Top 10 Nuclear and Solar Deals: Meta’s 2.6 GW Vistra PPA & Microsoft’s 10.5 GW Framework (2025-2026)

The dominant trend in data center energy procurement is a strategic pivot from a singular focus on intermittent renewables to securing massive quantities of 24/7, firm, carbon-free power, with nuclear energy emerging as a cornerstone technology. The relentless energy demand from Artificial Intelligence has forced hyperscalers to move beyond traditional Power Purchase Agreements (PPAs) and sign multi-gigawatt, multi-decade nuclear offtake agreements to ensure grid stability and achieve decarbonization goals. This is clearly demonstrated by Meta’s landmark 2.6 GW deal with Vistra and Amazon’s expanded 1.9 GW nuclear PPA. The theme for 2025-2026 is the pursuit of a reliable, baseload power portfolio, where record-breaking renewable deals, like Microsoft’s 10.5 GW framework, are now complemented by equally large investments in firm capacity to power the future of AI.

1. Meta & Alliant Energy Service Agreement (May 2026)

Company: Meta Platforms Inc.

Installation Capacity: 370 MW

Applications: Powering data centers

Source: Wisconsin PSC approves Alliant-Meta power deal

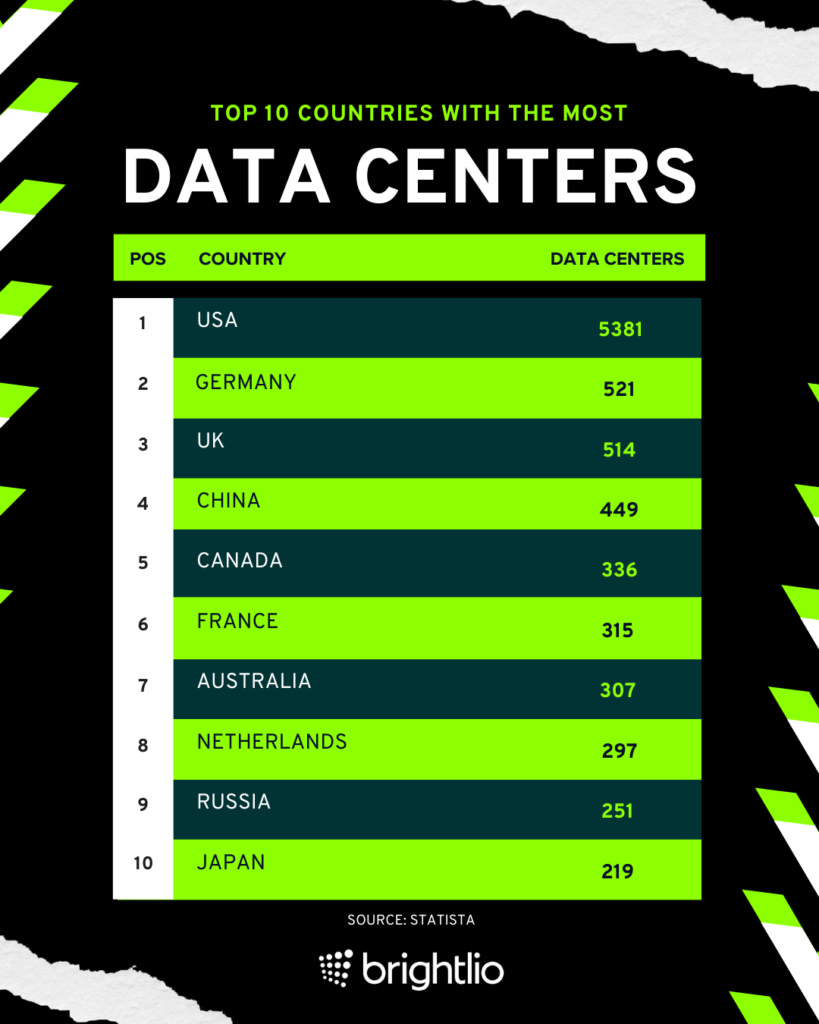

USA Dominates Global Data Center Landscape

As the first specific deal listed in the document, this chart provides broad, high-level context. It establishes the United States’ leading position in the global data center market, explaining why a significant number of major power agreements, like this one, are centered in the US.

(Source: Brightlio)

2. Meta Pennsylvania Solar PPA (March 2026)

Company: Meta Platforms Inc.

Installation Capacity: 80 MW

Applications: Powering regional data centers

Source: Meta Strikes 80 MW Solar Deal to Power Data Centers and Cut …

3. Google & Total Energies Texas Solar PPA (February 2026)

Company: Google (Alphabet Inc.)

