AI’s 100 k W Rack Crisis: How Strategic Partnerships Cement Liquid Cooling as Mandatory for 2026

Strategic Partnerships Accelerate Mandatory Liquid Cooling Adoption for 2026 AI Data Centers

Major technology and infrastructure players are forming critical alliances, moving liquid cooling from a niche solution before 2024 to a mainstream, co-developed standard essential for deploying high-density AI infrastructure in 2026. This shift from aftermarket components to integrated ecosystems, driven by chip manufacturers, makes liquid cooling a prerequisite for all new AI-focused data centers.

- Before 2025, the liquid cooling market was characterized by specialized vendors providing solutions for high-performance computing (HPC) and early AI adopters. The approach was largely fragmented, with data center operators sourcing cooling as a separate component to manage densities that were only beginning to exceed the limits of air cooling.

- The period from January 2025 to today marks a fundamental restructuring of the market. The problem is no longer just managing heat; it is about enabling the performance of next-generation hardware. This has forced chip designers, server manufacturers, and infrastructure providers into tight collaboration to ensure their products are viable.

- Recent partnerships directly link chip-level requirements to facility-level infrastructure. The collaboration between Chemours and 2 CRSi, announced in February 2026, aims to accelerate two-phase liquid cooling, while major players like Vertiv are launching modular solutions like the Mega Mod HDX in January 2026 specifically to meet pre-defined, high-density compute requirements from the start.

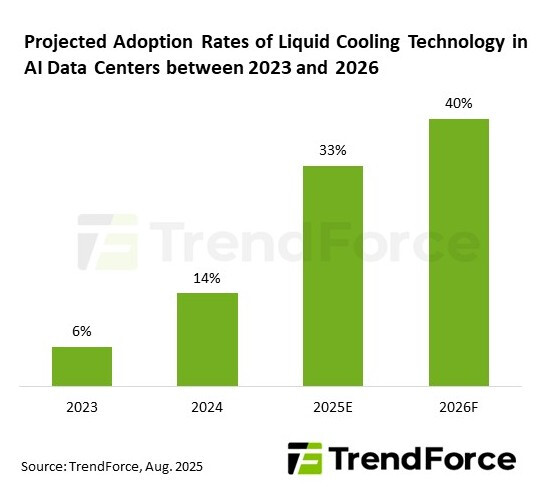

AI Pushes Liquid Cooling Adoption to 40% by 2026

This chart directly visualizes the section’s core argument, showing the rapid, mandatory adoption of liquid cooling in AI data centers forecasted to hit 40% by 2026.

(Source: TechPowerUp)

Investment and Deployments: Capital Flows Confirm the Liquid Cooling Mandate

A surge in both venture capital for startups and large-scale corporate investment into liquid cooling infrastructure confirms market confidence and accelerates the technology’s deployment to meet the urgent demands of AI. This financial validation, moving from funding R&D before 2024 to financing full-scale commercial deployments today, underscores the technology’s non-negotiable role in the current $7 trillion data center capital cycle.

Liquid Cooling Market Growth Signals Strong Investment

Projecting a market size of $20.7 billion, this chart quantifies the surge in capital flows and investment confidence that is validating liquid cooling as a mandated technology.

(Source: Market.us Scoop)

- Prior to 2024, investments were focused on early-stage innovation, with venture capital backing startups like Jet Cool, which raised $17 million in October 2023 to develop its technology. This funding targeted the development of novel cooling modules rather than their widespread implementation.

- From 2024 onward, capital allocation shifted dramatically towards deployment and scale. In September 2024, Liquid Stack secured $20 million from Tiger Global specifically to scale its AI cooling offerings, signaling investor focus on companies with proven commercial products ready for the growing market.

- The most significant signal of this shift is the move to large-scale infrastructure projects. In November 2024, Elea Data Centers announced a $300 million investment to deploy liquid cooling for AI in Brazil, in partnership with Vertiv. This represents a major commitment to building liquid-first data centers at a national scale, confirming the technology’s status as a bankable utility.

