Blue Hydrogen’s LNG Lifeline: Why Conoco Phillips’ 2026 Strategy Is Tied to Natural Gas

Blue Hydrogen Project Viability: Conoco Phillips’ Bet on LNG and CCUS for 2026

Conoco Phillips’ approach to the hydrogen economy is defined by strategic positioning rather than aggressive project execution, making its blue hydrogen ambitions entirely dependent on its core competencies in natural gas and carbon capture. The company’s 2025-2026 activities demonstrate a clear prioritization of its massive Liquefied Natural Gas (LNG) investments as the foundational pillar for future low-carbon ventures. This strategy leverages existing infrastructure and expertise to de-risk entry into the hydrogen market, treating it as a “low-carbon adjacency” to its primary business.

- Between 2021 and 2024, Conoco Phillips established its strategic framework by forming foundational partnerships for a proposed U.S. Gulf Coast ammonia plant with JERA and Uniper, alongside a venture investment in Ekona Power for turquoise hydrogen technology.

- The period from 2025 to today reveals a pivot to reinforcing the feedstock supply chain. Capital is overwhelmingly directed toward conventional oil and LNG, evidenced by the $9 billion Willow project and multiple agreements licensing its Optimized Cascade® liquefaction technology for new LNG facilities.

- This cautious, infrastructure-first approach contrasts with competitors like Shell, which is already executing on pilot hydrogen projects. Conoco Phillips is building the capability to produce blue hydrogen at scale but is waiting for market and policy conditions to mature before committing major capital.

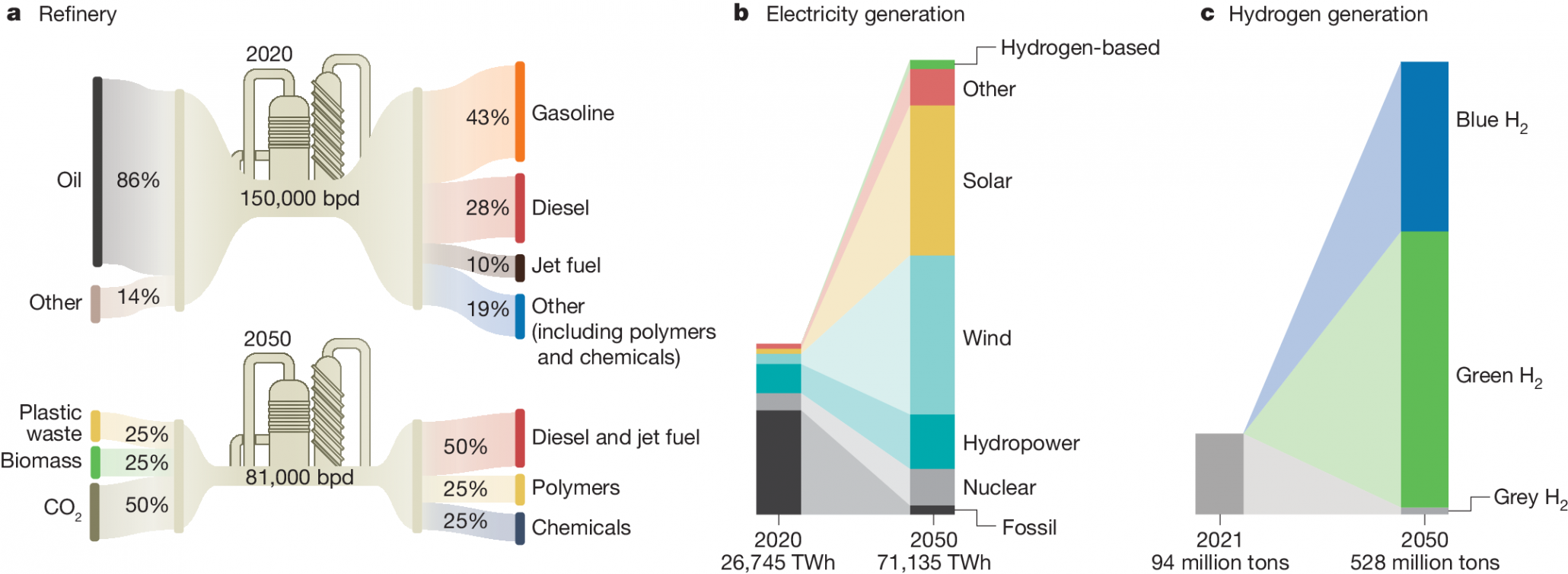

Future Hydrogen Mix Dominated by Low-Carbon

This chart shows the projected market shift toward blue and green hydrogen, which provides the macro-level justification for Conoco Phillips’ strategic bet on a low-carbon hydrogen future.

