Green Hydrogen Policy Risk: 6 Mtpa of Projects Halted, Atome Energy $665 M FID, and US 45 V Repeal (2025 to 2026)

Green Hydrogen Project Viability, Atome Energy’s FID vs. 6 Mtpa in Cancellations

In 2026, green hydrogen project viability has decisively split into two distinct and diverging paths, one centered on commercial fundamentals and the other on government subsidies. The first path is a subsidy-free model that de-risks development by securing low-cost renewable energy and binding offtake agreements, proven by Atome Energy’s Final Investment Decision (FID) for its Villeta project in April 2026. The second path, a subsidy-dependent strategy epitomized by the U.S. Department of Energy’s (DOE) Hydrogen Hubs program, is collapsing under the weight of severe policy risk, leading to widespread project cancellations and delays.

- Prior to 2025, the industry was characterized by a wave of ambitious project announcements, with developers banking on future government support, like the U.S. 45 V tax credit, to make projects economically viable.

- The landscape shifted dramatically in July 2025 with the passage of the “One Big Beautiful Bill Act” (OBBBA) in the U.S., which set a 2027 termination date for the crucial $3.00/kg hydrogen production credit.

- This policy reversal directly triggered a wave of industry retreats, with 6 million metric tons per annum (mtpa) of global projects being halted as incentives were scaled back.

- In sharp contrast, Atome Energy successfully navigated this turbulent period by structuring its project around a bankable offtake agreement with Yara International and access to low-cost hydropower, proving a commercially resilient alternative that does not depend on volatile government policy.

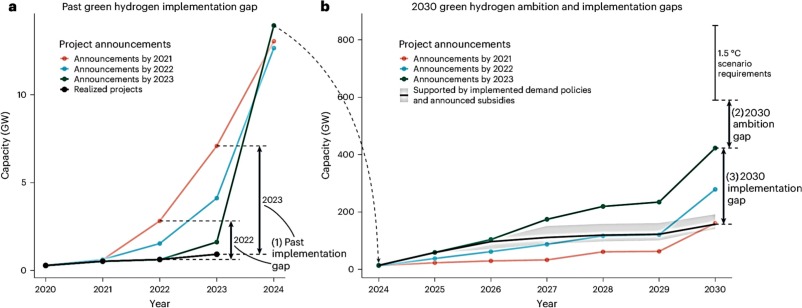

Green Hydrogen’s Widening Implementation Gap

This chart’s depiction of a growing gap between announced and realized projects directly visualizes the section’s central theme: the diverging paths of project viability and cancellation.

(Source: ScienceDirect.com)

$500 M in Cancellations, Air Products Halts NY Project Amid Policy Shifts

The profound policy uncertainty created by the OBBBA legislation in mid-2025 had an immediate and chilling effect on capital-intensive green hydrogen projects, leading to high-profile cancellations by major industrial players. This retreat demonstrated that for projects designed around government incentives, the risk of policy reversal is not a theoretical threat but an existential one that can halt development overnight.

Policy Landscape Steers Hydrogen Ecosystem

The diagram shows how the ‘Policy landscape’ is a primary driver of the hydrogen ecosystem, supporting the section’s focus on how policy shifts created existential risk for projects.

(Source: ScienceDirect.com)

- In February 2025, even before the OBBBA was passed, Air Products cancelled its planned $500 million green hydrogen facility in New York, citing market and policy headwinds that undermined the project’s economics.

- Following the OBBBA’s passage, the trend accelerated globally. In July 2025, BP abandoned its green hydrogen project in Australia, citing a strategic pivot back toward its core oil and gas operations.

- On the same day, Fortescue Metals Group also announced its exit from key hydrogen projects as part of a $150 million strategic refocus on its primary iron ore business.

- A broader market analysis from late 2025 confirmed the scale of the retreat, finding that over 75% of all announced green hydrogen projects were now at risk of cancellation due to a combination of funding gaps and policy instability.

