Grid Infrastructure Delays, 11 GW At-Risk Capacity, 5-Year Transformer Backlog, and 25 Project Cancellations (2024 to 2026)

11 GW At-Risk, PJM Power Bottlenecks Delay 2026 Data Center Projects

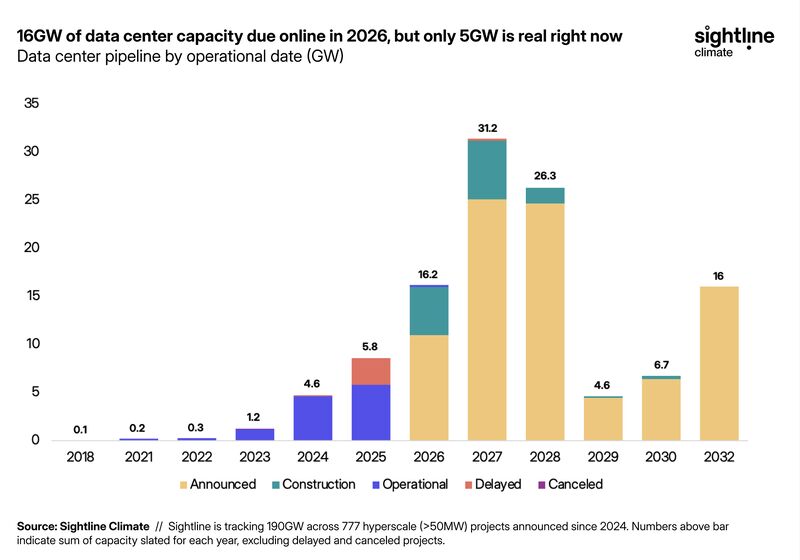

The primary risk to the U.S. data center sector is the fundamental mismatch between the industry’s rapid construction timelines and the multi-year delays for grid interconnection. While a data center can be built in 18-24 months, securing power now takes five to seven years, placing nearly 70% of the planned 2026 capacity pipeline at high risk of not being delivered on schedule. This is not a demand-side issue; it is a structural failure of power infrastructure to keep pace with digital growth.

- From 2021 to 2024, data center development was largely a real estate and construction challenge, with a primary focus on securing land and fiber. Beginning in 2025, the central challenge shifted decisively to power procurement, with grid availability becoming the go-no-go determinant for new projects.

- Of the approximately 16 GW of new U.S. data center capacity announced for a 2026 commercial operation date, only 5 GW is currently under construction. This leaves 11 GW in planning stages, exposed to severe grid-related delays.

- The U.S. faces a critical shortage of high-voltage transformers, with a reported 5-year backlog for new orders. This single supply chain failure can halt a multi-billion dollar project indefinitely, a factor that could delay 30% to 50% of facilities planned for 2026.

- Grid operators like PJM, which manages the grid for 13 eastern states, report that AI projects now spend more time waiting for physical grid upgrades *after* approval than they do in the interconnection queue itself, indicating the problem extends beyond procedural backlogs to physical infrastructure deficits.

11GW of 2026 Data Center Capacity Faces Delay Risk

The section heading ’11 GW At-Risk, PJM Power Bottlenecks Delay 2026 Data Center Projects’ directly matches the chart’s headline, which quantifies the at-risk capacity (11 GW) for a specific year (2026) due to delays.

(Source: LinkedIn)

Project Cancellations, PJM Grid Issues Lead to 4.7 GW Capacity Loss

Escalating grid connection delays and intensifying local opposition are directly causing a surge in data center project cancellations, removing significant planned capacity from the market before construction begins. This trend accelerated dramatically in 2025, as communities and regulators began to scrutinize the immense power and water consumption of new hyperscale facilities.

- The number of data center projects canceled due to local opposition and power constraints quadrupled from just six in 2024 to 25 in 2025.

- These 25 canceled projects represented a total of 4.7 GW of lost power capacity, a significant portion of the future supply needed to support AI and cloud growth.

