Australia Data Center Grid Strain, 430 MW Amazon PPA, AEMC Proposes New Ride-Through Rules (2025 to 2026)

Industry Risks: Australia Data Centers Face Systemic Failure Threats and 26% Price Hike Warnings

The primary risk for Australia’s data center sector has shifted from managing market growth to mitigating direct threats of grid destabilization, prompting unprecedented regulatory intervention in 2026. Before 2025, the industry focused on land acquisition and capacity expansion in a market characterized by strong, but manageable, power demand. The recent explosion in AI-driven workloads has created a new class of risk where the sheer electrical load and operating characteristics of new facilities threaten the stability of the National Electricity Market (NEM), forcing a fundamental change in how projects are planned and approved.

- In the 2021-2024 period, the main risk was securing favorable real estate and grid connections in a competitive market. In contrast, by 2026 the risk profile has escalated to a systemic level. Fitch Ratings now flags the sector’s expansion as a direct pressure point on Australia’s energy transition, with a key concern being the potential for multiple facilities to trip offline during a grid fault, triggering cascading blackouts.

- A stark indicator of this shift is the June 2026 warning from the Climate Council that the data center boom could drive household electricity prices up by 26%. This concern was not part of the mainstream discourse prior to 2025, when data centers were seen primarily as a driver of digital economic growth rather than a direct cost burden on consumers.

- The Australian Energy Market Commission (AEMC) responded in March 2026 by proposing new grid standards. These rules would force data centers to “ride through” grid disturbances, a significant departure from the previous model where facilities could disconnect to protect their own IT equipment at the expense of grid stability.

- The issue of grid congestion has become acute. Transgrid, a major network operator, reported receiving connection inquiries for over 14 GW of data center capacity, much of it speculative. This “phantom demand” complicates network planning and creates connection queues of 3-7 years, a bottleneck that was less severe in the pre-AI boom era. These pressures are also a growing concern for grid operators like Dominion in high-demand regions of the United States.

Investment Analysis: A $155 B Pipeline Confronts New Regulatory and Infrastructure Costs

While Australia’s data center investment pipeline has surged to an estimated A$155 billion, the financial calculus for these projects has been fundamentally altered by new government policies that shift infrastructure costs onto developers. The period before 2025 was defined by investment focused on building shell and core capacity. The current environment forces developers to internalize the costs of grid upgrades and new renewable energy generation, making energy strategy, not just real estate, the core component of project financing.

- The scale of investment has accelerated dramatically, becoming a primary driver of Australia’s 6.5% rise in private new capital expenditure in the March 2026 quarter. This contrasts with the steadier, more incremental growth seen between 2021 and 2024.

- In March 2026, the Australian Government released its “Expectations of data centres” framework, a landmark policy shift. It formally requires developers to underwrite new renewable generation and pay their full share of grid expansion costs, a direct financial burden that did not exist in prior years.

- This new cost reality is driving a strategic response. Genaspi Energy recently secured a contract under the federal Capacity Investment Scheme (CIS) to build a 300 MW solar farm and a 300 MW/1, 200 MWh battery specifically to power a major AI data center, demonstrating the emerging model of co-developed energy and digital infrastructure.

AI Power Surge Requires Massive Grid Investment

This chart directly supports the section’s focus on new infrastructure costs by highlighting the massive grid investment required to support the power surge from AI, a key component of the overall investment analysis for the $155B pipeline.

(Source: Aon)

Table: Australia Data Center Strategic Capital and Policy Shifts

| Entity / Policy | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Westpac Analysis | May 2026 | Estimated the total investment pipeline for Australian data centers to exceed A$155 billion, highlighting the sector’s macroeconomic significance. | Westpac IQ |

| Australian Bureau of Statistics | May 2026 | Identified data center expansions as a key driver of the 6.5% increase in private new capital expenditure for the March quarter, showing the sector’s growing impact on the national economy. | ARNnet |

| Goodman Group | Nov 2025 | Reported its data center development pipeline had reached A$17.5 billion, illustrating the scale of capital being committed by major property developers to the sector. | The B 2 B Market Report |

Partnership Analysis: Amazon’s 9 PPAs and Genaspi’s CIS Contract Signal a New Energy Model

Partnerships in the Australian data center market have evolved from traditional construction and colocation agreements to sophisticated energy-focused alliances designed to secure power and meet new regulatory demands. The dominant trend since 2025 is the move by hyperscalers and developers to directly underwrite new renewable energy projects through large-scale Power Purchase Agreements (PPAs), a strategy that was nascent in the 2021-2024 period but is now a prerequisite for major developments.

