DAC Investment Policy, Canada’s 60% CAPEX Credit, 3 Deep Sky Offtake Deals, and 20+ Global Projects (2021 to 2026)

DAC Project Risk, Canada’s CAPEX vs US OPEX Incentive Structure

Canada’s 60% Investment Tax Credit (ITC) accelerates Direct Air Capture (DAC) deployment by solving the primary barrier of high upfront capital, while the U.S. 45 Q production credit addresses long-term operational viability, creating two distinct risk and investment profiles for project developers.

- Between 2021 and 2024, the global DAC industry was shaped by policy formation, with Canada’s government designing its CCUS ITC to compete directly with the U.S. Inflation Reduction Act. The 60% rate for DAC was established as a strategic industrial policy to attract first-of-a-kind projects by heavily subsidizing capital expenditure (CAPEX).

- From 2025 to today, the focus has shifted to execution and commercialization. Canadian developers like Deep Sky are leveraging the 60% ITC to secure project financing and sign offtake agreements with buyers like Microsoft. This contrasts with U.S. projects, which focus on securing long-term revenue streams backed by the $180 per tonne 45 Q production credit.

- The Canadian model significantly improves a project’s Internal Rate of Return (IRR) and shortens the Payback Period, making it attractive for developers struggling to overcome the initial financing hurdle. However, it leaves projects fully exposed to high operating costs (OPEX), particularly energy, a risk directly subsidized by the U.S. 45 Q credit.

- Canada’s policy includes a “subsidy cliff, ” with the full credit rates extended to 2035 before being halved until 2040. This creates timeline risk and forces developers to accelerate permitting and construction, a pressure that is structured differently in the U.S. model, which uses a “begin construction” deadline of January 1, 2033.