Table: Major Green Hydrogen Project Cancellations (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| BP | July 2025 | Abandoned its planned green hydrogen production facility in Australia. The company stated the move was part of a strategic shift back toward oil and gas investments amid changing market conditions. | Reuters |

| Fortescue Metals Group | July 2025 | Halted its key hydrogen projects as part of a $150 million strategic pivot to refocus on its core iron ore mining operations. This marked a significant retreat from its aggressive green energy strategy. | Discovery Alert |

| Air Products | February 2025 | Cancelled a $500 million green hydrogen project in Massena, New York. The decision was a major blow to the U.S. hydrogen strategy and cited as evidence that the industry was ‘on life support’ due to economic and policy challenges. | E&E News |

Atome Energy’s Offtake Model, Yara International Agreement Secures $420 M (2026)

The single most critical factor for achieving green hydrogen project bankability in the current market is a long-term, binding offtake agreement, which provides the revenue certainty required to secure non-recourse project financing. Atome Energy’s success with its Villeta project serves as the definitive blueprint, demonstrating how a commercially-driven approach can succeed where subsidy-dependent models are failing.

Global vs. Local Supply Models

This diagram illustrates the global supply chain model—producing hydrogen in a renewable-rich region for export—which perfectly matches the Atome Energy/Yara strategy discussed in the section.

(Source: ScienceDirect.com)

- The commercial foundation of the Villeta project is a long-term, take-or-pay offtake agreement with Yara International, one of the world’s largest fertilizer companies. This contract guarantees revenue and insulates the project from commodity price volatility.

- This guaranteed revenue stream was the key that unlocked project financing, enabling Atome Energy to secure a $420 million debt package in March 2026.

- A significant portion of this financing, a $94.8 million investment from FMO, the Dutch entrepreneurial development bank, underscores the project’s bankability with development finance institutions that prioritize commercial soundness over speculative, subsidy-backed ventures.

- This offtake-led model directly solves the “chicken-and-egg” problem plaguing the U.S. market, where developers struggle to sign offtake agreements without subsidy certainty, and offtakers are unwilling to commit without price guarantees.

Table: Key Partnerships in Green Hydrogen Development

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Atome Energy & Yara International | March 2026 | A long-term, take-or-pay offtake agreement for green fertilizer produced at the Villeta facility. This agreement provided the revenue certainty needed to secure $420 million in debt financing. | FMO |

| U.S. DOE Hydrogen Hubs & Private Partners (e.g., Exxon Mobil) | 2023 – Present | The DOE selected seven hubs with numerous private partners to receive $7 billion in federal funding to catalyze regional hydrogen economies. However, their progress is now stalled due to the repeal of the 45 V credit, which was the central economic assumption for these partnerships. | RTO Insider |

Paraguay vs. United States, Atome Energy Proves Subsidy-Free Model Viability

The geographic focus for viable green hydrogen development has shifted from large economies with ambitious subsidy programs to regions that offer the core fundamentals of low-cost renewable energy and policy stability. The contrast between Paraguay, where Atome Energy’s project is advancing, and the United States, where the market is paralyzed, illustrates that resource advantages and a stable commercial framework now outweigh the promise of government funding.

Timeline of US Hydrogen Promotion Acts

This timeline details the US federal acts that created the subsidy-dependent model, providing essential context for the section’s critique of that approach in contrast to Paraguay’s.

(Source: ScienceDirect.com)

- Between 2021 and 2024, the United States was seen as a premier destination for green hydrogen investment, driven by the powerful incentives in the Inflation Reduction Act.

- From 2025 to today, the U.S. has become a high-risk market due to the policy whiplash from the OBBBA, which effectively destroyed the long-term business case for projects dependent on the 45 V tax credit.

- In contrast, Paraguay’s advantage lies in its abundant and low-cost baseload hydroelectric power. This structural benefit allows projects like Villeta to achieve a competitive Levelized Cost of Hydrogen (LCOH) without needing government production subsidies.

- This divergence confirms that for developers and investors in 2026, the most attractive locations are those offering intrinsic economic advantages rather than those reliant on politically vulnerable incentive schemes.

Electrolyzer Supply, Atome Energy’s 145 MW Project Highlights a Demand Problem

The primary constraint on green hydrogen growth in 2026 is not a lack of technology or manufacturing capacity, but a severe shortage of bankable projects ready to place equipment orders. While electrolyzer manufacturers like Thyssenkrupp have scaled up production, the demand side of the equation has failed to materialize due to the financing and policy hurdles stalling project development.

