Alkaline Electrolysis Cost Trajectory, 60% Chinese Cost Drop, €149 M Lhyfe Subsidy, and $2/kg Target (2025 to 2026)

Electrolyzer Supply Chain Risks, Chinese Dominance, 68% Capacity, and Western Response

The global green hydrogen industry’s path to cost-competitiveness is defined by a central tension: reliance on low-cost Chinese electrolyzers accelerates cost reduction but creates significant supply chain concentration risk, prompting Western nations to counter with substantial subsidies to foster domestic manufacturing. While this dynamic drives down the levelized cost of hydrogen (LCOH), it exposes the nascent market to geopolitical and logistical vulnerabilities.

- In the period from 2021 to 2024, the market was characterized by high-cost pilots in Europe and North America, with Western original equipment manufacturers (OEMs) leading technology development. However, by 2025–2026, Chinese manufacturers fundamentally altered the market by capturing an estimated 60% to 68% of global manufacturing capacity and driving down alkaline electrolyzer CAPEX to a $300–$450/k W range, a figure two to four times lower than Western equivalents.

- The availability of low-cost hardware from China is a primary enabler for projects targeting sub-$2/kg hydrogen, particularly in regions like India which are pursuing aggressive national hydrogen missions without large domestic subsidies. This creates a direct pathway to cost reduction independent of Western policy.

- This market shift has prompted warnings from European executives about losing the continent’s industrial base, highlighting the fragility of a supply chain dependent on a single region. Major project cancellations, like the $4 billion Topsoe and Air Products venture, underscore the real-world consequences of policy uncertainty and cost pressures in the West.

- In response, Western OEMs such as Cummins and Siemens Energy are now competing in a market where the price benchmark is set by Chinese scale, forcing accelerated innovation and cost-out programs to remain viable.

