Enhanced Geothermal Projects, Meta 300 MW PPA, 2 XGS Energy and Sage Geosystems Deals, and 4 Corporate Agreements (2025-2026)

The enormous power requirement of artificial intelligence has created an urgent need for firm, carbon-free energy, forcing a strategic re-evaluation of data center power procurement. Landmark agreements by Meta for 300 MW of next-generation geothermal power from XGS Energy and Sage Geosystems signal a critical shift, validating the use of oil and gas drilling technologies to secure the 24/7 electricity essential for AI operations. These deals demonstrate that after years of development, advanced geothermal is moving from pilot stages to commercial-scale deployment, directly addressing the limitations of intermittent renewables.

Geothermal Project Adoption, Meta 300 MW PPA and 4 Corporate Deals

Corporate power purchase agreements from major technology firms are accelerating the transition of next-generation geothermal from pilot projects to commercial-scale infrastructure assets. This shift is driven by the AI sector’s specific need for clean, firm, and reliable baseload power, a requirement that intermittent renewables like solar and wind cannot meet without expensive and large-scale energy storage.

- Between 2021 and 2024, next-generation geothermal was primarily in a research and demonstration phase, with projects focused on proving technological feasibility at smaller scales. The market was watching for a significant commercial validation signal.

- The turning point arrived in 2025-2026, beginning with a successful pilot by Fervo Energy, which led to a 115 MW PPA with Google to power its Nevada data centers. This event served as the critical proof-of-concept for the industry.

- Building on this momentum, Meta executed two significant PPAs in 2026 for a combined 300 MW of geothermal power from XGS Energy in New Mexico and Sage Geosystems in Texas, confirming the technology’s bankability for large-scale data center operations.

- Google expanded its commitment by signing a 150 MW agreement with established geothermal operator Ormat Technologies in February 2026, diversifying its geothermal portfolio between conventional and enhanced systems.

Chart visualizes the new geothermal race

The section discusses corporate PPAs accelerating geothermal adoption due to the need for firm power, a theme directly captured by this chart about the ‘new geothermal race’.

(Source: LinkedIn)

$462 M in Funding, Fervo Energy Series E Round

The successful technological de-risking of enhanced geothermal systems has unlocked a significant flow of private investment, enabling startups to scale operations and finance large-scale projects. This influx of capital is critical for covering the high upfront costs associated with deep drilling and well development, which were previously a major barrier to entry.

- In December 2025, Fervo Energy closed an oversubscribed Series E funding round of $462 million, with backing from strategic investors including Google. The capital is designated for accelerating project development to meet the surging power demand from the technology sector.

- Sage Geosystems‘ development was supported by a Series B financing round co-led by incumbent geothermal leader Ormat Technologies, a move that validates Sage’s hybrid approach and provides strategic operational expertise.

- Investment in next-generation geothermal reportedly grew by 85% in Q 1 2025 alone, reaching $1.7 billion, indicating strong investor confidence in the sector’s ability to provide a scalable solution for clean, firm power.

Table: Geothermal Strategic Investments

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fervo Energy | Dec 2025 | Raised $462 million in a Series E funding round backed by Google, Cal STRS, and B Capital. The funds will be used to scale development of geothermal plants to meet demand for 24/7 clean electricity. | ESG Dive |

| Sage Geosystems | Feb 2026 | Received a strategic investment from Ormat Technologies as part of a Series B financing round. The investment validates Sage’s technology and supports its PPA with Meta. | Investing.com |

| Vulcan Energy | 2025 | Fully secured financing for its Phase 1 Lionheart project in Germany, which combines geothermal energy with lithium extraction, demonstrating investor appetite for diversified geothermal business models. | IEA |

Meta 2 Geothermal Partnerships, XGS Energy and Sage Geosystems (2025-2026)

Strategic partnerships between geothermal technology developers and established energy service companies are becoming essential for project execution and scaling. These collaborations merge novel subsurface engineering with proven project management and drilling expertise, reducing execution risk and accelerating deployment timelines.

Diagram shows Sage Geosystems’ specific technology

The section focuses on partnerships with XGS and Sage Geosystems. This chart, from Sage, directly illustrates the ‘novel subsurface engineering’ it brings to its partnership, as mentioned in the text.