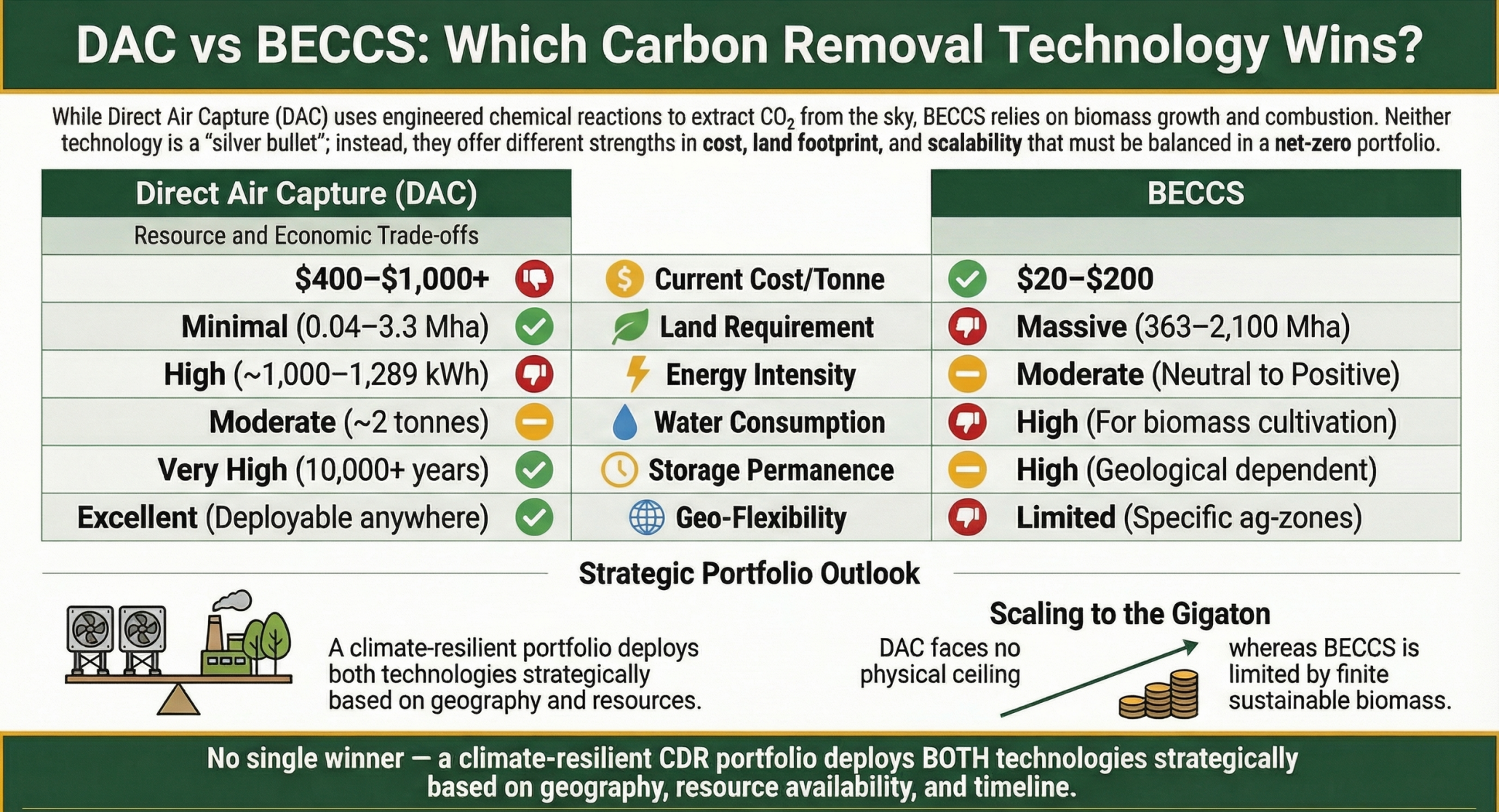

DAC vs. BECCS: Carbon Removal Technology Trade-offs

The section discusses project risk and financial structures (CAPEX vs OPEX). The chart informs this by illustrating the underlying technology trade-offs between DAC and an alternative, BECCS, which are fundamental to a project’s risk profile and financial model.

(Source: Green Fuel Journal)

$18.7 B Market Forecast, Canada’s DAC Policy Attracts Capital

Aggressive financial incentives in North America, led by Canada’s 60% ITC and the U.S. 45 Q, are directly responsible for the projected exponential growth of the DAC market, forecast to expand from under $200 million in 2025 to over $18 billion by 2035.

- The primary investment signal between 2021 and 2024 was the establishment of the policy frameworks themselves, which function as government-backed de-risking mechanisms for private capital. These policies created the foundation for the subsequent flow of investment into the sector.

- Post-2025, investment activity is materializing through large-scale, multi-year offtake agreements. These contracts, such as those secured by Deep Sky with Rubicon Carbon and Engie, represent bankable revenue streams made possible by the underlying policy support.

- The Canadian 60% upfront credit is particularly attractive to venture capital and private equity seeking to minimize initial cash outlay and maximize IRR on exit. In contrast, the predictable, long-term revenue stream from the U.S. 45 Q is more suitable for infrastructure funds with lower risk tolerances and longer investment horizons.

- Market forecasts reflect this policy-driven momentum. The consensus compound annual growth rate (CAGR) for the DAC market exceeds 50%, a growth trajectory almost entirely dependent on the continuation of these government incentives to bridge the gap to commercial profitability.

Global CO2 Capture Capacity to Surge by 2030

The section headline is a market forecast for Canada. The chart provides the global context for this forecast, showing a projected surge in worldwide capacity that underpins the potential for significant market growth and capital attraction in Canada.

(Source: Rystad Energy)

Deep Sky 3 Offtake Agreements, Microsoft and Google (2025 to 2026)

Following the implementation of Canada’s tax credit, DAC project developers like Deep Sky rapidly secured multi-year offtake agreements with major corporate buyers, validating the policy’s effectiveness in catalyzing a commercial market for carbon removal credits.

- While partnerships between 2021 and 2024 focused on technology validation and research, the period from 2025 onwards has seen a decisive shift toward commercial offtakes. This change is a direct result of the financial certainty provided by the ITC.

- In 2026, Deep Sky announced agreements with founding buyers including Microsoft, Royal Bank of Canada, and Google (via Frontier), signaling strong corporate demand for high-durability credits originating from Canadian projects.

- The maturing ecosystem is demonstrated by a May 2026 partnership between Deep Sky and Engie, which expanded beyond simple credit procurement to include joint market development and research to advance DAC deployment.

- A June 2025 multi-year offtake agreement with Rubicon Carbon further solidified Deep Sky’s revenue pipeline. This proves that the ITC is successfully creating the financial stability needed for developers to secure the long-term contracts necessary for project financing.