- Amazon Web Services (AWS) executed its largest renewable energy investment in the country in April 2026, signing nine new PPAs to add 430 MW of solar, wind, and battery capacity. This proactive procurement strategy is designed to de-risk its energy supply and meet both its corporate sustainability goals and the government’s new expectations.

- The partnership between Genaspi Energy and a major AI client, backed by a federal CIS contract, exemplifies the new “energy-sovereign” data center model. The development directly links a 1, 200 MWh battery and a 300 MW solar farm to a data center load, bypassing public grid constraints.

- These energy-centric partnerships reflect a global trend, as seen with hyperscalers exploring novel power sources, including collaborations with advanced nuclear developers like Thea Energy to meet future demand.

- The AEMC’s proposed rules are also forcing new technical partnerships. The requirement for ride-through capabilities makes co-located Battery Energy Storage Systems (BESS) a near-necessity, driving alliances between data center operators and energy storage providers like Bloom Energy.

Table: Australia Data Center Strategic Energy Partnerships

| Lead Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Genaspi Energy / AI Client | Jun 2026 | Won a federal CIS contract to build a 300 MW solar farm and a 300 MW/1, 200 MWh battery to directly power a major AI data center, creating a dedicated, “net renewable” grid. | Renew Economy |

| Amazon | Apr 2026 | Announced nine new PPAs in Australia, adding 430 MW of clean power capacity from solar, wind, and battery projects to support its data centers. | Data Centre Magazine |

| Microsoft | Feb 2026 | Met its goal to match 100% of its electricity use with renewable energy purchases, partly via a 15-year PPA with FRV Australia, showing early-mover advantage in renewable procurement. | Microsoft News |

Geographic Focus: Grid Constraints in Sydney Push Data Center Growth Toward Regional Zones

The geographic strategy for data center development in Australia is shifting from consolidating in established hubs to diversifying into regional areas to circumvent grid limitations. Between 2021 and 2024, development was heavily concentrated in Sydney, the country’s largest market. Since 2025, severe power constraints and connection delays in Sydney have forced developers to explore regional locations closer to renewable energy zones, trading proximity to the city for access to power, a trend also emerging in other constrained markets across the ASEAN region.

- Sydney, which holds the majority of Australia’s data center capacity, has become a victim of its own success. The concentration of facilities has exhausted available grid capacity in key western suburbs, leading to project delays and forcing network operators to plan major, costly upgrades.

- In response, developers are actively pursuing sites in regional New South Wales, Victoria, and other states. This strategy aims to co-locate new data centers with large-scale solar and wind farms, aligning with the government’s expectation that new demand is met with new supply.

- This regional diversification presents its own challenges. While power may be more accessible, these locations often lack the rich fiber optic connectivity and skilled workforce readily available in metropolitan hubs like Sydney, creating new logistical and operational hurdles.

Technology Maturity: AI Power Demand Forces Shift From Air to Liquid Cooling as a Baseline

The technology underpinning data center operations is undergoing a forced evolution, driven by the extreme power densities of AI hardware from companies like NVIDIA. Before 2025, air cooling was the default for the vast majority of facilities. Today, the power and heat generated by AI workloads are making liquid cooling a foundational requirement for new builds, shifting it from a niche, high-performance option to a mainstream commercial necessity. This change is critical for managing the power consumption that is straining the grid.

- The shift is validated by market forecasts. The global data center liquid cooling market is projected to grow from USD 6.77 billion in 2026 to USD 18.79 billion by 2031. This rapid adoption is a direct response to the inadequacy of air cooling for AI infrastructure.

- Liquid cooling offers significant efficiency gains, which are now critical for project viability. It can improve a data center’s Power Usage Effectiveness (PUE) by 0.1 to 0.3 and reduce electricity use for cooling by 15-20%. In the current environment of extreme power costs and grid constraints, these savings are no longer optional optimizations but essential enablers.

- The industry’s technical challenges are attracting new solution providers. Companies like Wiwynn are focusing on integrated power and cooling solutions for AI racks, indicating that the technology is maturing from components to integrated systems designed for rapid deployment at scale.

SWOT Analysis: Australia’s Data Center Sector at a Strategic Inflection Point

The Australian data center market has transitioned from a period of straightforward expansion to a complex new phase where energy and grid integration have become the central determinants of success or failure. The strengths that made Australia an attractive investment destination are now being tested by the acute weaknesses in its energy infrastructure, creating both significant threats and opportunities for developers who can adapt their business models.