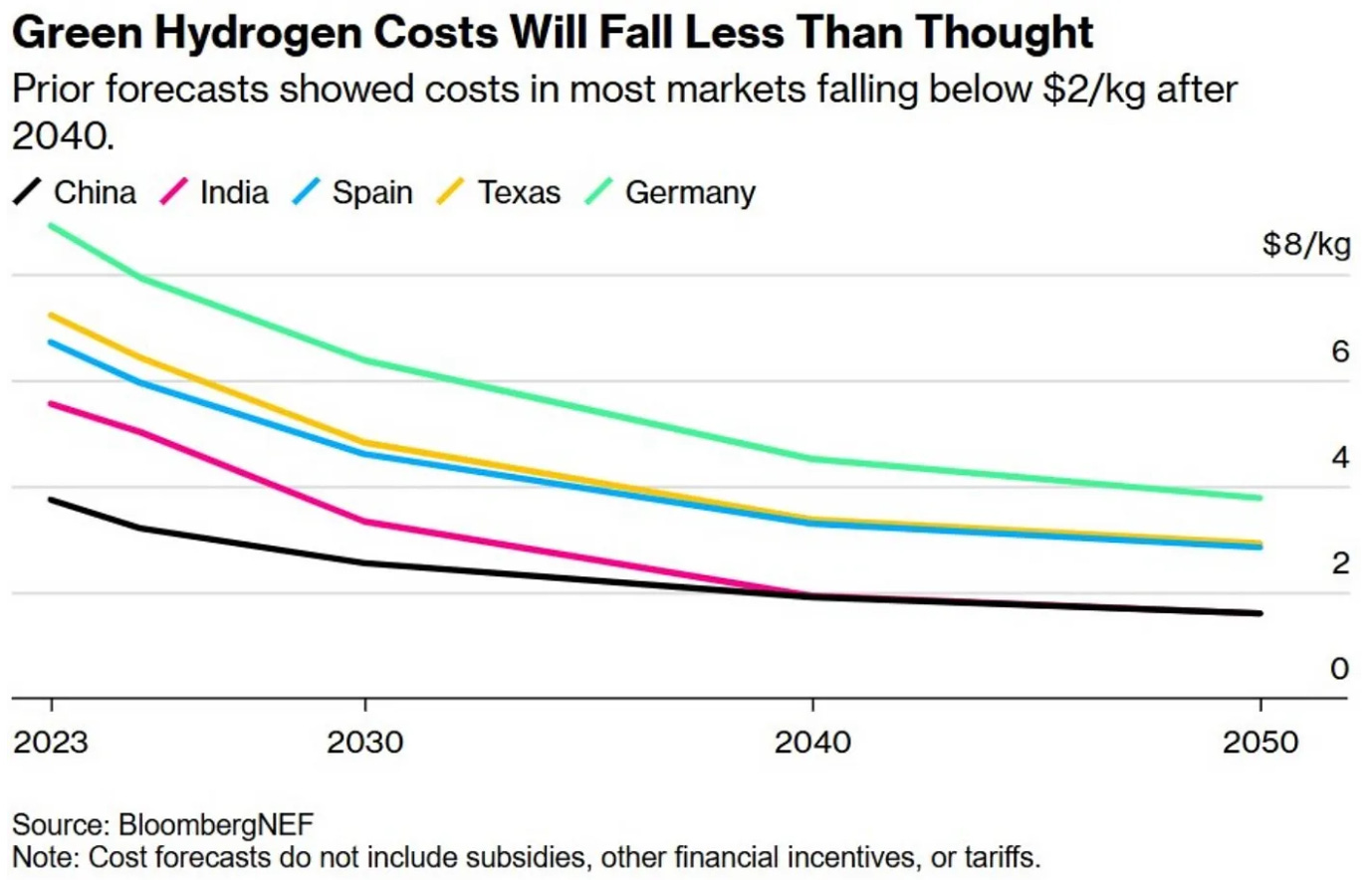

China to Lead Green Hydrogen Costs

This chart visualizes China’s projected cost leadership in green hydrogen, reinforcing the section’s point about Western reliance on low-cost Chinese electrolyzers.

(Source: Deep (Tech) Takes – Substack)

€4 B in Subsidies, France’s Hydrogen Strategy to Bridge the €5-€9/kg Cost Gap

European governments, led by France, are deploying billions in direct production subsidies to bridge the significant economic gap between the current green hydrogen cost of €5-€9/kg and the price needed for bankable offtake agreements, effectively de-risking early large-scale projects.

- France has committed €4 billion in subsidies as part of its national hydrogen strategy. A cornerstone of this policy was the April 2025 confirmation of a €149 million grant to the company Lhyfe for its 100 MW “Green Horizon” project near Le Havre, demonstrating direct state support for industrial-scale production.

- The French support mechanism, launched in January 2025, provides producers with aid over a 15-year period. It features a critical subsidy ceiling of €4/kg, which establishes a bankable revenue stream for producers even when their unsubsidized production costs are significantly higher.

- Complementing national efforts, the EU-wide European Hydrogen Bank is a key instrument for stimulating production. Its first auction in 2025 awarded €720 million to seven projects, while the second auction in February 2026 resulted in grant agreements for six projects representing 380 MW of new electrolysis capacity.

Table: European Green Hydrogen Subsidies and Initiatives

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| European Hydrogen Bank Auction 2 | Feb 2026 | Six projects signed grant agreements, adding a planned 380 MW of new electrolysis capacity across the EU to stimulate the market. | Hydrogen News from Europe |

| French National Subsidy Scheme | Mar 2026 | Analysis confirmed the average subsidy for supported low-carbon hydrogen projects is expected to be near €2/kg, creating a clear financial incentive for producers. | Argus Media |

| European Hydrogen Bank Auction 1 | Jul 2025 | Awarded €720 million to seven green hydrogen projects, primarily in Spain and Portugal, to kickstart large-scale production with direct financial backing. | Springer |

| Lhyfe “Green Horizon” Project | Apr 2025 | The French government confirmed a record €149 million subsidy for Lhyfe’s 100 MW plant, a key part of its €4 billion national hydrogen strategy. | Lhyfe |

China vs. Europe/US, A Fractured Path to $2/kg Green Hydrogen

The global race to $2/kg green hydrogen is fragmenting into two distinct regional models: a hardware-driven approach in China and India leveraging low-cost domestic manufacturing and access to cheap renewables, and a policy-driven approach in Europe and the US using massive subsidies to overcome higher domestic technology and energy costs.

- China and India are on the fastest track to unsubsidized cost parity. As of 2026, China hosts over 56% of global electrolyzer deployment, leveraging domestic manufacturing that has seen costs drop by over 60%. India has set a national mission to achieve a sub-$2/kg cost by 2030, with reports of discovered prices already hitting approximately $3.08/kg in early 2026.

- Europe remains dependent on subsidies to initiate projects. Policies like France’s €4/kg subsidy cap and the EU Hydrogen Bank’s auctions are explicitly designed to support projects with a current LCOH of €5/kg to €9/kg, with the strategic goal that building scale will eventually lead to organic cost reductions.

- The United States has implemented the world’s most aggressive production incentive via the Inflation Reduction Act. The $3.00/kg Clean Hydrogen Production Tax Credit (45 V) aims to make the US a market leader by directly buying down production costs, offsetting the higher price of domestically sourced equipment compared to Chinese imports.

