Fuel Cell Energy MCFC Pivot, 4 GW Data Center Pipeline and $35.6 M Q 2 Revenue (2021 to 2026)

On-Site Power Adoption, Fuel Cell Energy 4 GW Data Center Pipeline

The explosive growth of artificial intelligence is forcing data center operators to decouple from the constrained utility grid, creating an urgent, large-scale market for on-site power solutions that did not exist before 2025. This shift has pivoted fuel cell technology from a niche, often policy-driven clean energy solution into a critical infrastructure component for hyperscale data centers facing multi-year grid connection delays. The market now prioritizes speed-to-power and reliability over all else, a dynamic that is reshaping the commercial landscape for stationary fuel cells.

- Between 2021 and 2024, fuel cell adoption was characterized by smaller, sub-50 MW projects often tied to utility programs or microgrids. The technology was viewed as an alternative but not essential power source.

- The market inflection occurred in late 2025 and accelerated into 2026, driven by AI-induced power shortages. Fuel Cell Energy’s commercial sales pipeline swelled by 267% in a single quarter to 4 GW, with 89% of that demand coming from data centers, a segment that was previously a negligible part of its pipeline.

- This trend is not isolated. Competitor Bloom Energy secured a $2.6 billion deal with European AI firm Nebius in May 2026 and expanded its partnership with Oracle to deploy up to 2.8 GW of power, confirming that tech giants are now signing multi-gigawatt, multi-billion-dollar deals for on-site power.

- The validation of both Molten Carbonate and Solid Oxide technologies for this application indicates the market is large enough to support multiple scaled players, transforming the competitive positioning of the top two fuel cell companies.