(Source: POWER Magazine)

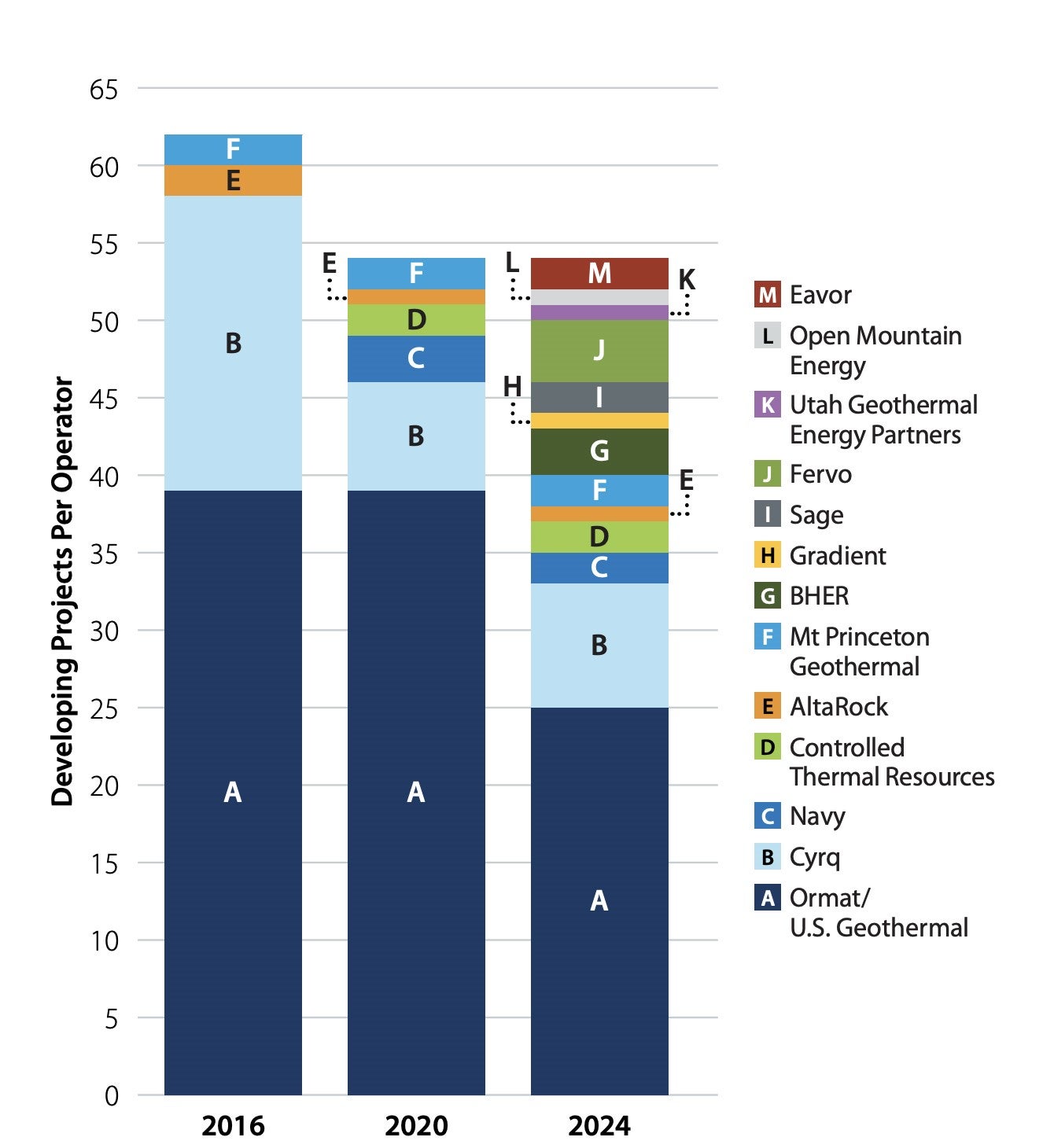

Chart shows diversification of geothermal operators

The section describes strategic investments in new players like Fervo and Sage. The chart perfectly illustrates this by showing the significant diversification of the operator landscape by 2024, including these new entrants.

(Source: POWER Magazine)

- In March 2026, XGS Energy announced a formal partnership with energy technology firm Baker Hughes to develop the 150 MW geothermal plant in New Mexico for Meta. This partnership combines XGS’s proprietary closed-loop technology with Baker Hughes‘ extensive experience in geothermal drilling and development.

- The collaboration between Sage Geosystems and its investor Ormat Technologies provides Sage with access to decades of experience in operating geothermal power plants, a critical factor for successfully delivering on its 150 MW PPA with Meta in Texas.

- These partnerships reflect a broader market trend where startups with innovative technology align with industry incumbents that possess the supply chains, workforce, and project delivery experience required for capital-intensive energy infrastructure projects.

