Green Hydrogen Grid Power, National Grid’s Mainspring Pilot, the $3/kg IRA Credit, and 2 Major Project Cancellations (2022-2026)

Hydrogen Grid Pilots: From Technical Demos to Commercial Reality Checks

The adoption of hydrogen for grid power has shifted from demonstrating technical feasibility in the early 2020 s to confronting commercial viability, where subsidy dependence and fuel supply risks are the primary determinants of project success.

- Between 2021 and 2024, the industry focus was on technical pilots. The National Grid project, announced in May 2022, was designed to prove that a Mainspring Energy linear generator could operate on 100% hydrogen and advance its Technology Readiness Level (TRL) from a prototype stage (TRL 6-7) into a grid-ready system.

- After 2025, the narrative changed to one of economic survival amid a market shakeout. The Northport project is now viewed as a success because it has advanced while larger ventures faltered, such as the cancellation of California’s ARCHES hydrogen hub in late 2025 after the project’s Department of Energy funding was withdrawn.

- The project’s viability is now defined by its focused, high-value application as a Dispatchable Electric Facility Resource (DEFR). This use case, providing a carbon-free alternative to gas peaker plants, has proven more resilient than speculative, broad “hydrogen economy” projects that failed to secure financing and offtake agreements.

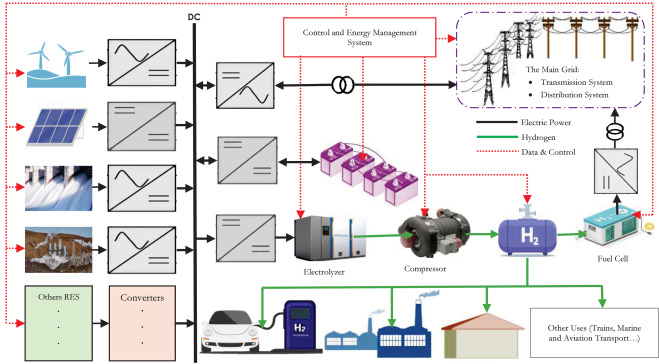

Green Hydrogen-to-Grid System Visualized

This diagram illustrates the technical pilot system described in the section, showing how renewable energy is converted to hydrogen and then back into electricity for the grid.

(Source: ScienceDirect.com)

$3/kg IRA Credit, National Grid’s Subsidy-Dependent Economics

The economic case for current hydrogen grid power projects is almost entirely dependent on the $3.00/kg clean hydrogen production tax credit (45 V) from the Inflation Reduction Act, which is required to make their Levelized Cost of Electricity (LCOE) competitive.

- The IRA tax credit functions as the central economic pillar for the sector, capable of reducing the Levelized Cost of Hydrogen (LCOH) by over 100%. This subsidy is the primary mechanism making fuel for projects like Northport financially feasible in the near term.

- Without this government support, the LCOE for hydrogen-fueled power generation is estimated between $250/MWh and $400/MWh. This cost is uncompetitive against incumbent technologies like natural gas peaker plants ($110-$170/MWh) and even emerging alternatives like 4-hour battery storage ($140-$220/MWh).

- This extreme policy dependence creates significant investment risk. The failure of projects like the ARCHES hub demonstrates the fragility of the financial model for ventures that lose access to government funding, showing that private capital is not yet ready to support these projects on their own merits.

Table: Hydrogen Project Investment and Cancellation Signals

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| ARCHES Hydrogen Hub | November 2025 | California’s Alliance for Renewable Clean Hydrogen Energy Systems (ARCHES) halted its hydrogen hub development after the DOE withdrew its funding. This signals the high risk associated with large-scale projects dependent on continued government financial support. | gasworld |

| Advanced Energy Manufacturing | H 1 2025 | The value of canceled advanced energy manufacturing investments exceeded the value of new announcements. This indicates a broader market correction and investor pullback from capital-intensive clean energy projects amid policy uncertainty. | RMI |

| National Grid / Mainspring Energy | May 2022 | Initial project announcement to install the world’s first 100% hydrogen-fueled linear generator at the Northport Power Plant. The project’s purpose was to serve as a proof-of-concept for replacing fossil-fuel peaker plants. | TBR News Media |

National Grid 1 Mainspring Energy Pilot, Tech Validation (2022-2026)

The partnership between National Grid and Mainspring Energy provides a successful model for de-risking new hydrogen technologies by creating a closed-loop system where a utility acts as both the project developer and the final energy offtaker.

- The collaboration, initiated in 2022, strategically aligned National Grid’s need for a decarbonized, dispatchable power source with Mainspring Energy’s need for a commercial validation site to prove its 100% hydrogen generator technology in a real-world grid environment.

- This integrated structure circumvents the primary commercial failure point for many large-scale hydrogen projects: the challenge of securing separate, bankable, long-term offtake agreements from third parties.

- The model’s potential for replication is evident in subsequent deals. In May 2025, a partnership was announced between electrolyzer firm Verdagy and Mainspring to demonstrate integrated hydrogen-fueled power generation, showing a trend toward creating more complete and de-risked technology packages.

Table: Key Hydrogen Technology De-Risking Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Verdagy / Mainspring Energy | May 2025 | Partnership to demonstrate H 2-fueled linear generators. This collaboration links an upstream hydrogen production technology (electrolyzers) with a downstream power generation unit, aiming to create a more integrated and bankable system. | Argus Media |

| National Grid Ventures / Mainspring Energy | August 2025 | Formal installation of the 100% hydrogen linear generator at Northport. The project serves as the first commercial deployment of the technology for grid stabilization, targeting TRL 9. | National Grid |

US Regional Focus, National Grid’s New York and California Pilots

Hydrogen grid power development is geographically concentrated in US states with aggressive decarbonization mandates and supportive policies, particularly New York and California, where regulatory pressure creates a viable market for zero-carbon dispatchable power.