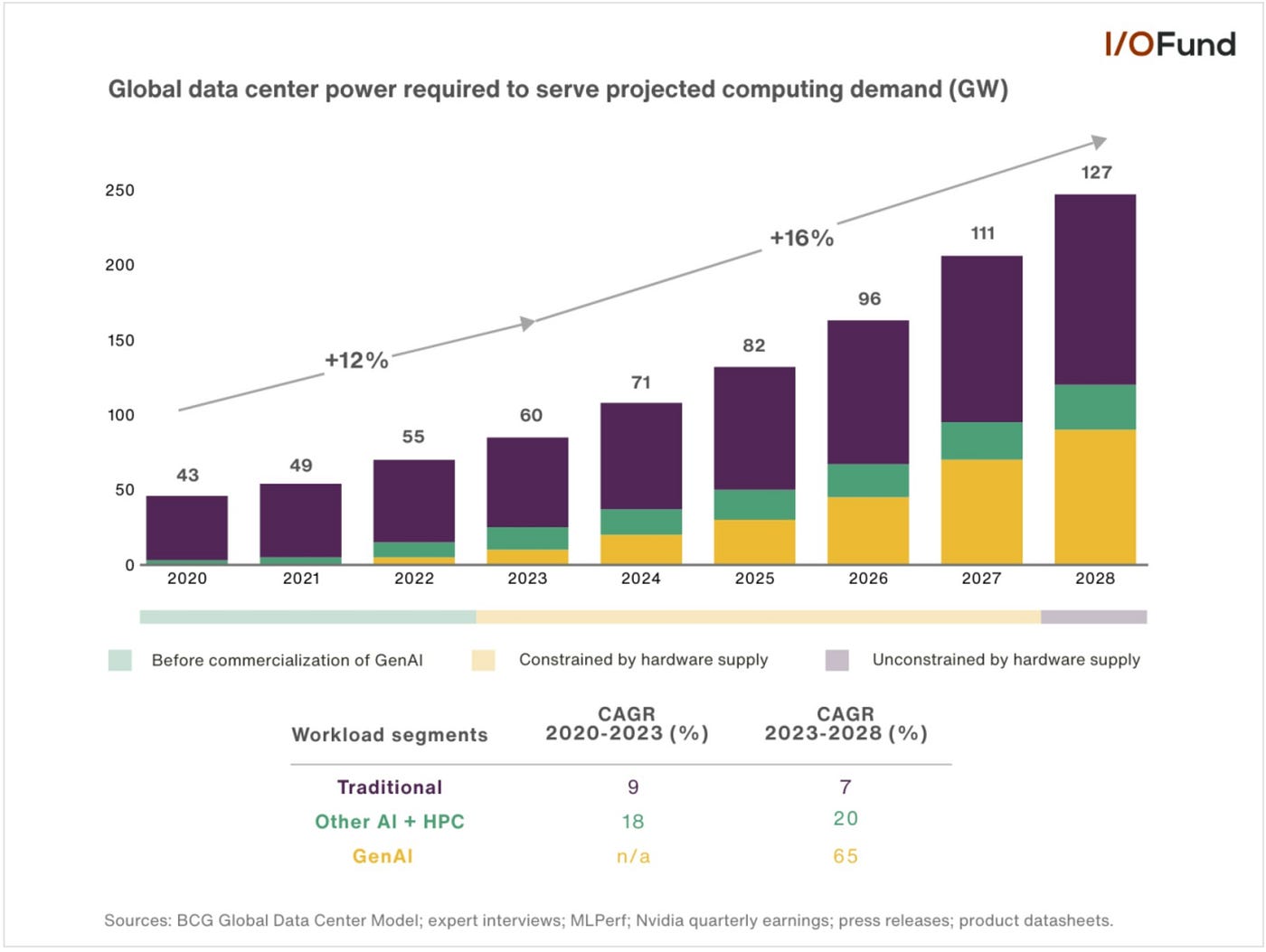

AI Boom Drives Massive Data Center Power Demand

This chart establishes the market context and core driver for the section’s topic, explaining why there is a significant data center pipeline for on-site power solutions like Fuel Cell Energy’s.

(Source: Beth Kindig – Medium)

$2.6 B Bloom Deal, Fuel Cell Energy Market Investment and Manufacturing Scale-Up

Capital is aggressively moving into the fuel cell sector, not through speculative venture funding, but through major customer contracts and balance sheet investments in manufacturing capacity, signaling the market has moved past technology validation to a race for industrial scale and execution. The primary financial challenge is no longer proving the technology works but funding the factories and inventory needed to fulfill multi-gigawatt order backlogs from creditworthy hyperscalers.

- In Q 2 2026, Fuel Cell Energy reported an increased cash position of $440.9 million, which it has earmarked to support a significant expansion of its Torrington, Connecticut, factory to a 500 MW annual production capacity.

- The scale of market demand is underscored by competitor Bloom Energy‘s $2.6 billion supply agreement with Nebius, announced in May 2026, to power European AI data centers. This follows its expanded partnership with Oracle, which involves deploying up to 2.8 GW of fuel cells.

- These large-scale commitments from customers effectively de-risk manufacturing investments by providing a clear line of sight to revenue, a stark contrast to the speculative factory builds that characterized earlier cleantech cycles.

Table: Data Center Fuel Cell Investments and Deployments (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fuel Cell Energy Manufacturing Expansion | Q 2 2026 | Announced plans to expand its Torrington, CT facility to 500 MW annual production capacity to meet anticipated demand from its 4 GW data center pipeline. | Stock Titan |

| Bloom Energy / Nebius | May 2026 | $2.6 billion agreement to deploy solid-oxide fuel cells to provide primary power for European AI data centers, signaling significant market traction outside the US. | Teski |

| Bloom Energy / Oracle | April 2026 | Expanded strategic partnership to deploy up to 2.8 GW of fuel cells to power Oracle’s growing cloud infrastructure and AI services in the US. | Bloom Energy |

US vs. Europe, Fuel Cell Energy’s Data Center Market Focus

While the need for data center power is a global issue, commercial activity for fuel cell deployments is overwhelmingly concentrated in the United States, driven by the location of its massive cloud computing hubs and some of the world’s most severe regional grid constraints. Europe is emerging as the second key market, but North America remains the clear center of gravity for demand and deployment in 2026.

- The vast majority of Fuel Cell Energy‘s 4 GW pipeline and Bloom Energy‘s landmark 2.8 GW Oracle agreement are targeted at the US market, where data center developers face grid interconnection queues of three to seven years in critical regions like Virginia’s Data Center Alley.

- Grid constraints in the US are well-documented, with grid operators like PJM struggling to accommodate new load, making on-site generation a necessity rather than a choice for developers needing to bring capacity online quickly.

- Europe has emerged as the next major growth front, validated by Bloom Energy‘s $2.6 billion deal with Nebius. This indicates that European data center operators are now facing similar grid-related challenges and are actively procuring on-site power solutions.

- Activity in Asia remains nascent but is showing early signals. Bloom Energy‘s 2.6 MW installation with Topco for a data center in Taiwan in May 2026 represents an initial foothold in a region where data center growth is also accelerating.

Commercial Scale Readiness, Fuel Cell Energy and its Molten Carbonate Fuel Cells

Stationary fuel cell technology has crossed the commercial threshold for data center applications, with the central challenge shifting from proving technical viability to demonstrating manufacturing scalability and the ability to execute rapid, multi-megawatt deployments. The market is no longer running small pilots; it is procuring power plants in factory-built, modular installments.

- Between 2021 and 2024, the narrative centered on demonstrating reliability through smaller-scale projects. In 2026, the discussion has fundamentally changed to fulfilling multi-gigawatt pipelines. Fuel Cell Energy‘s focus on a standardized, packaged 12.5 MW power block is a direct response to this need for scalable, repeatable deployments.