Installation Capacity: 1, 000 MW (1 GW)

Applications: Powering data centers in Texas

Source: Total Energies to Provide 1 GW of Solar Capacity to Power Google’s …

4. Meta & Vistra Nuclear PPA (January 2026)

Company: Meta Platforms Inc.

Installation Capacity: 2, 600 MW (2.6 GW)

Applications: Powering AI infrastructure and data centers

Source: Data Center Power & Energy News 2026: Weekly Project Updates

US Data Center Power Demand to Surge

The section describes a significant solar PPA by Google. The chart, with its general headline about surging US data center power demand, provides the fundamental business reason for this deal, as the growing demand necessitates proactive power procurement by hyperscalers.

(Source: Electric Choice)

5. Meta & ENGIE Solar PPA (October 2025)

Company: Meta Platforms Inc.

Installation Capacity: 600 MW

Applications: Powering data center footprint

Source: ENGIE and Meta strengthen their partnership with a major …

6. Meta & Enbridge Texas Solar PPA (July 2025)

Company: Meta Platforms Inc.

Installation Capacity: 600 MW

Applications: Powering data centers in Texas

Source: Meta to power Texas data centers with 600-MW solar plant

Meta Data Center Site Planned in Texas

The section details a specific Meta power purchase agreement in Texas. The chart, showing a Meta data center site in the same state, directly connects the abstract power deal to the physical infrastructure it is meant to support.

(Source: POWER Magazine)

7. Microsoft & Brookfield Renewable Energy Framework (July 2025)

Company: Microsoft

Installation Capacity: 10, 500 MW (10.5 GW)

Applications: Powering data centers in the USA & Europe

Source: Power Purchase and Interconnection Agreements for Data Centers

8. Meta & Invenergy Renewable PPA (June 2025)

Company: Meta Platforms Inc.

Installation Capacity: ~800 MW

Applications: Supporting data center operations

Source: Invenergy to Provide Meta with Nearly 800 MW

9. Meta & Talen Energy Nuclear PPA (June 2025)

Company: Meta Platforms Inc.

Installation Capacity: 1, 121 MW (1.1 GW)

Applications: Powering AI data centers with 24/7 carbon-free power

Source: Amazon, Talen Energy ink nuclear PPA to power data centers with …

US Data Centers Consume 4.4% of Electricity

The section details a nuclear PPA, a move towards securing 24/7 power. This chart quantifies the current, significant energy footprint of US data centers, providing a baseline that underscores why companies like Meta are seeking non-intermittent power sources for this already large consumption.

(Source: Electric Choice)

10. Amazon & Talen Energy Nuclear PPA Expansion (June 2025)

Company: Amazon

Installation Capacity: 1, 920 MW

Applications: Powering data centers with carbon-free electricity

Source: Talen Energy Expands Nuclear Energy Relationship with Amazon

Table: Top Data Center Power Deals (2025-2026)

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Meta Platforms Inc. | 370 MW | Powering data centers | Wisconsin PSC approves Alliant-Meta power deal |

| Meta Platforms Inc. | 80 MW | Powering regional data centers | Meta Strikes 80 MW Solar Deal to Power Data Centers and Cut … |

| Google (Alphabet Inc.) | 1, 000 MW (1 GW) | Powering data centers in Texas | Total Energies to Provide 1 GW of Solar Capacity to Power Google’s … |

| Meta Platforms Inc. | 2, 600 MW (2.6 GW) | Powering AI infrastructure and data centers | Data Center Power & Energy News 2026: Weekly Project Updates |

| Meta Platforms Inc. | 600 MW | Powering data center footprint | ENGIE and Meta strengthen their partnership with a major … |

| Meta Platforms Inc. | 600 MW | Powering data centers in Texas | Meta to power Texas data centers with 600-MW solar plant |

| Microsoft | 10, 500 MW (10.5 GW) | Powering data centers in the USA & Europe | Power Purchase and Interconnection Agreements for Data Centers |

| Meta Platforms Inc. | ~800 MW | Supporting data center operations | Invenergy to Provide Meta with Nearly 800 MW |

| Meta Platforms Inc. | 1, 121 MW (1.1 GW) | Powering AI data centers with 24/7 carbon-free power | Amazon, Talen Energy ink nuclear PPA to power data centers with … |

| Amazon | 1, 920 MW | Powering data centers with carbon-free electricity | Talen Energy Expands Nuclear Energy Relationship with Amazon |

Power Procurement Shifts: Hyperscaler Deals Move Beyond Intermittent Renewables

The diversity of these power deals signifies a crucial evolution in corporate energy strategy. While solar and wind remain vital, the deals show a clear recognition of their limitations for powering mission-critical, 24/7 AI workloads. Hyperscalers are now pursuing a sophisticated “all of the above” strategy. Microsoft’s staggering 10.5 GW framework with Brookfield represents the scaled-up, portfolio-level approach to procuring intermittent renewables. Simultaneously, Meta’s multiple nuclear PPAs, totaling over 3.7 GW with Vistra and Talen Energy, and Amazon’s 1.9 GW deal highlight a parallel strategy to secure firm, baseload, carbon-free power. This dual approach indicates that the industry is moving from simply accumulating renewable energy credits to building resilient, truly decarbonized energy portfolios capable of meeting extreme power demands.

