Oilfield Services Pivot to Offshore Wind: Halliburton’s 2026 Foundation Strategy Signals Market Shift

Commercial Adoption: From O&G Focus to Offshore Wind Foundation Projects

Halliburton executed a significant strategic shift in 2025, moving from a position of non-participation in the offshore wind market to actively commercializing enabling technologies for the sector’s most complex challenges. This pivot repurposed its core oil and gas competencies to directly address the high-growth floating offshore wind segment, a clear departure from its pre-2025 strategy of observing the clean tech space from a distance.

- Between 2021 and 2024, Halliburton’s engagement with clean energy was indirect, primarily through its Halliburton Labs accelerator, which incubated startups in adjacent fields like energy storage and hydrogen but had no companies focused on offshore wind. The company’s commercial activities remained exclusively within oil and gas.

- This changed on September 15, 2025, when Halliburton announced a scalable micropile anchoring solution developed with Subsea Micropiles. This technology is designed specifically for offshore wind foundations, providing a method to secure large structures in deep-water environments where floating wind projects are developed.

- The move strategically targets the floating offshore wind foundation market, a segment projected to grow to $15 billion by 2033 at a 15% compound annual growth rate. This allows Halliburton to enter the renewables supply chain by leveraging its existing expertise in subsea engineering, drilling, and grouting.

- This initiative is part of a broader portfolio of energy transition services. The company’s work in Carbon Capture and Storage (CCS), such as its contract for the Northern Endurance Partnership (NEP) project in the UK, demonstrates its strategy of providing specialized technical services across multiple decarbonization sectors.

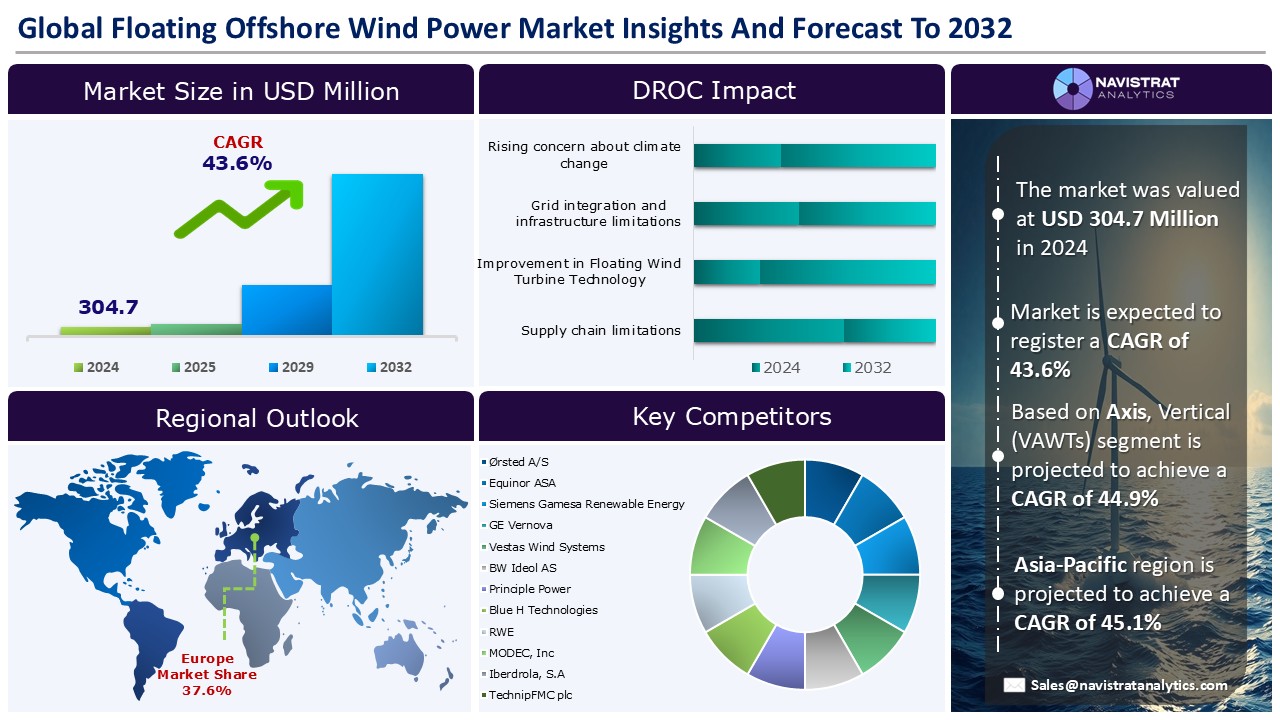

Floating Wind Market Poised for Explosive Growth

This chart quantifies the “high-growth floating offshore wind segment” Halliburton is targeting, validating its strategic pivot with a forecasted 43.6% compound annual growth rate.