Table: Key Investments and Deployments in Data Center Liquid Cooling

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Elea Data Centers & Vertiv | November 2024 | Announced a $300 million investment for the first large-scale liquid cooling deployment for AI data centers in Brazil, establishing a blueprint for emerging markets. | JSA.net |

| Liquid Stack | September 2024 | Secured $20 million in an investment round led by Tiger Global to scale its liquid cooling solutions specifically for the AI market. | Liquid Stack |

| Jet Cool | October 2023 | Raised $17 million in a Series A funding round led by Bosch Ventures to scale its liquid cooling technology and meet rising demand from the AI sector. | Jet Cool |

Critical Alliances: How NVIDIA, Vertiv, and Schneider Electric Redefined AI Cooling Standards

Strategic partnerships formed since late 2024 have fundamentally reshaped the AI infrastructure market, with hardware leaders like [NVIDIA] mandating liquid cooling through collaborations with power and thermal management giants. This shift standardizes liquid cooling as a non-negotiable, pre-integrated component for next-generation data centers, a stark contrast to the siloed, aftermarket approach that defined the industry before 2024.

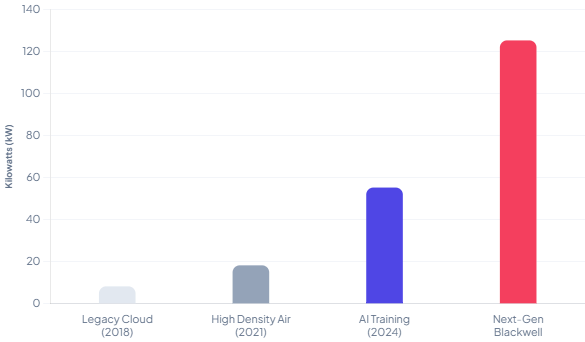

Exploding AI Power Density Drives New Cooling Standards

This chart shows the massive jump in rack power density from next-gen AI platforms, explaining why critical alliances with partners like NVIDIA are necessary to redefine cooling standards.

(Source: Global Data Center Hub)

- The alliance between Schneider Electric and NVIDIA, announced in December 2024, was a pivotal moment. By co-developing reference designs for AI data centers, the partnership transformed liquid cooling from a custom-engineered solution into a replicable, standardized blueprint, drastically reducing design complexity and accelerating deployment timelines.

- Vertiv formalized its partnership with NVIDIA in May 2024, focusing on creating advanced cooling solutions for the most demanding AI workloads. This collaboration also extends to the U.S. government’s COOLERCHIPS program, institutionalizing liquid cooling as a core technology for both public and private sector high-performance computing.

- These top-level alliances are proven to be commercially viable through large-scale deployments. The partnership between Elea Data Centers and Vertiv, which led to a $300 million project in Brazil, demonstrates that reference designs are successfully translating into tangible infrastructure investments globally.

Table: Strategic Partnerships Driving Liquid Cooling Standardization

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Chemours & 2 CRSi | February 2026 | Collaboration to qualify and accelerate the deployment of two-phase immersion cooling fluids for high-density servers, targeting up to a 90% reduction in cooling energy. | PR Newswire |

| Schneider Electric & NVIDIA | December 2024 | Partnership to develop and release the first publicly available reference designs for AI data centers, optimizing infrastructure for high-density GPU clusters. | Techzine |

| Vertiv & NVIDIA | May 2024 | Formalized partnership to develop advanced, full-stack cooling solutions for AI, including participation in the government’s COOLERCHIPS program. | Vertiv |

From Niche to Global Standard: North America and Europe Lead 2026 Liquid Cooling Deployments

While North America remains the dominant market for liquid cooling adoption driven by its hyperscale leadership, significant investments and regulatory pressures in Europe are accelerating its deployment, with new projects in South America signaling a rapid global expansion of the technology. Before 2024, liquid cooling was a niche solution concentrated in North American HPC sites; by 2026, it will be a global standard for AI.

North America Leads Global Liquid Cooling Market

This forecast confirms North America’s market dominance with a 35% share, directly supporting the section’s analysis of regional leadership in the global expansion of liquid cooling.

(Source: Data Center POST)

- North America continues to lead the market, accounting for a projected 46% market share by 2025. This is driven by the region’s concentration of AI developers and hyperscale operators, who are the primary consumers of high-density hardware from companies like NVIDIA and require solutions capable of handling the [AI power crisis].

- Europe’s adoption is uniquely propelled by stringent regulations. Germany’s Energy Efficiency Law, effective from 2025–2026, establishes strict targets for Power Usage Effectiveness (PUE) and mandates heat reuse. These requirements make liquid cooling, with its superior efficiency, a tool for compliance, not just performance.