(Source: Nature)

Capital Discipline vs. Clean Energy: Analyzing 2026 Investment Priorities

In the 2025-2026 timeframe, Conoco Phillips’ capital allocation strategy shows that conventional oil and gas projects remain the overwhelming priority, with low-carbon initiatives receiving only a small fraction of total investment. This financial posture indicates that while hydrogen is part of the long-term plan, near-term capital is focused on maximizing returns from its traditional hydrocarbon asset base, which in turn provides the necessary feedstock for future blue hydrogen production.

Willow Oil Project Costs Rise to $9B

This chart exemplifies Conoco Phillips’ near-term capital priority on large-scale conventional oil projects, directly supporting the section’s argument that fossil fuels remain the overwhelming focus.

(Source: Investing.com)

- The company’s estimated $9 billion investment in the Willow oil project in Alaska starkly contrasts with its reported annual spending of approximately $50 million on all combined carbon capture and hydrogen initiatives as of 2023.

- In May 2024, Conoco Phillips acquired Marathon Oil for $22.5 billion, a strategic move aimed at strengthening its U.S. shale gas position. This acquisition directly secures the natural gas feedstock required for its planned blue hydrogen projects, reinforcing the link between its fossil fuel and low-carbon strategies.

- The 2022 venture investment in Ekona Power, part of a $79 million funding round, represents a calculated, small-scale hedge in turquoise hydrogen technology. This provides Conoco Phillips with a future technology option without requiring significant near-term capital outlay.

Table: Conoco Phillips’ Strategic Investments (2022-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Willow Project | 2025 | Increased estimated cost to $9 billion for a long-life oil project. This massive capital allocation to conventional assets highlights the company’s primary investment focus. | World Oil |

| Acquisition of Marathon Oil | 2024 | A $22.5 billion transaction to acquire a major shale operator, significantly bolstering the natural gas feedstock supply essential for future blue hydrogen production. | Forbes |

| Annual Low-Carbon Spend | 2023 | Approximately $50 million per year allocated to early-stage evaluation of CCS and hydrogen projects, a modest sum compared to conventional CAPEX. | Petroleum News |

| Investment in Ekona Power | 2022 | Participated in a $79 million funding round for a methane pyrolysis company, providing a technology hedge in turquoise hydrogen. | Ekona Power |

Conoco Phillips’ Hydrogen Partnerships: Building an LNG-to-Ammonia Value Chain for 2026

The company’s partnership strategy has logically progressed from forming initial hydrogen project frameworks (2022-2023) to securing the underlying natural gas supply chain (2024-2025). This sequence demonstrates that the execution of its blue hydrogen and ammonia ambitions with partners like JERA and Uniper is contingent upon first solidifying its core business of natural gas production and liquefaction.

US Leads in Risky Uncontracted Blue Hydrogen

This chart highlights the significant market risk of developing projects without buyers, explaining why Conoco Phillips’ partnership strategy to secure offtake contracts is critical.

(Source: Carbon Credits)

- The foundational partnership for its hydrogen strategy was established in September 2022 with JERA Americas to develop a blue hydrogen and ammonia facility, followed by a critical Heads of Agreement in September 2023 with German utility Uniper as a major offtaker.

- Enabling partnerships in 2022, such as the agreement with Sempra Infrastructure for LNG project development and with Aris Water Solutions for produced water reuse, were critical for building out the necessary inputs and infrastructure for future hydrogen production.

- Partnerships in 2025 and early 2026, including an exploration venture with 3 D Energi for gas reserves and an EPC contract with Worley Rosenberg to extend the life of an oil field, show a continued operational focus on maximizing and securing fossil fuel feedstock.

Table: Key Hydrogen and Enabling Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| 3 D Energi | 2026 | Partnered on an exploration well to flag probable gas reserves, reinforcing the focus on securing natural gas feedstock for the blue hydrogen strategy. | Proactive Investors |

| JERA & Uniper | 2023 | Signed a Heads of Agreement for Uniper to purchase low-carbon ammonia from the proposed Gulf Coast facility, de-risking the project by securing a major customer. | JERA |

| Aris Water Solutions & Chevron | 2022 | Strategic agreement for beneficial reuse of produced water in the Permian Basin, an essential input for water-intensive blue hydrogen production via SMR. | Aris Water Solutions |

| JERA Americas | 2022 | Agreement to jointly develop a large-scale blue hydrogen and ammonia production facility on the U.S. Gulf Coast, forming the cornerstone of the hydrogen strategy. | Reuters |

| Sempra Infrastructure | 2022 | Framework agreement to develop Port Arthur LNG, strengthening the company’s control over the natural gas value chain needed for blue hydrogen feedstock. | Sempra |

Geographic Focus: Why the US Gulf Coast is Central to Conoco Phillips’ Hydrogen Plan

Conoco Phillips’ hydrogen and low-carbon activities are strategically concentrated on the U.S. Gulf Coast, a region that provides a unique convergence of its legacy natural gas infrastructure, access to global export markets, and favorable geology for carbon storage. The company’s 2025-2026 actions have further entrenched this regional focus, transforming the area into a hub for both its current US LNG dominance and its future blue hydrogen ambitions.