Alkaline Electrolysis 60% Cost Drop Signals Commercial Dominance (2025 to 2026)

Alkaline electrolyzer technology has achieved commercial maturity and cost leadership at scale, evidenced by Chinese manufacturers’ ability to reduce CAPEX by over 60% and capture the majority of the global market. While Proton Exchange Membrane (PEM) technology continues to advance, in 2026 it remains a higher-cost alternative primarily suited for specific applications.

- While the period between 2021 and 2024 was marked by a technical debate between the flexibility of PEM and the scale of alkaline, the market in 2025–2026 shifted decisively toward cost. Chinese-made alkaline units at $300–$450/k W became the undisputed global price benchmark.

- PEM technology, offered by firms like ITM Power, has also seen cost reductions. However, with Western PEM systems priced at $1, 000–$2, 000/k W, they are largely positioned for applications where dynamic response or a smaller footprint justifies the significant cost premium over Chinese alkaline systems.

- The competitive pressure is forcing innovation in the West. In April 2026, German company Sunfire launched a new 50 MW pressurized alkaline electrolyzer module explicitly designed to reduce total installed project costs by up to 50%, a direct strategic response to Chinese price leadership.

SWOT Analysis, Green Hydrogen’s Cost Trajectory and Supply Chain Exposure

The green hydrogen market’s primary strength is its rapid, policy-supported cost decline, but this is inextricably linked to its greatest weakness and most pressing threat: an over-reliance on a geographically concentrated manufacturing base in China that creates significant supply chain and geopolitical exposure for Western adopters.

Green Hydrogen Market to Surge

This chart quantifies the market opportunity discussed in the SWOT analysis, visualizing the massive growth potential that represents a key strength.

(Source: MarketsandMarkets)

Table: SWOT Analysis for Green Hydrogen Cost Reduction

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong policy support and net-zero targets established the foundation for growth. | Aggressive cost reductions in Chinese electrolyzers (>60%) and massive subsidies (US $3/kg, France €2/kg) make cost targets tangible. | The path to $2/kg became a function of deployable capital and manufacturing scale, not just R&D. |

| Weaknesses | High LCOH ($4-6/kg) and expensive Western electrolyzers limited commercial viability. | A stark cost and scale disparity emerged, with Chinese alkaline units at $300/k W vs. Western units at $600-$1, 200/k W. | The reliance on Chinese hardware to meet cost targets was validated, creating a structural dependency for many projects. |

| Opportunities | Potential for cost-down curves through learning and scale. | New production methods, like co-electrolysis using biomass, offer pathways to costs below $2/kg. Western innovation (e.g., Sunfire) responds to price pressure. | The market validated that multiple pathways to cost reduction exist, from manufacturing scale to process innovation. |

| Threats | Uncertainty around subsidy mechanisms and project financing delays. | Geopolitical tension and potential trade barriers targeting the Chinese-dominated supply chain. Industry warnings of Europe losing its industrial base to China. | The threat shifted from a lack of technology to a concentrated, potentially volatile supply chain for the key enabling technology. |

2028-2030 Target, The Path to $2/kg Green Hydrogen in Optimal Regions

If Chinese electrolyzer CAPEX remains low and Western subsidy programs are fully implemented without major policy reversals, the first large-scale projects will achieve an effective LCOH of $2/kg between 2028 and 2030, but only in optimal regions that combine low-cost renewable PPAs, access to cheap hardware, and strong production incentives.

The Path to $2/kg Green Hydrogen

This chart perfectly illustrates the cost reduction timeline, showing the projected path to the $2/kg target central to this section.

(Source: Intelligent Living)

- A critical leading indicator is the unsubsidized LCOH from new projects in India, which has already reported discovered prices near $3/kg. Continued declines in this market will signal true, market-based cost parity is approaching, independent of Western subsidies.

- The bankability of projects in the US and Europe hinges on the final rules and consistent application of the 45 V tax credit and the next EU Hydrogen Bank auctions. Any wavering in this policy support would immediately delay projects and push back the timeline for achieving cost targets.

- The price of Chinese electrolyzers must be monitored closely. A significant price increase, driven either by surging domestic demand in China or the imposition of trade barriers by Western nations, would slow the global cost-down curve and defer the $2/kg goal for all regions.

The questions your competitors are already asking

This report covers one angle of the global race to achieve sub-$2/kg green hydrogen. The questions that matter most depend on your work.

- Which electrolyzer manufacturers are gaining or losing ground as Chinese suppliers capture over 60% of global capacity?

- What is the outlook for achieving a sub-$2/kg levelized cost of hydrogen (LCOH) by 2026?

- How do low-cost Chinese alkaline electrolyzers compare to Western equivalents on CAPEX for utility-scale projects?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.