- The global expansion of liquid-cooled AI infrastructure is validated by significant projects in new markets. The $300 million Elea Data Centers project in Brazil, announced in late 2024, confirms that liquid cooling is not confined to established data center hubs and is being deployed at scale to build sovereign AI capabilities worldwide.

Technology Maturity: Commercial Scale Achieved for Direct-to-Chip and Immersion Cooling

Liquid cooling has decisively moved past the R&D phase, with Direct-to-Chip (D 2 C) emerging as the “gold standard” for immediate mass deployment and immersion cooling maturing for extreme-density applications. This dual-pronged maturation ensures that proven commercial solutions are available today to address the full spectrum of the 100 k W rack crisis, a significant advancement from the experimental phase prior to 2024.

Liquid Cooling Is Essential for High-Density Racks

This chart proves the section’s thesis on technology maturity by mapping cooling solutions to power density, showing liquid cooling is the required standard for racks over 50kW.

(Source: Compu Dynamics)

- Before 2025, liquid cooling, particularly full immersion, was often considered an experimental technology reserved for niche supercomputing applications. While D 2 C was gaining traction, it was not yet a default design choice and required significant custom integration.

- In 2025 and 2026, D 2 C has become the most widely adopted method for new AI racks, validated by its incorporation into reference designs by NVIDIA and comprehensive product portfolio launches from major server manufacturers like ASUS. It is now the primary solution for cooling racks in the 50 k W to 150 k W range.

- Immersion cooling is now being commercially deployed for the most extreme densities exceeding 100 k W. The launch of Infinium’s Edge™ platform in January 2026 for immersion cooling and TCO models showing a 39% cost reduction for a 10 MW AI data center confirm its economic and operational viability for the highest-end AI workloads.

