key data point for discussing both market Opportunities (capital inflow) and Threats (potential for a funding slowdown).

(Source: CarbonCredits.com)

2026 Outlook, Climeworks’ Path to Bankability via Project Finance

The critical test for DAC leaders like Climeworks in the year ahead is the conversion of strong demand signals from offtake agreements into the project financing and physical asset deployment required to scale the industry.

- If this happens: More financial institutions and multinational corporations follow the lead of TD Bank and Morgan Stanley by signing large, multi-year portfolio offtake agreements for durable carbon removal.

- Watch this: The announcement of “Final Investment Decisions” (FIDs) for new, large-scale DAC plants in North America. These decisions will be backed by the growing number of long-term offtake agreements, which serve as the collateral needed to secure project debt and equity.

- These could be happening: The development and rollout of more standardized financial products, such as CDR futures contracts or insurance mechanisms designed to de-risk these long-term agreements. This financialization is essential for attracting a wider pool of institutional capital beyond corporate balance sheets.

Financing is Top Cost Driver for Engineered CDR

The chart’s conclusion that financing is the primary cost driver for engineered CDR directly underscores the importance of the section’s topic: achieving ‘Bankability via Project Finance’ to lower costs and enable scaling.

(Source: Carbon Removal Updates – Substack)

The questions your competitors are already asking

This report covers one angle of carbon removal procurement strategy. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the multi-year carbon removal offtake market?

- What is the outlook for multi-technology CDR portfolios being adopted by the financial sector by 2030?

- How does Direct Air Capture compare to biochar and enhanced weathering for building a risk-managed carbon removal portfolio?

- Which financial institutions beyond TD Bank and Morgan Stanley are adopting multi-year, portfolio-based carbon removal offtake agreements?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.