Gulf Coast is a Key Hydrogen & CCUS Region

This map visually confirms the U.S. Gulf Coast’s importance as a hub for hydrogen and CCUS activity, directly aligning with the section’s focus on the region’s centrality to Conoco Phillips’ plan.

(Source: Enverus)

US Government Outlines Hydrogen Hub Roadmap

The U.S. government’s development roadmap provides the national strategic context for the private-sector hydrogen partnerships that Conoco Phillips is pursuing.

(Source: Plug Power)

- The 2022-2023 period established the U.S. Gulf Coast as the target location for the company’s flagship low-carbon ammonia project with JERA, designed to supply markets in the U.S., Europe, and Asia.

- In 2025, this geographic concentration was reinforced by the selection of Conoco Phillips’ proprietary liquefaction technology for the 22.5 mtpa Coastal Bend LNG project in Texas and the Monkey Island LNG project in Louisiana, solidifying its operational footprint in the region.

- While a small-scale 2025 arrangement with Alyeschem on Alaska’s North Slope demonstrates localized carbon commerce, the primary strategic and capital momentum for hydrogen remains firmly anchored to the Gulf Coast’s integrated energy ecosystem.

Technology Strategy: Leveraging Mature LNG Tech for Emerging Blue Hydrogen

Conoco Phillips’ technology strategy hinges on deploying its mature, highly efficient Optimized Cascade® LNG process to strengthen its natural gas business, which serves as the direct economic and feedstock bridge to the emerging blue hydrogen value chain. The company is using its current technological advantage in liquefaction to fund and enable a cautious, long-term entry into hydrogen and carbon capture, utilization, and storage (CCUS).

- Between 2021 and 2024, the company’s main exploratory technology initiative was its venture investment in Ekona Power. This move secured an option in turquoise hydrogen via methane pyrolysis, a potential long-term alternative to blue hydrogen that avoids gaseous CO 2.

- The dominant technology story in 2025 is the commercial success of the Optimized Cascade® process, which was selected for multiple major LNG plants. This shows the company’s immediate focus is on perfecting and monetizing the technology that produces the feedstock for blue hydrogen.

- Blue hydrogen production itself, along with large-scale CCUS and related technologies like Direct Air Capture, are viewed as technologies that require further maturation and policy support, such as the Inflation Reduction Act’s 45 Q tax credits, before Conoco Phillips commits to large-scale deployment.

SWOT Analysis: Conoco Phillips’ Hydrogen Position in 2026

An analysis of Conoco Phillips’ hydrogen strategy reveals that its greatest strength is the ability to leverage its vast natural gas portfolio and project management expertise. However, its primary weakness is a tangible lack of capital commitment and executed hydrogen projects compared to its fossil fuel investments, creating a strategic risk if the market accelerates faster than anticipated.

Hydrogen Production Capacity Set to Surge

This forecast quantifies the massive market growth opportunity that forms a key part of the company’s SWOT analysis, representing the potential reward for its strategic positioning.

(Source: Net Zero Technology Centre)

- Strengths are rooted in its existing business: deep expertise in natural gas, proprietary LNG technology, and a proven track record of managing large, complex energy projects.

- Weaknesses are defined by a cautious capital allocation strategy that heavily favors oil and gas, and a subsequent lag in tangible hydrogen project execution compared to more aggressive competitors.

- Opportunities are driven by favorable policy like the IRA, growing global demand for low-carbon ammonia, and the ability to repurpose existing LNG infrastructure for hydrogen and ammonia.

- Threats include regulatory uncertainty, rapid cost reductions in green hydrogen that could erode the competitiveness of blue hydrogen, and the risk of ceding market share to faster-moving peers.