- The National Grid project is strategically located at the Northport Power Plant on Long Island, New York. This region combines high electricity costs with a clear political objective to phase out aging fossil-fuel peaker plants, creating a direct market need for the technology.

- Prior to the Northport installation, Mainspring Energy’s linear generator technology was matured in California through a project funded by the California Energy Commission. This demonstrates a clear bi-coastal strategy of leveraging state-level funding and regulatory drivers to advance technology readiness.

- The divergent outcomes of the targeted Northport project in New York and the large-scale ARCHES hub failure in California suggest that smaller, utility-led initiatives are a more effective near-term pathway for deployment than complex, multi-sector regional consortiums.

Linear Generator TRL, National Grid Advances Tech to Commercial Scale

The National Grid Northport project successfully elevates the Technology Readiness Level (TRL) of 100% hydrogen-fueled linear generators from a validated prototype (TRL 7) to a commercially proven system (TRL 9), shifting the primary bottleneck from power generation hardware to the upstream fuel supply chain.

- Between 2021 and 2024, the technology’s readiness for pure hydrogen operation was limited to demonstration and pilot phases, with projects validating its performance in controlled environments to bring it from TRL 5 to TRL 7.

- The Northport installation in 2025 marks the critical transition to TRL 9, defined as an actual system proven in a live operational environment. This effectively establishes the generator as a commercially available solution for its intended grid application.

- This technological success now highlights a major discrepancy in maturity across the value chain. While the project proves the generator is ready for deployment, it also confirms that the lack of at-scale green hydrogen production, storage, and transport infrastructure is the primary constraint to widespread adoption.

SWOT Analysis, National Grid’s Hydrogen Power Execution Risks

The SWOT analysis reveals a technology with compelling technical strengths for a niche grid application, but its scalability is constrained by significant external economic dependencies and infrastructure weaknesses.

- The project’s key strength is its validation of a dispatchable, zero-carbon power source with minimal NOx emissions, directly addressing a critical need in renewable-heavy grids.

- Its primary weakness is a business model that is currently non-viable without the $3.00/kg IRA tax credit, exposing it to significant policy risk.

- The major threat is the unresolved challenge of securing a reliable, low-cost hydrogen supply, which could allow competing technologies like battery storage to capture the ancillary services market.

Table: SWOT Analysis for Hydrogen-Fueled Linear Generators

| SWOT Category | 2021 – 2024 (Demonstration Phase) | 2025 – 2026 (Commercial Pilot Phase) | What Changed / Validated |

|---|---|---|---|

| Strength | Theoretical fuel flexibility and low emissions profile. Fast ramping capability suitable for grid support. | Proven 100% hydrogen operation in a live grid setting (TRL 9). Validated as a carbon-free dispatchable resource with near-zero NOx emissions. | Technical performance claims were validated in a real-world commercial environment, moving from lab to grid. |

| Weakness | Uncertain capital cost and unproven LCOE. Technology readiness for 100% hydrogen was at the prototype level (TRL 6-7). | High LCOE ($250-$400/MWh) without subsidies. Extreme dependence on the IRA tax credit for economic viability. | The project confirmed the technology works but also quantified its non-competitive standalone economics, highlighting its reliance on subsidies. |

| Opportunity | Growing market for peaker plant replacements. Anticipation of government incentives like the IRA. | The $3.00/kg IRA 45 V tax credit is now law. State-level clean energy mandates create a protected market for zero-carbon firm power. | The market opportunity moved from hypothetical to tangible, anchored by specific government subsidies and regulatory drivers. |

| Threat | Competition from natural gas peakers and declining battery costs. Risk of immature hydrogen supply chain. | Policy risk of changes to the IRA. High-profile cancellations of other hydrogen projects (ARCHES) create negative market sentiment. Persistent lack of hydrogen infrastructure. | The fuel supply and policy risks, once theoretical, were validated as the primary threats to scaling after multiple large projects failed for these exact reasons. |

National Grid’s 2026 Replication Strategy and Fuel Supply Risks

In 2026, the central question for hydrogen grid power will be whether the Northport model can be replicated by other utilities, a scenario that depends entirely on securing long-term, cost-effective green hydrogen supply contracts backed by stable policy.

Offshore Wind-to-Hydrogen Model

This diagram provides a model for the replication strategy discussed, showing how offshore wind—a key renewable resource for the Northport plant’s region—can be used to create hydrogen for grid power.

(Source: ScienceDirect.com)

- If the $3.00/kg IRA tax credit is maintained with favorable implementation rules, watch for utilities in other regulated markets with constrained grids, such as PJM and ISO-NE, to issue Requests for Proposals (RFPs) for similar dispatchable, zero-emissions resources.

- These developments could be happening: Technology providers like Mainspring Energy may increasingly bundle their generators with electrolyzers from partners like Verdagy or form joint ventures with hydrogen suppliers to offer integrated, de-risked solutions to utility customers.

- If green hydrogen prices remain stubbornly high due to production and infrastructure delays, watch for utilities to limit their investment to short-duration battery storage systems. This would relegate hydrogen generators to niche, long-duration resilience applications rather than widespread grid balancing roles.

The questions your competitors are already asking

This report covers one angle of hydrogen grid power commercialization. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the hydrogen grid power market?

- What is the outlook for deploying hydrogen generators as gas peaker plant alternatives by 2030?

- National Grid and Mainspring activities. Is the hydrogen linear generator partnership progressing from pilot to commercial deployment?

- How do Mainspring’s hydrogen linear generators compare to fuel cells or turbines for grid peaking applications?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.