AI Manufacturing Constraint 2026: Why TSMC’s Sold-Out Capacity Is the Real AI Growth Governor

AI Hardware Risk 2026: How Manufacturing Capacity Became the Primary Choke Point

The principal risk to the artificial intelligence sector’s growth is no longer chip design but the physical manufacturing capacity for advanced semiconductor packaging and high-bandwidth memory (HBM). Insatiable demand has created a multi-year structural bottleneck, with Taiwan Semiconductor Manufacturing Company’s (TSMC) proprietary Chip-on-Wafer-on-Substrate (Co Wo S) technology and the HBM supply chain acting as the primary governors on AI hardware deployment through 2027. This constraint directly limits the pace of AI infrastructure build-out and intensifies supply chain concentration risk.

- Prior to 2024, the industry focus was on the performance of individual AI accelerators. The shift began as generative AI scaled, exposing the manufacturing process itself as the weak link. Between January 2025 and today, this has solidified into a crisis, with reports confirming TSMC’s Co Wo S capacity is sold out through 2026 and into 2027. Demand is reportedly three times the available supply, transforming advanced packaging from a commodity to a strategic, sovereign-class asset.

- The problem is a dual constraint of packaging and memory. HBM production is acutely resource-intensive, consuming approximately three times the wafer factory capacity per wafer compared to standard DDR 5 DRAM. This has forced memory producers like SK Hynix and Micron to reallocate production, leading them to declare their HBM supply sold out through 2025. This HBM shortage independently throttles GPU manufacturing, compounding the Co Wo S bottleneck.

- This scarcity has created a highly concentrated market where a few dominant players have secured the vast majority of future supply. Top-tier customers, including NVIDIA, AMD, Broadcom, and Google, have reportedly locked in over 85% of TSMC’s total Co Wo S capacity for 2026. This leaves less than 15% for all other AI chip companies, creating a significant barrier to entry and competition.

- The reallocation of resources toward high-margin HBM has triggered a cascading supply shortage across the broader electronics market. This impacts conventional DRAM and NAND flash, driving up component costs for PCs, smartphones, and non-AI servers. In early 2026, both HP and Lenovo signaled impending price hikes on commercial devices, directly attributing them to the memory crunch caused by the AI boom.

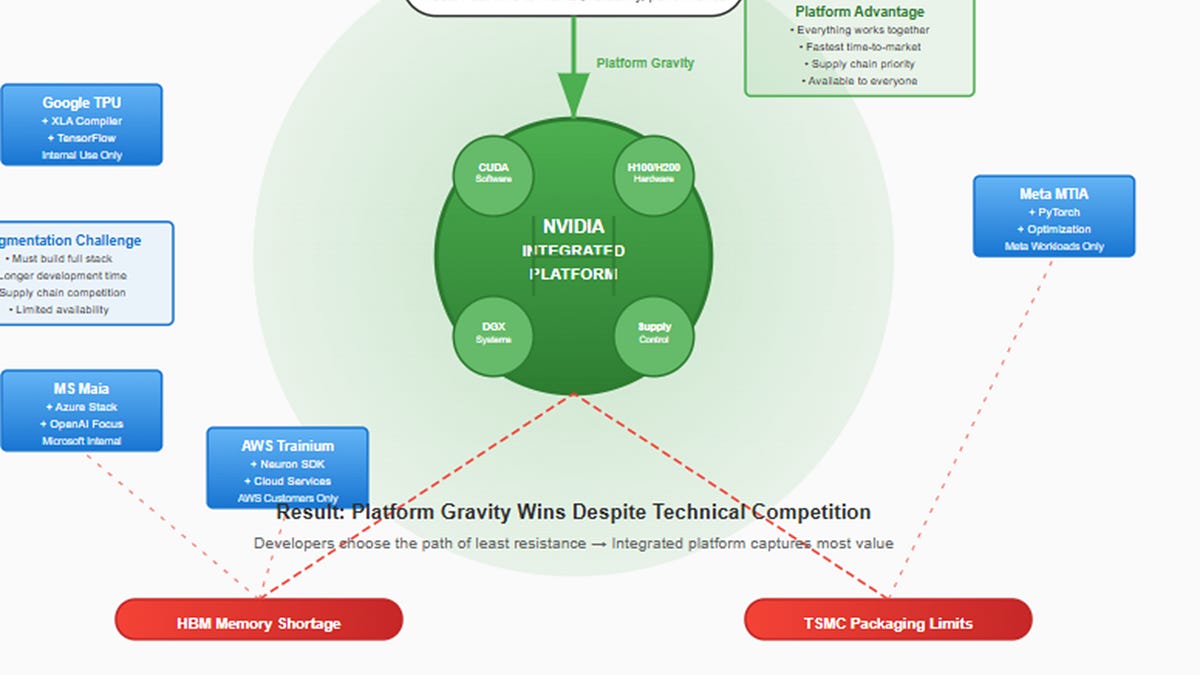

NVIDIA Platform Faces Key Supply Bottlenecks

This diagram visually defines the article’s core thesis by identifying the two primary choke points—HBM memory and TSMC packaging limits—that constrain the AI hardware sector.