(Source: Navistrat Analytics)

Partnership Ecosystem: Halliburton’s Alliances for Offshore Wind and Energy Transition

Halliburton’s partnership strategy evolved significantly after 2024, shifting from exclusively oil and gas-focused alliances to targeted collaborations aimed at developing and commercializing new technologies for offshore wind and adjacent low-carbon markets. This reflects a calculated move to build a diversified energy services portfolio.

- Prior to 2025, major partnerships, such as the long-term drilling services agreement with Vår Energi in June 2023 and the deepwater technology collaboration with Oil States Industries in November 2023, were aimed at strengthening its core offshore O&G offerings.

- The collaboration with Subsea Micropiles, announced in September 2025, marks the company’s first major technology partnership targeting the offshore wind sector. This alliance was instrumental in validating the new micropile anchoring and grout solution for wind foundations.

- In October 2025, Halliburton partnered with Volta Grid to provide distributed, lower-emission power for data centers, starting in the Middle East. While not directly a wind initiative, this move into stationary power for energy-intensive industries signals a clear diversification strategy beyond traditional oilfield services.

- The launch of the NEX Lab in January 2026 with Singapore’s A*STAR reinforces its R&D focus on advanced well completion technologies with applications across traditional energy, geothermal, and CCS, creating technological synergies that support its entire energy transition portfolio.

Table: Halliburton Energy Transition Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| A*STAR | Jan 2026 | Launched the NEX Lab to accelerate R&D for advanced well completion technologies applicable to energy, geothermal, and CCS. | JPT |

| Volta Grid | Oct 2025 | Strategic collaboration to develop and deploy distributed power generation systems for data centers, marking a diversification into stationary power markets. | World Oil |

| Subsea Micropiles | Sep 2025 | Technology collaboration to develop and validate a scalable micropile anchoring solution and innovative grout for offshore wind foundations. | Halliburton |

| In Capture JV | Mar 2025 | Awarded a service contract for technical assessment of a commercial-scale Carbon Capture & Storage (CCS) project offshore Australia. | World Oil |

Geographic Pivot: Targeting UK and US Offshore Wind Growth Hubs

Halliburton’s energy transition activities show a strategic geographic focus, initially concentrating on major oil and gas basins while positioning itself to capture future growth in key offshore wind markets like the UK and the US post-2025.

Global Offshore Wind Capacity Nears 500 GW

This forecast supports Halliburton’s geographic pivot by showing significant projected capacity growth in its target markets, with Europe reaching 195.4 GW and the U.S. growing to 30.2 GW.

(Source: Motive Power)

- Between 2021 and 2024, Halliburton’s geographic investments were centered on reinforcing its presence in major O&G hubs. This included opening new facilities in Namibia and Senegal and securing long-term contracts in Norway and Brazil.

- The company’s contract for the Northern Endurance Partnership (NEP) CCS project in August 2025 strategically places it in the UK North Sea, a primary hub for European decarbonization and offshore wind development. This allows Halliburton to build a track record in a key region for future wind projects.

- This positioning aligns with major government initiatives. The UK government’s $400 million commitment to its domestic offshore wind supply chain and the US target of 30 GW of offshore wind by 2030 represent the primary target markets for Halliburton’s new foundation technology and related services.

- Similarly, securing CCS assessment work in Australia with the In Capture JV in March 2025 establishes a foothold in another significant Asia-Pacific energy transition market, creating future opportunities for its integrated service offerings.

Technology Readiness: Micropile Anchors Move from R&D to Commercial Validation

In 2025, Halliburton advanced its energy transition technology from an exploratory phase centered on incubation to the commercial launch of a specialized solution for the offshore wind market, marking a critical step in technology readiness and a shift toward commercial deployment.

Floating Wind Market to Exceed $7.6B

This chart illustrates the significant market value for which Halliburton’s new micropile anchor technology is competing, justifying the company’s move from R&D to commercialization.

(Source: Global Market Insights)

- From 2021 to 2024, Halliburton’s clean tech strategy was defined by Halliburton Labs, which fostered early-stage, external technologies in areas like hydrogen (Sun Green H 2) and energy storage (Cache Energy) without direct product commercialization.

- The announcement of the scalable micropile anchoring solution in September 2025 represents a major maturity milestone. The technology was described as “developed and validated, ” indicating it has moved beyond the R&D phase and is ready for market adoption in floating and fixed-bottom wind farms.

- This core offering is supported by a portfolio of other mature technologies with direct applicability to offshore wind. The ROCS umbilical-less tubing hanger system, deployed with Shell in October 2025, introduces principles of remote, automated subsea installation that can reduce risk and cost in foundation and cable work.

- Likewise, the Range Star geothermal service, launched in 2025, provides precise subsurface navigation technology that is directly transferable to the accurate drilling of foundation piles required for large offshore wind turbines.

SWOT Analysis: Halliburton’s Strategic Position in the Offshore Wind Market

Halliburton’s strategic pivot in 2025 leveraged its deep-seated strengths in subsea engineering to seize a high-value opportunity in floating offshore wind, but its success now depends on overcoming new market competition and commercializing its technology at scale.