Hard-to-Abate Sectors Drive 40% of Emissions

The section highlights specific offtake agreements, representing demand for carbon removal. The chart explains the origin of this demand, showing that hard-to-abate sectors are a major source of emissions, thus creating a market for carbon removal credits.

(Source: JPT – SPE)

Table: Recent Commercial Agreements in the Canadian DAC Sector

| Company / Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Deep Sky / Engie | May 2026 | Partnership combines carbon credit procurement, market development, and joint research. This strategic alliance aims to accelerate DAC deployment by leveraging Engie’s energy expertise and market access. | ESG Today |

| Deep Sky / Microsoft, RBC, Google | April 2026 | Named as founding buyers for future carbon removal credits. Securing anchor customers from major technology and finance sectors provides critical validation and bankability for future projects. | Yahoo Finance |

| Deep Sky / Rubicon Carbon | June 2025 | Multi-year offtake agreement for the purchase of high-quality, durable carbon dioxide removal credits. This locks in a long-term revenue stream, de-risking future operations. | PR Newswire |

Global CCUS Deployment Grows to 45 Mt/Year

The section’s table details recent Canadian commercial agreements. The chart provides the macro context, showing the current global scale of CCUS deployment, which helps frame the significance of new Canadian projects contributing to this total.

(Source: ScienceDirect.com)

North America, Canada’s DAC Incentives vs. US 45 Q Dominance

North America has firmly established itself as the global epicenter for DAC deployment, driven by a direct policy competition between Canada’s upfront capital incentives and the United States’ long-term production credits.

- Prior to 2024, DAC activity was geographically dispersed, with notable pilot projects in Europe, such as those by Climeworks in Iceland and Switzerland, alongside early-stage work in North America.

- The introduction of Canada’s 60% ITC and the enhanced U.S. 45 Q has since concentrated new large-scale project announcements almost exclusively in these two countries, creating a powerful magnet for global capital and technology.

- Canada, particularly provinces like Alberta with favorable geology for CO₂ storage and a skilled energy workforce, is emerging as the preferred hub for projects prioritizing the reduction of initial capital expenditure.

- The U.S. attracts projects that can leverage the $180 per tonne production credit to secure long-term revenue and offset high operational energy costs, creating a distinct but parallel growth trajectory focused on operational subsidies.

Canada Maps Carbon Management Project Landscape

The section compares Canada’s incentives to US dominance. The map directly visualizes the result of these Canadian incentives, showing the locations of projects that constitute Canada’s carbon management ‘landscape’ in the North American context.

(Source: Natural Resources Canada – Canada.ca)

Commercial Viability, Canada’s ITC Impact on DAC TRL

Canada’s 60% ITC does not change the fundamental Technology Readiness Level (TRL) of DAC, which remains at pre-commercial or first-of-a-kind demonstration scale (TRL 6-8), but it critically accelerates the path to commercial viability by subsidizing the “valley of death” between pilot and megatonne-scale deployment.

- Between 2021 and 2024, DAC technology was primarily proven at the pilot scale. The core technology was ready for deployment, but prohibitive costs prevented scaling and the business case remained unproven.

- Post-2025, the ITC enables developers to finance and build demonstration plants at a much larger scale than previously possible. This accelerates the accumulation of operational data and drives down costs through learning-by-doing, which is essential for achieving commercial scale.

- The policy’s impact is not on inventing new technology but on financing its deployment. It shifts the key challenge from technical risk to execution risk: delivering large industrial projects on time and on budget to capture the full tax credit before the sunset clauses take effect.

- The high CAPEX of DAC systems, estimated to range from $317 to over $1, 000 per tonne of annual capacity, is the exact barrier the ITC is designed to overcome, making projects with a TRL of 6 or higher financially plausible for the first time.

Chart Shows High Cost of Direct Air Capture

The section addresses commercial viability and the impact of Canada’s Investment Tax Credit (ITC). The chart perfectly illustrates the core challenge the ITC aims to solve: the high cost of DAC, which is the primary barrier to its commercial viability.

(Source: Energy Industry Insights from Avanza Energy – Substack)

SWOT Analysis, Canada’s 60% DAC Investment Tax Credit

The SWOT analysis reveals Canada’s ITC as a powerful strength for attracting initial investment, but it highlights weaknesses in addressing long-term operational costs and threats from policy uncertainty. Developers must mitigate these risks through strategic energy procurement and long-term offtake contracts to ensure project success.