(Source: Kristal Lens by Kristal.AI)

Strategic Alliances 2026: Reshaping the AI Supply Chain Amid Co Wo S Scarcity

The intense and prolonged capacity shortage is forcing AI chip designers to forge new and unconventional alliances to de-risk their supply chains, moving beyond a sole reliance on TSMC. These partnerships are reshaping the competitive dynamics of the semiconductor industry, elevating the strategic importance of alternative foundries and Outsourced Semiconductor Assembly and Test (OSAT) firms.

- NVIDIA, the largest consumer of Co Wo S capacity, has been forced to seek alternatives to secure its aggressive growth targets. In early 2024, reports emerged that NVIDIA was in discussions with Intel to use its advanced packaging services, including its EMIB technology. A high-volume deal would mark a monumental shift in the foundry landscape, validating Intel as a credible alternative to TSMC.

- The crisis is fostering deeper integration between previously distinct parts of the supply chain. In mid-2025, SK Hynix and TSMC announced a collaboration to produce next-generation HBM 4 memory. This alliance aims to co-optimize the integration of memory stacks with logic chips at the foundry level, signaling a future where memory and packaging are designed in tandem.

- The supply overflow from TSMC has created a significant opportunity for OSATs. U.S. AI chipmakers are reportedly turning to firms like Powertech Technology Inc. (PTI) and ASE Technology for Co Wo S-like packaging solutions. These engagements, expected to run through 2027, are elevating OSATs from simple back-end service providers to strategic partners in the AI hardware ecosystem.

- Hyperscalers are also engaging directly in the packaging supply chain to secure capacity for their custom silicon. Forecasts for 2026 show AWS, in partnership with chip designer Alchip, is expected to dramatically increase its consumption of Co Wo S capacity after a dip in 2025, indicating a direct strategy to secure this critical resource for its own AI infrastructure plans.

Table: Key Strategic Partnerships in Advanced Packaging and HBM (2024-2026)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| SK Hynix & TSMC | June 2025 | Announced a collaboration to co-develop and produce next-generation HBM 4 memory. The partnership aims to optimize HBM integration with logic chips, addressing performance and thermal management challenges for future AI accelerators. | Granite Shares |

| NVIDIA & Intel (Reported) | Jan 2024 | Reports indicated NVIDIA turned to Intel Foundry Services to secure advanced packaging capacity. This move is a direct response to the Co Wo S bottleneck at TSMC and would serve as a critical second-sourcing strategy. | Tech Power Up |

| U.S. AI Chipmakers & Powertech (PTI) | Nov 2025 | Reports indicate that the Co Wo S capacity crunch at TSMC has pushed U.S. AI chipmakers to engage with OSATs like PTI for packaging solutions, with orders reportedly extending through 2027. | Trend Force |

| NVIDIA & Samsung (Struggles) | May 2025 | Reports note that Samsung has consistently struggled with HBM validation on NVIDIA’s platforms. Successful validation would introduce a major new HBM supplier, but persistent challenges have limited supply diversification. | CWNewsroom |

Geographic Concentration: How Taiwan’s Dominance Shapes Global AI Risk

The global AI hardware supply chain is critically dependent on a single geographic location, Taiwan, creating significant systemic risk. This concentration in advanced packaging, controlled almost exclusively by TSMC, has become a central point of failure for the entire industry and is prompting nascent but urgent diversification efforts, primarily led by the United States.

Geopolitical Risk Fragments Semiconductor Supply Chain

This map directly illustrates the geographic risk discussed in the section, visualizing a fragmented global supply chain and symbolizing the risk of depending on specific regions like Taiwan.

(Source: Medium)

- Between 2021 and 2024, Taiwan’s central role in semiconductor manufacturing was well-established, but the acute geopolitical risk was less of a daily operational concern for the AI sector. From 2025 onward, this geographic concentration has transformed into the industry’s single largest strategic vulnerability. With the vast majority of Co Wo S packaging performed in Taiwan, any disruption could halt the global supply of high-end AI accelerators.