Table: Geothermal Corporate Partnerships and PPAs

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Meta & XGS Energy / Baker Hughes | Jun 2025 – Mar 2026 | Meta contracted for 150 MW of closed-loop geothermal power in New Mexico. XGS partnered with Baker Hughes to combine proprietary technology with drilling and development expertise. | Yahoo Finance |

| Meta & Sage Geosystems | Feb 2026 | Meta signed a PPA for 150 MW of power from Sage Geosystems in Texas. The project utilizes a single-well closed-loop and geopressured system approach. | POWER Magazine |

| Google & Ormat Technologies | Feb 2026 | Google signed a 150 MW geothermal PPA with Ormat to power its Nevada data centers, expanding its portfolio of firm, clean energy sources. | Carbon Credits |

| Google & Fervo Energy | May 2025 | Google secured approval for a 115 MW PPA from Fervo Energy‘s EGS project, a landmark deal that proved the commercial viability of enhanced geothermal for data centers. | ENR |

US Hotspots, Meta Geothermal Sites in New Mexico and Texas

The geographic deployment of next-generation geothermal projects is expanding beyond traditional hydrothermal regions, driven by technological advancements that allow access to heat resources in a wider variety of geologic settings. The selection of New Mexico and Texas for Meta‘s projects highlights the strategy of co-locating power generation near data center clusters and leveraging regional oil and gas expertise.

Chart explains geothermal’s role for data centers

This section’s table details partnerships for Meta’s data centers. The chart visually explains the strategic purpose of these deals by showing how a geothermal plant directly provides power and cooling to a data center.

(Source: LinkedIn)

- Prior to 2025, commercial geothermal in the U.S. was heavily concentrated in states with obvious surface-level resources, such as California and Nevada. Project development was limited by a dependence on naturally occurring hydrothermal systems.

- The 2025-2026 period demonstrates a clear geographic expansion. The selection of New Mexico for the XGS Energy project aligns with the state’s significant untapped geothermal potential, as identified by geological surveys, and its proximity to Meta‘s existing data center infrastructure.

- The decision by Sage Geosystems to develop its project in Texas is particularly strategic, as it allows the company to tap into the state’s deep bench of drilling expertise and repurpose existing, non-productive oil and gas wells, potentially lowering costs and development timelines.

- This trend indicates that future geothermal projects will be increasingly sited based on proximity to large electrical loads, like AI data centers, rather than being restricted to specific volcanic regions.

Enhanced Geothermal TRL, Fervo Energy Pilot and Meta Commercial Validation

Next-generation geothermal technologies are rapidly advancing from demonstration to full commercial readiness, with Technology Readiness Levels (TRLs) progressing from mid-stage validation to early commercial deployment. The large-scale PPAs from hyperscale data center operators are the most definitive signal of this maturation, providing the bankability needed for widespread adoption.

- In the 2021-2024 period, advanced geothermal technologies like Enhanced Geothermal Systems (EGS) and closed-loop systems were generally considered to be at TRL 4-6, signifying validation in lab and relevant environments but not yet at full commercial scale.

- Fervo Energy‘s successful pilot project in 2025, which delivers power to Google, advanced EGS to TRL 7-8 (system prototype demonstration in an operational environment to full commercial deployment readiness). It proved that horizontal drilling and hydraulic fracturing could be precisely controlled for geothermal energy production.

- The 300 MW in contracts from Meta for technologies from XGS Energy and Sage Geosystems push these closed-loop and hybrid systems firmly into the TRL 7-8 range, as they are now being deployed in commercial-scale projects backed by a major corporate offtaker.

- This rapid progression shows a market that is quickly moving past technological hurdles and is now primarily focused on addressing commercial and regulatory challenges like cost, permitting, and grid interconnection.

SWOT Analysis, Meta’s Geothermal Strategy and Market Risks

The strategic push into next-generation geothermal by technology companies like Meta is driven by clear operational needs but is also exposed to significant execution risks common to emerging energy technologies. A SWOT analysis reveals that while the opportunity is substantial, the path to scaled deployment is dependent on overcoming infrastructure and regulatory hurdles.