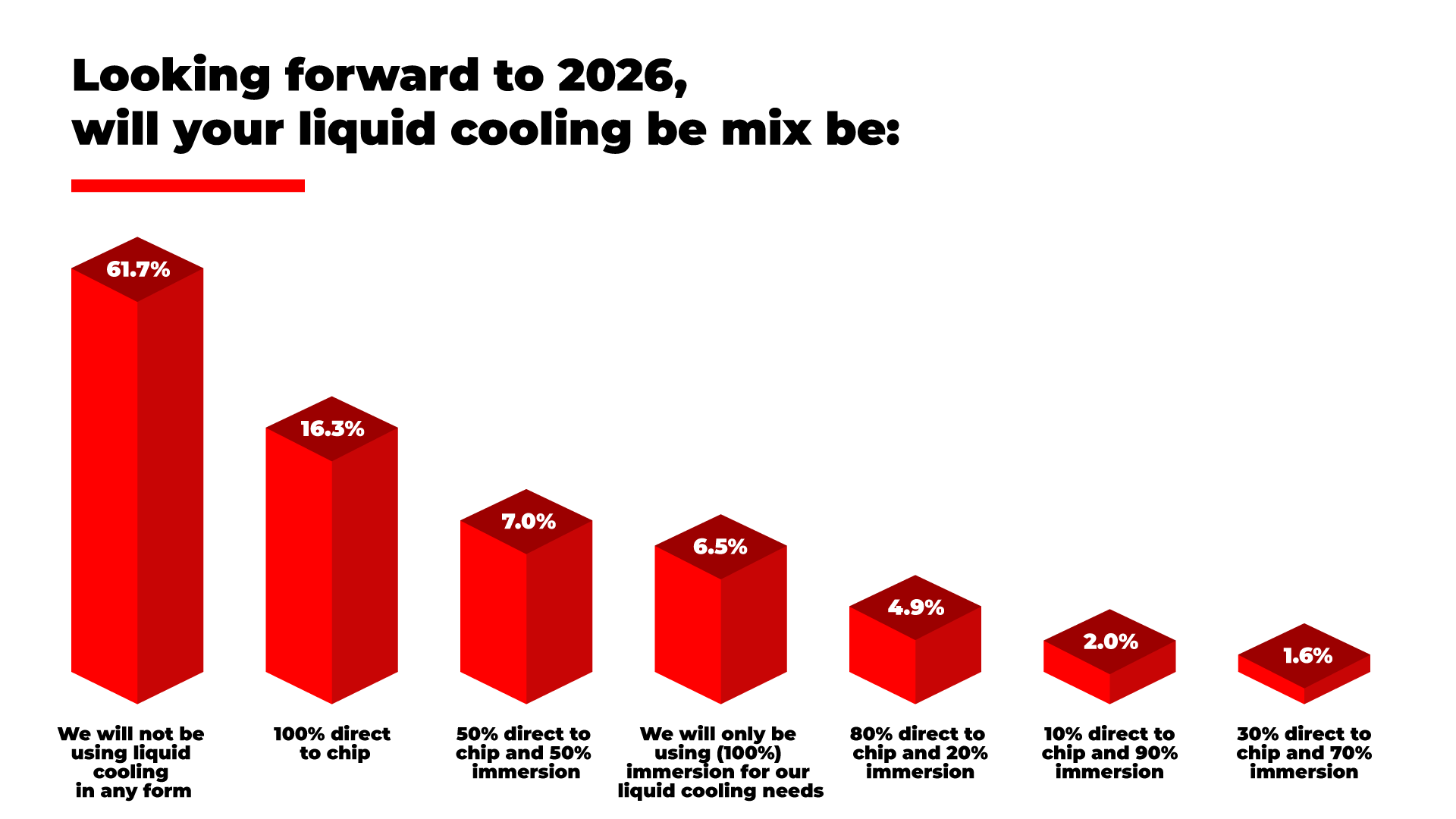

2026 Outlook: Supply Chain Bottlenecks Will Define Liquid Cooling Rollout Speed

If the supply chain for critical liquid cooling components like Coolant Distribution Units (CDUs), manifolds, and connectors cannot scale to meet the exponential demand from AI, data center construction timelines will face significant delays. This will create a major bottleneck for AI capacity expansion in 2026, irrespective of the capital available for investment.

Survey Reveals Potential Lag in Liquid Cooling Rollout

This survey supports the section’s theme of potential bottlenecks, showing that a majority of organizations do not plan to adopt liquid cooling by 2026, indicating a possible disconnect between need and implementation.

(Source: The Register: Enterprise Technology News and Analysis)

- If this happens: Data center operators will face extended lead times for essential cooling hardware, creating a direct conflict with the aggressive deployment schedules for new AI clusters. This could delay revenue generation and cede market share to competitors with more secure supply chains.

- Watch this: Monitor the lead times and pricing for high-capacity CDUs and quick-disconnect couplings from key vendors like Vertiv, Schneider Electric, and their component suppliers. A sustained increase in delivery times from weeks to months will be the primary indicator of a systemic supply-demand imbalance.

- These could be happening: Hyperscalers may begin to acquire or sign long-term, high-volume exclusivity agreements with liquid cooling component manufacturers to de-risk their buildouts. Furthermore, expect accelerated standardization efforts around D 2 C connectors and fluid specifications to simplify the supply chain and enable multi-sourcing.

Frequently Asked Questions

Why is liquid cooling becoming mandatory for new AI data centers by 2026?

Next-generation AI hardware is creating a ‘100 kW rack crisis’ where racks generate far more heat than traditional air cooling can handle. As a result, chip manufacturers like NVIDIA are collaborating with infrastructure partners to make liquid cooling a pre-integrated, standard requirement to ensure the performance and viability of their high-density products.

What has changed in the liquid cooling market since 2024?

Before 2024, liquid cooling was a niche, aftermarket component sourced separately. Since 2025, the market has shifted to an integrated ecosystem model. This is driven by strategic partnerships between chip designers (NVIDIA), server manufacturers, and infrastructure providers (Vertiv, Schneider Electric) who now co-develop standardized cooling solutions as part of the initial data center design.

Which type of liquid cooling is being adopted most widely?

Both Direct-to-Chip (D2C) and immersion cooling are maturing for different needs. D2C has emerged as the ‘gold standard’ for immediate mass deployment on new AI racks in the 50 kW to 150 kW range. Full immersion cooling is now being commercially deployed for the most extreme-density applications exceeding 100 kW.

What evidence shows that this shift to liquid cooling is actually happening?

The shift is confirmed by a surge in large-scale capital investments moving from R&D to deployment. Key examples include Elea Data Centers’ $300 million investment with Vertiv for a liquid-cooled AI facility in Brazil (November 2024) and Liquid Stack securing $20 million to scale its commercial AI cooling solutions (September 2024), validating market confidence.

What is the biggest risk to the widespread deployment of liquid cooling by 2026?

The biggest risk is a supply chain bottleneck. The article warns that if the manufacturing of critical components like Coolant Distribution Units (CDUs), manifolds, and connectors cannot scale to meet exponential demand, it will cause significant delays in data center construction and AI capacity expansion, regardless of the capital available.