- The United States is actively trying to mitigate this risk through policy and industrial strategy. The CHIPS and Science Act is a key mechanism, with a notable grant of $458 million awarded to SK Hynix in December 2024 to support its advanced packaging and HBM production facility in the U.S. This directly targets the two primary bottlenecks with a diversification objective.

- The rise of Intel Foundry Services represents the most significant U.S.-based effort to create a viable alternative to TSMC’s dominance. By positioning its fabs and packaging facilities in the U.S. and Europe, Intel is offering a geographically diversified supply chain as a key part of its value proposition to AI chipmakers wary of the concentration in Taiwan.

- Simultaneously, U.S. export controls aimed at China are forcing a potential fragmentation of the global supply chain. While these controls limit China’s access to leading-edge technology like Co Wo S, they are also accelerating China’s drive to build a fully independent domestic semiconductor ecosystem. This could lead to a bifurcated global market with separate standards and supply chains over the long term.

Manufacturing at Scale: The Technology Maturity Challenge Beyond Chip Innovation

The core technologies underpinning the AI hardware boom, Co Wo S packaging and HBM, are at a high level of technical maturity (TRL 9). The current crisis is not a failure of innovation but a challenge of industrial-scale manufacturing. The bottleneck has shifted from designing better chips to developing the processes, materials, and equipment needed to produce them in unprecedented volumes.

TSMC Ramps Up AI Chip Production Through 2026

This forecast exemplifies the “manufacturing at scale” challenge, showing how a key supplier, TSMC, is ramping up production of next-generation chips to meet unprecedented demand.

(Source: Webull)

- During the 2021-2024 period, the industry’s primary focus was on refining the performance and architecture of Co Wo S and HBM to enable more powerful chips. From 2025 to today, the challenge has pivoted to manufacturability. The critical problem is no longer what can be built, but how many can be built. This is reflected in TSMC’s aggressive Co Wo S capacity expansion, aiming to ramp from ~35, 000 wafers per month (wpm) in 2024 to a target of over 120, 000 wpm by late 2026.

- In response to scaling limitations, the industry is already developing the next generation of packaging. TSMC is working on larger interposers, targeting 5.5 times the current maximum field of view (reticle size) in 2026 and 9.5 times in 2027. This will enable single packages to contain 12 or more HBM stacks, a direct response to the demands of future AI models.

- The bottleneck is moving further down the supply stack to raw materials. A critical constraint has emerged in the supply of ultra-rigid glass fabric, an essential component for the substrates used in Co Wo S packaging. The primary Japanese supplier is reportedly sold out until 2027, making the ability of second-source suppliers like Taiwan Glass to ramp up production a key dependency for the entire ecosystem.

- Alternative packaging technologies are being developed to address future scaling needs. Innovations like Co Po S (Chip-on-Panel-on-Substrate) and System-on-Wafer (So W) aim to create even larger and more complex integrated systems. TSMC is targeting its Co W-So W technology for mass production in 2027, indicating the long-term roadmap to overcome today’s physical limitations.

SWOT Analysis 2026: Navigating the AI Hardware Manufacturing Bottleneck

The AI hardware market is defined by a powerful combination of immense demand and severe structural limitations. An analysis of its strengths, weaknesses, opportunities, and threats reveals a sector where pricing power is concentrated among a few gatekeepers, but where the very constraints on growth are creating openings for new competitors and technologies.

Table: SWOT Analysis for the AI Advanced Packaging & Memory Market

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong demand for AI chips from early adopters. NVIDIA’s established market leadership. | Explosive, “infinite” demand from hyperscalers. Extreme pricing power for NVIDIA (H 100 GPUs at $30, 000+) and TSMC. Pre-booking of capacity years in advance. | The value capture shifted from just the chip designer to the capacity holder. Demand was validated as structural, not cyclical. |

| Weaknesses | General semiconductor supply chain issues (post-COVID). Dependence on TSMC for leading-edge nodes. | Acute and specific bottlenecks in Co Wo S packaging and HBM memory. Extreme supplier concentration in Taiwan. Multi-year lead times for new capacity expansion. | The primary weakness moved from general front-end wafer supply to highly specific back-end packaging and memory integration, a much harder problem to solve quickly. |

| Opportunities | Development of custom ASICs by hyperscalers. Growth of AI applications. | Rise of credible alternative packaging suppliers (Intel Foundry Services, OSATs like ASE). Development of new materials (glass substrates) and technologies (Co Po S, So W). Massive investment in “picks and shovels” suppliers. | The bottleneck created a massive economic incentive for competitors to enter the high-margin advanced packaging market, threatening TSMC’s near-monopoly. |

| Threats | U.S.-China trade tensions. Potential for cyclical downturn in semiconductor demand. | Direct geopolitical risk to Taiwan. The bottleneck shifting downstream to power, cooling, and data center racks. A potential cooling of AI demand if ROI diminishes or if the power crisis stalls deployments. | The primary threat evolved from a market risk (demand drop) to a physical infrastructure and geopolitical risk (supply disruption or inability to power the hardware). |

Forward Outlook: Will the AI Manufacturing Bottleneck Ease or Shift by 2027?