- The financial impact of these cancellations and delays is substantial, with one research firm estimating that at least $156 billion of proposed projects were impacted in 2025 alone.

- In response to local concerns, lawmakers in at least 22 states introduced over 60 bills in 2025 to address the grid and environmental impacts of data centers, creating a complex and uncertain regulatory environment for developers.

Data Center Pipeline Collapses in Q4 2025

The section discusses ‘Project Cancellations’ and ‘Capacity Loss.’ The chart’s headline, ‘Data Center Pipeline Collapses,’ provides a strong visual and thematic representation of these concepts.

(Source: Energy Industry Insights from Avanza Energy – Substack)

Table: Data Center Project Cancellations

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Data Center Projects | 2025 | 25 projects representing 4.7 GW of capacity were canceled due to a combination of local opposition and power availability issues. This represents a quadrupling of cancellations compared to the previous year. | Heatmap News |

| U.S. Data Center Projects | 2025 | An estimated $156 billion worth of proposed data center projects were canceled or delayed in 2025 as opposition grew across multiple states. | Industrial Info |

| U.S. Data Center Projects | 2024 | Six data center projects were canceled due to public pushback and power constraints, setting the stage for the significant increase seen in 2025. | Utility Dive |

US East vs West, PJM Grid Constraints Reshape Data Center Siting

Power availability, not just fiber connectivity, is now the primary driver of data center site selection, forcing developers to abandon traditional hubs for regions with accessible grid capacity. The era of land banking in power-constrained zones like Northern Virginia is ending, replaced by a strategic search for viable grid interconnection points, fundamentally redrawing the map of U.S. digital infrastructure.

- Major data center markets, particularly in the eastern U.S. within the PJM territory, are effectively saturated. Utilities like Dominion Energy have indicated they cannot support the projected load growth without significant and time-consuming grid upgrades.

- The shift is toward regions with available power, driving development into new states and secondary markets. A 1-year lead in power delivery can be worth $3 – $4 million per MW in project value, incentivizing developers to prioritize energy access over other siting factors.

- Before 2024, site selection was dominated by proximity to internet exchange points and existing fiber routes. Post-2025, the process starts with utility and grid operator engagement to identify locations capable of supporting loads of several hundred megawatts or more.

PJM Developers 30% Shift to On-Site Generation as Grid Fails (2025 to 2030)

In response to grid failures, an accelerating trend is the adoption of on-site “behind-the-meter” power generation, shifting data center development from a real estate model to an integrated energy infrastructure project. This approach allows developers to bypass grid interconnection queues and de-risk project timelines, albeit at a significantly higher capital cost. This has led to a surge of interest in technologies from natural gas turbines to advanced fuel cells.

- More than 30% of data center projects announced in 2024 plan to use on-site power as their primary source, with projections indicating over one-third of all facilities will use 100% on-site power by 2030.

- This represents a marked change from the 2021-2024 period, where on-site power was almost exclusively for backup purposes. It is now a primary solution for securing the power needed for operations.

- The technology mix for on-site generation currently favors natural gas, with inquiries to gas networks for direct connections surging in 2024 and 2025. However, developers are also exploring a path to cleaner technologies, including hydrogen and small modular reactors (SMRs), to meet long-term sustainability goals.

On-Site Gas Power for Data Centers Skyrockets

The section heading specifically mentions a ‘Shift to On-Site Generation as Grid Fails.’ The chart’s headline about on-site power ‘skyrocketing’ is a direct and specific illustration of this trend.

(Source: Energy Industry Insights from Avanza Energy – Substack)

SWOT Analysis, PJM Data Center Development Execution Risks

While insatiable demand for AI compute provides a strong market opportunity, severe weaknesses in power infrastructure and growing external threats create significant execution risks. These factors increasingly challenge the viability of projects that have not secured power, representing the central tension in the market today.

- Strengths: Demand for AI-ready data centers is projected to grow exponentially, providing a clear revenue path for projects that can be successfully delivered.