- The market success of both Fuel Cell Energy’s Molten Carbonate (MCFC) platforms and Bloom Energy’s Solid Oxide (SOFC) systems validates that multiple fuel cell architectures are commercially ready to meet the high-availability requirements of data centers.

- The key differentiator is no longer just the core technology but the ability to deliver a complete, utility-scale power solution that bypasses grid dependency. This includes managing fuel supply, site engineering, and long-term service agreements, areas where both companies are building expertise.

SWOT Analysis, Fuel Cell Energy Execution and Market Opportunity

Fuel Cell Energy‘s strategic position has been transformed by the AI-driven power crisis, presenting it with a generational market opportunity that is simultaneously matched by immense execution risk. The company’s primary strength is its massive new sales pipeline, but this is offset by a history of financial losses and the formidable threat of a key competitor that has already established a strong first-mover advantage.

- Strength: The company’s 4 GW sales pipeline, with 89% driven by data centers, represents an unprecedented demand signal that could fundamentally rescale the company if converted.

- Weakness: A track record of financial underperformance, including a 5% revenue decline and a widening net loss to $77.6 million in Q 2 2026, raises questions about its ability to execute profitably.

- Opportunity: The insatiable and immediate power demand from AI data centers, coupled with years-long grid delays, creates a captive market for reliable, rapidly deployable on-site power.

- Threat: Bloom Energy is the established leader, having already secured multi-gigawatt, multi-billion-dollar contracts with tech giants, creating a significant competitive hurdle for Fuel Cell Energy to overcome.

FuelCell’s Backlog Shrinks Amidst Share Dilution

This chart highlights a significant business challenge, making it a perfect illustration for the ‘Weaknesses’ or ‘Threats’ component of the SWOT analysis section and the discussion on execution.

(Source: x.com)

Table: SWOT Analysis for Fuel Cell Energy’s Data Center Strategy (2026)

| SWOT Category | Observed Strengths / Weaknesses | Market Opportunities / Threats | Supporting Data Point / Signal |

|---|---|---|---|

| Strengths | Explosive growth in sales pipeline aligned with a major secular trend. | Ability to capture a significant share of the new data center power market. | Sales pipeline grew 267% sequentially to 4 GW, with 89% from data centers. (Source: Yahoo Finance) |

| Weaknesses | History of unprofitability and inconsistent financial performance. | Inability to convert pipeline to profitable revenue could erode investor confidence. | Reported a $77.6 million net loss and $12.9 million gross loss in Q 2 2026, both wider than prior year. (Source: Fuel Cell Energy) |

| Opportunities | Grid constraints create a massive, non-discretionary need for on-site power. | Become a primary energy infrastructure provider for the AI industry. | Data center power demand is forecast to surge 220% by 2030, while grid connection queues are 3-7 years long. (Source: Benzinga) |

| Threats | Intense competition from an established leader with proven large-scale deployments. | Bloom Energy‘s first-mover advantage could lock Fuel Cell Energy out of key customer accounts. | Bloom Energy announced a $2.6 B deal with Nebius and a multi-GW deal with Oracle in Q 2 2026. (Source: Teski) |

4 GW Pipeline Conversion, Fuel Cell Energy’s Critical 2026 Test

The single most critical indicator for Fuel Cell Energy‘s future is its ability to convert a meaningful portion of its 4 GW data center pipeline into firm, binding contracts within the next 12 months. The market has rewarded the company for its strategic pivot and the promise of its pipeline; it will now demand proof of execution in the form of signed, bankable power purchase agreements.

- If Fuel Cell Energy announces even one significant PPA (e.g., >100 MW) with a recognized hyperscale data center operator in the second half of 2026, watch for this to be a major validation of its strategy and a catalyst for further appreciation.

- Conversely, if the next two to three quarters pass without a material conversion from this pipeline, this could signal that its proposals are not commercially competitive against Bloom Energy or that its sales cycle is much longer than anticipated, which would likely put significant pressure on the stock.

- The progress of its 500 MW factory expansion in Torrington is another key signal. Ramping up manufacturing capacity ahead of firm orders is a calculated risk. Investors will be watching for any commentary that ties the pace of this expansion directly to signed contracts.

The questions your competitors are already asking

This report covers one angle of FuelCell Energy’s pivot to the data center power market. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the on-site fuel cell market for data centers?

- Is FuelCell Energy a good investment now that its commercial pipeline is dominated by AI-driven data center demand?

- How does Molten Carbonate (MCFC) technology compare to Solid Oxide (SOFC) for powering hyperscale data centers?

- Which data center operators are adopting on-site fuel cell power solutions?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.