The single most critical factor to monitor over the next 18 months is not AI model development, but the real-world execution of advanced packaging capacity expansion by players outside of TSMC. A success in this area, particularly from Intel, would signal the beginning of a rebalancing of the supply chain. A failure will prolong the current hardware-constrained environment and intensify the search for less hardware-intensive AI architectures. Meanwhile, the bottleneck is already showing signs of migrating downstream to energy and physical infrastructure.

HBM Supply Shortage Projected to Last Until 2027

This graphic directly answers the forward-looking question posed by the section, indicating that the critical High-Bandwidth Memory (HBM) supply bottleneck is expected to persist until 2027.

(Source: AI CERTs)

- Bull Signal for Supply Easing: If Intel Foundry Services publicly announces a high-volume advanced packaging win for a flagship AI product from a customer like NVIDIA or AMD by mid-2026, it would validate the viability of a second source and signal a loosening of the chokehold. This would be the most significant catalyst for alleviating the current constraint.

- Bear Signal for Prolonged Shortage: Continue to monitor TSMC’s quarterly earnings for specific figures on Co Wo S wafer-per-month output. Any downward revision or delay in meeting their expansion targets for late 2026 would confirm that the shortage will extend well beyond 2027, maintaining high prices and long lead times.

- Signal of a Shifting Bottleneck: The most important forward-looking indicator is the narrative from hyperscalers like Microsoft, Google, and Meta. Watch for their commentary in earnings calls to shift from a focus on securing GPUs to the challenge of securing sufficient power for their data centers. An increasing mention of gigawatt-scale power purchase agreements, grid interconnection queues, and advanced cooling will confirm the primary constraint is moving from manufacturing to infrastructure.

Frequently Asked Questions

Why is there a bottleneck in AI hardware production if chip designs keep improving?

According to the analysis, the primary bottleneck is no longer chip design but the physical manufacturing capacity for two key components: advanced packaging, specifically TSMC’s CoWoS technology, and high-bandwidth memory (HBM). Demand for these components is reported to be three times the available supply, with TSMC’s CoWoS capacity sold out through 2026 and HBM supply from major producers sold out through 2025.

How does the AI chip shortage affect consumer electronics like PCs and smartphones?

The intense demand for HBM for AI has forced memory producers like SK Hynix and Micron to reallocate their production capacity away from conventional memory. This has triggered a cascading supply shortage of standard DRAM and NAND flash, driving up component costs for PCs, smartphones, and non-AI servers. The report notes that companies like HP and Lenovo signaled price hikes on their devices in early 2026, directly attributing them to this memory crunch.

Are companies just waiting for TSMC to build more factories, or are there other solutions being pursued?

Companies are actively pursuing alternatives to de-risk their supply chains. NVIDIA is reportedly in talks to use Intel’s advanced packaging services. U.S. chipmakers are engaging with Outsourced Semiconductor Assembly and Test (OSAT) firms like Powertech Technology Inc. (PTI) for CoWoS-like solutions. Additionally, collaborations are forming, such as the one between SK Hynix and TSMC to co-develop next-generation HBM4 memory.

Besides manufacturing capacity, what is the biggest risk to the AI hardware supply chain?

The article identifies extreme geographic concentration as the single largest strategic vulnerability. The vast majority of advanced packaging, particularly CoWoS, is performed in Taiwan. This dependency on a single geographic location creates significant systemic risk for the global AI industry, as any disruption in Taiwan could halt the supply of high-end AI accelerators worldwide.

If the manufacturing bottleneck is solved, what is the next major challenge for the AI industry?

The analysis suggests the bottleneck is already showing signs of shifting downstream to physical infrastructure. The next primary constraint on AI growth is expected to be securing sufficient energy and advanced cooling for data centers. The article advises watching for hyperscalers to shift their focus from acquiring GPUs to securing gigawatt-scale power agreements and deploying advanced liquid cooling, which would confirm this trend.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.