Table: SWOT Analysis for Conoco Phillips’ Hydrogen Initiatives

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Established a low-carbon division and expertise in natural gas. Formed a key partnership with JERA for a major hydrogen project concept. | Demonstrated dominance in LNG technology with multiple contracts for the Optimized Cascade® process. Acquired Marathon Oil to secure vast gas reserves. | The strategy of leveraging natural gas competency as the entry point to hydrogen was validated. The company doubled down on its feedstock advantage. |

| Weakness | Low annual spend (~$50 million) on low-carbon ventures. Hydrogen projects remained in the Mo U/evaluation stage. | Massive capital ($9 B+) allocated to conventional projects like Willow, while hydrogen capital remains comparatively minimal. No FID on a major hydrogen project. | The gap between stated hydrogen ambition and actual capital deployment widened, confirming a cautious, follower-not-leader position. |

| Opportunity | The Inflation Reduction Act (IRA) was passed, enhancing 45 Q tax credits for CCUS. Secured an offtake agreement with Uniper. | Continued global demand growth for US LNG solidified the economic case for the feedstock value chain. Growing demand in Europe and Asia for low-carbon ammonia. | The commercial case for the U.S. Gulf Coast ammonia project strengthened due to both policy support and clear market demand signals. |

| Threat | Competitors like Exxon Mobil and Shell announced large-scale low-carbon business units and capital plans. | Analysts expect FIDs on major U.S. blue hydrogen projects by year-end 2025, but Conoco Phillips has not announced its participation in one. | The risk of being outpaced by more aggressive competitors became more pronounced as others moved toward project execution while Conoco Phillips focused on feedstock. |

2026 Outlook: Will Conoco Phillips Move from Strategy to Execution?

The single most critical development to watch for in 2026 is a Final Investment Decision (FID) on the U.S. Gulf Coast ammonia facility. Such a move would mark the company’s transition from a phase of strategic positioning to one of active project execution in the hydrogen economy, validating its long-term, infrastructure-led approach.

ConocoPhillips Aims for Net Zero by 2050

The company’s official net-zero trajectory provides the high-level ambition that frames the detailed SWOT analysis, representing the ultimate goal its hydrogen initiatives support.

(Source: ConocoPhillips)

- If an FID is announced, watch for a corresponding, multi-billion dollar increase in the company’s “Low Carbon Technologies” capital expenditure budget in subsequent financial reports. This will be the clearest signal of a genuine strategic shift.

- If no FID materializes by the end of 2026, it would suggest that the project’s economics are not yet favorable enough to compete for capital against conventional oil and gas projects, signaling a continued prioritization of near-term shareholder returns over first-mover advantage in hydrogen.

- The formation of new, dedicated CCUS infrastructure partnerships on the Gulf Coast would be a leading indicator of progress toward an FID, as securing reliable CO 2 transportation and storage is the primary technical and commercial hurdle for the project.

Frequently Asked Questions

What is Conoco Phillips’ main strategy for entering the blue hydrogen market?

Conoco Phillips’ strategy is to leverage its core competencies in natural gas and LNG as a foundational pillar for future low-carbon ventures. It treats blue hydrogen as a “low-carbon adjacency” to its primary business, focusing first on securing the natural gas feedstock and strengthening its LNG infrastructure before committing major capital to hydrogen production projects. This is described as a cautious, infrastructure-first approach.

Why is Conoco Phillips spending so much more on oil and gas than on hydrogen projects?

Conoco Phillips’ capital allocation strategy for 2025-2026 prioritizes maximizing returns from its traditional hydrocarbon assets. For example, it invested an estimated $9 billion in the Willow oil project and $22.5 billion to acquire Marathon Oil, compared to an annual spend of about $50 million on all low-carbon initiatives. This financial posture indicates that securing the natural gas feedstock for future blue hydrogen is the immediate priority, and the company is waiting for market and policy conditions to mature before making larger hydrogen investments.

How do partnerships with companies like JERA, Uniper, and the acquisition of Marathon Oil fit into the hydrogen plan?

These moves are sequential steps in building a complete value chain. The acquisition of Marathon Oil bolsters the natural gas supply, which is the essential feedstock for blue hydrogen. The foundational partnership with JERA is to develop the production facility itself, while the agreement with Uniper as a major offtaker de-risks the project by securing a future customer for the low-carbon ammonia.

Why is the U.S. Gulf Coast central to Conoco Phillips’ hydrogen ambitions?

The U.S. Gulf Coast is the strategic focus because it offers a unique combination of Conoco Phillips’ existing natural gas infrastructure, favorable geology for Carbon Capture, Utilization, and Storage (CCUS), and direct access to global export markets for both LNG and future ammonia. The company’s flagship ammonia project with JERA is planned for this region.

What is the most critical milestone to watch for by 2026 regarding Conoco Phillips’ hydrogen strategy?

The single most critical development to watch for is a Final Investment Decision (FID) on the U.S. Gulf Coast ammonia facility. An FID would signify the company’s transition from strategic positioning to active project execution and would be the clearest signal that the project’s economics are favorable enough to compete for capital against conventional oil and gas projects.