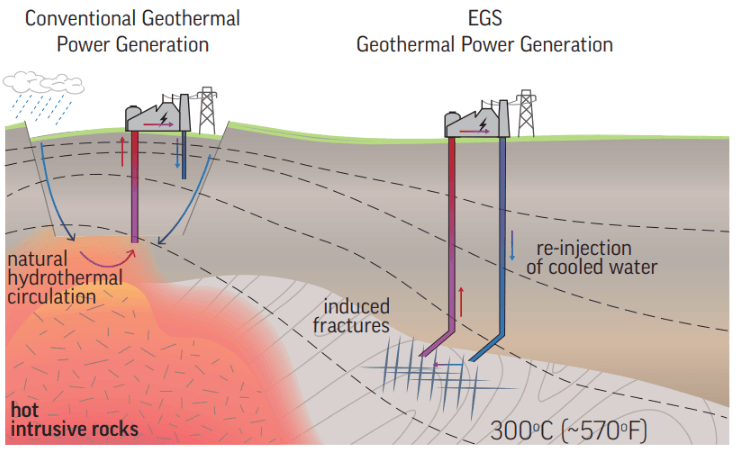

Diagram explains the technology being analyzed

This section introduces a SWOT analysis of next-generation geothermal. The chart provides essential context by explaining what Enhanced Geothermal Systems (EGS) are and how they differ from conventional methods.

- Strengths: The primary strength of geothermal is its ability to provide 24/7, baseload, carbon-free power, directly matching the operational profile of AI data centers.

- Weaknesses: High upfront capital costs and long project development timelines associated with drilling remain significant barriers compared to intermittent renewables.

- Opportunities: The insatiable and growing demand for clean, firm power from the AI industry creates a massive, bankable market for geothermal developers.

- Threats: Grid interconnection queues and permitting delays represent the most significant threats to project viability, capable of stalling projects for years regardless of technological readiness or project economics.

Table: SWOT Analysis for Enhanced Geothermal in Data Centers

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Theoretical high capacity factor (>90%) and potential for firm, clean power. | Demonstrated 24/7 power delivery in Fervo Energy‘s pilot for Google. Validated as a core solution for AI data center demand with Meta‘s 300 MW of PPAs. | The value proposition of “clean firm” power transitioned from a theoretical advantage to a commercially validated and bankable asset for hyperscalers. |

| Weaknesses | High upfront drilling costs, perceived risk of induced seismicity, and technology not yet proven at commercial scale. | Drilling costs remain high but are being offset by IRA tax credits and large-scale offtake agreements. Closed-loop systems from XGS Energy and Eavor are developed to minimize seismicity and water use. | While costs are still a factor, major corporate PPAs de-risk projects financially. Technology risk has been substantially mitigated through successful pilots and new, lower-risk designs. |

| Opportunities | Growing corporate demand for 24/7 clean energy and repurposing of oil & gas technology and workforce. | Explosive AI power demand creates a primary market. The Inflation Reduction Act (IRA) and subsequent legislation provide crucial tax credits (PTC/ITC) for geothermal projects. | The market opportunity crystallized from a general clean energy goal to a specific, urgent need for “clean firm” power to support the AI economy, making geothermal a strategic necessity. |

| Threats | Lengthy permitting processes and uncertainty around project economics without large-scale buyers. | Grid interconnection queues emerge as the single largest bottleneck, with wait times of 3-7 years. Policy uncertainty around tax credits (e.g., changes in the OBBBA of 2025) creates financing risk. | The primary threat shifted from technological and market risk to infrastructure and regulatory risk. Even with a proven product and willing buyers, projects can be stalled by grid and permitting delays. |

90 GW by 2050, Meta Geothermal and Grid Interconnection Risks

The most critical variable determining the future growth of the geothermal sector is the ability to overcome grid interconnection and permitting bottlenecks. While the technology is maturing and demand is clear, the path to the U.S. Department of Energy’s projection of 90 GW of geothermal power by 2050 is blocked by an antiquated energy infrastructure and regulatory system. The success of projects from Meta, Google, and others will depend as much on policy reform as on technological innovation.