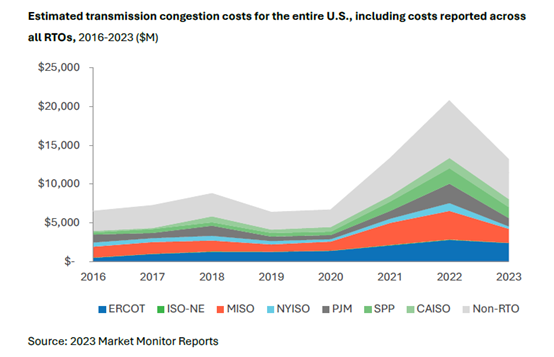

US Grid Congestion Costs Exceed $20B Annually

This chart provides a powerful case study for the ‘Threats’ and ‘Weaknesses’ components of the SWOT analysis. It quantifies the immense financial risk of grid congestion in a mature market, serving as a cautionary example for Australia’s strategic planning.

(Source: Prisma Photonics)

Table: SWOT Analysis for the Australian Data Center Market

| SWOT Category | 2021 – 2024 (Growth Phase) | 2025 – 2026 (Constraint Phase) | What Changed / Validated |

|---|---|---|---|

| Strengths | Politically stable, strong digital economy, attractive to global capital. Established as a primary data hub in the APAC region. | Massive A$155 B investment pipeline. Proactive regulatory action (AEMC, Federal Gov.) creating clear rules for development. Hyperscalers like Amazon are willing to fund new renewable projects. | The market’s attractiveness was validated by a surge in capital, but this also triggered a necessary, and ultimately positive, regulatory response to ensure sustainable growth. |

| Weaknesses | Aging transmission infrastructure. Growing, but manageable, concentration of demand in Sydney. | Severe grid bottlenecks with 3-7 year connection queues. Inability of existing grid to handle “lumpy” data center loads, creating systemic risk of cascading failures. | The simmering weakness of the grid was exposed and became an acute, primary constraint due to the speed and scale of the AI-driven demand shock. |

| Opportunities | Capture growing cloud adoption and digital service demand across the APAC region. Expand colocation capacity. | Mandates to underwrite renewables can accelerate Australia’s energy transition. Develop new “grid-positive” data center models with integrated storage. Drive innovation in liquid cooling and energy efficiency. | The crisis created an opportunity to redefine the data center’s role in the energy system, shifting it from a passive consumer to an active enabler of renewable generation and grid stability. |

| Threats | Competition from other APAC markets like Singapore and Tokyo. Rising land and construction costs. | Project delays and cancellations due to power unavailability (20% of projects at risk globally). Potential for electricity prices to rise 26% for all consumers. Regulatory crackdown stifling speculative development. | The primary threat shifted from market competition to fundamental resource scarcity (power and grid access), jeopardizing the viability of the entire project pipeline and creating social and political risk. |

Scenario Modelling: “Energy-Sovereign” Data Centers to Define 2027 Viability

The most critical factor for the Australian data center market in the next 12-18 months will be the ability of developers to execute on integrated energy strategies, effectively becoming “energy-sovereign.” Projects that continue to rely on speculative access to the public grid will face significant delays and cancellations, while those that bring their own power supply to the table will capture the market. This is not just a problem for Australia; developers in India such as Adani are facing similar challenges.

- If this happens: The final AEMC rule, expected in mid-2026, is implemented as proposed, mandating ride-through capabilities and other strict performance standards.

Watch this: An immediate increase in the deployment of on-site or co-located BESS for all new data center applications. Watch for partnership announcements between data center REITs and battery manufacturers. - If this happens: State planning authorities begin rejecting development applications that do not come with a dedicated PPA or direct investment in new renewable generation.

Watch this: A bifurcation of the market between well-capitalized hyperscalers (like Amazon and Microsoft) who can afford to underwrite gigawatt-scale renewable projects, and smaller colocation providers who may struggle to compete, potentially leading to market consolidation. - If this happens: Grid connection queues in Sydney and Melbourne show no signs of shortening despite network operator efforts.

Watch this: A surge in land acquisition and project announcements in regional areas near renewable energy zones, along with parallel investments in long-haul fiber optic networks to connect these remote sites back to major internet exchange points.

The questions your competitors are already asking

This report covers one angle of the escalating conflict between data center growth and grid stability in Australia. The questions that matter most depend on your work.

- What is the outlook for data center deployment in Australia’s National Electricity Market (NEM) given the systemic risks flagged by Fitch Ratings?

- What is the status of the AEMC’s proposed ride-through rules, and how will they impact project approvals from 2026 onwards?

- Which data center operators are gaining or losing ground based on their readiness for Australia’s new grid standards and the threat of a 26% price hike?

- What are the opportunities for grid-stabilizing solutions, like battery storage and demand response, in the Australian data center market?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.