Solar & Storage Dominate New US Power Capacity

The section discusses a strategic shift *away* from intermittent renewables. The chart illustrates the current status quo by showing the dominance of solar. This provides essential context by establishing the baseline from which the ‘shift’ mentioned in the heading is occurring.

(Source: Reuters)

USA Dominates Power Deals: Texas, Pennsylvania, and Iowa Emerge as Key Hubs

The geographic concentration of these deals within the United States is telling. States like Texas, Pennsylvania, Ohio, and Iowa are at the epicenter of this trend, driven by a combination of factors. Texas, with its abundant sun and favorable development environment, is a natural fit for massive solar projects like Google’s 1 GW deal with Total Energies and Meta’s 600 MW PPA with Enbridge. Meanwhile, Pennsylvania and Ohio, home to established nuclear fleets, are the logical locations for the landmark nuclear PPAs signed by Meta and Amazon. This concentration is not accidental; it follows the growth of data center alleys in these regions and highlights the critical need for co-locating power generation near the source of demand to avoid grid constraints.

Map Shows High Concentration of US Data Centers

The section highlights key US hubs for power deals, specifically mentioning Texas, Pennsylvania, and Iowa. The chart, a map illustrating the concentration of US data centers, visually reinforces this geographic theme by showing where this power demand is centered.

(Source: Electric Choice)

10.5 GW Frameworks & 2.6 GW PPAs: Microsoft and Meta Showcase Portfolio Maturity

These agreements reveal a significant maturation of energy procurement strategies. The era of one-off, small-scale PPAs is over for hyperscalers. Microsoft’s 10.5 GW deal is not for a single project but a long-term framework to develop a pipeline of assets, demonstrating a strategic move to de-risk development and secure capacity for years to come. Similarly, Meta’s 2.6 GW, 20-year nuclear PPA with Vistra represents a profound shift in commitment. Signing a multi-decade offtake agreement for nuclear power signals a willingness to engage in utility-scale, long-term infrastructure planning, treating energy security as a core business function rather than just a sustainability metric. This level of long-term commitment was previously the domain of utilities, not tech companies.

US Data Center Power Demand to Rise Five-Fold

The section focuses on the immense scale of recent power deals (10.5 GW). The chart provides the underlying driver for these massive procurements by forecasting that power demand will ‘rise five-fold,’ justifying the need for such large-scale energy frameworks.

(Source: WSJ)

Nuclear Power Scenarios: What to Expect After Meta’s 6.6 GW Commitment

The primary strategic action to watch for in the coming year is the transition from signing PPAs with existing nuclear plants to direct investment in new-build advanced nuclear, including Small Modular Reactors (SMRs). If hyperscalers continue to signal demand for firm, carbon-free power at this scale, expect energy and utility companies to accelerate development timelines and financial investment in next-generation nuclear technologies to meet this demand.

- The scale and duration of recent deals, such as Meta’s 20-year PPA for 2.6 GW with Vistra, provide the long-term revenue certainty needed to finance new nuclear projects.

- The expansion of Amazon’s relationship with Talen Energy to 1.9 GW now explicitly includes exploring SMR development, moving the concept from theory to a commercial partnership.

- Political and regulatory pressure, highlighted by concepts like the “Ratepayer Protection Pledge, ” is forcing tech companies to “bring their own power, ” making direct financing of co-located generation not just a strategic advantage but a potential necessity.

- The conversation has shifted to behind-the-meter generation, with developers already announcing over 100 GW of natural gas capacity. This establishes a precedent for co-located SMRs as a carbon-free alternative for baseload power.

The questions your competitors are already asking

This report covers one angle of the energy procurement strategy for AI data centers. The questions that matter most depend on your work.

- Which hyperscalers are gaining or losing ground in the race to secure firm, carbon-free power for AI?

- What is the outlook for nuclear power deployment in the data center sector by 2030?

- How does nuclear power compare to solar-plus-storage on cost and reliability for providing 24/7 power to AI data centers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.