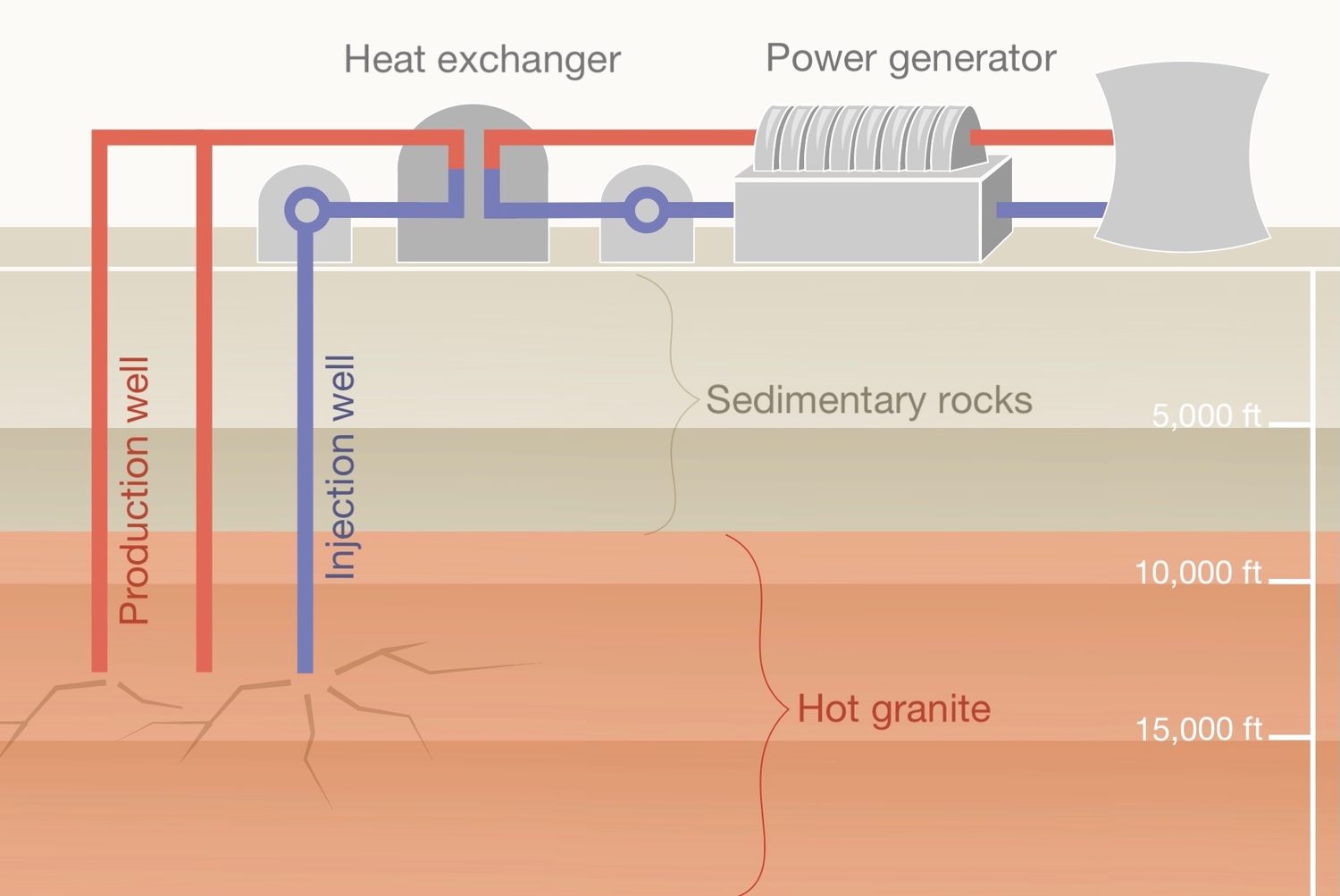

Diagram shows how enhanced geothermal works

This section’s table details a SWOT analysis, validating strengths with Fervo’s pilot. This diagram illustrates the EGS technology used by Fervo, explaining how the ’24/7 power delivery’ strength is achieved.

(Source: e360-Yale)

- If grid operators and regulators streamline interconnection queues, we will see an acceleration of geothermal project announcements and final investment decisions. Watch for reforms from FERC and regional grid operators.

- If permitting reform, such as the HEATS Act passed by the House in April 2026, is enacted and effectively implemented, project development timelines could be reduced by years. Watch for the Bureau of Land Management (BLM) to issue new, simplified regulations for exploration on federal lands.

- This could be happening now: Data center developers are increasingly co-locating new campuses in regions with high geothermal potential to secure dedicated power sources and bypass congested grid hubs. This could lead to the development of new energy and data infrastructure corridors in states like New Mexico, Texas, and Utah.

The questions your competitors are already asking

This report covers one angle of next-generation geothermal commercialization for AI data centers. The questions that matter most depend on your work.

- Which enhanced geothermal companies are gaining ground after the recent Meta and Google PPAs?

- What is the outlook for next-generation geothermal deployment for AI data centers by 2030?

- How does Sage Geosystems’ geopressured system compare to XGS Energy’s technology for utility-scale deployment?

- Which data center operators are adopting next-generation geothermal power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.