Green Hydrogen Production System Schematic

This schematic shows the role of the electrolyzer in the production chain, clarifying the specific technology component that is facing a demand problem, not a supply problem.

(Source: ScienceDirect.com)

- Global electrolyzer manufacturing capacity reached an estimated 25 GW per year as of March 2026, a significant increase from the roughly 8 GW per year available in mid-2024.

- Despite this nameplate capacity, utilization across Western electrolyzer producers remains at a low 10–20%. This gap is a direct indicator of the “valley of death” between project announcements and final investment decisions.

- Core technologies, including Alkaline Water Electrolysis (AWE) and Proton Exchange Membrane (PEM) electrolysis, are at a high Technology Readiness Level (TRL), with multiple large-scale demonstrations validating their performance.

- Atome Energy’s 145 MW Villeta project, having reached FID, is one of the few large-scale developments now moving toward equipment procurement, highlighting that the real bottleneck is commercial and financial, not technical. Even major players like Plug Power have had to axe projects due to these challenges.

SWOT Analysis, Atome Energy’s Model vs. US Subsidy-Dependent Path

The strategic divergence between subsidy-free and subsidy-dependent development models reveals a clear trade-off for investors and developers, balancing commercial resilience against extreme exposure to political and policy risk. The events of 2025 and 2026 have validated the strengths of the offtake-led model while exposing the fundamental weaknesses of relying on government incentives.

The Green Hydrogen Value Chain

This infographic outlines the key components of the hydrogen economy—from materials to policy and end-use—providing a holistic framework for the detailed SWOT analysis that follows.

(Source: ScienceDirect.com)

Table: SWOT Analysis for Green Hydrogen Development Models

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | U.S. Model: Massive government backing via IRA’s $3/kg tax credit promised strong returns and market creation. | Atome Model: Bankability based on a long-term, take-or-pay offtake agreement with a creditworthy partner (Yara International). | The strength of commercial contracts was validated as a more resilient foundation for bankability than government promises. |

| Weakness | Atome Model: Higher perceived sovereign risk and reliance on securing a single, large offtaker. | U.S. Model: Extreme dependence on the 45 V credit, which created a single point of failure for the entire business case. | The weakness of policy dependence was validated when the OBBBA’s passage in July 2025 created a “subsidy cliff, ” freezing the U.S. market. |

| Opportunity | U.S. Model: Opportunity to build a massive, nationwide hydrogen economy with public funding de-risking infrastructure. | Atome Model: Ability to replicate the model in any region with low-cost renewable resources, bypassing policy gridlock. | The opportunity for the subsidy-free model expanded as developers seek jurisdictions with resource advantages and policy stability. |

| Threat | Both Models: The “chicken-and-egg” problem of securing offtake before financing was a universal threat. | U.S. Model: Realized political threat of a new administration repealing or modifying critical clean energy incentives. | The threat of policy reversal became a reality for the U.S. model, while the Atome model mitigated its primary threat by successfully closing the offtake-financing loop. |

$420 M Secured, Atome Energy’s Model Signals an Offtake-First Future

Looking ahead, the most viable path for green hydrogen development will be a bottom-up, commercially-driven approach that prioritizes securing binding offtake agreements as the first and most critical step. The “if they sign, we will build” philosophy, proven by Atome Energy, will replace the speculative “if we build it, they will come” strategy that has stalled.

Hydrogen Engine Market Growth Forecast

This chart’s forecast of a rapidly growing hydrogen engine market validates the article’s concluding ‘offtake-first’ strategy by demonstrating strong future demand for hydrogen end-use applications.

(Source: Future Market Insights)

- If the current policy uncertainty in the United States persists, watch for a continued exodus of capital and project development activity towards regions with clear resource advantages and stable commercial frameworks, such as South America and parts of the Middle East.

- Within the U.S., a frantic “dash for dirt” could occur as a small number of well-positioned projects rush to begin construction before the 2027 deadline to grandfather themselves into the 45 V tax credit. Most other projects associated with the DOE Hubs will likely be formally cancelled or postponed indefinitely.

- Expect developers to increasingly pivot away from selling gaseous hydrogen and instead pursue vertical integration into more valuable and transportable derivatives with established markets, such as green ammonia for fertilizers (Atome/Yara) or green methanol for shipping.