- Weaknesses: The industry is fundamentally dependent on an aging grid infrastructure that was not designed for the scale and speed of current load growth.

- Opportunities: The power bottleneck creates a major opportunity for vertically integrated developers and energy companies to deliver combined power-and-compute solutions.

- Threats: A combination of regulatory scrutiny, community opposition, and persistent supply chain shortages for critical electrical equipment presents a formidable barrier to the majority of the planned pipeline.

Data Center Pipeline Shows Significant Risk

The section is a ‘SWOT Analysis’ focusing on ‘Execution Risks.’ The chart’s headline, ‘Data Center Pipeline Shows Significant Risk,’ summarizes a key finding that would be detailed within the Threats and Weaknesses portions of such an analysis.

(Source: Sightline Climate)

Table: SWOT Analysis for Data Center Development

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Robust demand from cloud and enterprise customers. Established financing models based on real estate. | Explosive, AI-driven demand for compute capacity. Hyperscaler customers are willing to sign long-term, high-value offtake agreements. | The demand signal became significantly stronger and more concentrated around AI workloads, validating the need for massive new capacity. |

| Weakness | Emerging signs of power constraints in primary markets like Northern Virginia. | System-wide power grid failure. Multi-year interconnection queues and critical equipment shortages (e.g., 5-year transformer backlog) are the norm. | The power constraint shifted from a localized issue to a systemic, industry-defining weakness that invalidates traditional development timelines. |

| Opportunity | Expansion into secondary and tertiary geographic markets. Focus on energy efficiency improvements. | Vertical integration with power generation. Development of on-site power plants (gas, fuel cells, SMRs) to bypass grid constraints. New financing models based on infrastructure. | The crisis created a new, high-value business model for developers who can solve the power problem first, turning an infrastructure weakness into a competitive advantage. |

| Threat | Localized “NIMBY” (Not In My Back Yard) opposition. Standard construction supply chain delays. | Organized, widespread community opposition leading to project moratoria and a quadrupling of cancellations. New state-level regulations targeting data centers. | The threat evolved from isolated opposition to a coordinated political and regulatory movement, adding significant risk and uncertainty to the permitting phase. |

PJM Market Bifurcation, 11 GW At-Risk Pipeline Splits Developers

The grid-constrained environment will bifurcate the data center market. The winners will be well-capitalized developers who can afford to build their own power infrastructure and secure long-term offtake agreements. Tier 2 and Tier 3 players, unable to compete for limited grid capacity or finance on-site power, will be increasingly squeezed out, leading to market consolidation and a concentration of power among a few large-scale, integrated players.

- If this happens: The current power constraints persist through 2028, as projected by multiple analyses.

- Watch this: An increase in partnerships between hyperscalers, data center developers, and energy companies like Next Era Energy to co-develop large-scale energy and compute campuses. Watch for the first final investment decisions on data centers co-located with SMRs.

- These could be happening: Smaller developers unable to secure power for gigawatt-scale projects will pivot to the edge computing market or become acquisition targets. The 11 GW of at-risk capacity will not disappear but will be re-scoped into later years, with a high percentage ultimately canceled in favor of projects with secured power.

Majority of 2026 Data Center Pipeline At-Risk

The section describes a ‘Market Bifurcation’ where the ’11 GW At-Risk Pipeline Splits Developers.’ The chart’s headline, ‘Majority of 2026 Data Center Pipeline At-Risk,’ perfectly describes the scale of the ‘at-risk’ side of this market split.

(Source: Energy Industry Insights from Avanza Energy – Substack)

The questions your competitors are already asking

This report covers one angle of the grid infrastructure constraints impacting the U.S. data center development pipeline. The questions that matter most depend on your work.

- What is the realistic outlook for new U.S. data center capacity delivery by 2026, considering the grid interconnection queues?

- What is the actual status of the 11 GW of at-risk data center projects announced for 2026?

- Who are the key suppliers of high-voltage transformers, and what is their current backlog status?

- What are the opportunities for on-site power and microgrid solutions to bypass utility grid constraints?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.