- The company successfully repurposed its core O&G strengths to enter the renewables market, validating its new strategy.

- Its primary weakness shifted from a complete lack of experience in wind to being an unproven supplier at a commercial scale in a competitive market.

- The opportunity became highly specific and actionable, moving from broad energy transition concepts to the tangible, high-growth floating wind foundation market.

Table: SWOT Analysis for Halliburton’s Offshore Wind Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Extensive subsea and drilling expertise; global O&G operational footprint; strong balance sheet. | Demonstrated ability to repurpose subsea expertise for wind foundations; established credentials in CCS projects (NEP); R&D infrastructure (NEX Lab). | The company validated its ability to apply core competencies to a new, high-growth renewables market segment, moving from theoretical strength to practical application. |

| Weaknesses | No direct experience or track record in the offshore wind supply chain; revenue heavily concentrated in O&G markets. | Limited commercial track record in delivering offshore wind projects; competing against established wind service providers like Subsea 7. | The weakness shifted from a ‘knowledge gap’ to a ‘commercialization gap.’ The challenge is no longer a lack of capability but the need to secure market share. |

| Opportunities | Broad growth in adjacent markets like CCUS, hydrogen storage, and geothermal energy. | Targeted entry into the high-growth floating offshore wind foundation market ($15 B by 2033); government support for domestic supply chains (UK, US). | The opportunity became specific and actionable. The company identified a precise, high-margin niche (foundations) that aligns perfectly with its existing strengths. |

| Threats | O&G market volatility; broad ESG pressure from investors to decarbonize operations. | Intense competition in the wind services market; risk of new micropile technology not achieving widespread commercial adoption or being out-innovated. | The threat evolved from broad, external pressures (ESG) to specific, internal market execution risks (commercial failure of a new technology). |

2026 Outlook: Commercial Contracts for Foundation Tech are the Next Critical Milestone

The defining indicator of Halliburton’s success in the offshore wind sector will be its ability to convert its 2025 technological launch into a significant commercial contract for a major floating wind project in 2026.

Major 2.8 GW US Wind Project Proposed

This chart provides a concrete example of the type of “large-scale commercial contract” in a key target market (US) that represents Halliburton’s next critical milestone.

(Source: Community Offshore Wind)

- If Halliburton secures a large-scale commercial contract for its micropile anchoring solution, watch for an acceleration of its energy transition strategy. This could include further R&D investment or the acquisition of complementary wind service companies to broaden its portfolio.

- These could be happening: other major oilfield service companies like SLB and Baker Hughes may be prompted to accelerate their own direct entries into the wind services market, intensifying competition for specialized services.

- Watch for the formal adaptation and marketing of Halliburton’s digital platforms, such as its drilling automation software, for offshore wind applications. This would signal a deeper integration of its technology stack into the renewables value chain, targeting the $13.44 billion wind O&M market.

- A key signal to monitor is the integration of its service offerings. Observe whether the company begins to bundle its CCS, geothermal, and offshore wind foundation services into a comprehensive “decarbonization infrastructure” package for major energy clients.

Frequently Asked Questions

What was Halliburton’s main strategy shift in 2025?

In 2025, Halliburton moved from a position of non-participation in offshore wind to actively commercializing a ‘scalable micropile anchoring solution’ for the sector. This pivot repurposed its core oil and gas competencies in subsea engineering and drilling to directly target the high-growth floating offshore wind foundation market, a clear departure from its pre-2025 strategy of only observing the clean tech space.

What specific technology is Halliburton offering for the offshore wind market?

In partnership with Subsea Micropiles, Halliburton is offering a ‘scalable micropile anchoring solution’ and an innovative grout. This technology is designed to secure the foundations of large offshore wind turbines, especially for floating projects in deep water, leveraging the company’s expertise in subsea drilling and grouting.

Why is Halliburton targeting the floating offshore wind market specifically?

Halliburton is targeting the floating offshore wind foundation market because it is a rapidly growing segment, projected to become a $15 billion market by 2033. This niche allows the company to apply its existing strengths in subsea engineering to a complex, high-value problem, providing a strategic entry point into the renewables supply chain without having to compete in all areas of wind energy services.

How was Halliburton involved in clean energy before 2025?

Before 2025, Halliburton’s engagement in clean energy was indirect. It ran the Halliburton Labs accelerator, which supported startups in areas like energy storage and hydrogen. However, the company itself did not have any commercial products or services for the renewables sector, and its business activities were exclusively focused on oil and gas.

What is the next major milestone for Halliburton’s offshore wind strategy?

The next critical milestone is for Halliburton to secure a large-scale commercial contract in 2026 for its micropile anchoring solution on a major floating wind project. This would validate its technology at a commercial scale and signal a successful market entry, likely leading to an acceleration of its overall energy transition strategy.