Top 10 SMR and Renewable PPAs: Google’s 500 MW Kairos Deal, Microsoft’s 10.5 GW Agreement (2024-2026)

The immense power requirements of artificial intelligence are forcing a strategic pivot in corporate energy procurement, moving beyond intermittent renewables to a diversified portfolio of firm, 24/7 carbon-free energy. Hyperscalers are now signing multi-gigawatt Power Purchase Agreements (PPAs) that include baseload sources like nuclear and hydropower to guarantee reliability. This is evidenced by Microsoft’s record-breaking 10.5 GW renewable energy deal with Brookfield Asset Management and Google’s pioneering 500 MW PPA for a Small Modular Reactor (SMR) with Kairos Power. The dominant theme for 2025 and beyond is the aggressive pursuit of a stable, hourly-matched clean energy supply, making power availability and reliability the paramount concern for data center expansion.

1. Total Energies & Google (February 2026)

Company: Google

Installation Capacity: 1, 000 MW (1 GW)

Applications: Powering data centers

Source: Total Energies and Google’s 1 GW Solar Deal Signals a New Phase …

2. Google & Linea Energy (June 2026)

Company: Google

Installation Capacity: 500 MW

Applications: Powering data centers in Texas

Source: Power Generation News – Energy Transition Finance

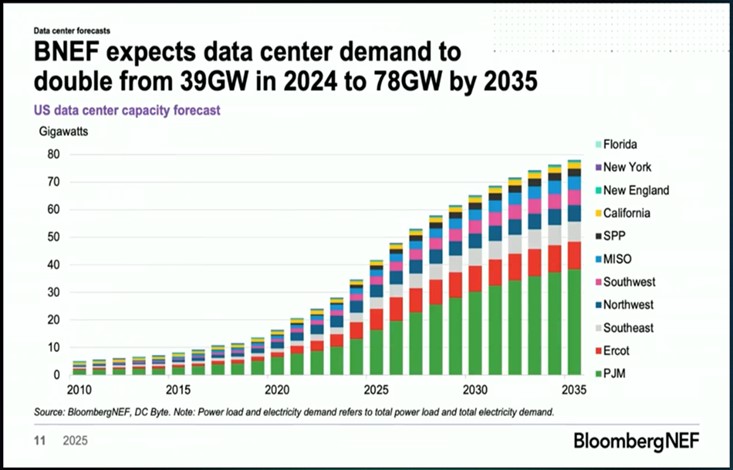

US Data Center Power Demand to Double by 2035

This PPA with a US-based partner is a strategic move by Google to secure energy in the American market, where data center power demand is forecast to double by 2035.

(Source: JD Supra)

3. Google & En BW (February 2026)

Company: Google

Installation Capacity: 100 MW

Applications: Powering European data centers

Source: Google inks PPA for 100 MW from Germany’s largest offshore wind …

ICT Sector Dominates European Renewable Energy Deals

The deal between tech giant Google and European utility EnBW is a specific example of the trend shown in the chart, where the ICT sector is the primary driver of renewable energy deals in Europe.

(Source: Rezolv Energy)

4. Meta & Unnamed Partner (March 2026)

Company: Meta

Installation Capacity: 80 MW

Applications: Powering data centers

Source: Meta Strikes 80 MW Solar Deal to Power Data Centers and Cut …

Corporate PPAs Drive Renewable Energy Growth

This deal, even with an unnamed partner, illustrates the fundamental trend that corporate PPAs are a primary mechanism for financing and developing new renewable energy capacity.

(Source: Federal Reserve Bank of Dallas)

5. Clearway Energy Group & Google (November 2025)

Company: Google

Installation Capacity: 1, 200 MW (1.2 GW)

Applications: Powering data centers across multiple U.S. grids

Source: Category Archives: Data Centers and AI – Advanced Power Alliance

Corporate Renewable PPA Market Sees Massive Growth

Google’s agreement with Clearway Energy Group contributes to and is representative of the massive overall growth in the corporate renewable PPA market depicted in the chart.