Map Shows Canada’s CO2 Storage Potential

The section is a SWOT analysis of Canada’s DAC tax credit. The map visualizes a key ‘Strength’ and ‘Opportunity’ for Canada: its vast geological potential for CO2 storage, a critical enabling factor for a successful national DAC industry.

(Source: Natural Resources Canada – Canada.ca)

Table: SWOT Analysis for Canada’s DAC Investment Tax Credit

| SWOT Category | 2021 – 2024 (Policy Design Phase) | 2025 – Today (Implementation Phase) | What Changed / Validated |

|---|---|---|---|

| Strength | Proposed 60% refundable credit for DAC was the most aggressive global incentive on paper, designed to attract capital. | The policy is now enacted, and the 60% refundability is a tangible financial tool. It dramatically improves project IRR and lowers the initial equity hurdle for developers. | The theoretical strength of the policy was validated as it successfully attracted project proposals and catalyzed commercial offtake agreements (e.g., Deep Sky). |

| Weakness | The ITC was designed to be CAPEX-focused, leaving uncertainty about how projects would cover long-term operational costs (OPEX), especially high energy use. | This weakness is now a primary strategic challenge. Projects are entirely exposed to energy price volatility, making access to low-cost, long-term clean power essential for survival. | The weakness was confirmed. The strategic focus for developers has shifted from securing the ITC to securing low-cost power and long-term revenue to cover OPEX. |

| Opportunity | The policy aimed to create a first-mover advantage for Canada in the global carbon removal market by building out infrastructure and a skilled workforce. | The opportunity is materializing as provinces like Alberta become hubs. The policy has spurred demand for high-quality credits, as seen in deals with Microsoft and Google. | The opportunity is being actively pursued. The ITC has successfully created a pipeline of projects and attracted corporate buyers, validating the market-making potential of the policy. |

| Threat | The primary threat was policy uncertainty and the risk of a “subsidy cliff, ” with the credit rate scheduled to decline after 2030 (now extended to 2035). | The threat is now a critical project risk. Developers face significant financial pressure to meet construction deadlines. Additionally, a future government could alter the credit, creating long-term uncertainty. | The threat of the subsidy cliff has been validated as a key driver of project timelines and risk. The extension to 2035 provided some relief but did not eliminate the core issue of policy dependency. |

Deep Sky’s Success, Canada’s ITC vs OPEX Reality in 2027

If developers in Canada can successfully pair the 60% CAPEX credit with long-term, low-cost clean power contracts, watch for a wave of Final Investment Decisions (FIDs) for megatonne-scale projects by 2027, which would validate the CAPEX-first incentive model.

- The most critical variable for success is OPEX, primarily energy cost. A key signal to watch for is Canadian DAC projects announcing long-term Power Purchase Agreements (PPAs) that make their all-in cost of removal competitive with U.S. projects benefiting from the 45 Q production subsidy.

- Watch for announcements of binding offtake agreements that extend 10-15 years. These long-term contracts are essential to de-risk projects beyond the initial CAPEX phase and are a prerequisite for securing traditional debt financing.

- Conversely, if low-cost energy proves elusive or permitting timelines for CO₂ storage facilities drag on, projects may struggle to become operational before the ITC’s value begins to decline, potentially stalling the industry’s momentum.

- The ultimate validation of Canada’s strategy will be the ability of early movers like Deep Sky to convert their initial offtake agreements and subsidized CAPEX into sustainable, positive operational cash flow.

CCUS Faces 152x Scale-Up Gap by 2050

The section discusses the ‘reality’ of scaling up by 2027. The chart provides the essential long-term perspective, illustrating the immense gap between current capacity and 2050 targets, which contextualizes the urgency and challenge of near-term scaling efforts.

(Source: Green Fuel Journal)

The questions your competitors are already asking

This report covers one angle of how competing government incentives are shaping Direct Air Capture project financing and risk. The questions that matter most depend on your work.

- How does Canada’s CAPEX-focused ITC compare to the U.S. OPEX-focused 45Q for improving a project’s Internal Rate of Return (IRR) and Payback Period?

- Deep Sky’s project financing in Canada. Are its offtake agreements sufficient to overcome the high operating cost risk not covered by the 60% ITC?

- What is the investment outlook for Canadian DAC projects, given the ‘subsidy cliff’ when the full credit rates are no longer extended after 2035?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.