(Source: Market.us Scoop)

6. Google & Brookfield Renewable (October 2025)

Company: Google

Installation Capacity: 670 MW

Applications: Securing baseload hydropower for data centers

Source: Power Update: A Surging Data Center Tide Lifts The Power Sector

Corporate Clean Energy Dealmaking Slows In 2025

This major PPA, scheduled for late 2025, stands out as a significant transaction, highlighting that strategic, large-scale deals can still be made even during a period of potential market slowdown.

(Source: BloombergNEF)

7. Meta & AES Corporation (May 2025)

Company: Meta

Installation Capacity: 650 MW

Applications: Supporting U.S. data centers with solar power

Source: Meta Buys 650 MW of Renewable Energy to Power U.S. Data Centers

8. Meta & Enbridge (July 2025)

Company: Meta

Installation Capacity: 600 MW

Applications: Powering Texas data centers with solar

Source: Meta to power Texas data centers with 600-MW solar plant

PPAs Gain Share in Corporate Renewable Procurement

Meta’s choice to use a PPA with Enbridge reinforces the trend shown in the chart, where Power Purchase Agreements are increasingly the preferred method for corporations to procure renewable energy over other options.

(Source: Market.us Scoop)

9. Microsoft & Brookfield Asset Management (May 2024)

Company: Microsoft

Installation Capacity: 10, 500 MW (10.5 GW)

Applications: Powering global data centers with a renewable portfolio

Source: Microsoft just signed the biggest corporate renewable energy deal …

Data Centers Driving Unprecedented Energy Demand

This massive PPA from May 2024 is a direct corporate response to the fundamental market driver: the unprecedented and escalating energy demand from data centers, as shown in the chart.

(Source: Enverus)

10. Google & Kairos Power (2024)

Company: Google

Installation Capacity: 500 MW

Applications: Securing firm nuclear power for 24/7 data center operations

Source: Do PPAs have a future in the data center sector? – DCD

Table: Top 10 Data Center PPAs (2024-2026)

| Company | Installation Capacity | Applications | Source |

|---|---|---|---|

| Microsoft | 10, 500 MW | Powering global data centers with a renewable portfolio | Microsoft just signed the biggest corporate renewable energy deal … |

| 1, 200 MW | Powering data centers across multiple U.S. grids | Category Archives: Data Centers and AI – Advanced Power Alliance | |

| 1, 000 MW | Powering data centers | Total Energies and Google’s 1 GW Solar Deal Signals a New Phase … | |

| 670 MW | Securing baseload hydropower for data centers | Power Update: A Surging Data Center Tide Lifts The Power Sector | |

| Meta | 650 MW | Supporting U.S. data centers with solar power | Meta Buys 650 MW of Renewable Energy to Power U.S. Data Centers |

| Meta | 600 MW | Powering Texas data centers with solar | Meta to power Texas data centers with 600-MW solar plant |

| 500 MW | Powering data centers in Texas | Power Generation News – Energy Transition Finance | |

| 500 MW | Securing firm nuclear power for 24/7 data center operations | Do PPAs have a future in the data center sector? – DCD | |

| 100 MW | Powering European data centers | Google inks PPA for 100 MW from Germany’s largest offshore wind … | |

| Meta | 80 MW | Powering data centers | Meta Strikes 80 MW Solar Deal to Power Data Centers and Cut … |

10.5 GW, Microsoft’s Record PPA Signals Market Shift

The scale and diversity of recent PPAs indicate that hyperscale data center operators are no longer just passive buyers of clean energy but are actively shaping energy markets. While massive renewable portfolio deals remain a cornerstone, as seen with Microsoft‘s historic 10.5 GW agreement with Brookfield, there is a clear trend toward technological diversification. The inclusion of 670 MW of hydropower in Google’s procurement strategy and a pioneering 500 MW deal for SMR nuclear power demonstrates that achieving 24/7 carbon-free energy is now the primary objective. This implies a strategic calculation that the intermittency of solar and wind alone cannot provide the required reliability for AI workloads, pushing companies to secure firm, baseload clean power sources to ensure constant operations.

Corporate Renewable PPA Capacity Surges Globally

Microsoft’s record-breaking 10.5 GW deal is a primary example and a significant contributor to the global surge in corporate PPA capacity illustrated by the chart, signaling a major market shift.

(Source: Market.us Scoop)

USA & Europe, Microsoft and Google Lead Global PPA Deals

The geographic focus of these mega-deals is concentrated in the United States and Europe, which offer mature regulatory frameworks and abundant renewable resources. In the U.S., Texas is a clear hotspot, with Meta and Google signing multiple large-scale solar PPAs to leverage the favorable market conditions in ERCOT. Google’s 1.2 GW portfolio deal with Clearway Energy Group spans multiple U.S. states, indicating a strategy of geographic diversification to mitigate grid-specific risks. In Europe, Google’s 100 MW offtake from En BW‘s offshore wind farm in Germany highlights the region’s leadership in this technology. Microsoft’s 10.5 GW deal explicitly targets projects in both the U.S. and Europe, confirming a global procurement strategy led by the largest tech firms to secure power in their primary data center markets.

Tech Giants Lead European PPA Contract Volume

This chart directly supports the section’s claim by providing data that shows tech giants like Microsoft and Google are leading the European market in PPA contract volume.

(Source: Rezolv Energy)

Google’s 500 MW SMR Deal Signals New Tech Adoption (2024)

These agreements reveal a spectrum of technological maturity. Solar and wind remain the workhorses of corporate decarbonization, demonstrated by the sheer volume of capacity contracted by Meta, Google, and Microsoft. However, the most strategically significant development is the move to secure PPAs for emerging and established firm power technologies. Google’s PPA with Kairos Power for 500 MW of SMR nuclear energy is a landmark event, signaling commercial validation for a next-generation technology previously confined to development stages. This marks the first major corporate PPA for an SMR, potentially de-risking the technology for other industrial offtakers. Similarly, Google‘s 670 MW PPA with Brookfield Renewable for hydropower represents a strategic return to a mature, baseload technology to ensure unwavering grid stability for its data centers.

Power is the Top Factor for Data Center Site Selection

The section on Google’s SMR deal highlights a strategic response to the issue shown in the chart; by investing in new, locatable power technology, companies can address the primary constraint of data center site selection.

(Source: JD Supra)

24/7 Clean Power, Google’s 670 MW Hydro PPA Sets Trend

Looking ahead, the most critical strategic action involves hyperscalers deepening their integration with the energy sector, moving beyond simple offtake agreements to directly funding and influencing grid development. Recent signals suggest this trend is already underway and accelerating.

- The Ratepayer Protection Pledge signed with the White House in March 2026 commits major tech firms to help fund the grid infrastructure upgrades their facilities necessitate, marking a new era of direct financial responsibility.

- The pursuit of 24/7 carbon-free energy, as exemplified by Google’s diverse procurement including hydropower and nuclear, is becoming the industry standard, forcing a move beyond simply balancing annual renewable energy credits.

- Reports of potential acquisitions, such as Alphabet’s rumored $4.75 billion bid for developer Intersect Power, suggest a future where hyperscalers may transition from being energy customers to energy asset owners to secure their supply chain.

- The unprecedented scale of deals like Microsoft’s 10.5 GW PPA is establishing a new class of energy buyer that commands enough demand to underwrite gigawatts of new generation, fundamentally altering utility and developer planning.

Big Tech’s Renewable Energy Strategies Compared

Google’s pioneering 24/7 clean power strategy, exemplified by this trend-setting hydro PPA, is a key strategic differentiator that would be a central point of analysis in a chart comparing big tech’s energy strategies.

(Source: Green Fuel Journal)

The questions your competitors are already asking

This report covers one angle of the corporate PPA market for data center and AI power. The questions that matter most depend on your work.

- Which hyperscalers are gaining or losing ground in the race to secure 24/7 carbon-free energy?

- What is the outlook for SMR deployment for data center power by 2030?

- How do nuclear SMR PPAs compare to large-scale renewable PPAs for providing baseload data center power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.